Cynnwys

- Summary and structure of this guide

- Introduction to public sector finances statistics

- Concepts

- The UK fiscal framework

- Fiscal aggregates included in the public sector finances statistics

- Data sources and data quality issues

- Relationship with the national accounts and revisions to published data

- Acronyms and abbreviations

- Contact details

- Annex 1: Additional sources of statistics and complementary information on the public finances

- Annex 2: The economic cycle, output gap, and automatic stabilisers

- Annex 3: Improvements resulting from the UK Statistics Authority's assessment report and the application of its Data Quality Assurance Toolkit

- Annex 4: Asset Purchase Facility in the fiscal aggregates

1. Summary and structure of this guide

This methodological guide provides comprehensive contextual and methodological information concerning the monthly Public sector finances (PSF) statistical bulletin, which is jointly produced by the Office for National Statistics (ONS) and HM Treasury (HMT). The guide sets out the conceptual and fiscal policy context for the bulletin, identifies the main fiscal measures and details how these are derived and inter-related. Additionally, it details the data sources used to compile the monthly estimates of the fiscal position.

This guide updates and summarises the content of a range of published articles, including the previous version of the PSF methodology guide (PDF, 361KB) published in August 2012.

Section 2 introduces the bulletin and the main fiscal aggregates that it provides. It also provides summary information on a range of users and uses of PSF statistics and related data.

Section 3 explains how PSF statistics are compiled according to national accounting rules, which determine the composition and the boundaries of the public sector and the categorisation of transactions undertaken by public sector bodies. It also refers to several alternative accounting and expenditure monitoring systems that are applied to underlying data sources, such as government departments' annual financial statements.

Section 4 introduces the fiscal policy context around PSF statistics. It describes the various fiscal frameworks and targets that the current and previous governments have adopted.

Subsequent sections are structured as follows:

Section 5 outlines the main fiscal aggregates reported in the PSF bulletin and their inter-relationships

Section 6 documents the sources of the data brought together to produce the main aggregates and discusses certain data quality issues

Section 7 outlines the relationship between the public sector finances and the UK National Accounts

Section 8 lists the main acronyms and abbreviations used in this guide

Section 9 provides contact details for anyone seeking further information or to provide comments

Several annexes provide supplementary information

2. Introduction to public sector finances statistics

2.1 About the public sector finances

Public sector finance (PSF) statistics for the UK are compiled and published monthly in the Public sector finances statistical bulletin, which aims to provide users with an indication of the current state of the UK's fiscal position.

PSF statistics are published jointly by the Office for National Statistics (ONS) and HM Treasury (HMT). Details of each organisation's responsibilities and accountabilities (PDF, 154KB) are available.

The statistics in the PSF bulletin are designated as UK National Statistics, which signifies that they are produced, managed and disseminated in accordance with the Code of Practice for Statistics.

The UK Statistics Authority has a statutory duty to assess (and periodically reassess) all designated National Statistics against its Code of Practice. The Authority published an assessment report for the PSF bulletin in October 2015.

2.2 Main measures of the state of the public sector finances

While the Public sector finances (PSF) bulletin presents a wealth of data on the public finances, prominence is given to a set of main aggregate measures.

All statistical aggregates published in the bulletin are defined using national accounts concepts and rules. The Office for National Statistics (ONS) produces the UK National Accounts on an internationally comparable basis, in accordance with the System of National Accounts 2008: SNA 2008 and the European System of Accounts 2010: ESA 2010. The SNA and ESA guidelines are updated periodically and since 2014 we have compiled PSF data with reference to the most recent guidance, ESA 2010, which is supplemented by the Manual on Government Deficit and Debt (MGDD). These European texts are consistent with the United Nations System of National Accounts: SNA 2008.

The main fiscal measures reported each month in the bulletin are summarised in this section and discussed further in Section 5 of this guide.

The first seven measures or aggregates detailed in this section have figured prominently in the bulletin for several years and can be regarded as headline aggregates.

It should be noted that these seven main aggregates are all "ex-measures", which signifies that the impact or contribution of any public sector banks has been excluded from the relevant calculations. There is currently just one banking group within the public sector, NatWest Group plc (formerly known as the Royal Bank of Scotland Group), although several other banks were formerly classified to the public sector in the wake of the financial crisis that began in 2007. More details of the effects and impact of the crisis are provided in Section 4.

Public sector current budget deficit (PSCB ex)

The public sector current budget deficit (PSCB ex) is the amount by which current expenditure and depreciation on capital assets together exceed current receipts. For months or other periods in which receipts exceed current expenditure and depreciation combined, there is a PSCB surplus rather than a deficit. The deficit or surplus is calculated on an accruals basis in accordance with ESA 2010. Accrual accounting is described in more detail in Section 3.

Public sector net borrowing (PSNB ex)

Public sector net borrowing (PSNB ex) is the amount by which total spending (current expenditure plus net investment) exceeds total receipts (including net capital transfers). Many commentators refer to the level of PSNB as "the deficit". As with PSCB, measurement of PSNB is on an accruals basis consistent with ESA 2010.

Public sector net cash requirement (PSNCR ex)

The public sector net cash requirement (PSNCR ex) is a cash measure closely related to PSNB (an accrued measure). It measures the public sector's need to raise cash by, for example, issuing gilts or running down liquid assets.

Until 1998, there was a broadly equivalent cash-based measure known as the public sector borrowing requirement (PSBR). The PSNCR name was introduced in 1998 to avoid possible confusion with PSNB. The PSNCR ex provides information on the cash demands of the public sector. However, most users of the public sector finances who are interested in cash data focus their attention on the central government net cash requirement (CGNCR). This is because the CGNCR provides a better metric of the amount of gilts and Treasury Bills that the UK government needs to issue. In contrast, PSNCR ex includes cash transactions that have no direct impact on the government's financing needs.

Public sector net debt (PSND ex)

Public sector net debt (PSND ex) comprises the excess of the public sector's financial liabilities (in the form of loans, debt securities, deposit holdings and currency) over its liquid financial assets (mainly foreign exchange reserves and cash deposits), with both measured at face or nominal value. It is often presented as a percentage of gross domestic product (GDP), which makes comparisons over time and with different countries more meaningful and is derived in accordance with ESA 2010 principles.

Public sector net debt (PSND ex BoE)

Introduced in the 2016 Autumn Statement, public sector net debt excluding the Bank of England (PSND ex BoE), removes the assets and liabilities held on the BoE's balance sheet from PSND ex. In the 2022 Autumn Statement, PSND ex BoE was mandated in the Charter for Budget Responsibility: Autumn 2022.

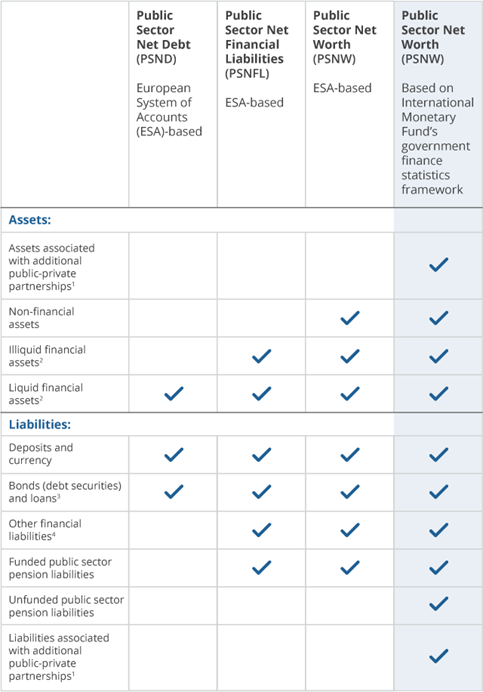

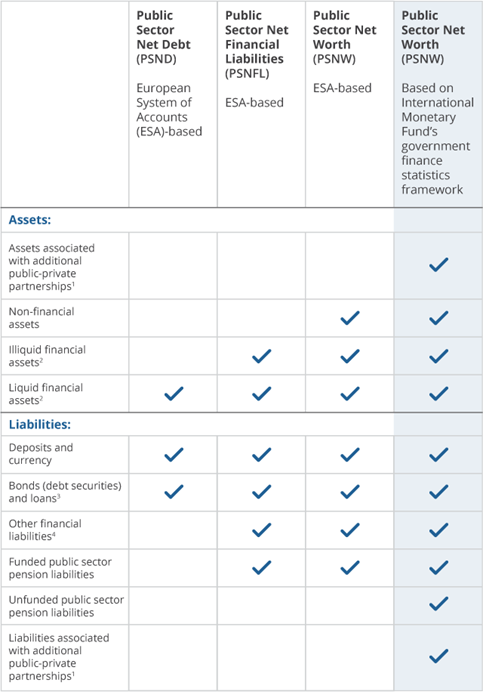

Public Sector Net Financial Liabilities (PSNFL ex)

Published for the first time in our December 2016 PSF bulletin, PSNFL ex is a broader fiscal aggregate than PSND because it includes all public sector financial assets and liabilities recognised by the national accounts. In the 2016 Autumn Statement, the UK government selected PSNFL ex as a new supplementary fiscal aggregate because it provides additional information concerning the public sector balance sheet.

Public Sector Net Worth (PSNW ex)

In April 2023, we introduced a new fiscal aggregate, public sector net worth (PSNW), in the PSF bulletin. PSNW summarises the value of both non-financial and financial assets, as well as considering the liabilities held by the public sector. It is more comprehensive than either the headline balance sheet aggregate, PSND or the supplementary aggregate, PSNFL. The new PSNW measure is on a comparable basis with existing metrics published in the PSF bulletin, but there are differences with other published versions of PSNW (explained in Section 5).

While the ex-measures are the government's preferred measures of the fiscal position and are used to set fiscal policy, the PSF bulletin also provides versions of each of the aggregates that encompass all public sector entities including public sector banks.

The composition and calculation of the aggregates introduced in this section and their inter-relationships are discussed in more detail in Section 5.

Various additional sources of official data complement the statistics provided in the PSF bulletin. Some provide more detail on components within the underlying data (such as receipts or expenditure), whilst others focus on alternative measures of the state of the public sector finances. These sources are detailed in Annex 1.

2.3 Supplementary presentation of public sector finances

In June 2019, we supplemented ESA 2010-based fiscal statistics with a dataset produced in accordance with the International Monetary Fund's Government Finance Statistics Manual (GFSM) 2014, enhancing transparency of our fiscal statistics and offering an alternative data presentation.

The Government Finance Statistics (GFS) framework described by GFSM 2014 differs marginally to ESA 2010 because of their different purposes. ESA 2010 provides guidance on the production of an integrated set of accounts for the whole economy. The GFS framework focuses on impacts of economic events on the government finances and wider public sector, in a way that allows fiscal analysis.

The addition of these GFS statistics widens the coverage and valuation basis of our fiscal statistics. They present information currently not included in the ESA 2010-based statistics, for example, unfunded pension schemes and some public-private partnerships (PPPs). The new datasets also bring together statistics that are compiled under ESA 2010, but not included in the public sector finances data, for example, contingent liabilities.

The supplementary tables we started producing in June 2019 are compliant with statements in the GFS framework, specifically, the balance sheet, statement of operations, and statement of other economic flows. Each statement contains aggregates useful for fiscal analysis, which are similar to the main public sector finances aggregates but may differ as a result of presentation or methodological differences. Table 1 lists these aggregates as well as their ESA 2010-based equivalents. More detailed explanations of the GFS framework and differences to ESA 2010 are available in a separate methodology guide.

| Statement | Aggregate | Definition | ESA 2010-based equivalent and differences |

|---|---|---|---|

| Balance Sheet | Net Worth | Total value of assets (financial and non-financial) minus total value of liabilities, measured at market value | Public sector net worth |

| Differences in coverage and valuation as net worth includes liabilities of unfunded employment-related pensions and assets associated with additional public-private partnerships, as well as valuing debt securities at market value. | |||

| Net Financial Worth | Total value of assets minus total value of liabilities, measured at market value | Public sector net financial liabilities | |

| Differences in coverage and valuation as net financial worth includes liabilities of unfunded employment-related pensions as well as valuing debt securities at market value. | |||

| Gross debt | All liabilities that are debt instruments, that is, liabilities in all financial instruments except equity and investment fund shares; and financial derivatives and employee stock options, measured at market value | Gross debt | |

| Gross debt is also presented with debt securities at nominal and face values | Differences in coverage and valuation – ESA 2010-based gross debt only includes liabilities in currency and deposits; loans; and debt securities at face value | ||

| Net debt | Gross debt minus financial assets corresponding to debt instruments | Public sector net debt | |

| Differences in coverage and valuation – public sector net debt includes only liabilities in currency and deposits; loans; and debt securities at face value, while only netting off liquid assets | |||

| Statement of operations | Gross operating balance | Revenue minus expense, when consumption of fixed capital is not included as an expense item | Saving, gross plus capital taxes |

| Differences resulting from treatment of unfunded employment-related pensions, coverage of PPPs as well as the exclusion of capital grants in Savings, gross plus capital taxes | |||

| Net operating balance | Revenue minus expense, when consumption of fixed capital is included as an expense item | Current budget deficit | |

| Differences resulting from treatment of unfunded employment-related pensions, coverage of PPPs as well as the exclusion of capital grants in current budget deficit | |||

| Net investment in non-financial assets | Acquisitions less disposals of non-financial assets | Net investment | |

| Differences resulting from the inclusion of capital grants in PSF | |||

| Net borrowing/lending | All revenue minus all expenditure (net operating balance minus net acquisition of non-financial assets) | Net borrowing/lending | |

| Differences resulting from treatment of unfunded employment-related pensions, coverage of PPPs |

Download this table Table 1: Government Finance Statistics Manual 2014 aggregates and public sector finances fiscal aggregate equivalents

.xls .csv2.4 Users and uses of public sector finances statistics and related data

Public sector finances (PSF) statistics and related data on government finances are vital inputs to the policy and forecasting work of HM Treasury (HMT) and the Bank of England (BoE), as well as the official forecasts produced by the Office for Budget Responsibility (OBR). In particular, the main fiscal aggregates introduced in Subsection 2.2 are used by HMT and OBR to monitor progress against fiscal forecasts and provide the baseline for the OBR's forecast.

The Debt Management Office (DMO) is both a supplier of data inputs and a user of public sector finance's statistics. Its responsibilities include debt and cash management for the UK government, lending to local authorities and managing certain public sector funds. It monitors main fiscal measures presented in the PSF bulletin, principally CGNCR, to inform its decisions relating to debt and cash management.

The public sector finances also provide related deficit and debt statistics to the International Monetary Fund (IMF) and the Organisation for Economic Cooperation and Development (OECD) on both an annual and quarterly basis. These organisations assess the performance of national economies and make policy recommendations to foster global growth and economic stability.

Through research and feedback, we have also been able to identify a broad range of additional users and uses of public sector finances statistics. Examples include:

UK-based research and analytical organisations such as: the Institute for Fiscal Studies (IFS) and the National Institute for Economic and Social Research (NIESR), which use the data as input into their assessments of economic performance and sustainability; and the House of Commons Library, which provides impartial information and research services for Members of Parliament and their staff in support of their parliamentary duties

members of the general public, who may use the (headline) statistics to assess UK fiscal performance and the implications for their own well-being and investment decisions

commercial analysis and research bodies, such as CEIC Data Co. Limited, FactSet and Timetric, who analyse data on behalf of their clients

news-focused media organisations, such as Thomson Reuters, Bloomberg, the Economist and the national newspapers, which use the statistics and associated commentary to deliver headlines and underlying narratives

rating agencies such as Standard and Poor's, Moody's and Fitch, which issue credit ratings for the debt of governments and both private and public corporations; additionally, they use public sector finances statistics in risk analysis to provide investment advice to clients

academics, who use data primarily for economic and financial analyses, which typically underpin articles for academic journals or other publications

3. Concepts

3.1 What is the public sector?

In economic statistics, bodies and transactions are recorded according to their economic substance, which may sometimes differ from their legal form. This means that a prerequisite for compiling fiscal statistics is to determine the composition and statistical boundary of the public sector.

The Office for National Statistics (ONS) has documented procedures to determine which entities should be classified within the public sector. We make classification decisions in accordance with the legally-binding European System of Accounts 2010: ESA 2010 and supplementary guidance, in particular the Manual on Government Deficit and Debt (MGDD). These documents set out the rules for producing national accounts and fiscal statistics.

The broad sectoral breakdown of the UK public sector published in the Public sector finances (PSF) bulletin is:

central government

local government

public corporations

The central government and local government sectors are, from an ESA 2010 perspective, subsectors of the general government sector. The public corporations sector does not directly map to a single institutional sector in ESA 2010 and instead comprises publicly-controlled entities from various subsectors of non-financial and financial corporations. For analytical purposes and to produce the main fiscal aggregates, we split public corporations into the following components:

Bank of England

public sector banking groups

public sector pension funds

other public corporations (mainly non-financial corporations)

Further information on these subsectors follows.

The central government subsector

The central government subsector includes all administrative departments of the state and other government agencies whose competence extends over the whole country, or large parts of the country. This subsector includes, amongst others, entities dealing with taxation, defence as well as public units in the health and education sectors.

Central government also includes publicly-controlled bodies with a corporate structure that are considered non-market producers for statistical purposes (in other words, bodies that do not operate like typical commercial enterprises in the market economy). NHS Trusts and Academy Schools are part of central government, as are, for example, Network Rail Limited and UK Asset Resolution Limited.

ESA 2010 specifies separate subsectors for state government and social security funds. Following a classification review, we concluded that the UK does not have any entities that fully meet the criteria for inclusion in these subsectors. For example, the state government subsector is more common under the federal structure, which is not present in the UK. Neither are the National Insurance funds sufficiently removed from the government departments to form a separate institutional sector. Bodies such as the devolved administrations and the National Insurance funds are therefore all included within the central government subsector.

The local government subsector

The local government subsector comprises administrative bodies, such as local authorities, whose competence extends only to particular localities within the economic territory of the UK. The subsector also includes the police forces, the fire and rescue forces and non-profit institutions that are under the control of a local authority or other local government body. The local authority Housing Revenue Account, which is the account that relates to most local authority-controlled housing, is excluded from the local government sector and is treated as a public corporation.

The public corporations subsector

Generally speaking, public corporations are publicly-controlled enterprises that are considered market producers for statistical purposes. This broad category includes both non-financial and financial corporations. Historically, the former had a significant impact on the public finances but this declined following the privatisations of the 1980s and early 1990s. The latter category had been less prominent historically but has since increased in size and impact.

Most changes to the composition of the sector have been caused by economic events. The financial crisis of 2007 prompted the UK government to take control of several commercial banks and building societies. Most have since been sold back to the private sector. As of 2019, NatWest Group plc is the sole remaining government-controlled bank within the public corporations subsector after Lloyds Banking Group reverted to private sector control in 2014.

The Bank of England (BoE), which fulfils the functions of a central bank, is also necessarily classified to the public corporations subsector. Data for the BoE have been presented separately within the PSF bulletin since January 2011 and comprise ONS estimates derived from the BoE's published accounts. Prior to January 2011, in the PSF bulletin data for the BoE were incorporated within time series for the entire public corporations subsector.

The changes to the international statistical framework and the associated methodological and classification decisions taken by the ONS also contributed to the evolution of the sector. For example, pension funds had not been included in the statistical boundary for the public sector until September 2019, with the liability for potential underfunding recorded in the government sector (in its capacity as employer) instead. This has changed with the transition to the gross recording of funded public pensions. The large amounts of assets and liabilities associated with funded pensions now have a very significant impact on the public sector data.

The composition of the UK public sector is illustrated in Table 2 in Section 3.2.

3.2 Sector classification

It is important to have clearly defined boundaries between the public and private sectors, and between subsectors. While a member of the EU, the UK developed comprehensive criteria for making classification decisions in conjunction with the Statistical Office of the European Union (Eurostat). Following the UK’s exit from the EU, new governance arrangements are being put in place that will support the adoption and implementation of high-quality standards for UK economic statistics. These governance arrangements will promote international comparability and add to the credibility and independence of the UK’s statistical system.

We routinely examine new units with public sector involvement to establish the appropriate statistical classification. Sometimes, we review the units that have existed for a long time and had been classified in the past. This can happen for a number of reasons, most commonly as a result of changes in governance or funding of those units (for example, a higher amount of fees collected by a body may reduce the need for grant funding and lead to a reclassification from general government to the public corporations subsector), or developments in the international statistical guidance. We therefore publish a forward work plan.

| Public sector | ||

|---|---|---|

| Public sector (excluding public sector banks) | Public sector banks | |

| General government | Public corporations | |

| Central government | Bank of England | (from March 2014 onwards, this sector consists solely of The Royal Bank of Scotland Group and its subsidiaries) |

| Local government | Other public corporations (mainly non-financial corporations) | |

| Public pension funds | ||

Download this table Table 2: Composition of the UK public sector

.xls .csv3.3 Alternative accounting systems – financial reporting versus statistical reporting

The national accounts summarise economic activity within the UK economy over a given period and enable the generation of economic indicators, such as gross domestic product (GDP). They also present information on lending and borrowing by different sectors (including households and the private sector, in addition to the public sector) in the capital account and the financial account; and the balance between assets and liabilities, termed net worth, for sectors and the UK overall, in the balance sheets account.

National accounts must be compiled in accordance with the global statistical framework, described in the United Nations' System of National Accounts 2008: SNA 2008. The UK adheres to the European version of the SNA 2008, the European System of Accounts 2010: ESA 2010, to produce the UK National Accounts. The principles underlying ESA 2010 are also applied to the production of most datasets included in the Public sector finance (PSF) bulletins, as successive UK governments have chosen to frame fiscal policy on ESA concepts.

ESA 2010 was adopted in the UK in 2014, replacing its predecessor, the European System of Accounts 1995: ESA 1995. SNA 2008 and ESA 2010 (as well as the earlier ESA 1995) are founded on the accruals approach to accounting, as are most modern business accounting standards. This means that transactions and associated claims and obligations are recorded in the period that they are agreed via formal contracts or otherwise, regardless of when payments are made.

Unlike most business-oriented accounting systems, ESA 2010 does not generally recognise accounting provisions (apart from standardised guarantees), nor contingent assets or liabilities. Nevertheless, EU Council Directive 2011/85/EU includes statistical requirements for the publication of specific contingent liabilities and other potential liabilities. We expect that some data will also be available in the Government Finance Statistics Manual (GFSM) 2014-based statistics.

Eurostat's Manual on Government Deficit and Debt (MGDD) gives supplementary guidance concerning the application and interpretation of ESA 2010 with regard to the public sector, although its primary focus is on general government.

MGDD and ESA 2010, like most modern accounting frameworks, focus primarily on economic substance rather than merely on legal form. Often, such an approach requires an analysis of which party bears the risks and rewards associated with an asset, liability, or transaction.

In addition to the main statistical datasets compiled on the basis of ESA 2010, we publish supplementary fiscal statistics based on International Monetary Fund's GFSM 2014, which is another framework derived from the SNA 2008. While mostly consistent with ESA 2010, it prescribes a different treatment for a number of economic activities such as unfunded pensions and coverage of public-private partnerships (PPPs), offering an alternative presentation of the PSF data.

Although the production of PSF statistics is consistent with ESA 2010 (or GFSM 2014), some of the underlying source data are derived from reported data on cash flows and from business-oriented accounting systems, which are discussed in this section.

Given that some accounting systems, such as ESA, are designed for statistical purposes while others focus on financial reporting, issues of non-alignment and inconsistency may arise if data produced for the latter purpose are required as inputs to statistical products. In the preparation of PSF statistics, care is taken to ensure that the source data derived from public sector accounting systems are, where necessary, transformed to achieve consistency with the statistical rules. PSF data sources and the adjustments made to transform input data into an ESA-consistent form (or GFSM-consistent in the case of the supplementary GFSM 2014-compliant statistics), are discussed in Section 6.

3.3.1 Cash management systems

The concept of cash is widely understood and accepted. Cash comprises notes and coins, together with holdings in accounts with banks or other financial institutions and can be readily accessed or transferred by electronic or other means. Cash is the quintessential liquid asset and can be used to settle any financial obligations. Other assets, be they financial or non-financial, can only be deemed to be liquid if they can easily and speedily be converted to cash with negligible impact on their value.

Tax authorities in many countries, including HM Revenue and Customs in the UK, allow small businesses to report their finances on a cash basis, as this is generally easier and less time-consuming. Cash payments are recorded when they are made or received, regardless of when the associated transactions or economic activities are undertaken. However, corporations are obliged to use accruals-based accounting systems, which are acknowledged as providing a better guide to the financial performance and position of a business than cash-based recording. Nevertheless, it is important for companies to carefully monitor cash flows to ensure that they can meet short-term financial obligations. The same is true for government.

HM Treasury (HMT) has a cash management and forecasting system, which is the primary source of monthly cash data that feed into the public sector finances and underlie some of the main statistics presented in the PSF bulletin (in particular the net cash requirement aggregates).

Another source is the Debt Management Office (DMO), which is an executive agency of HMT and is responsible for government (Exchequer) debt management and cash management. It conducts auctions of gilts to raise funds on a long-term basis and of Treasury Bills, which are a form of short-term funding (with maturities ranging from 1 to 12 months).

The DMO's debt management remit is published annually by HMT as part of the Debt Management Report. The debt management objective is "to minimise, over the long-term, the costs of meeting the government's financing needs, taking into account risk, while ensuring that debt management policy is consistent with the aims of monetary policy." Its cash management objective is to ensure that sufficient funds are always available to meet any net daily central government cash shortfall and minimise the cost of offsetting the government's net cash flows over time, within a risk framework approved by ministers. The DMO carries out market operations in light of forecasts of daily net cash flows into or out of the National Loans Fund (NLF), provided by HMT.

While the Exchequer's cash flow has a regular seasonal and monthly pattern, it is also subject to uncertainty with regards to the timing of some tax and expenditure flows. DMO achieves these net cash flow requirements for the government through a combination of bilateral dealing with market counterparties and Treasury Bill issuance. The range of instruments and operations that the DMO may use for cash management purposes is set out in its published Operational Notice.

The DMO also has operational responsibility for the Public Works Loan Board (PWLB), which is responsible for lending money from the National Loans Fund to local authorities and collecting the repayments. However, the policy framework is set by the Treasury.

In addition to its role in conducting monetary policy, the Bank of England (BoE) provides banking services for government and other financial institutions within and beyond the UK. It provides government with foreign currency accounts and payment services, securities custody and settlement services. It also acts as the DMO's settlement agent and as HMT's agent in the day-to-day management of the Exchange Equalisation Account, which holds the UK's official reserves (consisting of reserves of gold, foreign currency assets and International Monetary Fund Special Drawing Rights). Consequently, BoE is also an important supplier of monthly cash data, which relate primarily to earnings and flows.

While HMT, the DMO and BoE are the primary sources of cash data, there are various additional sources. The most significant of these are National Savings and Investments (NS&I) and UK Asset Resolution Limited (UKAR). NS&I is a government department that provides financing to government by issuing and selling retail savings and investment products to the public. UKAR is the holding company for Bradford and Bingley plc (B&B) and NRAM Limited, and is responsible for the orderly management of the closed mortgage books of both B&B and NRAM.

3.3.2 Financial reporting and business accounting

While cash data are essential to the production of monthly PSF statistics, comprehensive statistics on the state of the public finances also require the extraction of relevant data from financial reports (typically produced annually or bi-annually). For published PSF statistics, much of the required basic data is sourced from the financial reporting systems of public sector bodies, such as central government departments, local authorities, health trusts and public corporations.

These bodies maintain accounting systems for two main purposes: internal reporting (budgeting and performance measurement) and external financial reporting. For external reporting, data must conform to, or be converted into, a form that is compatible with the legally required accounting framework. For internal reporting, data may be held in more flexible forms that satisfy alternative categorisations and accounting rules.

Government departments have prepared annual accounts since 1866. Until financial year ending (FYE) 2000, the accounts were reported on a cash basis. By the late 1990s, it had become evident that the perceived advantages of cash accounting (namely the availability of timely and accurate estimates) were outweighed by some serious drawbacks. As cash measures reflect the timing of payments rather than underlying transactions, they are more prone to erratic and volatile movements. Hence, on balance, accruals-based reporting offers a better guide to the performance of individual entities and to the underlying fiscal position of the public sector than an exclusively or primarily cash-based approach.

Accruals-based accounting standards have been developed primarily as guidelines for financial reporting by private sector corporations. Consequently, when the public sector utilises such accounting standards, issues of compatibility and practical applicability may arise. Hence, financial reporting standards sometimes need to be adapted or interpreted in novel ways for use by public sector bodies.

3.3.3 The Financial Reporting Advisory Board (FRAB), and resource accounting and budgeting (RAB)

The role of ensuring that public sector financial reporting is as consistent as possible with that of the private sector is undertaken by the independent Financial Reporting Advisory Board (FRAB).

The FRAB, which was established in 1996, aims "to promote the highest possible standards in government reporting". It advises on reporting across government departments and on the implementation of public sector accounting policies. Each year the FRAB updates the Government financial reporting manual (FReM), which is the technical accounting guide for the preparation of financial statements of central government entities. The FRAB also oversees the financial reporting rules applied within the local government and health sectors. The ONS and HMT are represented on the FRAB.

The financial year ending (FYE) 1998 saw the start of major changes in public sector financial reporting in the UK with the adoption of resource accounting and budgeting (RAB), which aimed to align accounts and budgets more closely with government policy priorities and facilitate the shift to an accruals basis. Implementation was finally completed in FYE 2000.

The implementation of RAB in 1998 coincided with the adoption of the ESA 95 statistical framework for national accounts. These developments were reflected in the PSF bulletin, which gave greater prominence to accrued fiscal measures than traditional cash measures. Since 1998, governments' fiscal targets and rules have also been framed in terms of accrued measures.

3.3.4 IFRS

International Financial Reporting Standards (IFRS) are financial reporting standards developed by the International Accounting Standards Board (IASB), whose purpose is to develop and maintain a set of consistent global accounting standards. The Council of the European Union has adopted certain IASB standards. As such, EU-listed corporate groups, including banks and insurance companies, have been obliged to prepare their consolidated accounts in accordance with IFRS since 1 January 2005. IFRS was implemented and adopted for the UK private corporate sector from 1 January 2005, in accordance with EU Regulation 1606/2002 (PDF, 112KB).

FRAB has interpreted and adapted IFRS for use in the FReM and associated public sector financial reporting manuals. Central government departments adopted IFRS (via the FReM) from FYE 2010 and local government from FYE 2011. The first set of audited IFRS-based Whole of Government Accounts (WGA) was published in December 2011, for FYE 2010.

3.3.5 UK generally accepted accounting practice

UK generally accepted accounting practice (PDF, 1.6MB) (UK GAAP) represents the collected body of UK accounting standards (as issued by the UK Financial Reporting Council), supplemented by guidance published by acknowledged accounting experts. These standards were used by government departments as the basis of reporting their financial accounts on an accruals basis between FYE 2000 and FYE 2009.

3.4 Public expenditure frameworks

Over time, multiple accounting frameworks have developed to measure UK government spending. Each has been tailored to meet the requirements of one or more of the following diverse financial management purposes:

budgeting – used by HM Treasury (HMT) to control government spending and overall public expenditure

producing estimates, which are the means via which Parliamentary approval is obtained for departmental spending

monitoring the overall fiscal position by tracking the main aggregates presented in the PSF bulletin

preparing resource accounts (the annual financial accounts and reports of public sector bodies) in accordance with commercial accounting principles (IFRS) adapted for use in the public sector

producing the Whole of Government Accounts (WGA), a consolidated set of commercial accounts prepared by HMT for the whole of the public sector

HMT's budgeting system aims to control public expenditure to support the government's fiscal framework. It also seeks to provide incentives for departments to manage spending, deliver high-quality public services and offer value for money to taxpayers. Underpinning this is a measurement framework, defined by HMT and explained in detail in the consolidated budgeting guidance. The framework is in some areas aligned more closely with national accounts concepts and principles than underlying departmental resource accounts.

Government departments have separate "resource" budgets (encompassing current expenditure such as pay or procurement) and "capital" budgets (covering new investment and net policy lending). Each budget is then sub-divided into spending that scores either as departmental expenditure limits (DEL), or as annually managed expenditure (AME). DEL spending encompasses items that HMT expects departments to manage and predict quite accurately (for example, staff costs, consultancy services and most grant payments). AME comprises spending that HMT recognises is more difficult to forecast. Typically, this comprises elements that are demand-led and can be volatile, such as benefit payments and tax credits.

Each department's budget (that is, the amount available to spend) is set for a period of multiple years during the Spending Review process, in accordance with government priorities. For example, in autumn 2015, HMT carried out a Spending Review for the period from financial year ending (FYE) 2016 to FYE 2020 (and, for some departments, up to FYE 2021).

DEL totals are fixed at the review and departments may not exceed them. AME totals are necessarily more challenging to manage, so departments are expected to monitor them closely and inform HMT if spending rises significantly above forecast levels.

Government needs Parliamentary approval for departments' annual budgets. Estimates are the Parliamentary means of granting this authority. The main estimates, normally published around the start of the financial year, are the starting point of the supply procedure. In approving the estimates, Parliament grants statutory authority for the consumption of resources and capital by government, and for cash to be drawn from the Consolidated Fund (PDF, 310KB) (the government's main current account held at the Bank of England). Around January or February, new or revised estimates are presented to Parliament, updating the earlier requests for supply. These estimates are generally referred to as supplementary estimates. Once approved by Parliament, the estimates become firm expenditure limits that cannot be exceeded by departments. Extensive guidance on the production of estimates is available on the HMT website.

In the late 2000s, it became clear that the use of multiple spending frameworks was unnecessarily complex, hindering scrutiny and accountability, whilst increasing burdens and reducing efficiency. The Clear Line of Sight Project was set up to address these weaknesses through:

aligning the budgets, estimates and accounts frameworks as closely as possible

reducing the number of spending publications

bringing forward the publication of departmental financial reports and accounts by one month to June

Consequently, from FYE 2012 estimates have been produced on essentially the same basis as HMT's budgeting framework.

Nôl i'r tabl cynnwys4. The UK fiscal framework

4.1 Fiscal policy and the public sector finances statistics

While it is intended to assist a diverse range of users, the primary function of the Public sector finances (PSF) bulletin is to provide statistics that enable government and bodies such as the Office for Budget Responsibility (OBR) to monitor and analyse the UK fiscal position (that is, the state of the public finances). These analyses may in turn inform fiscal policy decisions, such as how much government should spend and how this expenditure should be financed (by taxation, by borrowing, or a combination of these). This section of the guide describes the policy context around the bulletin and the various rules and targets that have been set by successive governments in recent decades.

Fiscal policy and monetary policy are the main tools available to steer the UK economy at a macro level.

In the 2022 Autumn Budget and Spending Review, the UK Government published its Charter for Budget Responsibility: autumn 2022 update. This document presents the fiscal mandate by which its performance will be assessed, to:

- have public sector net debt (excluding the Bank of England) as a percentage of GDP falling by the fifth year of the rolling forecast period.

The fiscal mandate is supplemented a target to:

- ensure public sector net borrowing does not exceed 3% of GDP by the fifth year of the rolling forecast period

There is a further supplementary target to ensure that expenditure on welfare is contained within a predetermined cap and margin set by the Treasury. However, this target is not defined by data that are part of the ONS' public sector finance dataset.

Fiscal policy is typically complex. The same overall fiscal position could be reached using numerous and diverse policy interventions. For example, government could fund additional public spending either via increases in taxes or extra borrowing, or a combination of both. Nevertheless, governments generally aim to be transparent and stable in their conduct of fiscal policy, often working within a published framework with a specified set of overall targets.

The Charter also states an aim to strengthen over time a range of measures of the public sector balance sheet such as public sector net debt, public sector net financial liabilities and public sector net worth through effective management of assets, liabilities and risks.

Currently, the primary goal of UK monetary policy is to maintain stable prices. This involves controlling inflation by adjusting short-term interest rates. Responsibility for overseeing monetary policy was assigned to the Monetary Policy Committee (MPC) of the Bank of England (BoE) in May 1997. The MPC is operationally independent of government and each month it convenes to decide whether to adjust the Bank Rate, an important short-term interest rate, which influences interest rates charged by commercial banks and other financial institutions. Successive governments have set an inflation target for the annual increase in the Consumer Prices Index (CPI) not to exceed 2%. If this target is consistently exceeded the MPC is likely to raise the Bank Rate. The BoE's secondary monetary policy goal is to support government's other economic objectives, including those for growth and employment.

4.2 Former fiscal frameworks

4.2.1 Fiscal targets prior to 1997

For around 30 years prior to 1997, fiscal targets were generally expressed in relation to the public sector borrowing requirement (PSBR). A balanced budget had a nil PSBR. As noted in Section 2, the current equivalent of the PSBR is the public sector net cash requirement (PSNCR).

Over the course of the 1980s, governments frequently adjusted their targets for the PSBR, often aiming to reduce it over the medium-term or maintain it at modest levels. The surplus in financial year ending (FYE) 1988 (the first for nearly 20 years) prompted tax cuts and the adoption of a balanced budget as a medium-term objective.

By the early 1990s, the budget surplus had disappeared, although budget balance remained the medium-term objective. The eventual return to balance followed a period of persistent budget deficits. From a peak deficit in FYE 1994, the PSBR was reduced to around 1% of gross domestic product (GDP) in 1997 through strict fiscal control of public expenditure.

4.2.2 The golden rule and framework for fiscal policy (1997 to 2008)

In 1997, as part of its wider macroeconomic reforms, government laid out a new framework for fiscal policy (PDF, 516KB) that included delegating responsibility for monetary policy to the Bank of England (BoE) and for debt and cash management to the Debt Management Office (DMO).

The reforms were intended to alleviate the greater macroeconomic instability of the UK economy compared with other G7 countries, which had become apparent over several decades. Frequent changes to the conduct of fiscal and monetary policy had contributed to this problem.

The new framework was formally introduced at Budget 1998 with a legislated Code for Fiscal Stability, which set out main principles for fiscal management and enhanced reporting requirements. It also prescribed a new role for the National Audit Office (NAO) to audit the assumptions underpinning the public finance projections. It provided for flexibility in responding to unforeseen developments by reformulating fiscal rules and objectives.

In 1997, the government established two fiscal policy objectives with different time horizons:

over the medium-term, public finances had to be sound, and spending and taxation had to impact fairly within and between generations

over the short-term, automatic stabilisers (see Annex 2) were to be used to help smooth the path of the economy and to complement monetary policy

In 1998, the government established two fiscal rules:

the golden rule stated that over the economic cycle the government would borrow only to invest and not to fund current spending

the sustainable investment rule stated that public sector net debt (PSND) as a proportion of GDP would be held at a stable and prudent level over the economic cycle; other things being equal, net debt would not exceed 40% of GDP over the course of the economic cycle

In practice, conformance to the golden rule requires a public sector current budget (PSCB) balance or surplus over the duration of the economic cycle. The sustainable investment rule, when applied in conjunction with the golden rule, imposes constraints on levels of capital expenditure by the public sector.

An assessment by HMT in 2008 judged that the government had met its fiscal rules over the economic cycle that had begun in FYE 1998 and had concluded in FYE 2007.

4.2.3 The financial crisis and the introduction, and subsequent modification, of PSF measures excluding financial interventions (2008)

The onset of the financial crisis and associated shocks that began to hit the UK economy in financial year ending (FYE) 2008 led the government to make exceptional interventions in the financial sector. This included taking control of several commercial banks. The Chancellor, in a lecture delivered in November 2008 (PDF, 2.1MB), signalled that the government would temporarily depart from the fiscal rules, asserting that "to apply these rules rigidly in today's changed conditions would be perverse."

New concepts and aggregates for measuring the fiscal position were introduced in the PSF bulletin around this time. These comprised measures of public sector net debt (PSND) and public sector net borrowing (PSNB) that excluded the temporary impacts of financial interventions. These so-called ex-measures were typically abbreviated to PSND ex and PSNB ex respectively.

The rationale for this change in focus was that the conventional measures would be distorted by the impacts of these interventions and would not reflect the true, underlying position of the public finances (given that government's intention was to eventually return control of the banks to the private sector and terminate other special schemes supporting the financial system). Since August 2008 in the case of PSND ex and since December 2009 for PSNB ex, the ex-measures have been reported alongside their longer-established and fully inclusive counterparts in the PSF bulletin.

The 2010 article, Public sector finances excluding financial interventions (PDF, 167KB), explained the underlying rationale and policy context for the ex-measures and how they were derived. Since 2009, the aggregates used for setting fiscal targets have been ex-measures. However, as explained in this section, the definitions of PSNB ex and PSND ex were modified in 2014.

The initial intervention in financial markets that prompted the introduction of the ex-measures was the taking into temporary public ownership of Northern Rock in October 2007. This was triggered by Northern Rock's precarious financial state, which had obliged it to seek emergency funding from the BoE, precipitating the first run on a British bank in more than a century. The ONS Classification Committee ruled that the public sector had the power to control Northern Rock's corporate policy and consequently it was classified as a public financial corporation for national accounts and PSF purposes.

Northern Rock's gross liabilities (net of liquid assets) increased PSND from the point of its entry into the public sector. As the government's stated intention was to return Northern Rock to private ownership, Northern Rock's finances were excluded from the public sector, for the purposes of calculating the ex-measures. This meant that Northern Rock's debt was excluded from PSND ex and its transactions with the private sector were excluded from PSNB ex. Furthermore, it implied that government's transactions with Northern Rock would affect PSNB ex.

The same rationale and methodology was applied to subsequent interventions relating to other public sector banks, including Bradford and Bingley, Lloyds Banking Group and the Royal Bank of Scotland Group (now known as the NatWest Group plc), each of which was taken under government control. The impacts of certain additional interventions were also initially excluded from the ex-measures.

These interventions principally comprised the establishment of the Asset Purchase Facility (APF) and the Special Liquidity Scheme (PDF, 89KB) (SLS). These schemes were designed to underpin the financial sector, improving liquidity and strengthening banks' balance sheets, and were operated by the BoE. The SLS allowed banks to swap illiquid mortgage-backed and other securities for specially issued Treasury Bills. The APF was the body set up to carry out the BoE's quantitative easing scheme, mainly by purchasing gilts financed by a loan from the BoE, created by increasing reserves. They were not intended to have extended lifespans and hence they could be regarded as temporary. The SLS was established in 2008 and terminated in 2012, but the APF which was set up in January 2009 is still functioning.

Annex 4: Asset Purchase Facility in the fiscal aggregates, presents further information on the recording of the APF scheme within the public sector finances.

The APF was established as a wholly-owned subsidiary of the BoE. It is fully indemnified by HM Treasury (HMT): any financial losses resulting from the asset purchases are borne by HMT and any gains are owed to HMT.

Originally, it was envisaged that payments due to or from HMT would be settled when the scheme ended. But the scale and likely duration of the scheme were extended and, in November 2012, HMT announced changes to the cash management arrangements for the APF. This provided for cash surpluses held in the APF to be transferred to HMT on a quarterly basis. Initially these changes did not impact on the treatment of the APF in the ex-measures. However following a UK Statistics Authority review (PDF, 473KB) of the treatment of the transactions, and an Office for National Statistics (ONS) consultation exercise (PDF, 192KB) and review (PDF, 129KB) of the ex-measures, the ONS decided in 2014 that only public sector banks would be excluded from the ex-measures.

As part of the consultation and review, the ONS developed the following principles to inform the composition of the current (and any future) ex-measures. The ONS concluded that they should:

Be as inclusive as possible, whilst avoiding manifest distortions (such as, for example, those from public sector banks) so that they:

- ensure that the full range of public sector liabilities (on a national accounts basis) are reported as transparently as possible

- do not intrinsically create one-off factors in their design without justification; the previous method of excluding some indemnified schemes until they came to an end when there was a balancing transaction intrinsically creates one-off transactions, these can then cause further issues for users in assessing underlying trends; for example, when the Special Liquidity Scheme ended there was a one-off impact on net borrowing of £2.3 billion

- allow transactions or classifications to be excluded if they create distortions that clearly impair the understanding of public sector finances because of their size and their lack of correlation with their effects on the government's need to issue gilts

Be consistent in their effect on debt and borrowing.

Respect the building block for national accounts: the institutional unit (institutional units have autonomy of decision-making and file their accounts); this means that any ex-measures should not sub-divide institutional units.

Apply the European System of Accounts (ESA) boundary rules for central, local and general government:

- this ensures that the government net borrowing and gross debt measures in the public sector finances are aligned with the Maastricht definitions of government deficit and debt

- it means that no ex-measure should exclude any bodies that are categorised in the government sector and so ex-measures should only look to sub-divide the public corporations sector

Be wholly consistent with the ESA guidance on transactions and stocks:

- this ensures that measures in the public sector finances are calculated in the same way as in international measures and prevents ex-measures being developed that are not consistent with national accounts and Maastricht debt and deficit

- it further ensures that any ex-measures exclude public sector bodies and then record their transactions and stocks in accordance with national accounts principles, preventing inconsistent treatment in ex-measures of individual transactions and stocks

- in this way we are ensuring that the measures are based on sound internationally-agreed concepts and definitions

Be created alongside a publication strategy that maximises the transparency of factors that impact on the public sector finances with details published below institutional unit level described fully in terms of the framework outlined previously.

4.2.4 Relaxation of fiscal rules in response to the financial crisis (2008 to 2010)

In its Pre-Budget November 2008 report, Facing global challenges: supporting people through difficult times (PDF, 1.2MB), the government formally announced that in light of the ongoing financial crisis it would temporarily depart from the fiscal rules. This relaxation was intended to allow fiscal policy to shore-up aggregate demand in the economy and reduce the likelihood of a deep recession. Adherence to the golden rule requirement to balance the current budget over the cycle would have required a huge amount of fiscal tightening, which would have exacerbated the economic slowdown.

The government indicated that it was content to allow public sector debt to rise to absorb the immediate shocks, with fiscal policy set to support both the financial sector and the broader economy. The Pre-Budget report detailed a temporary fiscal stimulus package, worth 1% of GDP in financial year ending (FYE) March 2010. This included an immediate, temporary reduction in the rate of VAT to 15% until the end of the 2009 calendar year and the bringing forward of £3 billion of capital spending from the following financial year. The fiscal relaxation was reflected in sharp rises in current budget deficit, net borrowing and net debt for central government and the public sector for FYE 2010.

At the Budget March 2010, preceding the dissolution of Parliament in May, a consolidation plan was presented with the following targets for borrowing and debt:

PSNB ex to more than halve from a projected level of 11.8% of gross domestic product (GDP) to 5.5% of GDP or less by FYE 2014

PSNB ex to be reduced as a share of GDP in each year from FYE 2010 to FYE 2016

PSND ex to be falling as a share of GDP in FYE 2016

4.2.5 The coalition government's fiscal framework and mandate (2010 to 2015) and the role of the Office for Budget Responsibility

A reformed fiscal framework was established following the formation of the coalition government in May 2010. The new framework was written into legislation via the Budget Responsibility and National Audit Act 2011.

The Act requires governments to lay a Charter for Budget Responsibility (PDF, 259KB) (the Charter) before Parliament. The Charter sets out the government's fiscal policy framework, which includes HM Treasury (HMT) objectives for fiscal policy, as set by government and HMT's fiscal mandate (the government's main fiscal targets). The Charter was initially published in April 2011 but has since been revised and updated on several occasions to reflect modifications made to the framework.

The fiscal policy objectives detailed in the initial 2011 version of the Charter were to:

ensure sustainable public finances that support confidence in the economy, promote intergenerational fairness and ensure the effectiveness of wider government policy

support and improve the effectiveness of monetary policy in stabilising economic fluctuations

The Charter also presented HMT's mandate for fiscal policy over the 2010 to 2015 Parliament, which was:

- a forward-looking target to achieve cyclically-adjusted current balance by the end of the rolling, five-year forecast period

The mandate was supplemented by:

- a target for public sector net debt as a percentage of GDP to be falling by a fixed date of FYE 2016, ensuring the public finances were restored to a sustainable path

The Charter also set out HMT's objective in relation to debt management policy, which was:

- to minimise, over the long-term, the costs of meeting the government's financing needs; this was to be done whilst considering risk and ensuring that debt management policy was consistent with the aims of monetary policy

This mandate deliberately focused on current spending, as reflected in the targeting of the current balance. The exclusion of capital expenditure can be viewed as a means of safeguarding public investment, which is generally considered to be the most economically productive element within public spending. A cyclically-adjusted aggregate (see Annex 2) was targeted, such that the automatic stabilisers could operate fully in support of the economy. The mandate was to lapse at the 2015 dissolution of Parliament.

The major innovation detailed in the new framework was the creation of an independent Office for Budget Responsibility (OBR) in May 2010. The rationale was that this would increase transparency and openness in official forecasting and assessments of fiscal policy. It was intended to allay concerns that a Chancellor or ministerial colleagues might otherwise exert pressure on HMT to produce unduly optimistic economic and financial forecasts.

The OBR's principal remit is to examine and report on the sustainability of the public finances. The Charter for Budget Responsibility (PDF, 311KB) states that the remit provides for the OBR to investigate the impact of trends and policies on the public finances from a multitude of angles, including through forecasting, long-term projections and balance sheet analysis. It performs this duty completely independently of government.

Prior to the establishment of the OBR, responsibility for producing official forecasts for economic indicators and fiscal aggregates, and for assessing fiscal policy sat with HMT. The Charter specified that, following the transfer of responsibilities to the OBR, HMT would "continue to maintain the necessary analytical and macroeconomic expertise to provide ongoing advice to the government."

The Charter indicated that the Chancellor would commission the OBR to produce fiscal and economic forecasts on specified dates at least twice a year, one of which would coincide with Budget day. The forecast horizon was to be consistent with that set by the Chancellor and would always be for a period of at least five financial years. In practice, since its inception, the OBR has published five-year horizon forecasts for the UK economy and public finances biannually in its Economic and Fiscal Outlook (EFO) publications. In addition, it publishes two other publications:

an annual Forecast Evaluation Report (FER) each autumn, examining how the forecasts have compared with subsequent outturns, drawing lessons for improving future forecasts

a biannual Fiscal Risks and Sustainability Report (FRSR) which examines the fiscal impact of past public sector activity, as reflected in the assets and liabilities that it has accumulated on its balance sheet, and fiscal risks facing the UK , whilst also examining the sustainability of public sector finances via long-term projections of how spending and revenues may evolve and the impact this would have on public sector net debt

The OBR's economic forecast includes projections for GDP, inflation, labour market indicators, and the balance of payments current account. The Charter specified that in its forecasts the OBR was to include projections of a number of PSF aggregates, including:

public sector current expenditure

public sector gross investment

public sector net investment

public sector current receipts

the current balance

public sector net borrowing

general government net borrowing

the central government net cash requirement

public sector net debt

general government gross debt

any other aggregate or indicator as is required to judge progress or achievement against the government's mandate for fiscal policy, or is required for the purposes of the government's European commitments, in particular the Stability and Growth Pact

The Charter also required the OBR to assess progress towards meeting fiscal targets. In practice, this has involved assessing whether the government's fiscal policy is consistent with a greater than 50% chance of meeting the fiscal mandate.

4.2.6 Adjustments to the fiscal framework and mandate: introduction of the welfare cap (2014 to 2016)

As a means of exerting stricter control of spending in an area that can be difficult for government to control, the coalition government decided to introduce a welfare cap. The cap is a cash limit on the amount that government can spend on certain social security benefits and tax credits. The cap excludes expenditure on pensions, Jobseekers' Allowance and Housing Benefit. Tax Credits, Child Benefit and Disability Benefit are examples of benefits that are in scope. Unlike the other fiscal targets, the welfare cap is not based on national accounts concepts or principles and no data directly relating to the welfare cap is published in the public sector finances.

The introduction of the cap at the Budget 2014 was reflected in an updated Charter (PDF, 192KB) with a revised mandate. The revised mandate included a restating of the target for public sector net debt (PSND) as:

- an aim for PSND as a percentage of GDP to be falling by 2016 to 2017

Following the general election in May 2015, the Charter (PDF, 428KB) was further updated with a revised mandate for fiscal policy, but no changes in the objectives for fiscal policy or role of the OBR. The updated Charter was approved by Parliament in October 2015 and the revised mandate was expressed as:

in normal times, once a headline surplus has been achieved, the Treasury's mandate for fiscal policy is a target for a surplus on public sector net borrowing in each subsequent year

for the period outside normal times from 2015 to 2016, the Treasury's mandate for fiscal policy is a target for a surplus on public sector net borrowing by the end of 2019 to 2020

for the period from 2015 to 2016 until 2019 to 2020, the Treasury's mandate for fiscal policy is supplemented by a target for public sector net debt as a percentage of GDP to be falling in each year

after 2019 to 2020, the normal times target will apply unless and until the OBR assess, as part of their economic and fiscal forecast, that there is a significant negative shock to the UK

a significant negative shock is defined as real GDP growth of less than 1% on a rolling four-quarter-on-four-quarter basis.

The expression, "normal times", can be construed as periods when the economy is growing steadily, in the absence of significant negative shocks as defined in the previous final bullet point.

4.2.7 Current fiscal framework with the introduction of new supplementary fiscal aggregates (2016 onward)

The autumn 2016 update to the Charter stated that, in order to provide for sustainable public finances, HMT's objective for fiscal policy was to:

- return the public finances to balance at the earliest possible date in the next Parliament

HMT's mandate for fiscal policy in Parliament was:

- a target to reduce cyclically-adjusted public sector net borrowing to below 2% of GDP by 2020 to 2021

The 2016 Autumn Statement included an announcement by the Chancellor that two new supplementary fiscal aggregates had been defined, which would provide additional commentary on the state of the public sector balance sheet and context for the main fiscal metric of public sector net debt. These supplementary aggregates, public sector net debt excluding the Bank of England (PSND ex BoE), and public sector net financial liabilities (PSNFL), are described in Section 5.

The Chancellor also announced that the government intended to move to a single major fiscal event each year. Traditionally, UK governments had tended to reveal their plans for taxation in a spring budget and announce planned government expenditure in an autumn report or statement. However, over time the distinction had become less clear cut, such that planned tax changes might be presented to Parliament either in spring or in autumn.

The Chancellor signalled that the spring 2017 Budget would be the last springtime fiscal event that would include taxation plans. Thereafter, budgets were to be delivered in the autumn, with the first one taking place in autumn 2017. The move to a single fiscal event meant that businesses and individuals would face less frequent changes to the tax system, helping to promote certainty and stability. From winter 2017, Finance Bills were to be introduced following the Budget, affording Parliament more time to scrutinise tax changes before the tax year in which most of them take effect.

4.3 UK’s compliance with the Maastricht Treaty while a member of the EU

In preparation for monetary union, various safeguards against fiscal profligacy were enshrined in the Treaty on the Functioning of the European Union (commonly known as the Maastricht Treaty), which came into force in 1993. The Stability and Growth Pact requires all member states to avoid excessive budget deficits and levels of government debt.

The reference values set out in the Pact, which member states should endeavour not to exceed, comprise a general government (GG) deficit (or net borrowing) of 3% and GG gross debt of 60% of gross domestic product (GDP). Failure to meet these targets and more especially the deficit target, may result in the Commission initiating excessive deficit procedure (EDP) actions, as discussed in this section.

EU member governments are obliged to report their actual and planned deficits, along with their levels of debt, in detailed data tabulations to the Statistical Office of the European Union (Eurostat) in accordance with fixed deadlines.

The UK left the EU on 31 January 2020. A transition period was in place from 1 February 2020 to 31 December 2020 during which the UK continued to supply data to Eurostat in accordance with EU membership rules. The rules governing the new relationship between the EU and UK took effect on 1 January 2021, after which the UK stopped supplying Eurostat with EDP data.

4.4 International comparisons of debt and deficit

The UK government debt and deficit statistical bulletin is published quarterly in January, April, July and October each year. This is to coincide with when EU member states are required to report on their debt and deficit to the European Commission.

The general government debt and deficit figures published in this statistical bulletin for the time period 1997 onwards (when the ESA framework was first adopted for the compilation of data in the UK) are fully consistent with those published in the public sector finances, being compiled on the same European System of Accounts: ESA 2010 basis.

There are two main differences between the headline debt and deficit measures between the public sector finance statistics and those used for international comparisons.

Firstly, this bulletin includes only the debt and deficit of central and local government bodies. The public sector finances' measures also include the debt and deficit of other public sector bodies, including public non-financial corporations and the Bank of England.

Secondly, this bulletin reports gross debt, while the focus of the public sector finances is net debt. Gross debt represents only the financial liabilities (debt securities, loans and deposits) of central and local government, while net debt deducts any liquid assets (mainly official reserve assets and other cash or assets that can quickly and easily be converted into cash) from the financial liabilities to arrive at a net figure.

It is important to achieve coherence in the estimates provided in both datasets. Therefore, each quarter (more specifically in March, June, September and December) PSF data are aligned to the more detailed quarterly data (as reported to both OECD and IMF).

Aligning datasets

For the latest month and financial year-to-date, outturn data in the PSF bulletin has to reflect the latest available information, while ensuring coherence with the EDP bulletin. Therefore, the following approach is adopted:

the latest reported month reflects the most up-to-date PSF data available

the quarterly data in the periods common to both EDP and PSF bulletins are aligned

the estimates for the month immediately prior to the latest month, but after the period of aligned quarterly data, are calculated by taking the latest cumulative estimates for the financial year-to-date and subtracting both the cumulative totals for those aligned quarters in the financial year and the latest month estimates

For example, in the PSF published in September:

the August estimates use the latest reported data

the PSF data in the period April to June are aligned to the estimates in the EDP bulletin

the July figures are derived from the financial year-to-date (April to August) less the sum of the aligned period (April to June) and less the estimates for August

This alignment process results in a temporary adjustment to the published monthly profiles. This adjustment will unwind in the dataset reported in the bulletin published in the following month, when the PSF estimates are decoupled from the EDP bulletin to reflect the latest available data.

In this example, the estimate originally derived for July may subsequently be revised to reflect the latest source data. This phenomenon is discussed further in the Public sector finances revisions policy.

Nôl i'r tabl cynnwys5. Fiscal aggregates included in the public sector finances statistics

This section amplifies the descriptions, provided in Section 2 of this guide, of the main fiscal metrics published in the Public sector finances (PSF) bulletin. These comprise a set of aggregates, designed primarily by HM Treasury (HMT) to monitor progress towards government fiscal goals (discussed in Section 4). The PSF statistics are designed to provide reliable, timely and appropriate information to enable users, including HMT and Office for Budget Responsibility (OBR), to gauge progress towards the government's fiscal goals.

5.1 Composition and reconciliation of the PSF aggregates

Three of the main fiscal aggregates, the public sector current budget deficit (PSCB), public sector net borrowing (PSNB) and the public sector net cash requirement (PSNCR), relate to economic activity and associated transactions that occur within a defined, limited period (such as a month, quarter, or year). They can be categorised as "flow" measures. Conversely, public sector net debt (PSND), public sector net financial liabilities (PSNFL) and public sector net worth (PSNW) record the cumulative net value of liabilities that have accumulated at a given point in time and can be categorised as "stock" measures.

5.1.1 Public sector current budget deficit (PSCB)

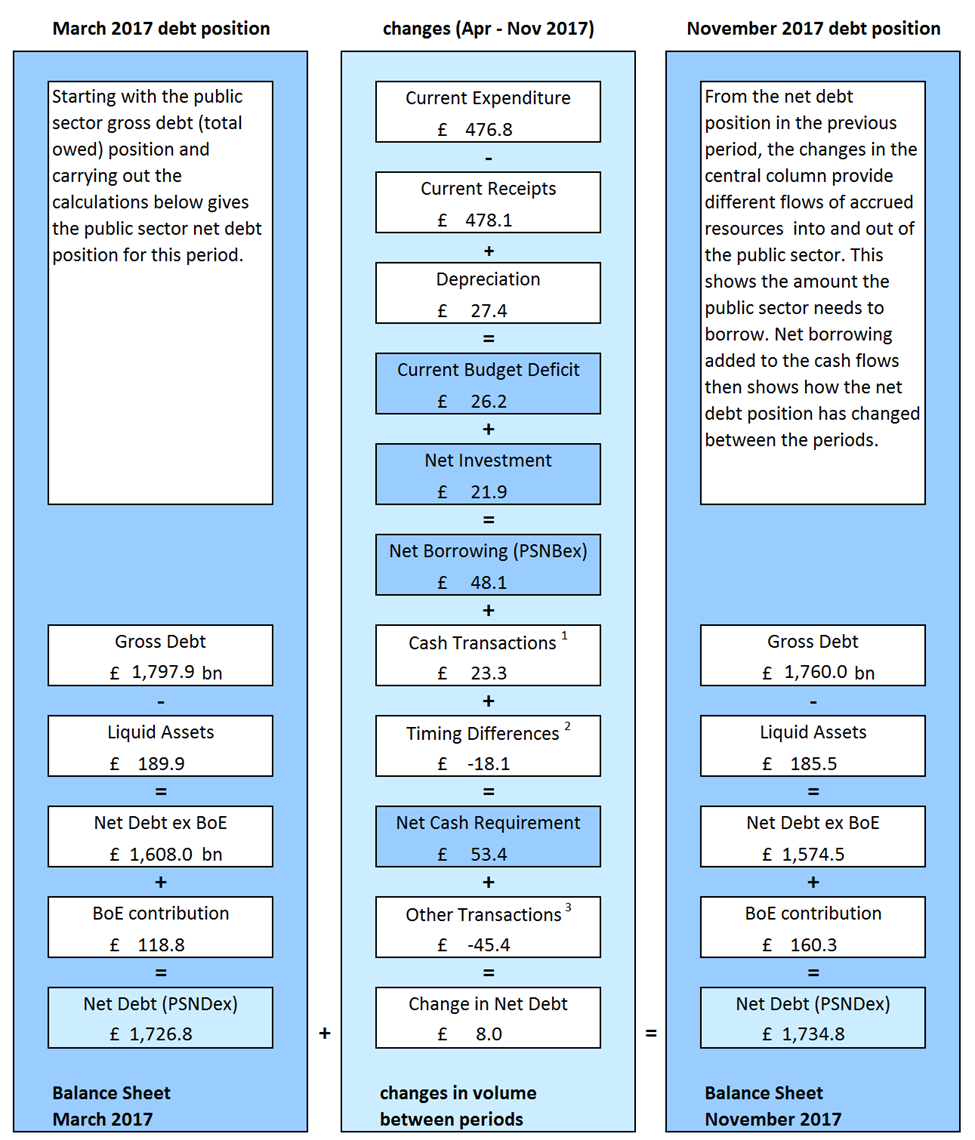

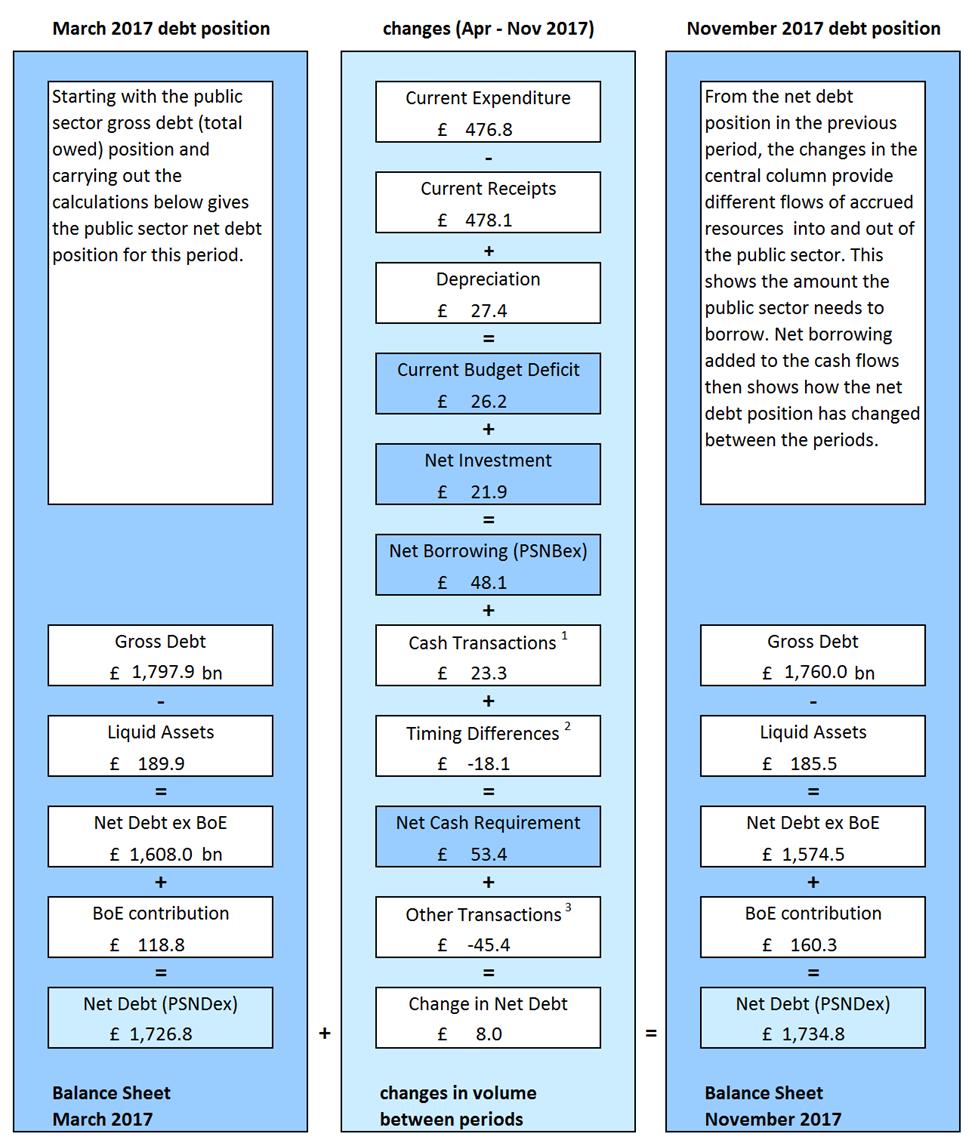

In Section 2.2 we noted that PSCB represents the balance of receipts over current expenditure, after providing for depreciation on capital assets. Hence, depreciation is treated as an expense for the period concerned, as in commercial accounts. So we can measure the deficit (or surplus if receipts exceed the two other components) as:

current budget deficit equals (current expenditure minus current receipts) plus depreciation

An illustration is provided in the upper section of the middle column of Figure 1, where data for current revenue, expenditure and depreciation for the period April to November 2017 are provided. One can see that over that eight-month period:

current budget deficit equals (£476.8 billion minus £478.1 billion) plus £27.4 billion equals £26.2 billion

So, over that eight-month period there was a current budget deficit of around £26.2 billion.1

Figure 1: Connections between main PSF aggregates, and an illustration of how various elements contribute to changes in PSND ex over time

Source: Office for National Statistics

Notes:

Cash transactions in (non-financing) financial assets, which do not impact on net borrowing.

Timing differences between cash and accrued data.

Revaluation of foreign currency debt (for example, foreign currency). Debt issuances or redemptions above or below debt valuation (for example, bond premia and discounts and capital uplifts). Changes in volume of debt not due to transactions (for example, sector reclassification).

Download this image Figure 1: Connections between main PSF aggregates, and an illustration of how various elements contribute to changes in PSND ex over time

.png (336.4 kB){kind=link}