1. Main points

The number of people in employment increased by 24,000 to 32.80 million in the three months to October 2019 compared with the previous quarter, with the employment rate reaching a record high of 76.2%.

The unemployment rate for women fell to a record low of 3.5%.

Self-employment was associated with longer working hours (of over 45 hours a week) for all workers.

Real regular pay was 0.2% lower than the pre-downturn peak reached in April 2008, and real total pay was 4.3% lower than the pre-downturn peak reached in February 2008.

Since 1971, the Phillips curve shifted down and to the left and has become flatter.

2. Overview of the UK labour market

The UK labour market has remained relatively tight. In the period August to October 2019, employment, unemployment and economic inactivity rates were largely unchanged compared with the preceding three months. Employment and economic inactivity levels increased while unemployment decreased.

The Bank of England’s latest Monetary Policy Report (MPR) stated that the unemployment rate of 3.9% in the three months to August 2019 was below the Bank’s estimate of the equilibrium unemployment rate of 4.5%. The MPR concluded that although the labour market appeared to remain tight, it “did not appear to be tightening further, however, with official and survey measures of employment growth having softened.”

The tight labour market was also highlighted by the latest KPMG and Recruitment and Employment Confederation (REC) UK Report on Jobs, which reported that recruitment to permanent posts fell in November because of uncertainty linked to the elections and to Brexit. The report indicated that candidate numbers decreased sharply while demand for workers remained weak. The latest Vacancy Survey data show that vacancies reduced by 18,000 to 800,000 in the three months to October 2019 and by 20,000 to 794,000 in the three months to November.

Another survey, the IHS Markit/CIPS UK Manufacturing PMI report, stated that manufacturing output, new orders and employment all fell in November. The CIPS Purchasing Managers’ Index fell from 49.6 in October to 48.9 in November, which was the seventh consecutive time that the index was below 50, indicating persistent contraction. Firms continued to destock following the postponement of the UK’s exit from the EU. Further, the UK Services PMI Business Activity Index fell from 50 in October to 49.3 in November, signalling a reduction in activity, although staffing numbers stabilised.

UK productivity remained below its pre-downturn level, partly because of weakness in investment and uncertainty about the future trade relationship with the EU. The MPR stated that the weak productivity growth together with faster pay growth increased unit labour costs and firms absorbed the higher costs in their profit margins rather than passing the costs to consumers.

Nôl i'r tabl cynnwys3. Latest labour market estimates

Employment

The number of people in employment increased by 24,000 (or 0.1%) on the quarter to 32.80 million in the three months to October 2019. The employment rate reached a record high of 76.2%.

Employment growth slowed in 2019 compared with previous years. Figure 1 shows employment growth since the period January to March 2014. It shows that employment growth weakened between January and October 2019 (except in the period April to June).

Figure 1: Quarterly employment growth has been weakening since the beginning of 2019

Quarterly employment growth, UK, seasonally adjusted, January to March 2014 to August to October 2019

Source: Office for National Statistics – Labour Force Survey

Download this chart Figure 1: Quarterly employment growth has been weakening since the beginning of 2019

Image .csv .xlsSlowing employment growth was partly a result of fewer workers being available for work and historically low unemployment levels. The Bank of England suggested it was also partly a result of uncertainty in the economy.

The quarterly increase in employment was driven by men

The increase in the level of employment was driven by the number of employed men, which increased by 54,000 (or 0.3%) on the quarter to 17.31 million. The number of employed women fell by 30,000 (or -0.2%) to 15.49 million over the same period.

As discussed in our labour market economic commentaries for August 2019 and for September 2019, this is contrary to recent trends whereby the number of women getting into employment has generally been higher than that of men. In the year to October 2019, 235,000 women became employed compared with 74,000 men. This translates to 3.2 women becoming employed for every man employed.

The strong performance of women in the labour market caused the employment gap between men and women to reduce from 2.01 million in the three months to November 2018 to 1.83 million in the three months to October 2019.

Self-employment was dominated by men

People in employment can be classified as employees or as self-employed (excluding unpaid family workers and workers in government-supported training and employment programmes). The number of self-employed workers increased by 33,000 to a record high of 4.96 million in the three months to October 2019. The quarterly increase was driven more by men (who increased by 20,000 to 3.30 million) than by women (who increased by 13,000 to 1.66 million). In the year to October 2019, self-employment increased by 182,000, which consisted of 96,000 men and 86,000 women.

The proportion of self-employed workers in total employment trended upwards, particularly since the period August to October 2005. The proportion was flat at 15.1% between January and October 2019.

Self-employed workers have, on average, greater flexibility over their working arrangements than employees. They may have more leisure time, but on average they earn less than employees. A notable feature of self-employment is that it more-than doubled among people aged 65 years and older between 2009 and 2017. The increase is partly associated with people living longer and healthier lives, making it possible for older people to remain economically active.

Our study on young people’s expectations from self-employment found that one in five young people (aged 16 to 21 years) expressed an intention to become self-employed at some point in the future. Of those aged 22 to 30 years, one-tenth become self-employed after leaving school. Young people expect high pay and leisure time from self-employment.

Self-employed workers worked longer hours than employees

Recent data on usual weekly hours of work show that self-employment is associated with longer working hours (over 45 hours a week) for all workers and among men and women. In the three months to October, 25.8% of all workers who were self-employed worked more than 45 hours a week, while 17.2% of all employees did the same.

Figure 2 shows the distribution of working hours for employees and self-employed workers in the three months to October 2019. There was a larger proportion of self-employed men (31.4%) who worked longer working hours than of women (14.9%).

Figure 2: Most employees and self-employed workers usually worked 31 to 45 hours per week

Usual weekly hours of work for self-employed workers and employees, UK, August to October 2019

Source: Office for National Statistics – Labour Force Survey

Download this chart Figure 2: Most employees and self-employed workers usually worked 31 to 45 hours per week

Image .csv .xlsFigure 2 shows that most employees and self-employed workers worked 31 to 45 hours a week. Most self-employed men (45.8%) worked 31 to 45 usual weekly hours, while most self-employed women (36.7%) worked 16 to 30 usual weekly hours.

The Organisation for Economic Co-operation and Development (OECD) defines part-time working as working 30 hours or less per week in one’s main job.1 Using this definition, we observe that in the three months to October, 60.0% of self-employed women and 22.8% of self-employed men worked part-time. Over the same period, 39.5% of female employees and 12.2% of male employees worked part-time. Most part-time workers (72.7%) did so by choice.

Overall, more women than men worked part-time, but they did so for different reasons. Men tend to work part-time either because they earn enough money from part-time employment or because they are financially secure. Women tend to work part-time because they want to spend more time with family or because they have caring responsibilities.

Unemployment

The number of unemployed people decreased by 93,000 to 1.28 million in the year to October 2019. On a quarterly basis, it fell by 13,000 in the three months to October 2019. The unemployment rate was largely unchanged at 3.8% over the same period.

The fall in the number of unemployed people was driven by women, whose unemployment reduced by 18,000 to 566,000. On a year-on-year basis, the number of unemployed women reduced by 64,000. The number of unemployed men increased by 4,000 to 715,000 on the quarter but reduced by 29,000 in the year to October.

The three months to October saw the lowest unemployment rate on record for women at 3.5%. For men, the unemployment rate was largely unchanged at 4.0%. Analysing the two rates together shows that despite equalising in the first half of 2018, there has been a growing gap between the rates, as shown in Figure 3.

Figure 3: The gap between men and women’s unemployment rates has been increasing since mid-2018

Male and female unemployment rates, UK, seasonally adjusted, September to November 2011 to August to October 2019

Source: Office for National Statistics – Labour Force Survey

Download this chart Figure 3: The gap between men and women’s unemployment rates has been increasing since mid-2018

Image .csv .xlsFigure 3 shows the widening gap between men and women’s unemployment rates. The unemployment rates for both men and women more than halved between September to November 2011 and August to October 2019, reflecting strong labour market performance seen over that period.

Comparing the unemployment rates for women in selected OECD countries between Quarter 3 (July to Sept) 2009 and Quarter 2 (Apr to June) 2019 shows that for many countries, unemployment decreased while for a few, it increased, as shown in Figure 4. The UK had a lower female unemployment rate than the OECD average in both periods.

Figure 4: The UK had a lower female unemployment rate than the OECD average in Quarter 3 2009 and Quarter 2 2019

Unemployment rates for women in selected OECD countries, Quarter 3 (July to Sept) 2009 and Quarter 2 (Apr to June) 2019

Source: OECD – Labour market statistics

Download this chart Figure 4: The UK had a lower female unemployment rate than the OECD average in Quarter 3 2009 and Quarter 2 2019

Image .csv .xlsBetween 2009 and 2019, Ireland and Poland experienced the largest decreases in female unemployment rates (of 4.9 percentage points each), followed by Germany (4.7 percentage points) and the UK (3 percentage points). Over the same period, Greece experienced the largest increase in the female unemployment rate (of 8.1 percentage points), followed by Italy (1.7 percentage points) and Norway (0.5 percentage points).

In Quarter 2 2019, the UK’s female unemployment rate was higher than the rates for Germany (2.3%), Norway (3.2%) and the Netherlands (3.4%) but lower than the rates for France (8.4%), Finland (6.3%) and Sweden (6.4%).

Economic inactivity

In the three months to October 2019, the level of economic inactivity of workers aged 16 to 64 years increased by 19,000 to 8.61 million, while the inactivity rate remained largely unchanged at 20.8%.

This increase was driven by a rise in the number of women who were economically inactive, up 42,000 to 5.27 million. The number of economically inactive men fell by 24,000 to 3.34 million. The inactivity rate for women increased by 0.2 percentage points to 25.3%, while that for men declined by 0.1 percentage points to 16.2%.

There are several categories of economically inactive people. People who were economically inactive because they were looking after family or their home fell from 2.30 million in the three months to October 2014 to a record low of 1.97 million in the three months to October 2019. This is a predominantly female category (1.73 million or 88%); much of this decline can be explained by more women being in employment.

Another category of economically inactive people is the retired. The proportion of economically inactive people who were retired fell from 14.4% in the three months to October 2014 to 13.0% in the same period in 2019. One of the reasons for the fall in the proportion is the increase in the State Pension age for women (from 60 years) in phases towards equalisation with that for men (at 65 years in November 2018). This meant that from 2010 onwards, when the regulations became effective, more women stayed in the labour market longer than previously.

Notes for: Latest labour market estimates

- The OECD definition is different from the one used in the UK Labour Force Survey (LFS), where respondents are asked to self-classify their main job as either full-time or part-time. The statistics based on the OECD definition therefore differ from those based on the LFS definition.

4. Average weekly earnings

Average weekly earnings are expressed as total average weekly pay (which includes bonus payments) or as regular average weekly pay (which excludes bonus payments). In the year to October 2019, total average weekly pay increased by 3.2% to £542 per week, and regular average weekly pay increased by 3.5% to £510 per week. The weaker growth in total pay is largely because of the unusually high bonuses that were recorded in the same period in 2018.

In real terms (that is, accounting for inflation as measured by the Consumer Prices Index including owner occupiers’ housing costs (CPIH, 2015=100)), real total pay increased by 1.5% to £502 per week and real regular pay increased by 1.8% to £472 per week.

In the year to October 2019, real regular weekly pay was £1 (or 0.2%) lower than the pre-downturn peak of £473 reached in April 2008. Over the same period, real total weekly pay was £23 (or 4.3%) lower than the pre-downturn peak of £525 reached in February 2008.

There have been differences between private and public sector earnings. In the year to October, private sector total pay increased by 3.2% to £541 per week. Public sector total pay increased by 3.1% to £547 per week over the same period. Figure 5 shows the trend of the ratio of private to public sector total earnings. It shows that in the year to October, private sector total average weekly earnings were 1.1% less than total earnings in the public sector.

Figure 5: Private sector total average weekly earnings were 1.1% less than total earnings in the public sector in the year to October

Ratio of private to public sector total average weekly earnings, Great Britain, seasonally adjusted, January 2000 to October 2019

Source: Office for National Statistics – Monthly Wages and Salaries Survey

Download this chart Figure 5: Private sector total average weekly earnings were 1.1% less than total earnings in the public sector in the year to October

Image .csv .xlsFigure 5 shows that the private sector total average weekly pay increased strongly relative to the public sector pay from 2012 onwards. This reduced the total pay gap between the two sectors.

Nôl i'r tabl cynnwys5. The UK’s Phillips curve

The UK employment rate increased from an average of 70.4% in 2010 to a record high of 76.2% in the period August to October 2019. The increase in the employment rate was associated with a falling unemployment rate; this was reduced to a historically low rate of 3.8% (in the period January to March 2019) last reached in the period November 1974 to January 1975. Economists like Bell and Blanchflower have questioned whether the economy has now reached full employment or not. Others question if the historically low rate of unemployment will not result in increasing wage inflation, as predicted by the Phillips curve relationship.

The Phillips curve is an economic concept developed by A.W. Phillips (1958)1 stating that inflation and unemployment have a stable and inverse relationship. It traces the average relationship between pay growth and the equilibrium in the labour market over a business cycle (that is, the balance between the demand for labour and the supply of labour, with the associated level of unemployment). It suggests that low unemployment is associated with high wage inflation and vice versa.

The study of the Phillips curve is interesting because currently, UK unemployment is at historically low levels and wage growth is relatively low compared with the period before the economic downturn. This means the trade-off between wage growth and the unemployment rate implied by the Phillips curve analysis appears not supported by the most recent period data.

The Phillips curve has been influential in the monetary policy frameworks of central banks. For instance, the US Federal Reserve uses it in deciding the interest rate policy. The Bank of England considers the Phillips curve in its monetary policy framework. In a 2014 speech, the Bank of England considered the Phillips curve stable. Three years later, in another speech in November 2017, the Bank of England queried if the relationship between wages and unemployment had disappeared in the most recent period (that is, moved lower and flatter over time). The flattening of the Phillips curve caused the Bank of England to use a variant formulation of the Phillips curve relationship by replacing the unemployment rate with the output gap (that is, the difference between actual and potential gross domestic product (GDP)).

The trends of wage growth and the unemployment rate

The period 1971 to 1992 saw periods of high nominal wage growth, reaching a peak of 32.2% between December 1974 and February 1975 and of 21.8% between August and October 1980. Wage growth declined from the 1980s onwards, but it reached a peak of 10.6% between June and August 1990. Between 1971 and 1979, the unemployment rate averaged 4.7%, but it reached a peak of 5.7% between July 1977 and January 1978. Between 1980 and 1992, it averaged 9.7% but reached a peak of 11.9% between February and June 1984.

Between 1993 and 2007, the economy was relatively stable and was characterised by inflation targeting from October 1992. Between 2008 and 2019, the economy was recovering from the impacts of the 2008 to 2009 economic downturn.

Between 2011 and 2013, there was a pay freeze in the public sector. From 2013 to 2018, pay awards were capped at 1%. As a result, nominal wages were largely insensitive to falling unemployment, resulting in low inflationary pressure. During that period, wage growth remained below its pre-downturn average rate (of 4.8% between 2006 and 2007). The trends of pay growth and the unemployment rate are shown in Figure 6.

Figure 6: The trends of the unemployment rate and average wage growth tended to move in opposite directions

Unemployment and wage growth rates, seasonally adjusted, January to March 1971 to August to October 2019

Source: Office for National Statistics - Labour Force Survey and Monthly Wages and Salaries Survey

Download this chart Figure 6: The trends of the unemployment rate and average wage growth tended to move in opposite directions

Image .csv .xlsThe two series moved counter-cyclically to each other. Between 1971 and 1992, the correlation coefficient was -0.62. Between 1993 and 2007, the correlation coefficient was -0.46. Between 2008 and 2019, it was -0.54.

The correlation coefficients indicate strong negative relationships in the relative movements of the two variables in the three periods. The negative correlations are generalised by the wage Phillips curve. Over time, both the unemployment rate and average wage growth have become less volatile. This may be linked to stabilising inflation expectations in the economy since the introduction of inflation targeting in 1992.

The UK Phillips curve has shifted to the left and became flatter

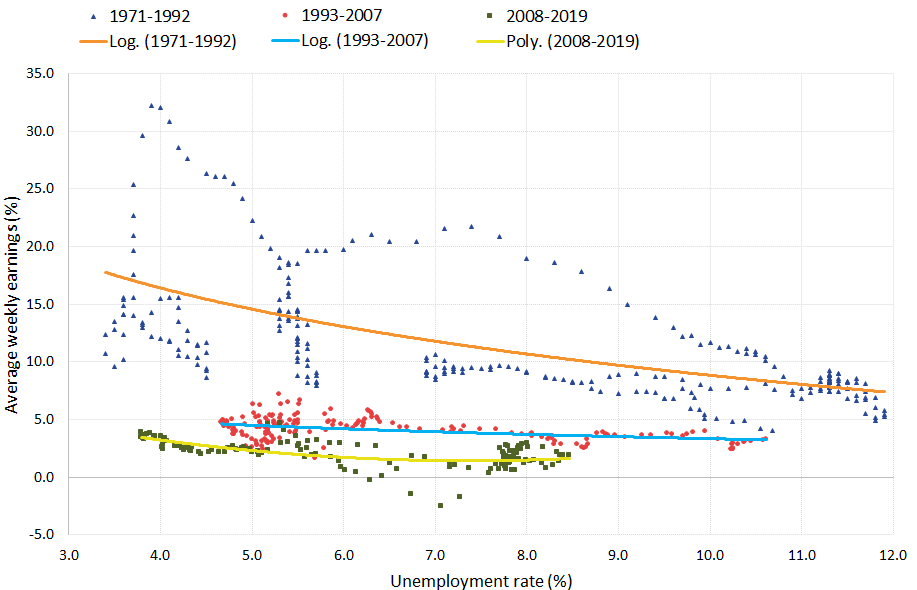

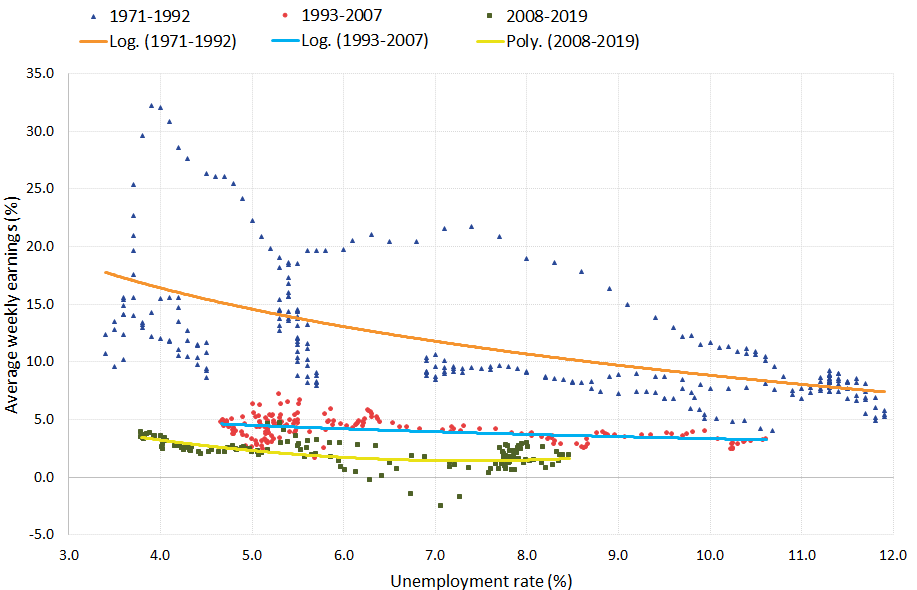

The relationship between wage growth and the unemployment rate can be illustrated with the wage Phillips curve. Since the Phillips curve relationship has changed over time, a common approach is to divide the analysis by grouping together years that were characterised by similar economic conditions. The period between 1971 and 2019 can be divided into three phases: 1971 to 1992, 1993 to 2007, and 2008 to 2019. Three Phillips curve relationships are therefore produced as shown in Figure 7.

Figure 7: The Phillips curve has been shifting down and to the left over time

Phillips curves, UK, 1971 to 2019

Source: Office for National Statistics - Labour Force Survey and Monthly Wages and Salaries Survey

Notes:

- Log. = Logarithm. A logarithmic function is a function that is the inverse of an exponential function.

- Poly. = Polynomial function. A polynomial function is an expression of more than two algebraic terms, especially the sum of several terms that contain different powers of the same variable(s).

Download this image Figure 7: The Phillips curve has been shifting down and to the left over time

.png (43.0 kB) .xls (75.8 kB){kind=link}

The Phillips curve can shift upwards and downwards, depending on the combinations of wage growth and unemployment. The slope of the curve shows the speed of wage adjustment to a change in unemployment. From 2008 onwards, low wage growth does not seem to have contributed to inflation.

Figure 7 shows that the Phillips curve shifted down and to the left and that it became flatter. The Phillips curves got flatter over time mainly because of low wage growth. Comparing the 1993 to 2007 and 2008 to 2019 Phillips curves shows that that curve shifted downwards, indicating declining nominal wage growth with low unemployment.

Why might the Phillips curve have become flatter?

Policymakers would want to know why the Phillips curve has become flatter. There are several possible explanations for this phenomenon.

Greater credibility of monetary policy

The success of inflation targeting could mean that wage inflation became stabilised around 2% and was more stable irrespective of the unemployment rate. Greater credibility of policymakers to maintain inflation around the policy target could cause workers to believe that actual inflation would not be significantly different from the target. This could have persuaded them to lower their pay demands, dampening pay growth.

Underemployment in the economy

The Phillips curve may have flattened because spare labour market capacity in the economy exceeds that measured by unemployment. The unemployment rate does not represent all the spare labour market capacity in the economy. Economists Bell and Blanchflower argued that in the post-downturn period, the UK economy experienced elevated involuntary part-time employment and other forms of under-employment. Higher underemployment resulted in higher spare labour market capacity that firms could tap into to satisfy their demand for labour.

The existence of underutilised labour puts downward pressure on wage growth. Low wage growth is associated with a larger output gap. The economy can bring in more resources into production without generating inflationary pressures. The trend of the economic activity rate got steeper from 2011 onwards because more people joined than left the labour market. The trend of the unemployment rate got negatively steeper from that time onwards. Therefore, as more people joined the labour market, they increasingly became employed rather than unemployed, implying that unemployment could not act as a stimulus for wage growth.

Growing number of new working arrangements

There has been faster growth in alternative working arrangements since the financial downturn. Work has become less structured and less secure for some workers. Self-employment as well as flexible, part-time and zero hours contract working have increased. At the same time, there has been growth in the number of people who worked part-time and did not want to work full-time. We analysed this group of workers in our November 2019 labour market economic commentary. The proportion of temporary workers among all employees reduced from a peak of 6.5% between June and December 2014 to 5.1% between August and October 2019. However, the number of workers reporting that they were employed on zero hours contracts increased from 624,000 in the period April to June 2014 to 896,000 in the same period in 2019.

Although new working arrangements increased flexibility for workers, they reduced earnings and bargaining power, which reduced wage growth. Andy Haldane, Chief Economist at the Bank of England, argued that the growth of the “gig” economy increased the divisibility of labour, which compressed wage growth.

Figure 8 shows the indices of the proportion of self-employed workers in total employment and the proportion of part-time workers in total employment.

Figure 8: The proportion of part-time workers gradually trended downwards from 2012 onwards, and that of self-employed workers trended upwards from 2008 onwards

Proportions of self-employed workers and of part-time workers, UK, seasonally adjusted, January to March 2006 to August to October 2019

Source: Office for National Statistics – Labour Force Survey

Download this chart Figure 8: The proportion of part-time workers gradually trended downwards from 2012 onwards, and that of self-employed workers trended upwards from 2008 onwards

Image .csv .xlsAndy Haldane highlighted the impacts of self-employment and temporary work on wage growth. He stated that self-employment is associated with a wage discount of about 15% of employees, and temporary working has a wage discount of 5% to 6%. The discounts put downward pressure on wage growth.

The global flows of workers, and particularly the free movement of workers within the EU, caused the UK’s labour supply constraint to become less binding, which put downward pressure on wage growth. The same process can increase productivity and wage growth in the economy. That there was immigration and falling unemployment indicates that domestic and foreign labour were more complementary than substitutable.

The fall in the unionisation rate

Another factor associated with falling wage growth is declining unionisation in the economy. In our August 2019 labour market economic commentary, we examined the change in the unionisation rate and the trade union wage premium since 1995. Trade union membership reduced from a peak of 13.21 million in 1979 to 6.88 million in 2017, a decrease of 48%. The union wage premium for all workers reduced from 25.9% in 1995 to 7.9% in 2018. For private sector workers, it reduced from 15.3% in 1995 to 2.6% in 2018. In the public sector, the premium fell from 30.3% in 1995 to 11.6% in 2018. Overall, women have a higher trade union wage premium (15.4% in 2018) than men (3.9% in 2018).

The fall in the unionisation rate reduces the power of unions. With no union representation, collective bargaining in the workplace collapses and contracts and wage settlements become individualised. PwC argued that the shifting of the Phillips curve is partly a result of a fall in union bargaining power because employers have higher bargaining power than individual workers.

The fall in productivity growth

The low wage growth experienced since the economic downturn may be explained by low productivity growth. When productivity growth is sluggish, wage growth will also be held back. The correlation between productivity growth and wage growth was high (0.52) between 1993 and 2019. From 2008 onwards, low productivity growth weighed down on wage growth, as shown in Figure 9.

Figure 9: Slow productivity growth tended to hold back wage growth

Quarterly productivity and wage growth rates, UK, March 1993 to June 2019

Source: Office for National Statistics – Monthly Wages and Salaries Survey

Download this chart Figure 9: Slow productivity growth tended to hold back wage growth

Image .csv .xlsAlthough this observed correlation does not equate to causality, economic theory tells us that wage growth is determined by productivity growth. This is because workers are paid a portion of what they produce. Low productivity can therefore lead to low wage growth, which flattens the Phillips curve.

Digitalisation and globalisation of the value chain

Digitalisation has put some workers at high risk of some of their duties and tasks being automated in the future, replacing tasks currently done by workers with technology. Such risk makes it hard for the affected workers to bargain for higher wages as they face the prospects of being replaced with machines and of being unemployed unless they retrain into other professions.

Mark Carney, the Governor of the Bank of England, commented that the globalisation of the value chain puts pressure on workers in industries that can move their operations abroad to countries with lower labour costs. A global value chain means part of production or whole production processes can be shifted abroad. For fear of losing their jobs, workers may be persuaded to be content with lower wage settlements.

Another aspect of globalisation relates to increased labour mobility across countries and continents. Flexible migration policies increase the pool of labour from which firms can employ. This induces competition between the local labour market and the rest of the world. It creates a locally contestable labour market that causes low wage growth because local workers would not want wages to rise to a level that attracts more competition or that causes employers to prefer workers from abroad. For these reasons, international migration of workers is contentious in many countries.

The government’s response to the economic downturn

The government’s wage response during the economic downturn (2008 to 2009) may have contributed to the flattening of the Phillips curve. The government’s decision to freeze pay in the public sector (between 2011 and 2013) and to fix pay awards to 1% (between 2013 and 2018) signalled for slower wage growth in the economy. This may have caused measured private sector wage growth.

To some extent, the breakdown in the relationship between wage growth and unemployment was in part a result of the public sector wage growth limits. It may have increased risk aversion among workers who did not want to move or to lose their jobs. When workers get increasingly risk averse, they tend to reduce job-to-job movements, which reduces the pay growth associated with changing jobs.

Notes for: The UK’s Phillips curve

- Phillips, A. W. H. (1958) ‘The Relation Between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861–1957.’ Economica, n.s., 25, no. 2: 283 to 299.