1. Main points

The unemployment rate dropped to 4.7% in the 3 months to January 2017, from 5.1% a year earlier; it has not been lower since June to August 1975.

The rate of wage growth slowed in the 3 months to January 2017; adjusted for inflation, average weekly earnings grew at their slowest rate since November 2014.

The number of vacancies remained broadly unchanged.

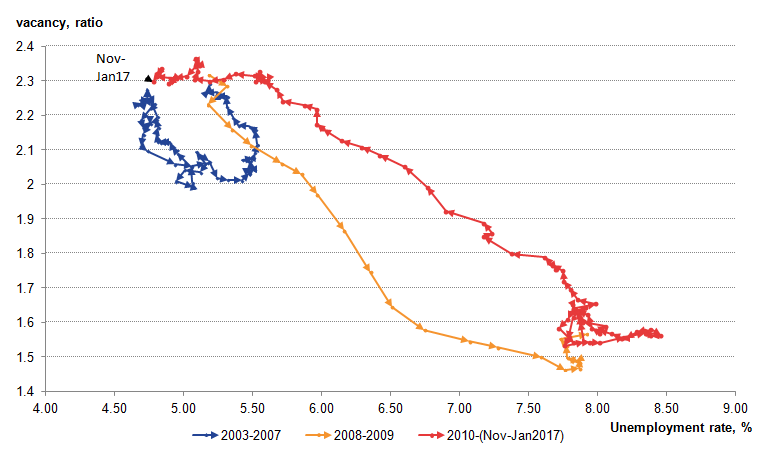

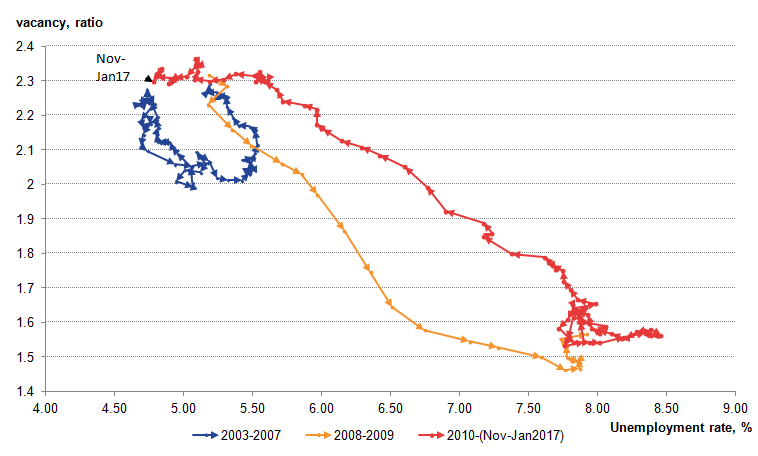

There appears to be a marked improvement in the matching efficiency of jobs to workers since the downturn, as suggested by the Beveridge curve.

2. UK unemployment rate drops to its equal lowest in over 4 decades

The number of people in work increased by 92,000 in the 3 months to January 2017 to 31.85 million, with an increase in full-time employment (a rise of 136,000) partly offset by a fall in part-time employment (a fall of 44,000). Consistent with mostly continuous employment gains, the unemployment rate dropped to 4.7% in the 3 months ending January 2017, down from 5.1% a year earlier (Figure 1). It has not been lower since the 3 months ending August 1975.

Figure 1: Quarterly change in employment ('000) and unemployment rate (%)

UK, seasonally adjusted, Nov to Jan 2009 to Nov to Jan 2017

Source: Office for National Statistics, Labour Force Survey

Download this chart Figure 1: Quarterly change in employment ('000) and unemployment rate (%)

Image .csv .xlsThe drop in the unemployment rate occurred alongside a slight increase in both the activity rate (the proportion of people aged between 16 and 64 who were economically active) to 78.4%, and the participation rate (the proportion of people aged over 16 who were economically active) to 63.6% in the 3 months to January 2017. Similarly, the employment rate remained at a record high of 74.6%, while the ratio of redundancies to employment remains at a low level compared to historical averages. The number of vacancies has remained relatively steady since early 2015 after rising strongly over 2012 to 2014.

Nôl i'r tabl cynnwys3. Rate of wage growth slows

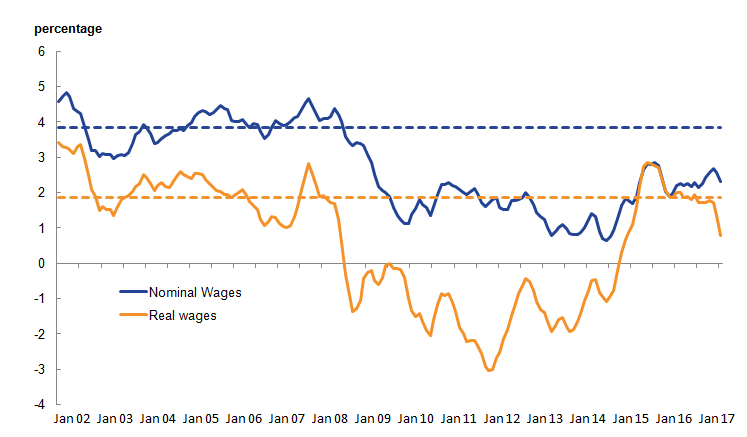

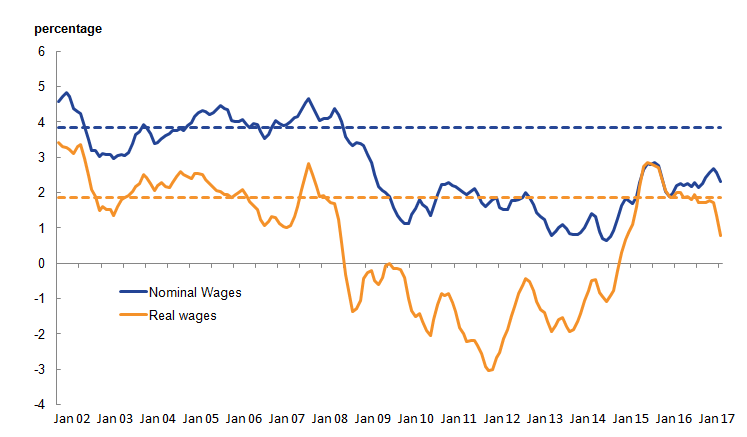

Despite indications of strength in labour market activity, the rate of wage growth slowed in the 3 months to January 2017. Nominal average weekly earnings for employees in Great Britain increased by 2.2% including bonuses in January 2017, and by 2.3% excluding bonuses compared with a year earlier. The rate including bonuses is the weakest since April 2016, while the rate excluding bonuses is the weakest since August 2016.

Recent movements in nominal wages are occurring alongside a pick-up in consumer price inflation. Adjusted for inflation, average weekly earnings increased by 0.7% including bonuses, and by 0.8% excluding bonuses, compared with a year earlier. This is the weakest growth in real earnings since November 2014.

Figure 2: Regular average weekly earnings growth: real and nominal

UK, seasonally adjusted, 3 month on 3 month a year ago, Jan 2002 to Jan 2017.

Source: Office for National Statistics, Labour Force Survey

Notes:

- Dashed lines indicate pre-crisis averages (calculated over 2002 to 2007)

Download this image Figure 2: Regular average weekly earnings growth: real and nominal

.png (32.1 kB) .xlsx (20.2 kB){kind=link}

4. Recent trends in vacancies

One key indicator of strength in the labour market is the number of vacancies, which has remained relatively steady since early 2015 after rising strongly over 2012 to 2014.

Vacancies remained broadly unchanged in the 3 months to February 2017. Figure 3 shows the percentage change in vacancy levels for the 3 months, compared to the previous overlapping three months, broken down by 3 major sectors of the economy – production, construction, and services. Manufacturing, which represents around 7% of vacancies, is included in the production series.

Figure 3: Contribution to change in vacancy level by sector

UK, seasonally adjusted, 3 months on (overlapping) 3 months, Dec to Feb 2002 to Dec to Feb 2017

Source: Office for National Statistics, Vacancy survey

Notes:

- Total vacancies exclude agriculture, forestry and fishing.

- Services are defined as industry sectors G to S.

- Production sectors include Mining and quarrying (B), Manufacturing (C), Electricity, gas and air conditioning supply (D), and Water supply, sewerage and waste activities (E).

Download this chart Figure 3: Contribution to change in vacancy level by sector

Image .csv .xlsThese data show that the services sector contributes the majority of the percentage change in vacancies each quarter, with a much smaller share accounted for by changes in production and construction vacancies.

The impact of the economic downturn between 2008 and 2009 can be clearly seen, with a 14% fall in vacancies between the third (July to September) and fourth (October to December) quarters of 2008. Vacancy growth has been broadly positive since early 2012, coinciding with a rising UK employment rate.

Since April to June 2015, vacancy growth has been erratic. However, it has been less volatile than the period following the downturn. December to February 2017 saw a rise in overall vacancies, driven by a rise in vacancies in the services and construction sectors.

Nôl i'r tabl cynnwys5. Relationship between vacancies and unemployment

In recent years, various indicators point to a tightening in labour market conditions. One measure of labour market tightness is the ratio of unemployment to vacancies (Figure 4), giving an indicator of both the demand and supply for labour and job competition.

During the period from 2002 to 2007, the unemployment-to-vacancy ratio averaged 2.5 and deviated from this average by no more than plus or minus 0.4 points throughout this period. Given that the consistency of this ratio pre-downturn was also in line with the relatively stable unemployment rate at a time when there was little slack in the labour market, the average over this period is a potential benchmark for tightness in the labour market. The ratio more than doubled to reach 5.7 at the start of the economic downturn, indicating an opening up of labour market slack and higher competition for vacancies. The ratio remained relatively high compared with before the downturn during 2009 and 2010 then began to steadily fall towards the end of 2011. This coincided with the start of the fall in the unemployment rate, when the labour market began to show signs of improvement for those both in work and looking for work.

Figure 4: Unemployment-to-vacancy ratio and its 2002 to 2007 average

UK, seasonally adjusted, ratio, Nov to Jan 2002 to Nov to Jan 2017

Source: Office for National Statistics, Labour Force Survey, Vacancy Survey

Download this chart Figure 4: Unemployment-to-vacancy ratio and its 2002 to 2007 average

Image .csv .xlsIn mid-2015, the unemployment-to-vacancy ratio dipped below its 2002 to 2007 average for the first time since mid-2008, reflecting both falling unemployment numbers and rising vacancies for several years. It has more recently reached 2.1 in the 3 months to January 2017 – its lowest level since November to January 2005.

Figure 5 plots the vacancy rate against the unemployment rate over time, creating a Beveridge curve1. For most of the period before 2008, the Beveridge curve remained in a relatively narrow band with the economy moving up and down the curve, which may indicate economic stability. During the economic downturn in 2008 and 2009, firms no longer found it profitable to hold onto staff or open vacancies. As a result, the unemployment rate increased and the vacancy rate decreased, causing a movement down the Beveridge curve.

The apparent outward shift in the Beveridge curve after the downturn may be a temporary cyclical change due to frictions in the labour market. The most recent data points indicate a leftward shift in the Beveridge curve back to pre-downturn positions with historically low unemployment and relatively high vacancy rates.

Figure 5: UK Beveridge curve: vacancy and unemployment rate

UK, seasonally adjusted, percentage, Jan to March 2003 to Nov to Jan 2017

Source: Office for National Statistics, Labour Force Survey, Vacancy Survey

Notes:

- The Beveridge curve is a graphical representation of the relationship between job vacancies and the unemployment rate.

- The search and matching model assumes that the level of vacancies corresponds to labour demand over time. This correspondence may be distorted by shifts in the cost of recruitment advertising, among other factors.

Download this image Figure 5: UK Beveridge curve: vacancy and unemployment rate

.png (26.9 kB) .xlsx (17.0 kB){kind=link}

This may be caused by an improvement in matching efficiency compared to the 2008 to 2009 downturn period. If firms are opening fewer vacancies because they are content with recent matches and the skills workers offer, then this will coincide with a downward shift in the Beveridge curve. Demand conditions will then affect future movements along a slightly tighter Beveridge curve if this is established over time.

Nôl i'r tabl cynnwys