Cynnwys

- Main points

- Things you need to know about this release

- In summary

- What’s changed in this release?

- The treatment of pensions in public sector finances

- Country and regional public sector finances

- How much is the public sector borrowing?

- How big is public sector debt?

- How much cash does the public sector need to raise?

- How was debt in the latest financial year accumulated?

- How do these figures compare with official forecasts?

- Revisions since previous release

- International comparisons of borrowing and debt

- Background information

- Planned changes for future releases

- Recent announcements concerning the Term Funding Scheme

- Recent events that may impact on public sector finances

- Quality and methodology

1. Main points

Public sector net borrowing (excluding public sector banks) in the latest full financial year (April 2017 to March 2018) was £39.4 billion; that is, £6.3 billion less than in the previous financial year (April 2016 to March 2017) and £5.8 billion less than official (Office for Budget Responsibility) expectations; this is the lowest net borrowing since the financial year ending March 2007.

Public sector net borrowing (excluding public sector banks) in the current financial year-to-date (April 2018 to June 2018) was £16.8 billion; that is, £5.4 billion less than in the same period in 2017; this is the lowest year-to-date (April to June) net borrowing since 2007.

Public sector net borrowing (excluding public sector banks) decreased by £0.8 billion to £5.4 billion in June 2018, compared with June 2017; this is the lowest June net borrowing since 2016.

Public sector net debt (excluding public sector banks) was £1,792.3 billion at the end of June 2018, equivalent to 85.2% of gross domestic product (GDP), an increase of £33.0 billion (or a decrease of 1.0 percentage points as a ratio of GDP) on June 2017.

Following the passage of the Regulation of Registered Social Landlords (Wales) Act 2018 on 13 June 2018, housing associations in Wales have been reclassified from the public sector to the private sector, reducing public sector net debt at the end of June 2018 by £2.7 billion.

Public sector net debt (excluding both public sector banks and Bank of England) was £1,600.6 billion at the end of June 2018, equivalent to 76.1% of GDP, a decrease of £23.7 billion (or a decrease of 3.5 percentage points as a ratio of GDP) on June 2017.

Central government net cash requirement in the current financial year-to-date (April 2018 to June 2018) was £14.1 billion; that is, £1.9 billion more than in the same period in 2017.

2. Things you need to know about this release

Public sector net borrowing excluding public sector banks (PSNB ex) measures the gap between revenue raised (current receipts) and total spending (current expenditure plus net investment (capital spending less capital receipts)). Public sector net borrowing is often referred to by commentators as “the deficit”.

The public sector net cash requirement (PSNCR) represents the cash needed to be raised from the financial markets over a period of time to finance the government’s activities. This can be close to the deficit for the same period but there are some transactions, for example, loans to the private sector, which need to be financed but do not contribute to the deficit. It is also close but not identical to the changes in the level of net debt between two points in time.

Public sector net debt excluding public sector banks (PSND ex) represents the amount of money the public sector owes to private sector organisations including overseas institutions, largely as a result of issuing gilts and Treasury Bills, less the amount of cash and other short-term assets it holds.

While borrowing (or the deficit) represents the difference between total spending and receipts over a period of time, debt represents the total amount of money owed at a point in time.

The debt has been built up by successive government administrations over many years. When the government borrows (that is, runs a deficit), this normally adds to the debt total. So reducing the deficit is not the same as reducing the debt.

If you’d like to know more about the relationship between debt and deficit, please refer to our article The debt and deficit of the UK public sector explained.

Nôl i'r tabl cynnwys3. In summary

Borrowing in the latest full financial year (April 2017 to March 2018) was the lowest financial year borrowing for 11 years.

In the latest full financial year, the public sector borrowed £39.4 billion; that is, £6.3 billion less than in the previous financial year (April 2016 to March 2017) and £5.8 billion less than official expectations. Of this borrowing, £40.6 billion was borrowed to cover capital spending (or net investment), such as on infrastructure. The borrowing to cover the “day-to-day” activities of the public sector (the current budget deficit) was in surplus by £1.3 billion. This current budget surplus is the first annual surplus since the financial year ending March 2002. However, it must be remembered that this is a provisional estimate and it may be revised as forecasts are replaced by audited data.

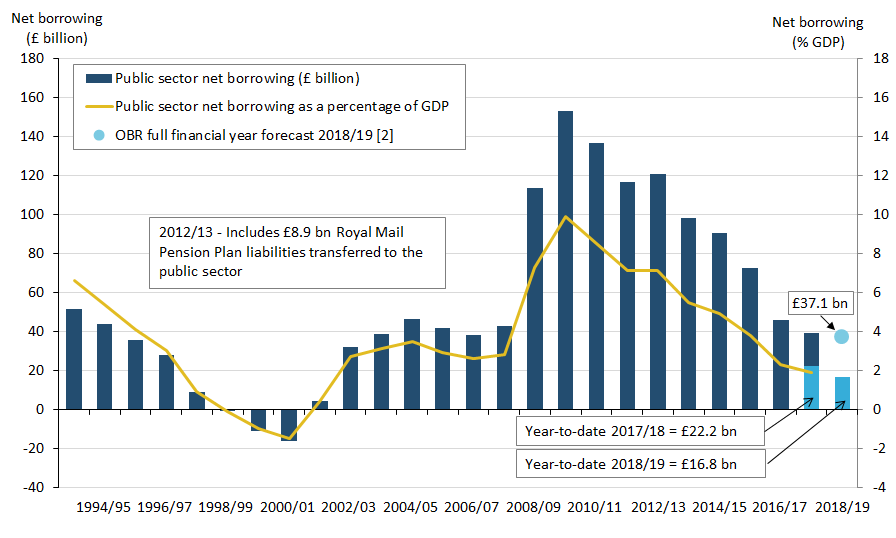

Over the next 12 months (April 2018 to March 2019), the Office for Budget Responsibility, which produces the official government forecasts, expects the public sector to borrow £37.1 billion; around one-quarter of what it borrowed in the financial year ending March 2010 (April 2009 to March 2010), at the peak of the financial crisis.

So far in this financial year (April 2018 to June 2018), the public sector has borrowed £16.8 billion; that is, £5.4 billion less than in the same period in 2017; again, this represents the lowest year-to-date borrowing for 11 years.

Figure 1: Public sector net borrowing (excluding public sector banks)

Cumulative financial year-to-date (April to June 2018) compared with previous full financial years (April to March), UK

Source: Office for National Statistics

Notes:

- OBR forecast for public sector net borrowing excluding public sector banks from March 2018 Economic and Fiscal Outlook (EFO).

Download this chart Figure 1: Public sector net borrowing (excluding public sector banks)

Image .csv .xlsOften commentators abbreviate the official term public sector net borrowing (excluding public sector banks) to simply “the deficit”.

It is important to understand that reducing the deficit is not the same as reducing the debt. The debt has been built up by successive government administrations over many years. When the government borrows (that is, runs a deficit), this normally adds to the debt total.

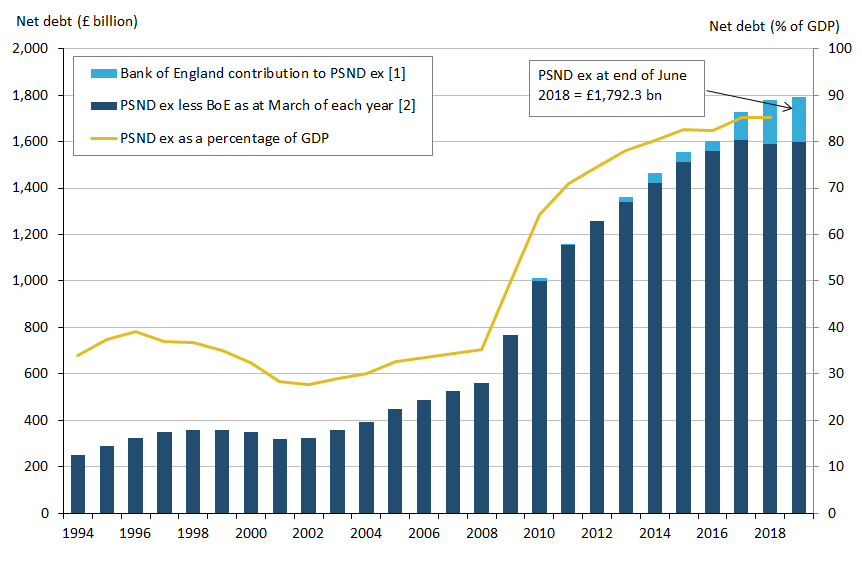

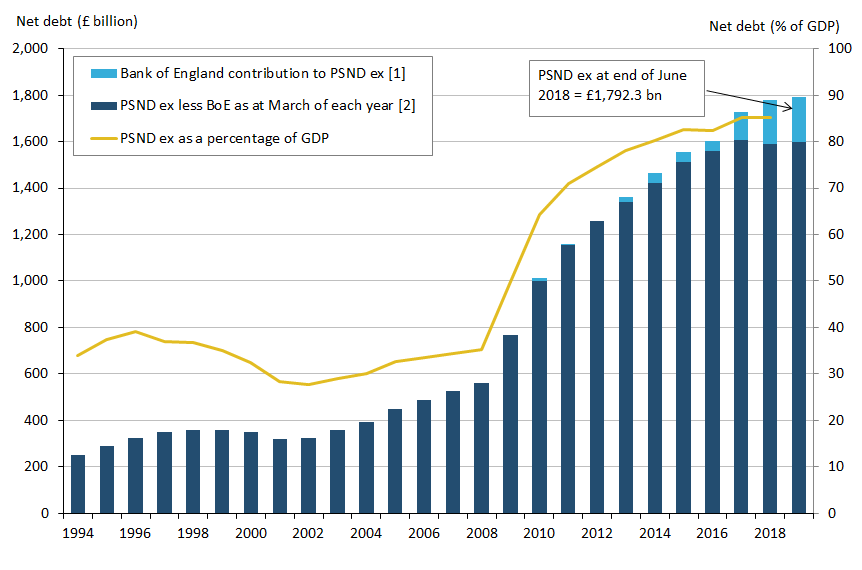

At the end of June 2018, the amount of money owed by the public sector to the private sector stood at around £1.8 trillion (or £1,792.3 billion), an increase of £33.0 billion on June 2017. This £1.8 trillion equates to 85% of the value of all the goods and services currently produced by the UK economy in a year (or gross domestic product (GDP)).

However, if we were to exclude the impact of the Bank of England’s programme of temporary activities designed to boost the economy from net debt, then this £1.8 trillion reduces by £0.2 trillion to £1.6 trillion (or £1,601 billion) at the end of June 2018, or 76% of GDP.

Nôl i'r tabl cynnwys4. What’s changed in this release?

This section presents information on aspects of data or methodology that have been introduced or improved since the publication of the previous bulletin.

Contribution to the EU budget

Every year the European Commission (EC) reports retrospective adjustments to the EU budget contributions of EU member states based on the latest Value Added Tax (VAT) and gross national income (GNI) data.

In June 2018, the UK paid £628 million to the EU budget through GNI and VAT based contributions, which are made net of the UK rebate. This payment consisted of our standard monthly VAT and GNI based contribution of £865 million, along with a £237 million credit covering earlier years.

Housing associations

Following the passage of the Regulation of Registered Social Landlords (Wales) Act 2018, we have completed an assessment of the housing associations in Wales. We have concluded that registered social landlords in Wales are private, market producers and as such they were reclassified to the private non-financial corporations sub-sector for the purpose of national accounts and other economic statistics such as public sector finances. This reclassification was effective from 13 June 2018, when Royal Assent was passed, with public sector net debt reducing by £2.7 billion at the end of June 2018 as a result. Public sector net borrowing will be reduced by around £0.2 billion per financial year as a result of this reclassification.

In recent weeks the Housing (Amendment) (Scotland) Bill has passed Stage 3 of the Scottish Parliament and as such, Office for National Statistics (ONS) is likely to review the classification status of registered social landlords in Scotland and Northern Ireland in the near future.

The Department for Communities launched a consultation on the future of House Sales Schemes in Northern Ireland, running between 3 July and 24 September 2018.

Royal Bank of Scotland (RBS) Group plc share sale

On 4 June 2018, UK Government Investments Limited (UKGI) announced the successful completion of the disposal of 7.7% of HM Treasury's shareholding in RBS, with proceeds of £2.5 billion.

As with similar share sales, the proceeds from the sale have reduced central government net cash requirement (CGNCR) in June 2018 and public sector net debt (PSND) at the end of June 2018 by the £2.5 billion proceeds from the sale, but had no impact on public sector net borrowing.

As a result of this sale, the RBS shareholding of HM Treasury has reduced from 70.1% of the ordinary share capital of the company, to approximately 62.4%.

Public sector net financial liabilities

When the supplementary fiscal aggregate of public sector net financial liabilities (PSNFL) was first introduced in November 2016, we explained that we would work to improve the quality of the underlying data.

To date, the most significant improvement has been to the estimate of the net liability of government in relation to funded public sector pension schemes, which were introduced in the August 2017 bulletin. Our programme of work includes improving holdings of other public sector assets and liabilities; recently, further progress has been made in improving loan assets and equity holdings.

Nôl i'r tabl cynnwys5. The treatment of pensions in public sector finances

On 21 June 2018, we published a technical note and consultation document concerning the treatment of pensions within the public sector finances (PSF). The note explains different options for the presentation of pension statistics in the PSF publications and provides the recommendations made by the expert advisory committee, the Public Sector Finances Technical Advisory Group. The consultation offers an opportunity to provide feedback on these recommendations within the following broad themes:

- how the assets and liabilities of the funded public sector pension schemes should be presented

- how the balance sheet and transactions of the Pension Protection Fund should be incorporated

- how the obligations of the unfunded public sector pension schemes should be presented

This consultation opened on 21 June 2018 and will close on Friday 31 August 2018.

Nôl i'r tabl cynnwys6. Country and regional public sector finances

On 1 August 2018, we will be publishing our latest Country and regional public sector finances statistical bulletin for financial year ending March 2017.

This will be the second time we have published public sector revenue, expenditure and net fiscal balance on a country and regional basis and follows our previous publication, Country and regional public sector finances: financial year ending March 2016.

Nôl i'r tabl cynnwys7. How much is the public sector borrowing?

In the financial year-to-date (April to June 2018), the public sector spent more money than it received in taxes and other income. This meant it had to borrow £16.8 billion; that is, £5.4 billion less than the same period in 2017.

Of this £16.8 billion of public sector net borrowing excluding public sector banks (PSNB ex), £10.3 billion related to the cost of the “day-to-day” activities of the public sector (the current budget deficit), while £6.4 billion was capital spending (or net investment), such as on infrastructure.

Figure 2 presents both monthly and cumulative public sector net borrowing (excluding public sector banks) in the current financial year-to-date (April to June 2018) and compares these with the previous financial year.

Figure 2: Public sector net borrowing (excluding public sector banks)

Cumulative financial year-to-date (April to June 2018) compared with the financial year ending March 2018 (April 2017 to March 2018), UK

Source: Office for National Statistics

Download this chart Figure 2: Public sector net borrowing (excluding public sector banks)

Image .csv .xlsThe difference between central government's income and spending makes the largest contribution to the amount borrowed by the public sector. In the latest financial year-to-date (April to June 2018), of the £16.8 billion borrowed by the public sector, £19.4 billion was borrowed by central government, while local government borrowing was in surplus by £2.9 billion.

In the current financial year-to-date, central government received £169.4 billion in income, including £125.0 billion in taxes. This was around 3% more than in the same period in 2017.

Over the same period, central government spent £184.2 billion, around 1% less than in the same period in 2017. Of this amount, just below two-thirds was spent by central government departments (such as health, education and defence), around one-third on social benefits (such as pensions, unemployment payments, Child Benefit and Maternity Pay), with the remaining being spent on capital investment and interest on government’s outstanding debt.

Appendix D to this release contains a detailed breakdown of public sector current receipts.

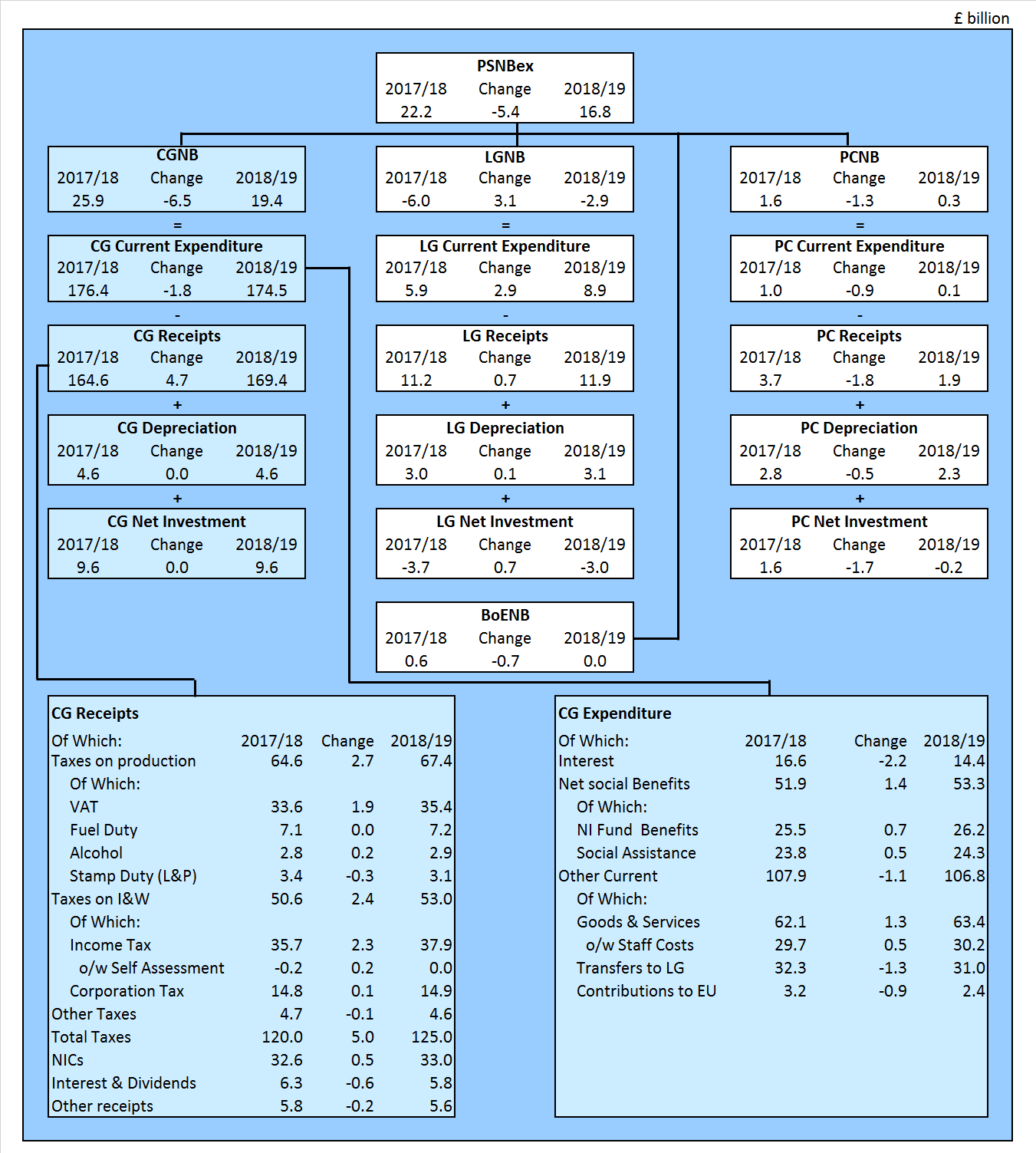

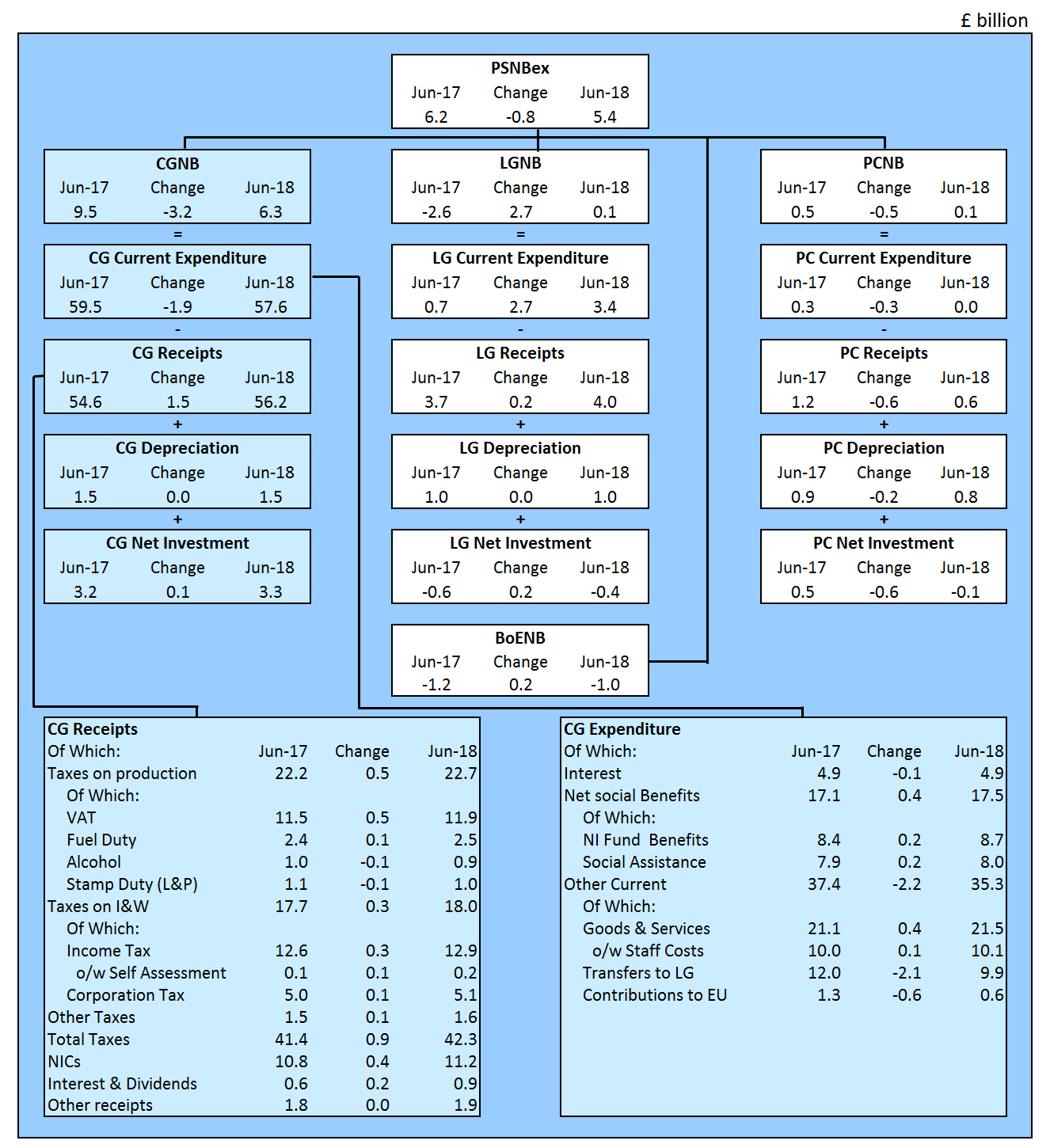

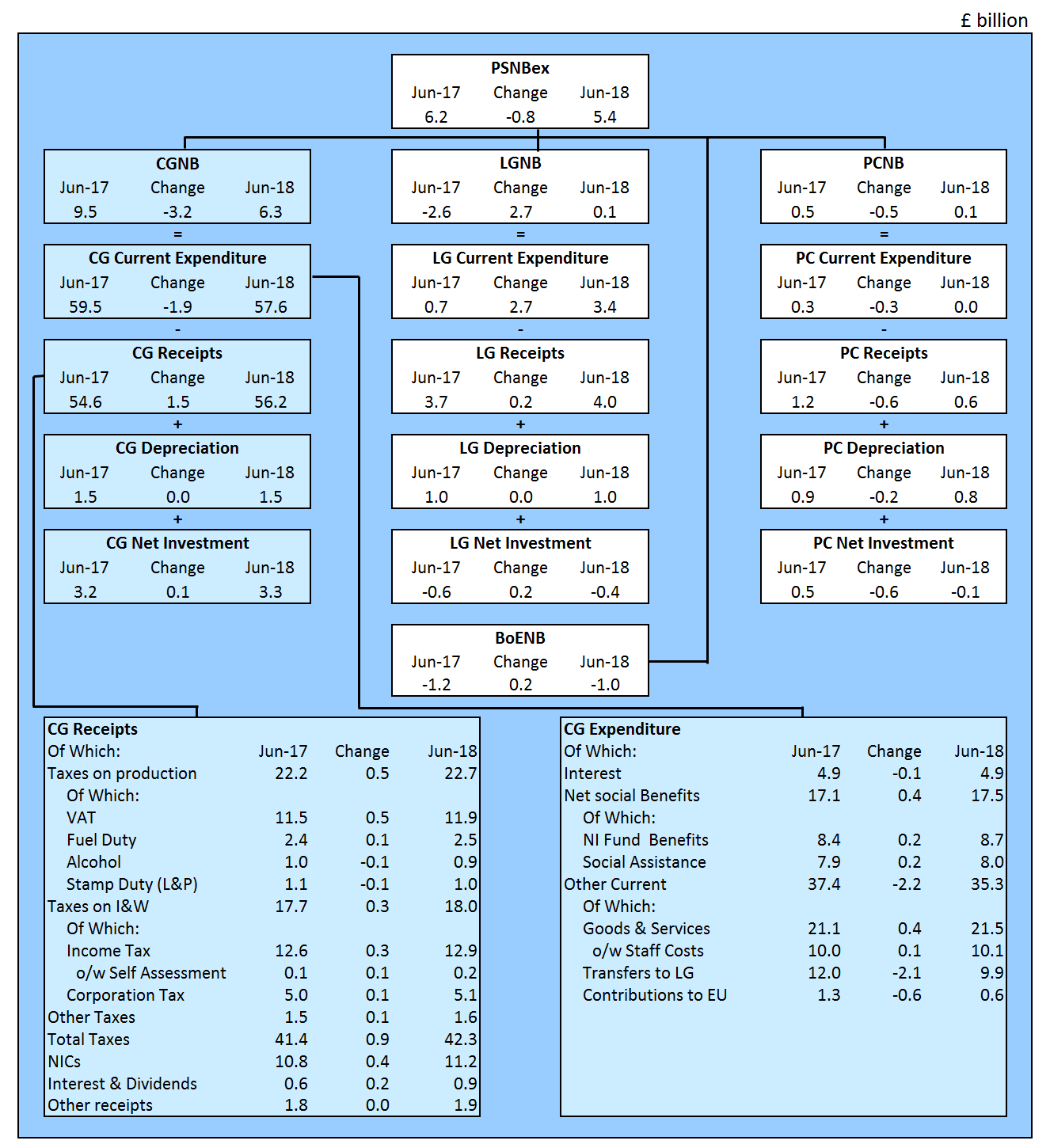

Figure 3 summarises public sector borrowing by sub-sector in the current financial year-to-date (April to June 2018) and compares these with the same period in the previous financial year.

This presentation splits PSNB ex into each of its four sub-sectors: central government, local government, public corporations and Bank of England.

A further breakdown (receipts, expenditure (both current and capital) and depreciation) is provided for central government, local government and public corporations, with central government current receipts and current expenditure being presented in further detail.

Figure 3: Contributions to public sector net borrowing (excluding public sector banks) by sub-sector

Current financial year-to-date (April to June 2018), UK

Source: Office for National Statistics

Notes:

- PSNBex – Public sector net borrowing excluding public sector banks.

- CGNB – Central government net borrowing.

- LGNB – Local government net borrowing.

- PCNB Non-financial public corporations net borrowing.

- BoENB – Bank of England net borrowing.

- L&P – Land and property.

- I & W – Income and wealth.

- Contributions to EU – UK VAT, GNI and abatement contributions to the EU budget.

- NICs – National Insurance contributions.

Download this image Figure 3: Contributions to public sector net borrowing (excluding public sector banks) by sub-sector

.png (119.6 kB) .xls (87.6 kB){kind=link}

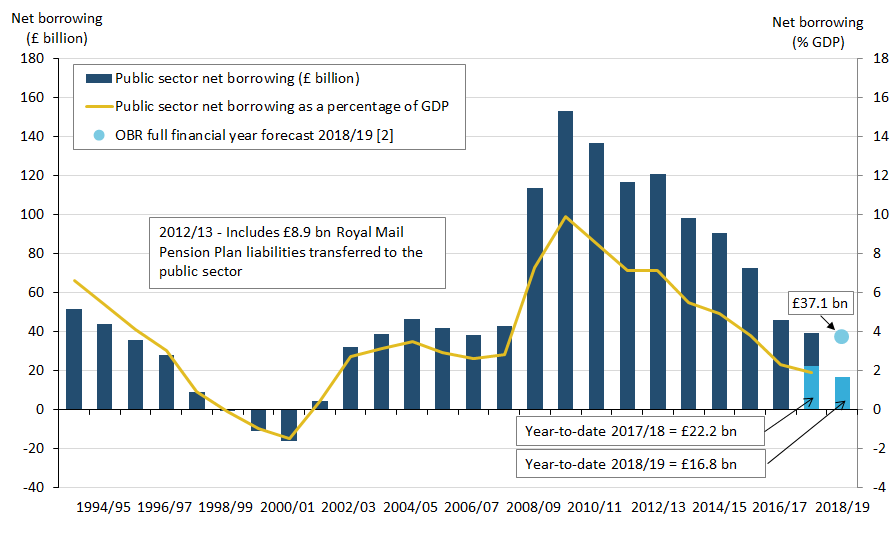

Figure 4 illustrates that annual borrowing has been falling generally since the peak in the financial year ending March 2010 (April 2009 to March 2010).

In the latest full financial year (April 2017 to March 2018), the £39.4 billion (or 1.9% of gross domestic product (GDP)) borrowed by the public sector was around one-quarter of PSNB ex in the financial year ending March 2010, when borrowing was £153.1 billion (or 9.9% of GDP).

Figure 4: Public sector net borrowing (excluding public sector banks)

April 1993 to June 2018, UK

Source: Office for National Statistics

Notes:

- Financial year 2017/18 represents the financial year ending 2018 (April 2017 to March 2018).

- Office for Budget Responsibility (OBR) full financial year forecast of £37.1 billion for public sector net borrowing excluding public sector banks (March 2018 Economic and Fiscal Outlook).

- Ytd equals year-to-date (April to June).

Download this image Figure 4: Public sector net borrowing (excluding public sector banks)

.png (42.8 kB) .xls (85.5 kB){kind=link}

The data for the latest month of every release contain some forecast data. The initial outturn estimates for the early months of the financial year, particularly April, contain more forecast data than other months, as profiles of tax receipts, along with departmental and local government spending are still provisional. This means that the data for these months are typically more prone to revision than other months and can be subject to sizeable revisions in later months.

Since the first estimate of PSNB ex for the financial year ending March 2018 (April 2017 to March 2018) was published on 24 April 2018, the estimate has been revised downward by £3.2 billion, from £42.6 billion to £39.4 billion. At this stage, none of the data underlying the estimates of borrowing in the latest full financial year are audited.

Currently, for the financial year ending March 2018:

central government net borrowing comprises largely provisional data supplied by departments

local government net borrowing is based on budget (forecast) data provided by the Ministry of Housing, Communities and Local Government (MHCLG) and the devolved administrations, updated where appropriate with in-year quarterly data published by MHCLG

public corporations’ net borrowing is based on Office for National Statistics (ONS) forecasts based on published Office for Budget Responsibility (OBR) data

Currently, for the financial year ending March 2017:

central government net borrowing comprises largely audited account data

local government data are mainly based on final outturn figures published by MHCLG and the devolved administrations

public corporations’ net borrowing is based on provisional returns from HM Treasury Whole of Government Accounts for the financial year ending March 2017, final outturn figures published by MHCLG, published accounts for individual public corporations and OBR forecasts

Appendix F shows revisions to the first reported estimate of financial-year-end public sector net borrowing (excluding public sector banks) by sub-sector. It summarises revisions to the first estimate of public sector net borrowing (excluding public sector banks) by sub-sector for the last six financial years. Revisions are shown at 6 and 12 months after year-end.

We have published an article, Public Sector Finances – Sources summary and their timing (PDF, 23KB), which provides a brief summary of the different sources used and the implications of using those data in the monthly Public sector finances (PSF) statistical bulletin.

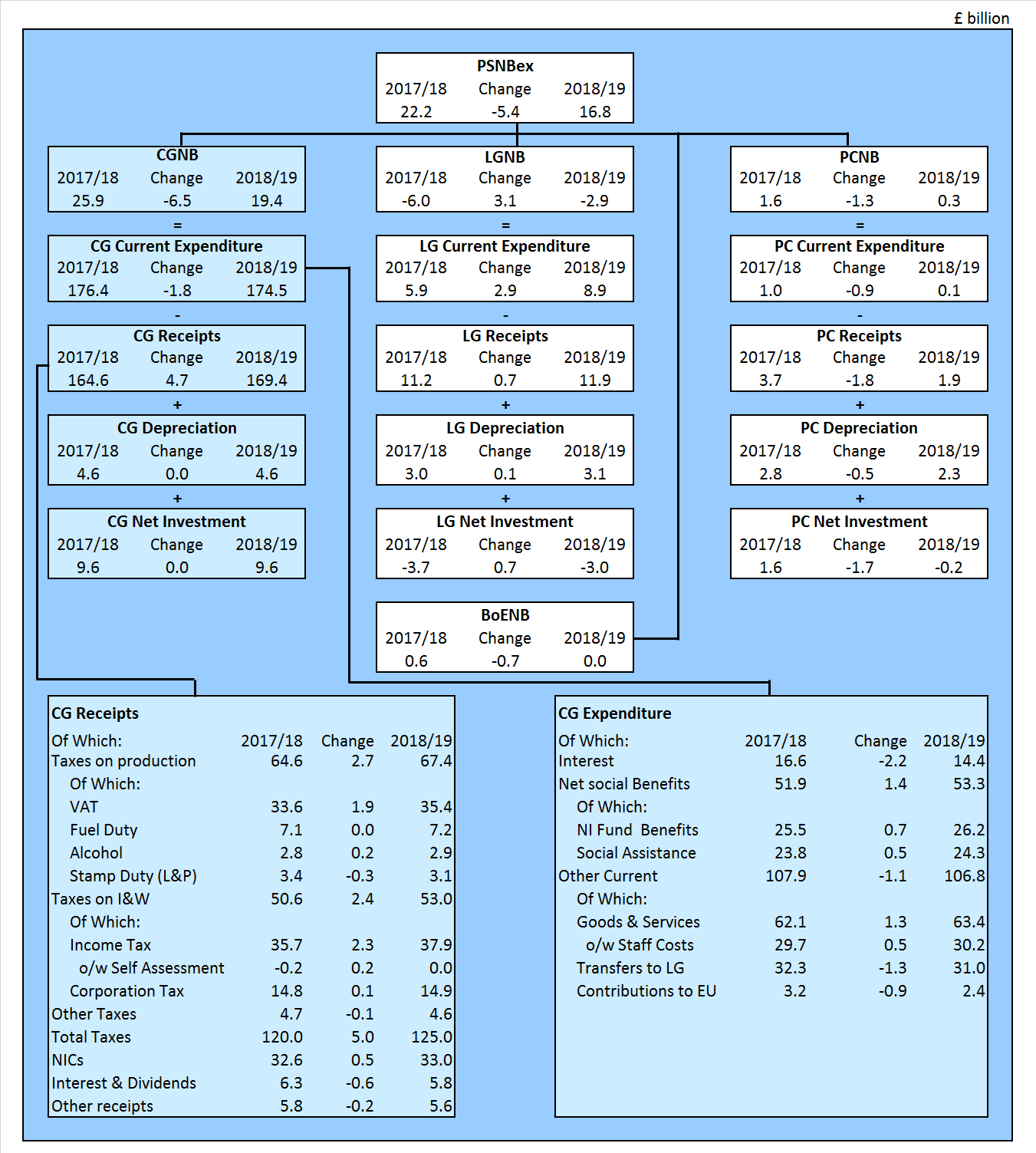

Focusing on the latest month

In June 2018, the public sector spent more money than it received in taxes and other income. This meant it had to borrow £5.4 billion; that is, £0.8 billion less than in June 2017.

Figure 5 summarises public sector borrowing by sub-sector in June 2018 and compares this with the equivalent measures in the same month a year earlier (June 2017).

This presentation splits public sector net borrowing excluding public sector banks (PSNB ex) into each of its four sub-sectors: central government, local government, public corporations and Bank of England.

A further breakdown (receipts, current expenditure, capital expenditure and depreciation) is provided for central government, local government and public corporations. Central government current receipts and current expenditure are presented in further detail.

Both local government and public corporations data for June 2018 are initial estimates. Most of these components are calculated by ONS based on OBR forecasts, with additional administrative source data used to estimate transfers to each of these sectors from central government.

Figure 5: Contributions to public sector net borrowing (excluding public sector banks) by sub-sector

June 2018, compared with June 2017, UK

Source: Office for National Statistics

Notes:

PSNBex – Public sector net borrowing excluding public sector banks.

CGNB – Central government net borrowing.

LGNB – Local government net borrowing.

PCNB – Non-financial public corporations net borrowing.

BoENB – Bank of England net borrowing.

L&P – Land and property.

I & W – Income and wealth.

Contributions to EU – UK VAT, GNI and abatement contributions to the EU budget.

NICs – National Insurance contributions.

Download this image Figure 5: Contributions to public sector net borrowing (excluding public sector banks) by sub-sector

.png (107.5 kB) .xls (87.6 kB){kind=link}

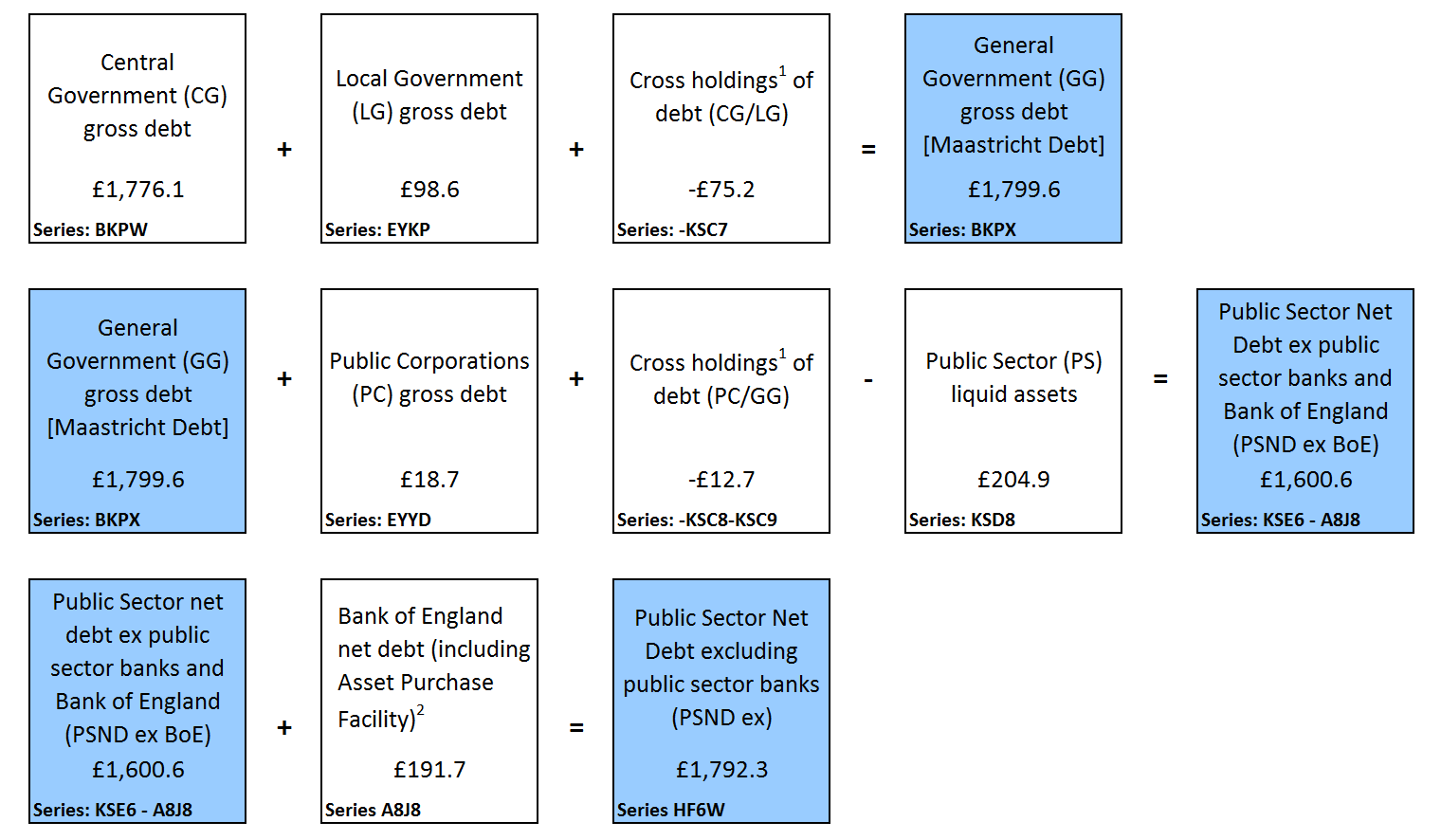

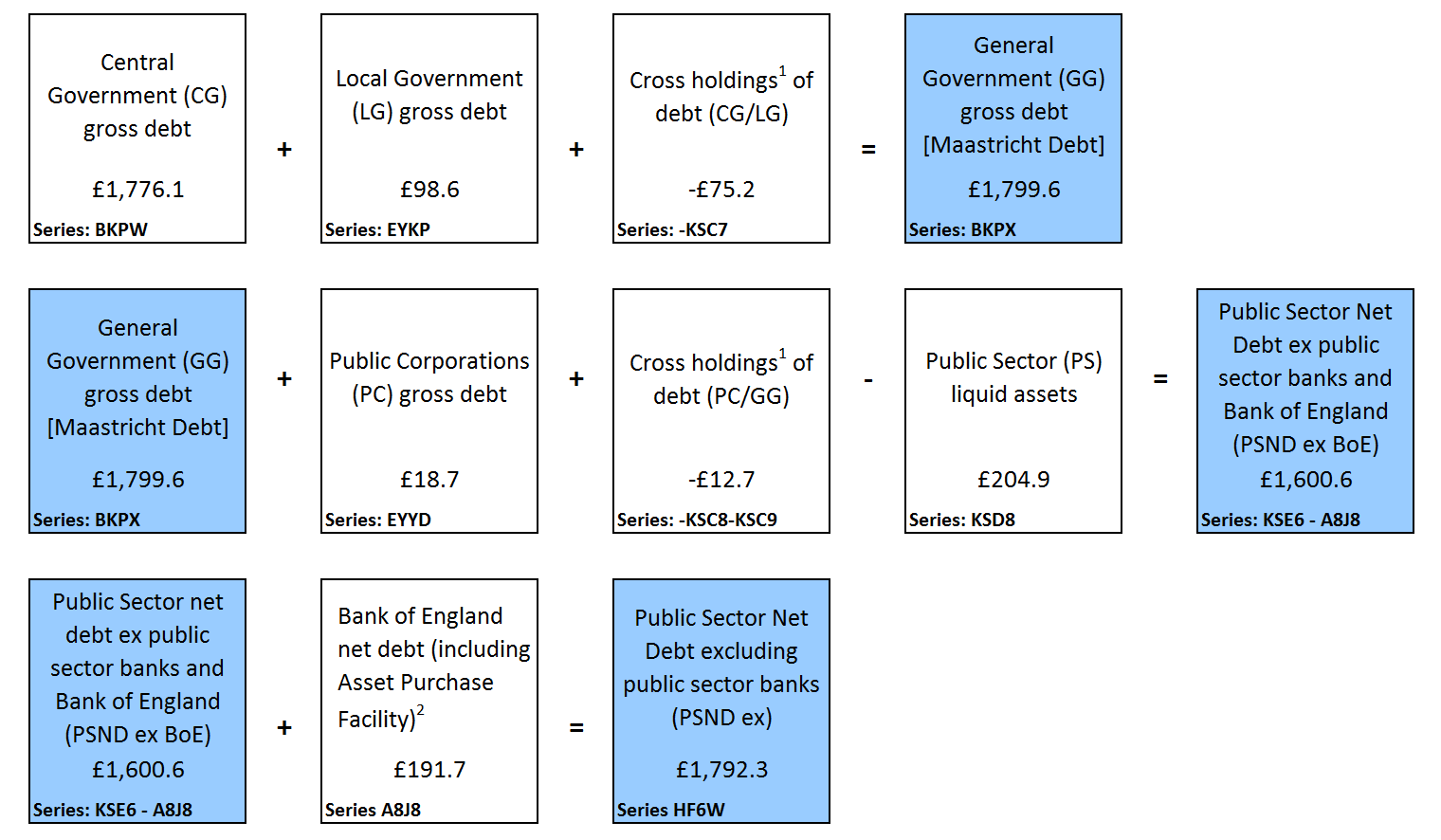

8. How big is public sector debt?

At the end of June 2018, the amount of money owed by the public sector to the private sector stood at around £1.8 trillion, which equates to 85.2% of the value of all the goods and services currently produced by the UK economy in a year (or gross domestic product (GDP)).

This £1.8 trillion (or £1,792.3 billion) debt at the end of June 2018 represents an increase of £33.0 billion since the end of June 2017.

The introduction of the Term Funding Scheme (TFS) in September 2016 led to an increase in net debt, as the loans provided under the scheme are not liquid assets and therefore do not net off in public sector net debt (against the liabilities incurred in providing the loans).

Since June 2017, the net debt associated with Bank of England (BoE) increased by £56.7 billion to £191.7 billion. Nearly all of this growth was due to the activities of the Asset Purchase Facility, which includes £57.2 billion from the TFS.

The TFS closed for drawdowns of further loans on 28 February 2018 with a loan liability of £127.0 billion. The TFS loan liability at the end of June 2018 was £126.5 billion.

If we were to exclude the activities of the BoE in the estimation of public sector net debt (excluding public sector banks), it would reduce by £191.7 billion, from £1,792.3 billion to £1,600.6 billion, or from 85.2% of GDP to 76.1%.

Figure 6 breaks down outstanding public sector net debt at the end of June 2018 into the sub-sectors of the public sector. In addition to public sector net debt excluding public sector banks (PSND ex), this presentation includes the effect of public sector banks on debt.

Figure 6: Contributions to public sector net debt by sub-sector at the end of June 2018, UK

Source: Office for National Statistics

Notes:

PSND – Public sector net debt.

PSBsND – Public sector Banks net debt.

PSNDex – Public sector net debt excluding public sector banks.

BoEND – Bank of England's contribution to net debt.

PSND ex less BoE – Public sector net debt excluding both public sector banks and Bank of England.

NFPCND – Non-financial public corporations' net debt.

GGND – General government net debt.

Download this chart Figure 6: Contributions to public sector net debt by sub-sector at the end of June 2018, UK

Image .csv .xlsNet debt is defined as total gross financial liabilities less liquid financial assets, where liquid assets are cash and short-term assets, which can be released for cash at short notice without significant loss. These liquid assets comprise mainly of foreign exchange reserves and bank deposits.

Figure 7 presents public sector net debt excluding public sector banks (PSND ex) at the end of June 2018 by sub-sector. Time series for each of these component series are presented in Tables PSA8A to D in the Public sector finances Tables 1 to 10: Appendix A dataset.

Figure 7: Contributions to public sector net debt (excluding public sector banks) by sub-sector at the end of June 2018, UK

Source: Office for National Statistics

Notes:

Cross-holdings between sub-sectors are removed in calculating public sector net debt, gross debt and liquid assets.

APF – Bank of England Asset Purchase Facility.

Download this image Figure 7: Contributions to public sector net debt (excluding public sector banks) by sub-sector at the end of June 2018, UK

.png (83.3 kB) .xls (184.3 kB){kind=link}

Figure 8 illustrates PSND ex from the financial year ending March 1994 to the end of June 2018, highlighting the BoE contribution to net debt; due largely to its quantitative easing measures, through the activities of the Asset Purchase Facility (including the Term Funding Scheme).

Figure 8: Public sector net debt (excluding public sector banks)

March 1994 to the end of June 2018, UK

Source: Office for National Statistics

Notes:

Includes Asset Purchase Facility (APF), which includes the Term Funding Scheme (TFS).

Public sector net debt excluding public sector banks (PSND ex) is the combination of PSND ex Bank of England (BoE) plus BoE contribution to PSND ex.

Download this image Figure 8: Public sector net debt (excluding public sector banks)

.png (43.2 kB) .xls (67.1 kB){kind=link}

9. How much cash does the public sector need to raise?

The net cash requirement is a measure of how much cash the public sector needs to raise from the financial markets (or pay out from its cash reserves) to finance its activities. This amount can be close to net borrowing for the same period but there are some transactions, for example, lending to the private sector or the purchase of shares, that need to be financed but do not contribute to net borrowing. Similarly, repayments of principal on loans extended by government or sales of shares will reduce the level of financing necessary but not reduce the net borrowing.

Figure 9 presents public sector cash requirement by sub-sector in the current financial year-to-date (April to June 2018). Time series for each of these component series are presented in Table PSA7A in the Public sector finances Tables 1 to 10: Appendix A dataset.

Figure 9: Contributions to public sector net cash requirement (excluding public sector banks) by sub-sector

Current financial year-to-date (April to June 2018), UK

Source: Office for National Statistics

Notes:

Effects of cash transactions between sub-sectors are removed in calculating public sector total net cash requirement (and consolidated expenditure and income totals).

APF – Bank of England Asset Purchase Facility.

Download this image Figure 9: Contributions to public sector net cash requirement (excluding public sector banks) by sub-sector

.png (51.0 kB) .xls (170.0 kB){kind=link}

Central government net cash requirement (CGNCR) is a focus for some users, as it provides an indication of the volume of gilts (government bonds) the Debt Management Office may issue to meet the government’s borrowing requirements.

In the current financial year-to-date (April to June 2018), CGNCR was £14.1 billion, that is, £1.9 billion more than in the previous year. This increase in net cash requirement is due largely to a reduction of £4.2 billion in the sale of assets between these periods.

In the current financial year, central government received £8.6 billion in cash terms from the sale of assets (£1.4 billion in spectrum licences, £5.3 billion in UK Asset Resolution (UKAR) mortgage assets and £2.5 billion in Royal Bank of Scotland (RBS) shares), while over the same period in 2017, this figure stood at £12.8 billion (£11.8 billion of UKAR mortgage assets).

CGNCR is quoted both including and excluding the net cash requirement of Network Rail (NR) and UKAR, which manages the closed mortgage books of both Bradford and Bingley, and Northern Rock Asset Management. It is the CGNCR excluding NR and UKAR that is the particular focus of users with an interest in the gilt market.

CGNCR excluding NR and UKAR increased by £2.1 billion to £14.4 billion in the current financial year-to-date (April to June 2018), compared with the same period in 2017.

Nôl i'r tabl cynnwys10. How was debt in the latest financial year accumulated?

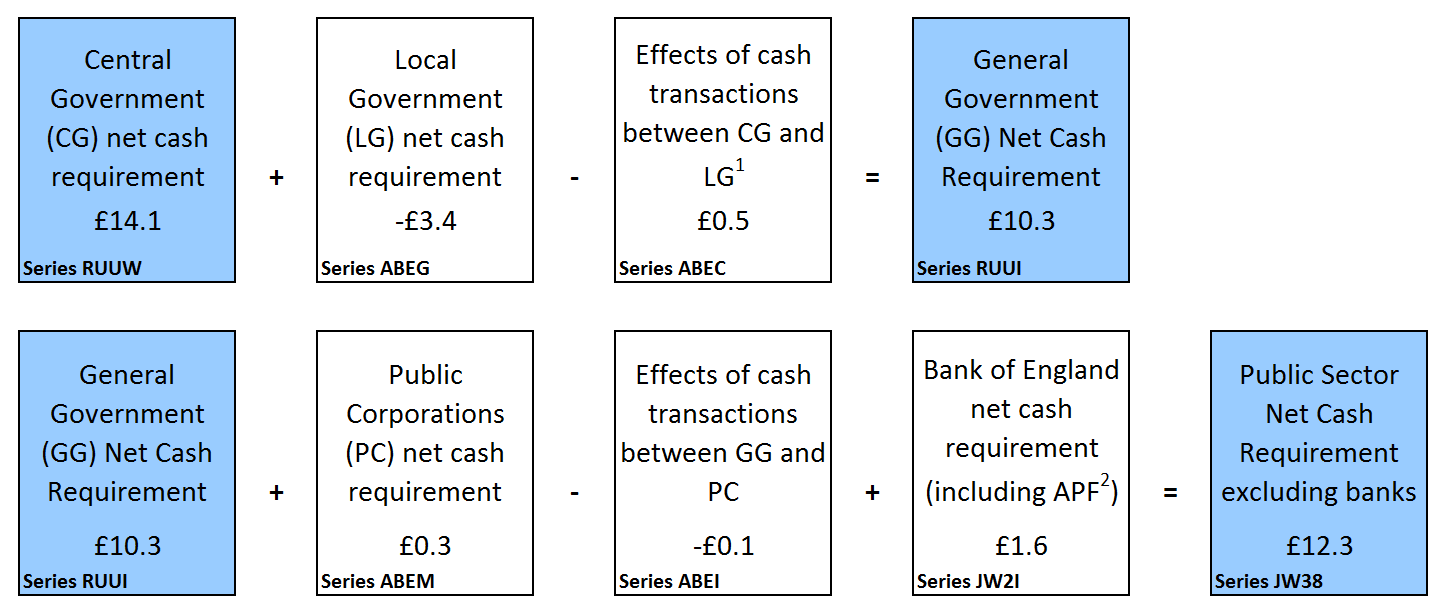

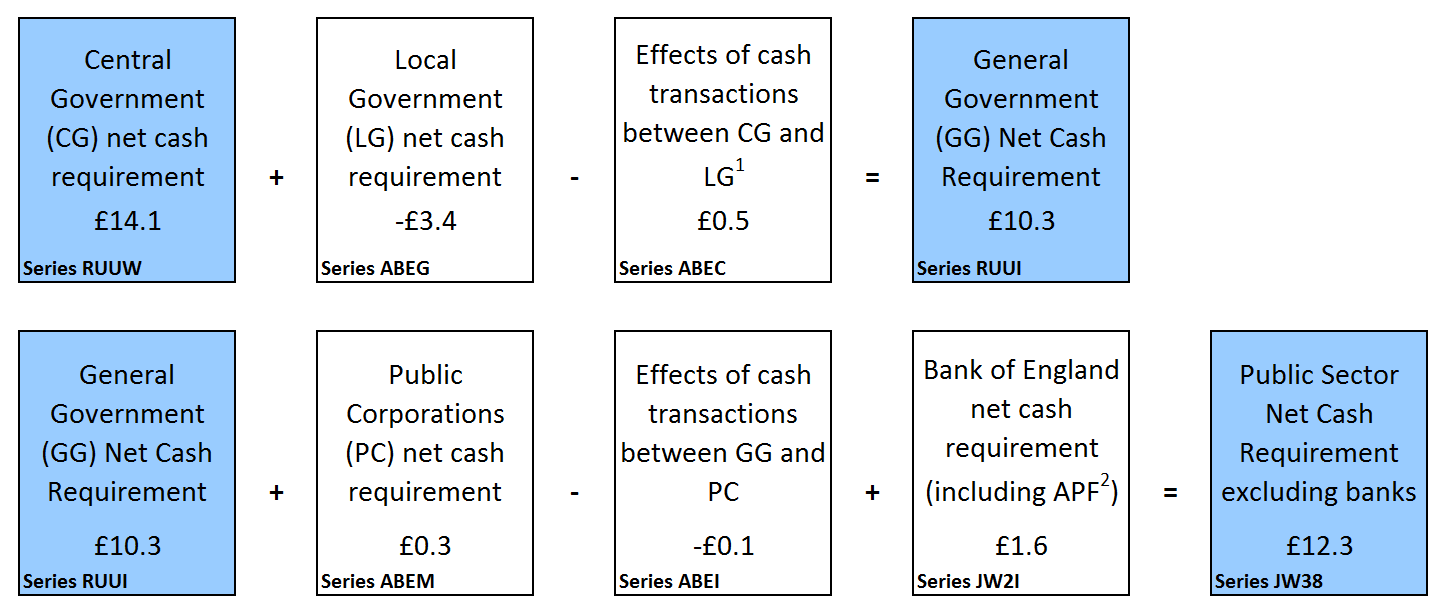

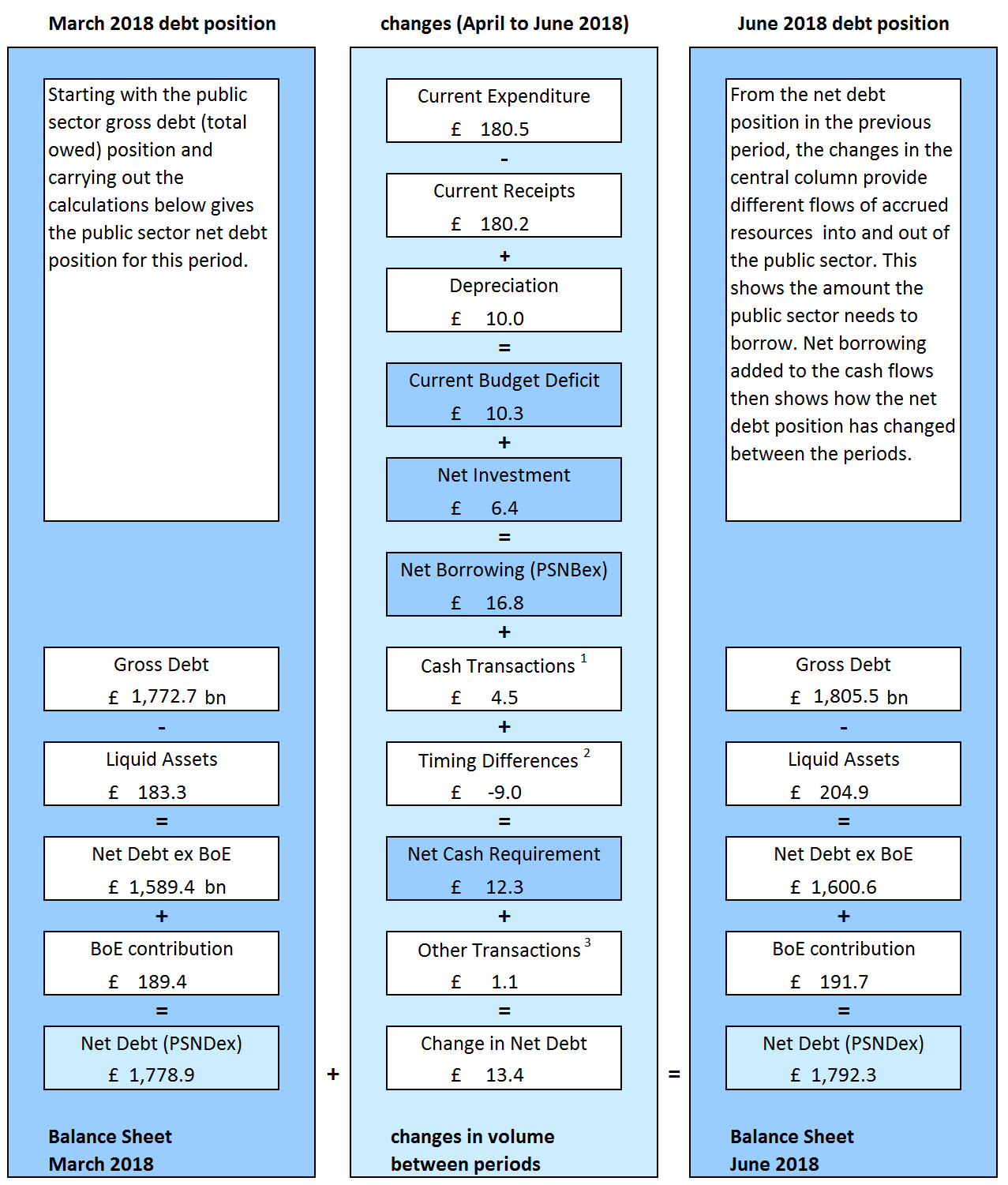

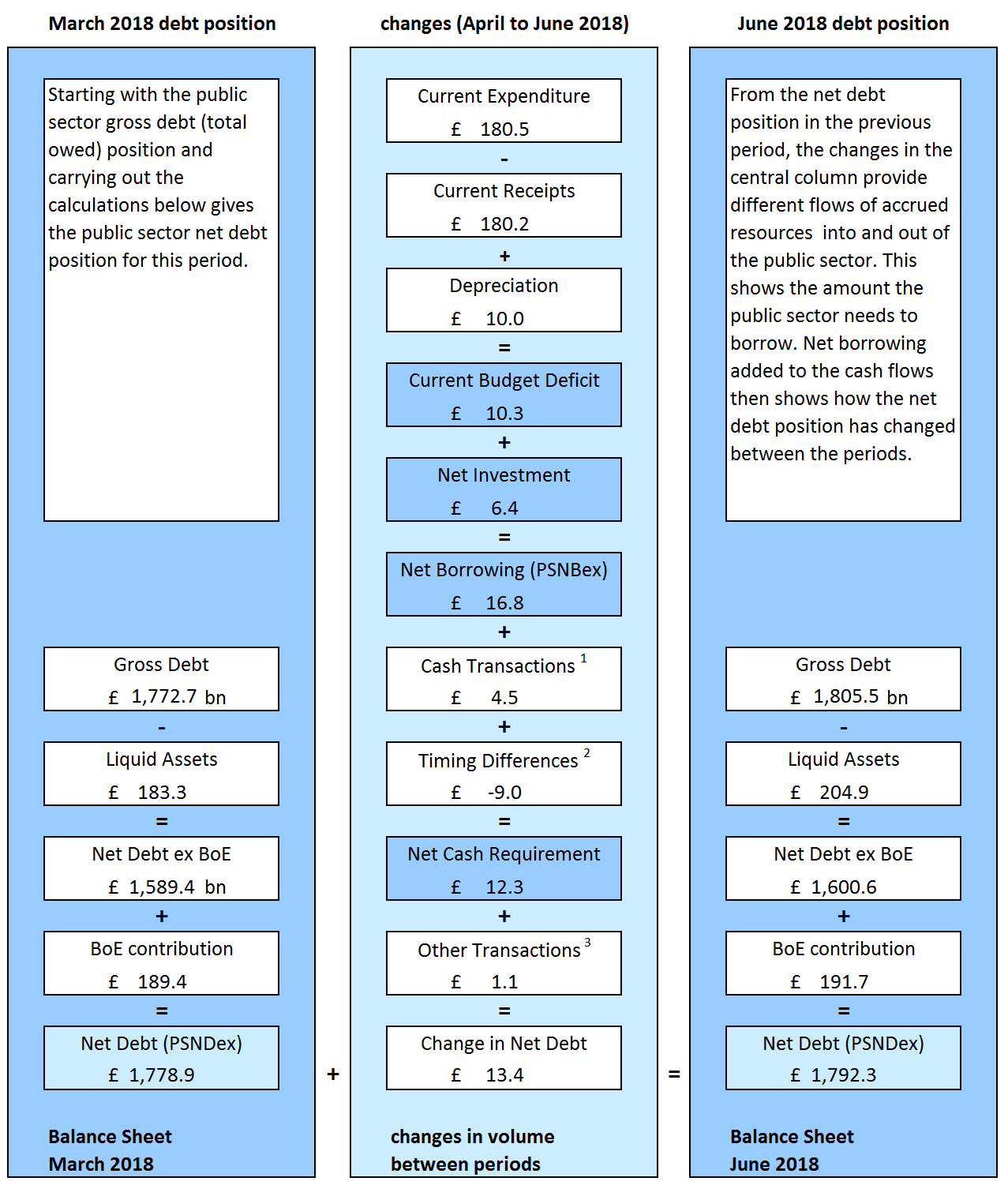

Figure 10 brings together the borrowing components detailed in Figure 3 to illustrate how the differences between income and spending (both current and capital) have led to the accumulation of debt in the current financial year-to-date (April to June 2018).

This presentation excludes public sector banks, focusing instead on the public sector net borrowing excluding public sector banks (PSNB ex) measure.

The reconciliation between public sector net borrowing and net cash requirement is presented in more detail in Table REC1 in the Public sector finances Tables 1 to 10: Appendix A dataset.

Figure 10: Components of net debt

How the difference in expenditure and receipts affect public sector net debt (excluding public sector banks), UK

Source: Office for National Statistics

Notes:

Cash transactions in (non-financing) financial assets, which do not impact on net borrowing.

Timing differences between cash and accrued data.

Revaluation of foreign currency debt (for example, foreign currency). Debt issuances or redemptions above or below debt valuation (for example, bond premia and discounts and capital uplifts). Changes in volume of debt not due to transactions (for example, sector reclassification).

Download this image Figure 10: Components of net debt

.png (94.3 kB) .xls (60.4 kB){kind=link}

11. How do these figures compare with official forecasts?

The Office for Budget Responsibility (OBR) normally produces forecasts of the public finances twice a year (currently in March and November). The government has adopted OBR forecasts as its official forecast.

OBR forecasts used in this bulletin are based on those published on 13 March 2018.

Public sector net borrowing (excluding public sector banks) in the financial year ending March 2018 was £39.4 billion; that is, £6.3 billion less than in the previous financial year (April 2016 to March 2017) and £5.8 billion less than the £45.2 billion forecast by OBR. However, this £39.4 billion represents our fourth estimate and will be revised over the coming months as we replace our initial estimates with provisional and then final outturn data.

Over the financial year ending March 2019, OBR expects the public sector to borrow £37.1 billion; around one-quarter of what it borrowed between March 2009 and April 2010, at the peak of the financial crisis.

Figure 11 presents the cumulative public sector net borrowing for the latest full financial year. The figure also presents the OBR forecasts for the current financial year (April 2018 to March 2019), as well as the cumulative borrowing in the current financial year-to-date (April to June 2018).

The monthly path of spending and receipts is not smooth within the financial year and also can vary compared with previous years, both of which can affect year-on-year comparisons.

Figure 11: Public sector net borrowing (excluding public sector banks)

Cumulative financial year-to-date (April to June 2018) compared with the financial year ending March 2018 (April 2017 to March 2018), UK

Source: Office for National Statistics

Notes:

For the financial year ending 2018 (April 2017 to March 2018).

For the financial year-to-date ending 2019 (April to June 2018).

OBR forecast for public sector net borrowing excluding public sector banks from March 2018 Economic and Fiscal Outlook (EFO).

Download this chart Figure 11: Public sector net borrowing (excluding public sector banks)

Image .csv .xlsTable 1 compares the current outturn estimates for each of our main public sector (excluding public sector banks) aggregates for the latest full financial year with corresponding OBR forecasts for the following financial year. Further, it compares the current financial year-to-date (April to June 2018) outturn estimates with those of the previous financial year.

Caution should be taken when comparing public sector finances data with OBR figures for the full financial year, as data are not finalised until sometime after the financial year ends, with initial estimates made soon after the end of the financial year often subject to sizeable revisions in later months as forecasts are replaced with audited outturn data.

There may also be known methodological differences between OBR forecasts and outturn data.

Table 1: Latest outturn estimates compared with Office for Budget Responsibility forecasts

| Office for Budget Responsibility (OBR) forecasts in the current financial year-to-date (April to June 2018) compared with the latest full financial year (April 2017 to March 2018), UK | |||||||

| Excluding public sector banks | £ billion1 (not seasonally adjusted) | ||||||

|---|---|---|---|---|---|---|---|

| Financial year-to-date7 | Full financial year8 | ||||||

| 2017/18 | 2018/19 | % change | 2017/18 outturn | 2018/19 OBR forecast9 | % change | ||

| Current budget deficit2 | 14.7 | 10.3 | -29.8 | -1.3 | -1.9 | 46.9 | |

| Net investment3 | 7.4 | 6.4 | -13.8 | 40.6 | 39.0 | -4.0 | |

| Net borrowing 4 | 22.2 | 16.8 | -24.4 | 39.4 | 37.1 | -6.0 | |

| Net debt 5 | 1,759.3 | 1,792.3 | 1.9 | 1,778.9 | 1835.0 | 3.2 | |

| Net debt as a percentage of GDP6 | 86.2 | 85.2 | NA | 85.3 | 85.5 | NA | |

| Source: Office for National Statistics | |||||||

| Notes: | |||||||

| 1. Unless otherwise stated. | |||||||

| 2. Current budget deficit is the difference between current expenditure (including depreciation) and current receipts. | |||||||

| 3. Net investment is gross investment (net capital formation plus net capital transfers) less depreciation. | |||||||

| 4. Net borrowing is current budget deficit plus net investment. | |||||||

| 5. Net debt is financial liabilities (for loans, deposits, currency and debt securities) less liquid assets. | |||||||

| 6. GDP at current market price. | |||||||

| 7. Financial year-to-date refers to the period from April to June. | |||||||

| 8. 2018/19 refers to financial year ending in March 2019 and 2017/18 refers to financial year ending in March 2018. | |||||||

| 9. All OBR figures are from the OBR Economic and Fiscal Outlook published in March 2018. | |||||||

| 10. NA means "not applicable". | |||||||

Download this table Table 1: Latest outturn estimates compared with Office for Budget Responsibility forecasts

.xls (50.7 kB)12. Revisions since previous release

Revisions can be the result of both updated data sources and methodology changes. This month, the reported revisions are as a result of updated data sources only.

It is important to note that revisions do not occur as a result of errors; errors lead to corrections and are identified as such when they occur. This month we have no errors to report.

Table 2 presents the revisions to the headline statistics presented in this bulletin compared with those presented in the previous publication (published on 21 June 2018).

Table 2: Revisions to main aggregates

| Revisions since the previous public sector finances bulletin (published 21 June 2018), UK | |||||||||

| £ billion1 (not seasonally adjusted) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Net borrowing | |||||||||

| Period | CG2 | LG3 | NFPCs4 | BoE5 | PSNB ex6 | PSND ex7 | PSND % of GDP | PSNCR ex8 | |

| 1999/00 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.1 | 0.0 | |

| 2000/01 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.1 | 0.0 | |

| 2001/02 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | |

| 2002/03 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.1 | 0.0 | |

| 2003/04 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.1 | 0.0 | |

| 2004/05 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | |

| 2005/06 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.1 | 0.0 | |

| 2006/07 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.1 | 0.0 | |

| 2007/08 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.2 | 0.0 | |

| 2008/09 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.2 | 0.0 | |

| 2009/10 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.3 | 0.0 | |

| 2010/11 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.4 | 0.0 | |

| 2011/12 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.4 | 0.0 | |

| 2012/13 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.4 | 0.0 | |

| 2013/14 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.3 | 0.0 | |

| 2014/15 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.3 | 0.0 | |

| 2015/16 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.3 | 0.0 | |

| 2016/17 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | -0.1 | 0.0 | 0.0 | |

| 2017/18 | -0.1 | 0.0 | 0.0 | 0.0 | -0.1 | -0.1 | -0.1 | 0.0 | |

| 2018/19 YTD | -0.6 | 0.1 | 0.1 | 0.0 | -0.5 | 0.4 | -0.1 | 0.2 | |

| 2018 April | -0.3 | 0.0 | 0.0 | 0.0 | -0.2 | 0.2 | -0.2 | 0.0 | |

| 2018 May | -0.4 | 0.1 | 0.0 | 0.0 | -0.3 | 0.4 | -0.1 | 0.2 | |

| Source: Office for National Statistics | |||||||||

| Notes: | |||||||||

| 1. Unless otherwise stated. | |||||||||

| 2. Central government. | |||||||||

| 3. Local government. | |||||||||

| 4. Non-financial public corporations. | |||||||||

| 5. Bank of England. | |||||||||

| 6. Public sector net borrowing excluding public sector banks. | |||||||||

| 7. Public sector net debt excluding public sector banks. | |||||||||

| 8. Public sector net cash requirement excluding public sector banks. | |||||||||

| 9. 2017/18 represents financial year ending 2018 (April 2017 to March 2018). | |||||||||

| 10. 2018/19 YTD refers to the current financial year-to-date (April to May 2018). | |||||||||

Download this table Table 2: Revisions to main aggregates

.xls (52.7 kB)Revisions to public sector net borrowing (excluding public sector banks) in the current financial year-to-date (April to May 2018)

The data for the latest month of every release contain some forecast data. The initial outturn estimates for the early months of the financial year, particularly April, contain more forecast data than other months, as profiles of tax receipts, along with departmental and local government spending are still provisional. This means that the data for these months are typically more prone to revision than other months and can be subject to sizeable revisions in later months.

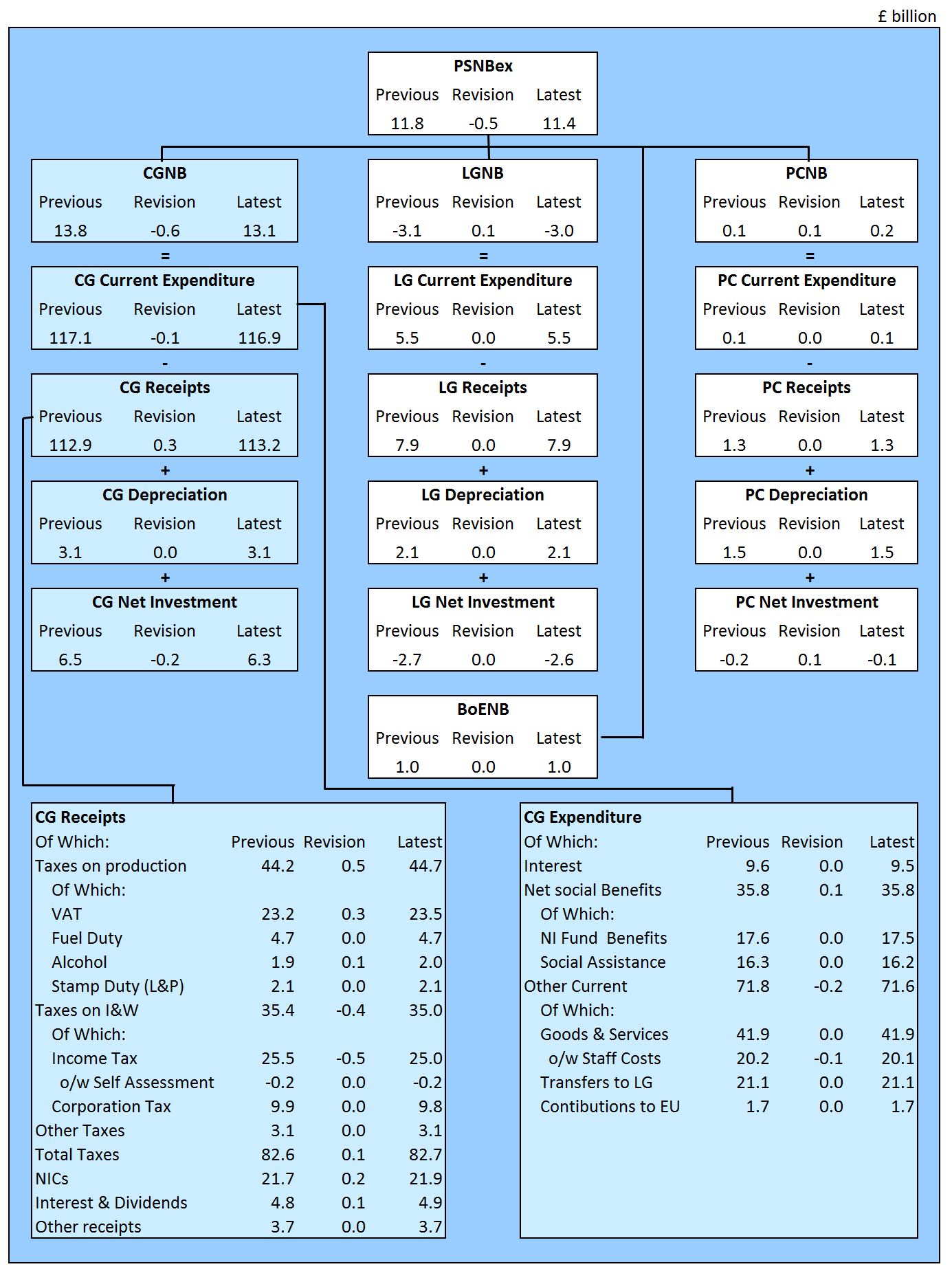

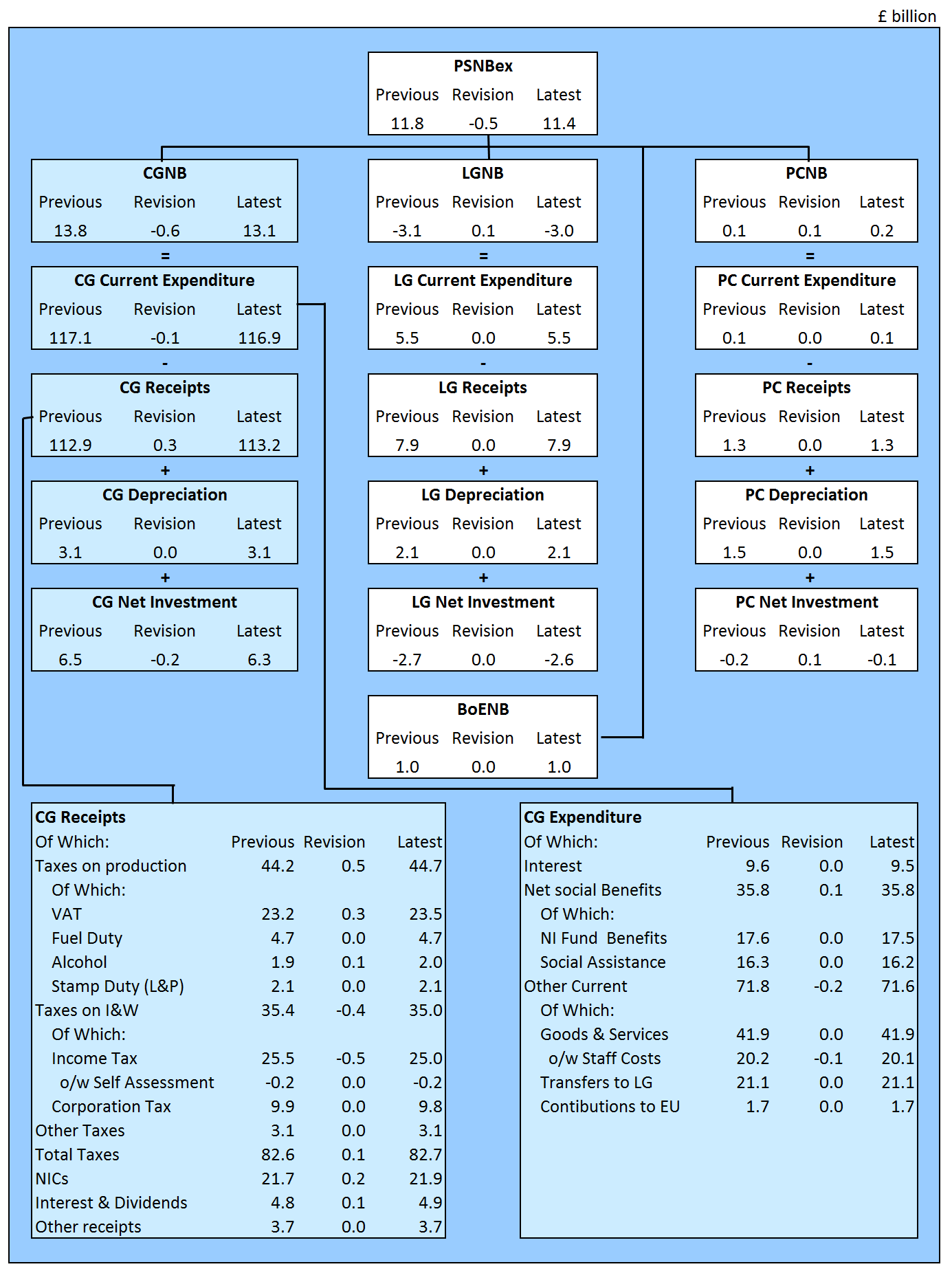

Public sector net borrowing excluding public sector banks (PSNB ex) has been revised down by £0.5 billion compared with figures presented in the previous bulletin (published on 21 June 2018).

Of this £0.5 billion downward revision to PSNB ex, there was a £0.6 billion reduction in the estimate of central government net borrowing, partially offset by a £0.1 billion increase in the estimation of both local government’s and public corporations’ contribution to net borrowing.

Central government receipts were revised upwards by £0.3 billion, with increases in previous estimates of Value Added Tax, National Insurance contributions and Alcohol Duties of £0.3 billion, £0.2 billion and £0.1 billion respectively. These increases in revenue were partially offset by a decrease of £0.5 billion in the previous estimate of Income Tax.

In the same period, both central government current and capital expenditure were revised downwards by £0.1 billion and £0.2 billion respectively.

Figure 12 breaks down this revision to PSNB ex by each of its four sub-sectors: central government, local government, non-financial public corporations and Bank of England (BoE).

The figure also provides a further breakdown of central government current receipts and current expenditure reflecting the significance of these components within borrowing at a public sector level.

Figure 12: Revisions to net borrowing

Latest data covering April to May 2018, compared with that presented in the previous bulletin (21 June 2018), UK

Source: Office for National Statistics

Notes:

PSNBex – Public sector net borrowing excluding public sector banks.

CGNB – Central government net borrowing.

LGNB – Local government net borrowing.

PCNB – Non-financial public corporations net borrowing.

BoENB – Bank of England net borrowing.

L&P – Land and property.

I & W – Income and wealth.

Contributions to EU – UK VAT, GNI and abatement contributions to the EU budget.

NICs – National Insurance contributions.

Download this image Figure 12: Revisions to net borrowing

.png (123.2 kB) .xls (88.6 kB){kind=link}

Revisions to public sector net debt (excluding public sector banks)

This month we have increased our estimate of public sector net debt (excluding public sector banks) as at the end of May 2018, by £0.4 billion. This revision was due in part to a reduction of £0.1 billion in our estimate of public corporations’ liquid assets and in part to a £0.3 billion increase in our estimate of Bank of England’s contribution to net debt.

Data covering the normal operations Bank of England (those operations that exclude the Asset Purchase Facility Fund) are sourced from their annual report. The 2018 annual report (covering 1 March 2017 to 28 February 2018) was published on 14 June 2018. We used the data contained in this report to calculate net debt, borrowing and cash requirement data for The Bank and used these estimates to inform our projections of data from March 2018 to date.

Revisions to public sector net debt (excluding public sector banks) as a ratio of GDP

Though revisions to the monetary value of net debt are limited to recent periods, the ratio of net debt to GDP has been revised back to the financial year ending March 1997. These changes are as a result of us including the latest estimates of GDP (published on 29 June 2018).

Revisions to public sector net borrowing (including public sector banks)

This month we received updated public sector banks’ profit and loss data covering the period July to December 2017. These data have enabled us to update previous estimates of the net borrowing associated with public sector banks. Further, estimates covering the period January 2018 to date have been updated to reflect this new information.

As a consequence of receiving these data, our estimate of public sector net borrowing has increased by £6.7 billion in the financial year ending March 2018 and £1.0 billion in the current financial year-to-date.

Nôl i'r tabl cynnwys13. International comparisons of borrowing and debt

The UK government debt and deficit statistical bulletin is published quarterly (in January, April, July and December each year), to coincide with when the UK and other EU member states are required to report on their deficit (or net borrowing) and debt to the European Commission.

On 17 July 2018, we published UK government debt and deficit: March 2018, consistent with Public sector finances, UK: May 2018 (published on 21 June 2018). In this publication we stated that:

general government gross debt was £1,763.8 billion at the end of March 2018, equivalent to 85.8% of gross domestic product (GDP); 25.8 percentage points above the Maastricht reference value of 60%

general government deficit (or net borrowing) was £40.7 billion in the financial year ending March 2018, equivalent to 2.0% of GDP; 1.0 percentage point below the Maastricht reference value of 3%

The UK general government debt and deficit data we published on 17 July 2018 were published by Eurostat on 20 July 2018 in context with the other 27 EU member states.

It is important to note that the GDP measure, used as the denominator in the calculation of the debt ratios in the UK government debt and deficit statistical bulletin, differs from that used within the Public sector finances statistical bulletin.

Nôl i'r tabl cynnwys14. Background information

What does the public sector include?

In the UK, the public sector consists of five sub-sectors: central government, local government, public non-financial corporations, Bank of England and public financial corporations (or public sector banks).

Unless otherwise stated, the figures quoted in this bulletin exclude public sector banks (that is, currently only Royal Bank of Scotland (RBS)), as the reported position of debt (and to a lesser extent borrowing) would be distorted by the inclusion of RBS's balance sheet (and transactions). This is because government does not need to borrow to fund the debt of RBS, nor would surpluses achieved by RBS be passed on to government, other than through any dividends paid as a result of government equity holdings.

The sub-sector breakdown of public sector net borrowing is summarised in Table PSA2 in the Public sector finances Tables 1 to 10: Appendix A dataset.

Should I look at monthly or financial year-to-date data to understand public sector finances?

A financial year is an accounting period of 12 months running from 1 April one year to 31 March the following year. For example, the financial year ending March 2016 comprises the months from April 2015 to March 2016.

Due to the volatility of the monthly data, the cumulative financial year-to-date borrowing figures provide a better indication of the position of the public finances than the individual months.

Are our figures adjusted for inflation?

All monetary values in the Public sector finances (PSF) bulletin are expressed in terms of “current prices‟, that is, they represent the price in the period to which the expenditure or revenue relates and are not adjusted for inflation.

In order to compare data over long time periods, to aid international comparisons and provide an indication of a country’s ability to service borrowing and debt, commentators often discuss changes over time to fiscal aggregates in terms of gross domestic product (GDP) ratios. GDP represents the value of all the goods and services currently produced by the UK economy in a period of time.

The use of GDP in public sector fiscal ratio statistics

An article, The use of GDP in public sector fiscal ratio statistics, explains that for debt figures reported in the monthly public sector finances, a 12-month GDP total centred on the month is employed, while in the UK government debt and deficit statistical bulletin, the total GDP for the preceding 12 months is used.

As a consequence of using a centred GDP estimate, our estimates include a degree of official forecast data produced by the Office for Budget Responsibility (OBR) and are subject to revision when the OBR updates its estimates (usually in March and November each year).

Figures expressed as a ratio of gross domestic product

At the end of each financial year, while data for current budget deficit, net investment and net borrowing for the final quarter of the financial year (January to March) are available, GDP for the corresponding period is not. To enable us to publish estimates of these figures as ratios of GDP for the latest full financial year, the final quarter of the GDP denominator is estimated based on forecasts produced by the OBR.

This estimate of GDP will be used in the March, April and May publications and was revised in the June publication when the published value of GDP became available.

Are our figures adjusted for seasonal patterns?

All monetary values in the PSF bulletin are not seasonally adjusted. We recommend you use year-on-year comparisons (be it cumulative financial year-to-date or individual monthly borrowing figures) rather than making month-on-month comparisons.

Are our monthly figures likely to change over time?

Each PSF bulletin contains the first estimate of public sector borrowing for the most recent period and is likely to be revised in later months as more data become available.

In publishing monthly estimates, it is necessary to use a range of different types of data sources. Some of these are subject to revision as budget estimates (forecasts) are replaced by outturn data and these then feed into the published aggregates.

In addition to those that stem from updated data sources, revisions can also result from methodology changes. An example of the latter is the changes that were due to the introduction of improved methodology for the recording of Corporation Tax, Bank Corporation Tax Surcharge receipts and Bank Levy implemented in the PSF estimates released in February 2017.

Appendix F: Revisions to the first reported estimate of financial-year-end public sector net borrowing (excluding public sector banks) by sub-sector; summarises revisions to the first estimate of public sector borrowing (excluding public sector banks) by sub-sector for the last six financial years. Revisions are shown at 6 and 12 months after year end.

We have published an article, Public Sector Finances – Sources summary and their timing (PDF, 22KB), which provides a brief summary of the different sources used and the implications of using those data in the monthly public sector finances (PSF) statistical bulletin.

Why do some of the tax figures quoted by HMRC differ from those presented in this bulletin?

There are a number of differences between the presentation of tax receipts reported by both Office for National Statistics (ONS) and HM Revenue and Customs (HMRC) in their respective publications.

HMRC present their data on a cash basis, while we present the corresponding data on both a cash basis (in the calculation of central government net cash requirement – Table PSA7D) and on a time-adjusted (or accruals) basis (in the calculation of central government net borrowing – Table PSA6B and 6D).

Further, we roll some individual taxes together to form aggregates, where HMRC may not. For example, we present Corporation Tax as an aggregate of Corporation Tax, Bank Surcharge and Diverted Profit Tax, while HMRC present these taxes individually.

The differences between HMRC and ONS’s tax presentation is discussed further in Section 7 of the PSF Quality and Methodology Information (QMI) report, with a focus on the three of the largest tax headings: Value Added Tax (VAT), Corporation Tax and Income Tax.

Alignment between public sector finances and national accounts: June 2018

On 29 June 2018, we published an article explaining the differences between public sector net borrowing estimates published in the public sector finances and those in the national accounts. The article forms a part of a regular series of articles published annually alongside the Blue Book publication.

Nôl i'r tabl cynnwys15. Planned changes for future releases

On 17 July 2018, we published an article Looking ahead: developments in public sector finance statistics, providing users with an overview of those areas where existing methodologies are, or will be, under review.

The aim is to give users early sight of those areas where the fiscal statistics might be significantly impacted by methodological or classification changes during the coming 24 months. The article is designed to help government in its fiscal planning and support the Office for Budget Responsibility (OBR) in its role in producing fiscal forecasts. For this reason, the publication date was set to coincide with the OBR’s publication of their latest Fiscal Sustainability Report. The article was the first ONS article of this type.

The article discusses the following topics:

- student loans

- pensions

- depreciation

- leases

- public sector financial assets

East Coast Mainline

On 16 May 2018, the government announced that from 24 June 2018, London North Eastern Railway (LNER) will take over the running of East Coast Mainline services. We are currently investigating the implications of this decision and our conclusions will be announced in due course.

Nôl i'r tabl cynnwys16. Recent announcements concerning the Term Funding Scheme

On the 21 June 2018, the government published a new Memorandum of Understanding between HM Treasury and the Bank of England (BoE), which sets out the financial relationship between the two institutions.

This memorandum announced that during the current financial year (April 2018 to March 2019), the £127 billion liabilities of the Term Funding Scheme (TFS) will be transferred from the Bank of England Asset Purchase Facility Fund (APF) to the Bank’s own balance sheet and that the HM Treasury indemnity for it was being removed.

TFS was introduced in 2016, as a quantitative easing measure under the APF umbrella, to enable financial institutions to cut the time in passing on interest rate reductions to consumers and businesses.

This change will have no impact on public sector net debt (both including and excluding public sector banks).

Further, to enable the Bank to take TFS on balance sheet without an indemnity from the Treasury, a capital injection of £1.2 billion from HM Treasury to BoE has been announced. The nature of the capital injection will be formally discussed at a classifications meeting and announced in due course.

In conjunction with this work we will review our presentation of the loans associated with the Bank of England Asset Purchase Facility Fund in Table PSA9, a part of Appendix A to this release.

Nôl i'r tabl cynnwys17. Recent events that may impact on public sector finances

This section acknowledges recent government announcements that may have future implications on public sector finances.

EU withdrawal agreement

On 8 December 2017, the government published a joint report on progress during phase 1 of negotiations between the European Union and the UK (PDF, 383KB), under Article 50 of the Treaty on European Union (TEU) on the UK’s orderly withdrawal from the EU.

Although the Office for Budget Responsibility (OBR) discusses the EU settlement in Annex B (PDF, 2.5MB) of their Economic and Fiscal Outlook – March 2018, the details in the report are still subject to negotiation and so there is insufficient certainty at this stage for us to complete a formal assessment of impact on the UK public sector finances.

Carillion insolvency

Following Carillion Plc declaring insolvency on 15 January 2018, the UK government announced that it will provide the necessary funding required by the Official Receiver, to ensure continuity of public services through an orderly liquidation. The Official Receiver has been appointed by the court as liquidator, along with partners at PwC that have been appointed Special Managers. The defined benefit pension schemes of former Carillion employees are currently being assessed by the Pension Protection Fund (PPF) prior to any transition into the PPF scheme.

We are currently investigating the various impacts of the liquidation of Carillion on the public sector finances, including in relation to the public-private partnership projects in which Carillion was involved and the additional funding that the government has provided in order to maintain public services. We will announce our findings in due course.

Prior to liquidation, Carillion held approximately 450 contracts with government, representing 38% of Carillion’s 2016 reported revenue.

Nôl i'r tabl cynnwys18. Quality and methodology

The Public sector finances Quality and Methodology Information (QMI) report contains important information on:

the strengths and limitations of the data and how it compares with related data

uses and users of the data

how the output was created

the quality of the output including the accuracy of the data

This report was last updated on 7 March 2018.

Monthly statistics on the public sector finances: a methodological guide

On 21 June 2018, we published an updated methodological guide providing comprehensive contextual and methodological information concerning the monthly Public sector finances statistical bulletin. The guide sets out the conceptual and fiscal policy context for the bulletin, identifies the main fiscal measures, and explains how these are derived and inter-related. Additionally, it details the data sources used to compile the monthly estimates of the fiscal position.

The guide updates and summarises the content of a range of published articles, including the previous version of the PSF methodology guide published in August 2012 (360.2KB).

How is the debt interest paid by the government affected by movements in the level of Retail Prices Index?

Index-linked gilts, a form of government bond, are indexed to the Retail Prices Index (RPI). When the RPI rises, the inflation uplift that applies to index-linked cash flows (both regular coupon payments and final payment at gilt maturity) also rises. If the RPI should fall, the inflation uplift would also fall. In this way, the returns to the investor from holding index-linked gilts are maintained in real terms – as measured by the RPI.

Taking £100 as the unit price for a gilt, an index-linked gilt will pay more than £100 at redemption if the RPI increases over the life of the gilt. Similarly, if the RPI increases over the life of the gilt each coupon payment will be higher than the previous one; while if the RPI were to decrease, a coupon payment could be lower than the previous one.

Both the uplift on coupon payments and the uplift on the redemption value are recorded as debt interest paid by the government, so month-on-month there can be sizeable movements in payable government debt interest as a result of movements in the RPI.

The RPI applied to index-linked gilts is typically lagged by three months (though some older gilts have an eight-month lag). As a result of this lag, the amount central government spends on interest on its outstanding debt is typically low in March compared with the rest of the year. In January, prices are typically discounted (for example, due to January sales), so depressing the RPI and decreasing the uplift on index-linked gilts in March, three months later.

Time series of central government debt interest (series identifier NMFX) and the index-linked gilt capital uplift (series identifier MW7L) are available in Tables PSA6B and REC3 in the tables associated with this release or by searching directly by series identifier.

Adjustments to local government data in the current financial year

Most local government data are annual, relating to financial years (April to March), and based on information collected from local authorities by the Ministry of Housing, Communities and Local Government, and the devolved administrations.

The data are collected in two main phases: budget, before the start of the financial year, and outturn, after the end of the financial year.

Some information is available within the year and this is taken into account wherever possible.

In recent years, planned expenditure initially reported in budgets has systematically been higher than the final outturn expenditure reported in the audited accounts. We therefore include adjustments to reduce the amounts reported at the budget stage and this affects the figures for the latest financial year. Each quarter, this underspend adjustment is reviewed such that it reflects the latest available information.

UK Statistics Authority assessment of public sector finances

On 20 June 2017, the UK Statistics Authority published a letter confirming the designation of the monthly Public sector finances bulletin as a National Statistic. This letter completes the 2015 assessment of public sector finances.

In order to meet the requirements of this assessment we published an article, Quality assurance of administrative data used in the UK public sector finances. This report provides an assessment of the administrative data sources used in the compilation of the public sector finances statistics in accordance with the UK Statistics Authority’s Administrative Data Quality Assurance Toolkit.

We introduced a new supplementary fiscal aggregate of public sector net financial liabilities (PSNFL) as an Experimental Statistic in November 2016, explaining that there would be an ongoing programme of work to improve the quality of its underlying data. As a result of improvements to date, in April 2018, public sector net financial liabilities excluding public sector banks (PSNLF ex) was re-designated from an Experimental Statistic to an official statistic.

How classification decisions are made

Each quarter we publish a forward workplan outlining the classification assessments we expect to undertake over the coming 12 months. To supplement this, each month a classifications update is published, which announces classification decisions made and includes expected implementation points (for different statistics) where possible.

Classification decisions are reflected in the public sector finances at the first available opportunity and, where necessary, outlined in this section of the statistical bulletin.

Pre-release access to ONS statistics

On 15 June 2017, the National Statistician announced that from 1 July 2017 pre-release access to Office for National Statistics (ONS) statistics would cease. While there is no longer any pre-release access granted to the Public sector finances bulletin, it should be noted that this bulletin remains jointly produced by members of the Government Statistical Service (GSS) working in both ONS and HM Treasury.

GSS staff will continue to work together to produce the bulletin but ministers and those officials not directly involved in the production and release of statistics will not have access to them in advance of publication.

Time series data

All data contained within these publications are available to download via the Public sector finances time series dataset. From April 1997 to date, where available, time series are presented as monthly data, with series extending further back in time, generally presented on a quarterly or financial year basis.

Time series exclusive to the public sector finances borrowing by sub-sector presentation are only available as quarterly time series, though these extend back to 1946.

Supporting documentation

Documentation supporting this publication is available in appendices to the bulletin:

Large impacts on public sector fiscal measures excluding banking groups: Appendix B

Public sector finances revisions analysis on main fiscal aggregates: Appendix C

Impact of the reclassification of housing associations into the public sector: Appendix E

Revisions to the first reported estimate of public sector net borrowing: Appendix F

Public sector borrowing by sub-sector

Each month, at 9:30am on the working day following the Public sector finances statistical bulletin, we publish Public sector finances borrowing by sub-sector. This release contains an extended breakdown of public sector borrowing in a matrix format and also estimates of total managed expenditure (TME).

Nôl i'r tabl cynnwys