Cynnwys

- The effects of the coronavirus pandemic

- Main points

- Challenges of measuring the effects of the coronavirus pandemic on the public finances

- Central government net cash requirement

- Borrowing

- Borrowing in April 2020

- Borrowing in the financial year ending March 2020

- Debt

- Revisions

- Public sector finances data

- Glossary

- Measuring the data

- Strengths and limitations

- Related links

2. Main points

The effects of the coronavirus (COVID-19) pandemic are not fully captured in this release, meaning that estimates of national accounts-based (accrued) tax receipts, borrowing and gross domestic product (GDP) in particular are subject to greater than usual uncertainty.

Central government net cash requirement (central government net cash requirement excluding UK Asset Resolution Ltd, Network Rail and the COVID Corporate Finance Facility) in April 2020 was £63.5 billion, £73.3 billion more than in April 2019; the highest cash requirement in any month on record (records began in April 1984).

Central government net cash requirement in the latest full financial year was £56.5 billion, £19.6 billion more than in the previous financial year; the highest cash requirement in any financial year since the financial year ending March 2017.

Borrowing (public sector net borrowing excluding public sector banks, PSNB ex) in April 2020 is estimated to have been £62.1 billion, £51.1 billion more than in April 2019; the highest borrowing in any month on record (records began in January 1993).

Borrowing in March 2020 was revised up by £11.7 billion to £14.7 billion, largely due to a reduction in the previous estimate of tax receipts and National Insurance contributions and the recording of expenditure associated with the Coronavirus Job Retention scheme.

Borrowing in the latest full financial year (April 2019 to March 2020) is estimated to have been £62.7 billion, £22.5 billion more than in the previous financial year; these are not final figures and will be revised over the coming months as we replace our initial estimates with provisional and then final outturn data, and as more information on the effects of the COVID-19 pandemic becomes available.

Debt (public sector net debt excluding public sector banks, PSND ex) at the end of April 2020 was £1,887.6 billion (or 97.7% of GDP), an increase of £118.4 billion (or 17.4 percentage points) compared with April 2019; the largest year-on-year increase in debt as a percentage of GDP on record (monthly records began in March 1993).

4. Central government net cash requirement

Given the uncertainty around our national accounts-based (accrued) measures, this month we place a greater emphasis than usual on our leading cash measure, the central government net cash requirement (excluding both UK Asset Resolution Ltd and Network Rail).

The central government net cash requirement (CGNCR) is the amount of cash needed immediately for the UK government to meet its obligations. To obtain cash, the UK government sells financial instruments, gilts or Treasury Bills.

The amount of cash required will be affected by changes in the timing of tax payments by individuals and businesses but does not depend on forecast tax receipts in the same way as our national accounts-based (accrued) measures.

The CGNCR contains the timeliest information and is less susceptible to revision. However, as for any cash measure, the CGNCR does not reflect the overall amount for which government is liable or the point at which any liability is incurred – it only reflects when cash is received and spent.

Table 1 demonstrates how central government's net cash requirement is calculated from its cash receipts and cash outlays. This presentation focuses on the central government's own account and excludes cash payments to both local government and public non-financial corporations.

Notably, in April 2020 VAT cash receipts were negative at minus £0.9 billion, because VAT repayments, being made as normal, exceeded VAT payments.

Businesses can generally reclaim the VAT paid on goods and services purchased for use in their business. Where a business charges its customers less VAT than they paid on their purchases, HM Revenue and Customs (HMRC) repays the difference to the business.

Also, the government announced a deferral scheme for Value Added Tax payments, enabling UK businesses to pay VAT due between 20 March 2020 and 30 June 2020 at a later date (though before 31 March 2021). With some payments being deferred and repayments being made, overall cash VAT receipts are lower than usual in April 2020.

| £ billion | ||||||||

|---|---|---|---|---|---|---|---|---|

| April | Financial year | |||||||

| 2019 | 2020 | Change | % change | 2018/19 | 2019/20 | Change | % change | |

| Total paid over¹ | 58.4 | 32.7 | -25.7 | -44.0 | 589.7 | 602.2 | 12.5 | 2.1 |

| Of which: Income tax² | 18.4 | 14.6 | -3.8 | -20.7 | 200.2 | 204.3 | 4.0 | 2.0 |

| NICs³ | 13.5 | 11.1 | -2.4 | -17.8 | 136.6 | 143.1 | 6.4 | 4.7 |

| VAT⁴ | 13.0 | -0.9 | -13.9 | -106.9 | 131.9 | 130.0 | -2.0 | -1.5 |

| Corporation tax⁵ | 7.7 | 3.6 | -4.1 | -53.8 | 56.2 | 63.2 | 7.0 | 12.5 |

| Interest and dividends | 4.7 | 4.7 | 0.0 | -0.7 | 17.0 | 18.6 | 1.6 | 9.3 |

| Other receipts⁶ | -0.6 | 1.6 | 2.3 | 367.0 | 25.3 | 30.7 | 5.4 | 21.3 |

| Total cash receipts | 62.5 | 39.1 | -23.5 | -37.5 | 632.0 | 651.5 | 19.5 | 3.1 |

| Interest payments | 0.7 | 11.0 | 10.3 | 1,454.3 | 37.8 | 35.9 | -1.9 | -5.0 |

| Net acquisition of company securities⁷ | -4.3 | 0.0 | 4.3 | 100.0 | -12.7 | -4.3 | 8.4 | 66.1 |

| Net department outlays⁸ | 55.8 | 91.4 | 35.5 | 63.7 | 636.7 | 668.2 | 31.5 | 5.0 |

| Of which: CJRS⁹ | 0.0 | 5.2 | 5.2 | 100.0 | - | - | - | - |

| Total cash outlays | 52.2 | 102.3 | 50.1 | 95.9 | 661.7 | 699.8 | 38.1 | 5.8 |

| Own account NCR¹⁰ | -10.3 | 63.3 | 73.6 | 714.3 | 29.8 | 48.4 | 18.6 | 62.6 |

| NRAM and B&B | 2.9 | 0.0 | -2.9 | -99.6 | -0.8 | 0.1 | 0.9 | 108.4 |

| Network Rail | 0.0 | 0.0 | 0.0 | 2.2 | -1.2 | -0.5 | 0.7 | 56.7 |

| COVID Corporate Facility Fund | 0.0 | 15.9 | 15.9 | 100.0 | - | - | - | - |

| Own account NCR¹¹ | -7.4 | 79.1 | 86.6 | 1,162.8 | 27.7 | 47.9 | 20.2 | 73.0 |

Download this table Table 1: Central government net cash requirement on own account

.xls .csvOn the same day as we release the public sector finances, HMRC publish a Summary of HM Revenue and Customs tax receipts, National Insurance contributions (NICs), tax credit expenditure and Child Benefit for the UK containing a detailed list of cash receipts.

Nôl i'r tabl cynnwys5. Borrowing

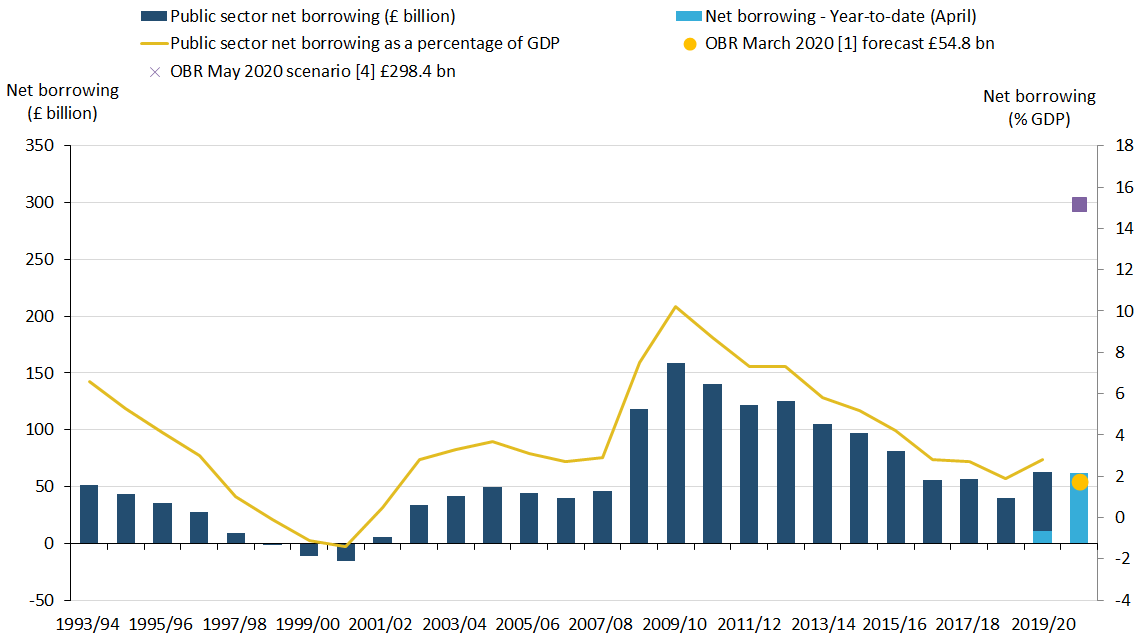

The coronavirus (COVID-19) pandemic has had an unprecedented impact on borrowing, with the £62.1 billion borrowed in April 2020 being the highest in any month on record (records began January 1993).

Last month we explained the uncertainty around our provisional estimate of borrowing in March 2020. This month we have increased that estimate by £11.7 billion to £14.7 billion, largely due to reductions in the previous estimate of taxes and the additional expenditure associated with the Coronavirus Job Retention scheme.

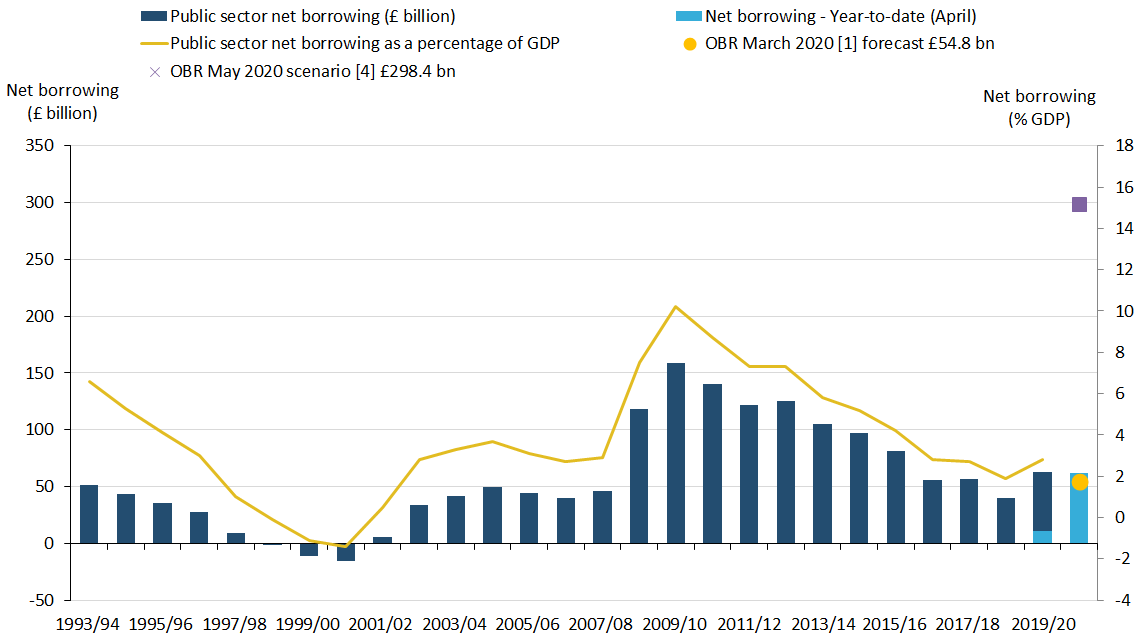

In their Coronavirus Reference Scenario published 14 May 2020, the Office for Budget Responsibility (OBR) estimate that borrowing in the current financial (April 2020 to March 2021) will be £298.4 billion, around five times the amount borrowed in the latest full financial year (April 2019 to March 2020) and almost twice as much that borrowed in the financial year ending March 2010, at the peak of the financial crisis.

Figure 1: The Office for Budget Responsibility Coronavirus reference scenario1 estimate borrowing to increase to £298.4 billion for the financial year ending March 2021

Public sector net borrowing excluding public sector banks, UK, April 2020 compared with the financial year ending March 2020 (April 2019 to March 2020)

Source: Office for National Statistics - Public Sector Finances

Notes:

- OBR Coronavirus reference scenario originally published 14 April 2020. This chart uses the updated fiscal data published 14 May 2020.

- The Office for Budget Responsibility (OBR) full financial year forecast of PSNB ex for the FYE March 2021, taken from the March 2020 Supplementary (13 March 2020).

Download this chart Figure 1: The Office for Budget Responsibility Coronavirus reference scenario^1^ estimate borrowing to increase to £298.4 billion for the financial year ending March 2021

Image .csv .xls6. Borrowing in April 2020

In April 2020, the public sector spent more money than it received in taxes and other income. Over this period, the public sector borrowed £62.1 billion, £51.1 billion more than it borrowed in April 2019. This unprecedented increase in borrowing reflects the emerging effects of the government's coronavirus (COVID-19) measures.

In their Coronavirus Reference Scenario published 14 May 2020, the Office for Budget Responsibility (OBR) estimate that borrowing in April 2020 would be £66.6 billion, £4.5 billion more than our initial estimate.

The difference between central government's income and spending makes the largest contribution to the amount borrowed by the public sector.

In April 2020, central government borrowed £66.2 billion, while local government was in surplus by £7.3 billion. This local government surplus partially reflects the increase in current transfers from central government to fund its COVID-19 measures.

The data for the latest month of every release contain some forecast data. The initial outturn estimates for the early months of the financial year, particularly April, contain more forecast data than other months, as profiles of tax receipts, along with departmental and local government spending are still provisional. This means that the data for these months are typically more prone to revision than other months and can be subject to sizeable revisions in later months.

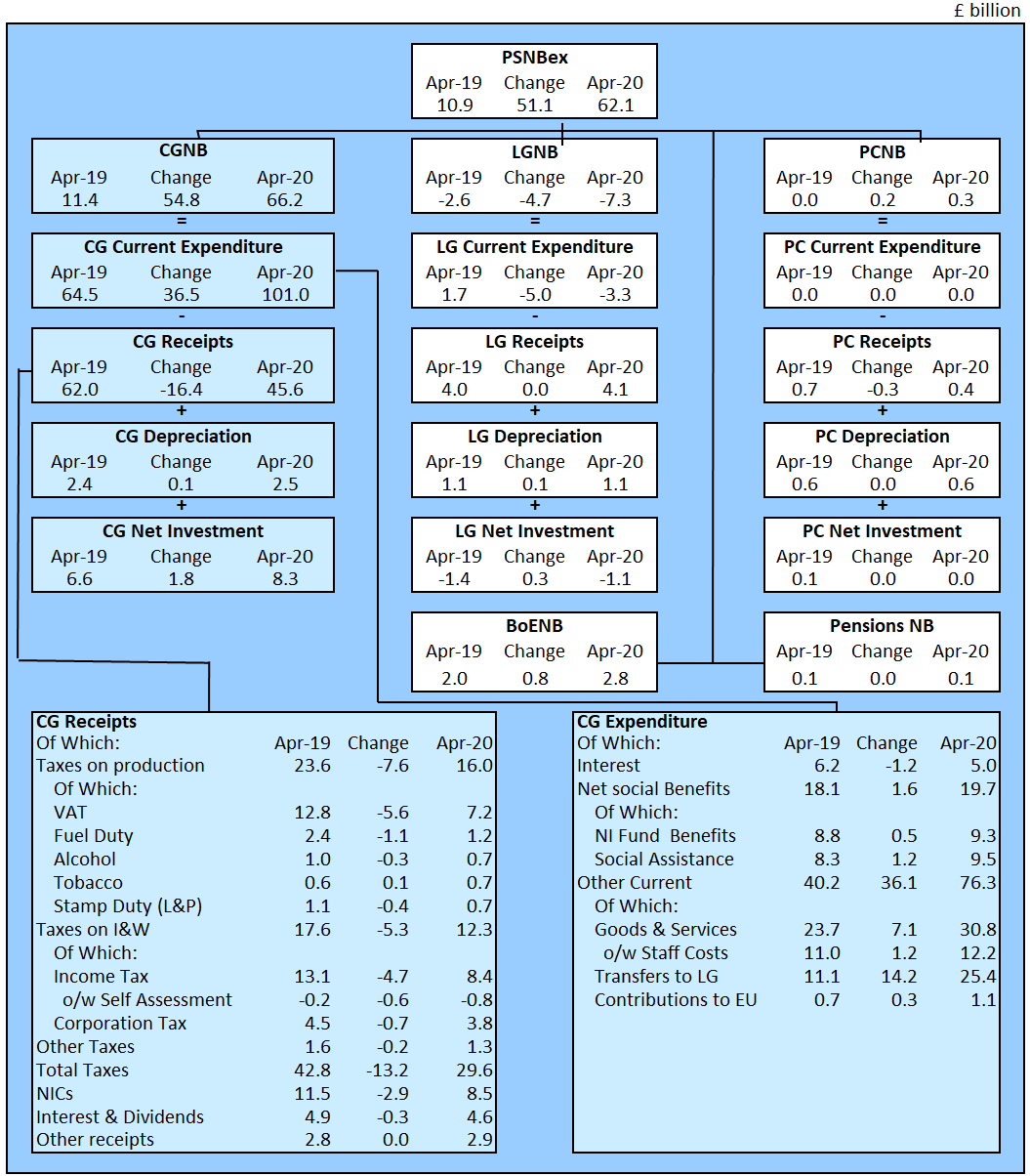

Figure 2 summarises how each of the five sub-sectors (central government, local government, non-financial public corporations, public sector pensions and the Bank of England (BoE)) contribute to the overall growth in monthly borrowing in April 2020 and compares this with the equivalent measures in the same month a year earlier (April 2019).

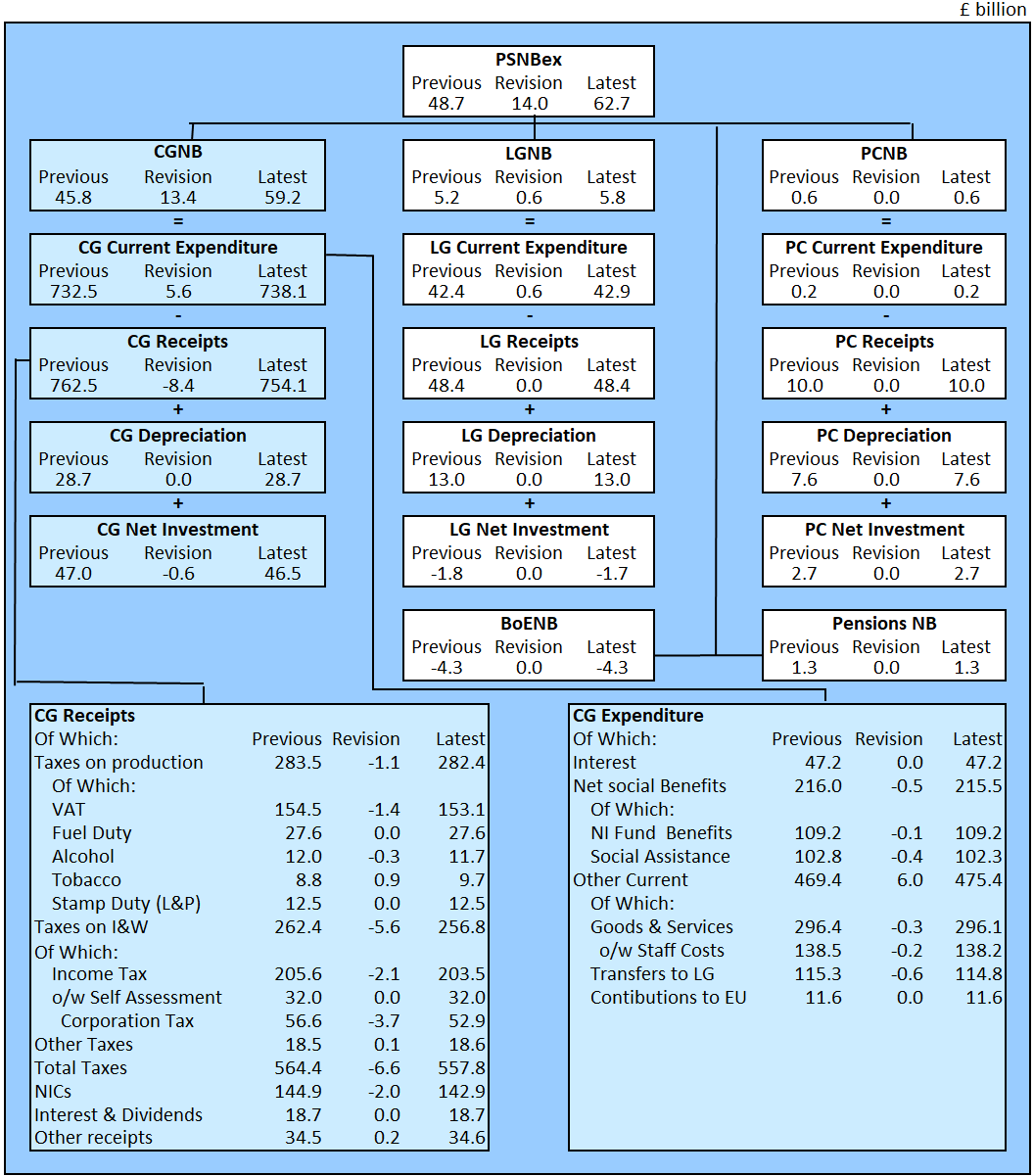

Figure 2: How each sector contributes to the growth in monthly borrowing

Public sector net borrowing by sub-sector, UK, April 2020, compared with April 2019

Source: Office for National Statistics – Public Sector Finances

Notes:

- PSNBex – Public sector net borrowing excluding public sector banks.

- CGNB – Central government net borrowing.

- LGNB – Local government net borrowing.

- PCNB – Non-financial public corporations: net borrowing.

- BoENB – Bank of England net borrowing.

- L&P – Land and property.

- I & W – Income and wealth.

- Contributions to EU – UK VAT, GNI and abatement contributions to the EU budget.

- NICs – National Insurance contributions.

- o/w – Of which.

Download this image Figure 2: How each sector contributes to the growth in monthly borrowing

.png (90.9 kB) .xls (85.5 kB){kind=link}

Central government receipts

In April 2020, central government receipts fell by £16.4 billion compared with April 2019 to £45.6 billion, including £29.6 billion in tax revenue.

These figures are always subject to some uncertainty, as many tax measures such as Value Added Tax (VAT), Corporation Tax and Pay As You Earn (PAYE) income tax contain some forecast cash receipts data and are liable to revision when actual cash receipts data are received. These forecasts are currently based on OBR's Coronavirus Reference Scenario published 14 May 2020.

Newly recorded central government revenue

In April 2020, the government introduced a digital services tax that applies to businesses providing a social media service, search engine or an online marketplace available to UK users.

In April 2020, central government received £29.0 million in digital services tax revenue.

Though the Digital Services Tax applies from April 2020, receipts are recorded on a national accounts (accrued) basis from January 2020 not April 2020. This arises from our method of time-adjusting cash receipts and it occurs because many businesses use a calendar year accounting period.

Bank of England Asset Purchase Facility Fund

In April 2020, there was a £4.0 billion dividend transfer from the Bank of England Asset Purchase Facility Fund (BEAPFF) to HM Treasury.

As with other such transfers, central government net borrowing will be reduced by an amount equivalent to the transfer, while the net borrowing of Bank of England will be increased by an equal and offsetting amount, with no impact at a public sector borrowing level.

Central government expenditure

In April 2020, central government spent £109.3 billion, an increase of 53.9% on April 2019. Of this amount, around three quarters was spent by central government on providing services and grants (for example, related to education, defence, and health and social care), with the remainder was spent on social benefits (such as pensions, unemployment payments, Child Benefit and Statutory Maternity Pay), capital investment and interest on the government's outstanding debt.

Subsidies paid by central government

This month we have recorded the expenditure associated with the Coronavirus Job Retention Scheme (CJRS) for the first time. CJRS is a temporary scheme designed to help employers pay wages and salaries to those employees who would otherwise be made redundant.

While there remains international debate about the appropriate treatment of similar schemes in other countries, our provisional assessment is that these payments are subsidies on production by central government to the employers.

In April 2020, central government subsidy expenditure was £16.3 billion, of which £14.0 billion were CJRS payments. Additionally, the subsidies paid by central government in March 2020 have been increased by £7.0 billion to reflect the additional CJRS payments not previously recorded.

Estimates of accrued CJRS payments are currently based on OBR's Coronavirus Reference Scenario published 14 May 2020.

Departmental expenditure on goods and services

Departmental expenditure on goods and services in April 2020 increased by £7.1 billion compared with April 2019, including a £1.2 billion increase in expenditure on staff costs and a £5.7 billion increase in the purchase of goods and services. This increase in pay and procurement partially reflects expenditure by the Department of Health and Social Care to respond to the COVID-19 pandemic.

Current transfers from central to local government

Central government grants to local authorities in April 2020 increased by £14.2 billion compared with April 2019, mainly to fund additional support because of the COVID-19 pandemic.

While transfers from central government to local government increase central government's borrowing, it reduces local government's borrowing by an equal and offsetting amount and so has no direct borrowing impact at a public sector level.

Interest payments on the government's outstanding debt

Interest payments on the government's outstanding debt in April 2020 were £5.0 billion, a £1.2 billion decrease compared with April 2019. Changes in debt interest are largely a result of movements in the Retail Prices Index (RPI) to which index-linked bonds are pegged.

Local government and public corporations data

Both the local government and public corporations data for April 2020 are initial estimates, largely based on OBR's Coronavirus Reference Scenario published 14 May 2020. We have reflected our estimation of impact of COVID-19 in these data.

Current and capital transfers between these sectors and central government are based on administrative data supplied by HM Treasury.

Nôl i'r tabl cynnwys7. Borrowing in the financial year ending March 2020

This month we publish the second provisional estimate of borrowing for the full financial year ending March 2020.

Between April 2019 and March 2020, the public sector borrowed a total of £62.7 billion, £22.5 billion (or 56.1%) more than in the same period the previous financial year.

These are not final figures and will be revised over the coming months as we replace our initial estimates with provisional and then final outturn data, and as more information on the effects of the coronavirus (COVID-19) pandemic becomes available.

Since our first estimate of borrowing for the full financial year ending March 2020 (published 23 April 2020), we have revised borrowing up by £14.0 billion, largely due to reductions in the previous estimate of taxes and the additional expenditure associated with the Coronavirus Job Retention scheme in March 2020.

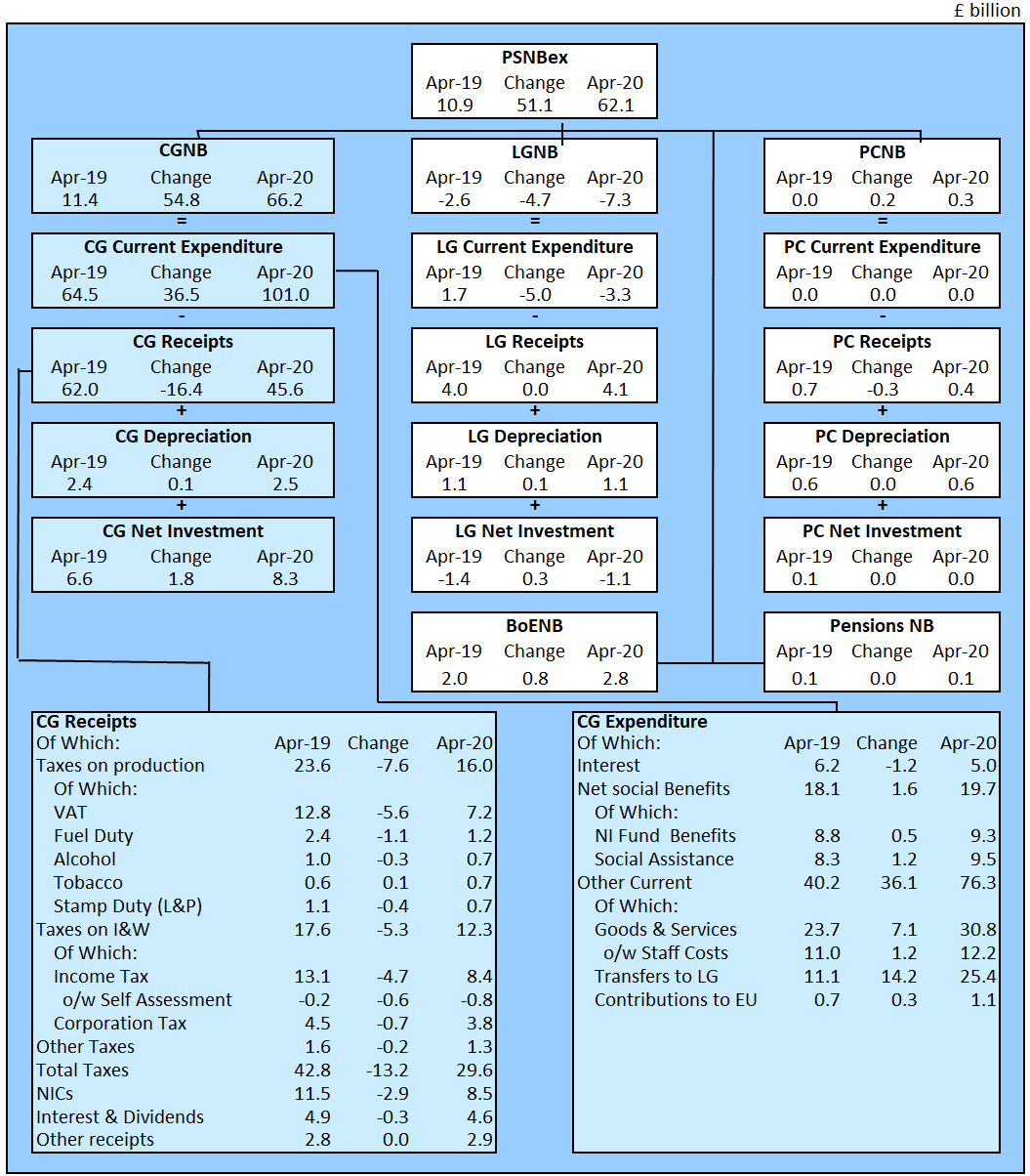

Figure 3 summarises how each of the five sub-sectors (central government, local government, non-financial public corporations, public sector pensions and the Bank of England (BoE)) contribute to the overall growth in monthly public sector net borrowing excluding public sector banks (PSNB ex) in the latest full financial year and compares this with the equivalent measures in the financial year ending March 2019.

Figure 3: How each sector contributes to the growth in borrowing

Public sector net borrowing by sub-sector, UK, latest full financial year (April 2019 to March 2020) compared with the financial year ending March 2019

Source: Office for National Statistics – Public Sector Finances

Notes:

- PSNBex – Public sector net borrowing excluding public sector banks.

- CGNB – Central government net borrowing.

- LGNB – Local government net borrowing.

- PCNB – Non-financial public corporations net borrowing.

- BoENB – Bank of England net borrowing.

- L&P – Land and property.

- I & W – Income and wealth.

- Contributions to EU – UK VAT, GNI and abatement contributions to the EU budget.

- NICs – National Insurance contributions.

- o/w – Of which.

Download this image Figure 3: How each sector contributes to the growth in borrowing

.png (96.9 kB) .xls (85.5 kB){kind=link}

Borrowing has generally been falling since its peak in the financial year ending March 2010. However, borrowing in the latest full financial year (April 2019 to March 2020) was £62.7 billion, £22.5 billion more than in the previous financial year, largely due to the impact of the COVID-19 pandemic in March.

Figure 4: Borrowing in the latest financial year was around one-third (30.7%) of the amount borrowed in the financial year ending March 2010

Public sector net borrowing excluding public sector banks, UK, April 1993 to April 2020

Source: Office for National Statistics – Public Sector Finances

Notes:

- The Office for Budget Responsibility (OBR) full financial year forecast of PSNB ex for the FYE March 2021, taken from the 13 March 2020 EFO.

- Financial year 2019 to 2020 represents the FYE 2020 (April 2019 to March 2020).

- Financial year-to-date represents April.

- OBR Coronavirus reference scenario originally published 14 April 2020. This chart uses the updated fiscal data published 14 May 2020.

Download this image Figure 4: Borrowing in the latest financial year was around one-third (30.7%) of the amount borrowed in the financial year ending March 2010

.png (40.5 kB) .xls (69.1 kB){kind=link}

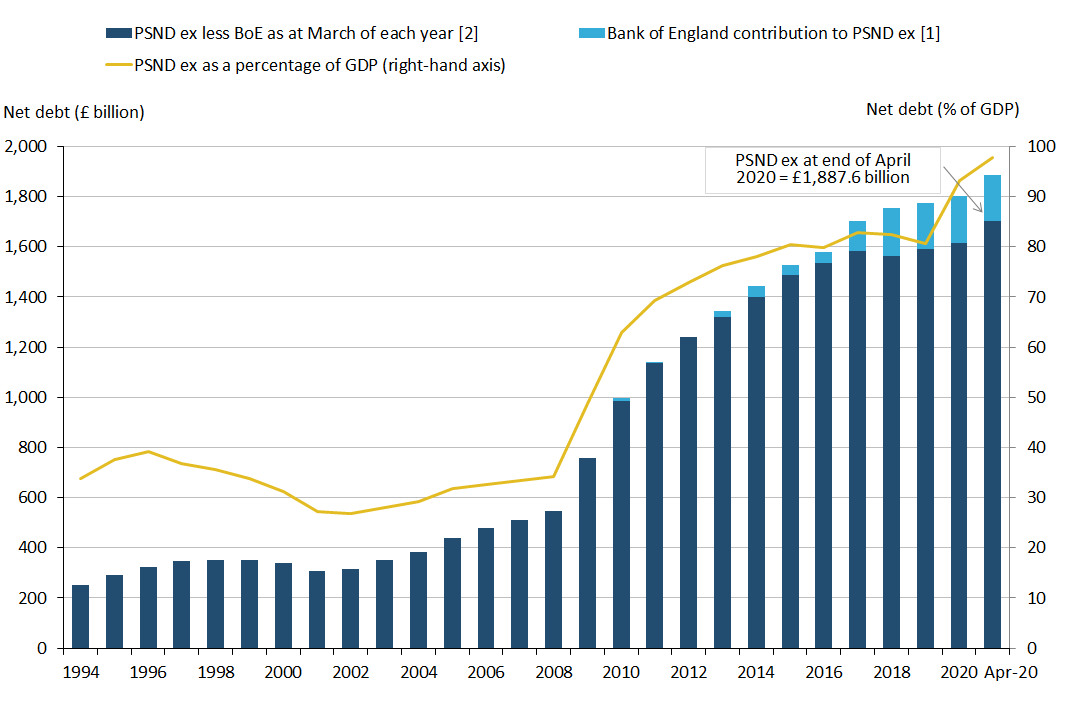

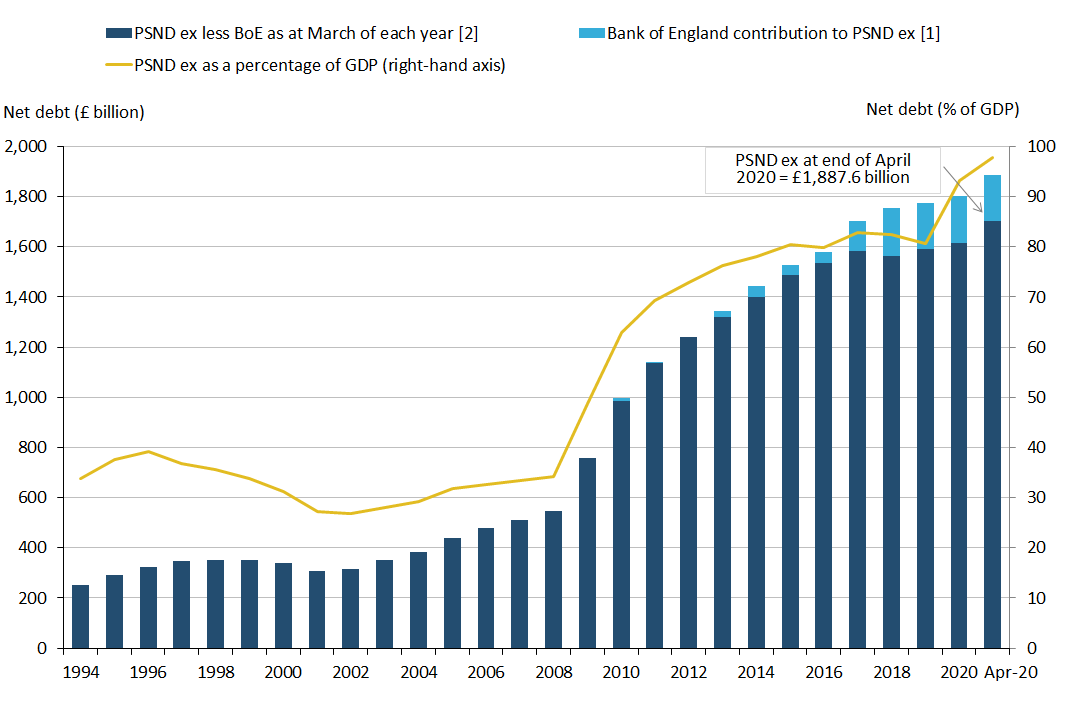

8. Debt

At the end of April 2020, the amount of money owed by the public sector to the private sector was approximately £1.9 trillion (or £1,887.6 billion), which equates to 97.7% of gross domestic product (GDP).

In April 2020, the Debt Management Office (DMO) issued £51.7 billion in gilts at nominal value, raising £58.5 billion in cash. This represents an unprecedented increase in gilts issuance (at nominal value) compared with March 2020.

Further, on 23 April 2020, the DMO published April 2020: Revision to the DMO's 2020-21 Financing Remit for May to July 2020 (PDF, 264KB), in which it announced that it will raise £180 billion during the May to July 2020 (inclusive) period, exclusively through issuance of conventional and index-linked gilts.

When the government borrows, this normally adds to the total debt, but it is important to remember that reducing the deficit is not the same as reducing the debt.

The Bank of England's contribution to debt

The Bank of England's contribution to debt is largely a result of its quantitative easing activities via the Bank of England Asset Purchase Facility Fund and Term Funding Schemes.

If we were to remove these temporary effects, debt at the end of April 2020 would reduce by £184.5 billion (or 9.6% percentage points of GDP) to £1,703.1 billion (or 88.1% of GDP).

Bank of England Asset Purchase Facility Fund

In March 2020, the Bank of England announced the expansion of its Asset Purchase Facility Fund (APF) to £200 billion in total, made up of £190 billion in gilts and £10 billion in corporate bonds.

At the end of April 2020, the gilt holdings of the APF have increased by £43.7 billion (at nominal value) compared with the end of March 2020, to £428.5 billion in total. This increase is of a similar order of magnitude to the new issuance by the DMO in April 2020 of around £51.7 billion (at nominal value), which means that gilt holdings by units other than the APF have changed to a much smaller degree than the level of issuance in April.

As a result of these gilt holdings, the impact of the APF on public sector net debt stands at £85.8 billion, the difference between the nominal value of its gilt holdings and the market value it paid at the time of purchase. Note that the final debt impact of the APF depends on the disposal of the gilts at the end of the scheme.

Term Funding Scheme and Term Funding Scheme incentives for Small and Medium-sized Enterprises

In March 2020, the Bank of England announced the expansion of its Term Funding Scheme with the introduction of Term Funding Scheme incentives for Small and Medium-sized Enterprises (TFS SME).

In April 2020, £8.2 billion of loans were made under the TFS SME scheme, bringing the total stock of loans under the TFS umbrella to £115.4 billion and so adding an equivalent amount to public sector net debt.

Figure 5: Debt as a percentage of gross domestic product (GDP) has been falling in recent financial years; however the measures introduced to address the COVID-19 pandemic have increased this ratio considerably

Public sector net debt excluding public sector banks, UK, March 1994 to the end of April 2020

Source: Office for National Statistics – Public Sector Finances

Notes:

- Includes Asset Purchase Facility (APF), which includes the Term Funding Scheme (TFS) and TFS incentives for small and medium-sized enterprises (TFS SME).

- Public sector net debt excluding public sector banks (PSND ex) is the combination of PSND ex Bank of England (BoE) plus the BoE’s contribution to PSND ex.

- Public sector net debt excluding public sector banks (PSND ex) shown at the end of each financial year (March), unless otherwise stated.

Download this image Figure 5: Debt as a percentage of gross domestic product (GDP) has been falling in recent financial years; however the measures introduced to address the COVID-19 pandemic have increased this ratio considerably

.png (38.4 kB) .xls (73.2 kB){kind=link}

Unusually, this month our published table REC3: Reconciliation of Central Government Net Cash Requirement and Changes in Net Debt, has a £10.9 billion in "other" category in April 2020. We will investigate this figure with a view to re-allocating it in the May 2020 presentation.

Nôl i'r tabl cynnwys9. Revisions

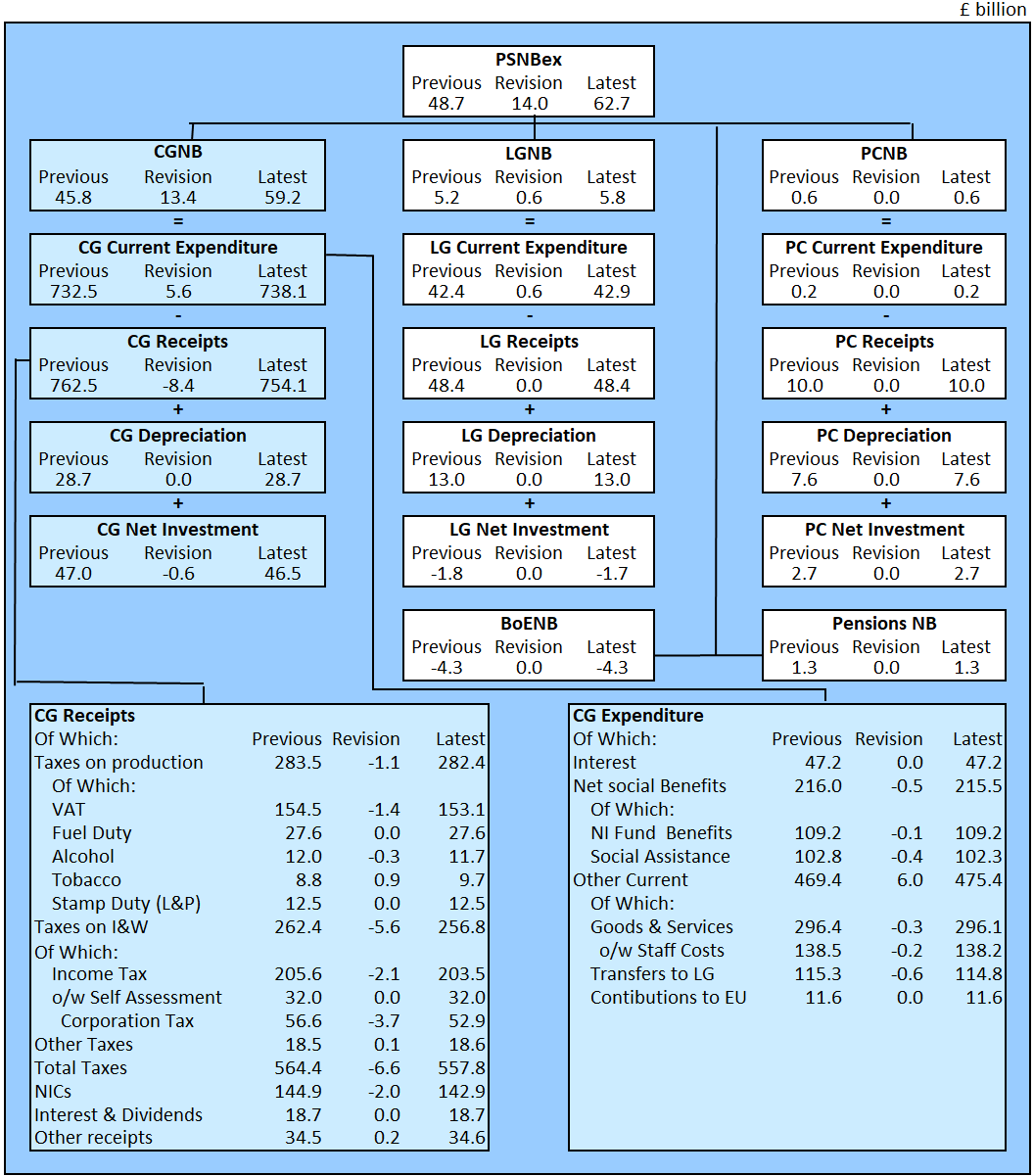

Table 2 shows the revisions to the headline statistics presented in this bulletin compared with those presented in the previous bulletin (published on 23 April 2020), while Figure 6 shows how each element of the public sector contributes to the revision in the latest full financial year net borrowing (public sector banks net borrowing excluding public sector banks, PSNB ex).

The data for the latest months of every release contain a degree of forecasts; subsequently these are replaced by improved forecasts as further data are available and finally outturn. The revisions presented in this section are largely the result of new tax data received from our data suppliers and the inclusion of the estimated expenditure associated with the Coronavirus Job Retention Scheme (CJRS) for the first time.

We have updated the estimates of gross domestic product (GDP) used to present a number of our measures, notably public sector net debt, as a percentage of GDP with the latest Office for National Statistics (ONS) figures (published 13 May 2020) and the estimates in OBR's Coronavirus Reference Scenario published on 14 May 2020.

| £ billion¹ (not seasonally adjusted) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Net borrowing | |||||||||

| Period | CG² | LG³ | NFPCs⁴ | PSP⁵ | BoE⁶ | PSNB ex⁷ | PSND ex⁸ | PSND % of GDP⁹ | PSNCR ex¹⁰ |

| 2016/17 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 2017/18 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 2018/19 | 0.8 | 0.0 | 0.0 | 0.0 | 0.0 | 0.8 | 0.0 | 0.0 | 0.0 |

| 2019/20 | 13.4 | 0.6 | 0.0 | 0.0 | 0.0 | 14.0 | 0.1 | 13.6 | 0.7 |

| 2019 Apr | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 2019 May | 0.1 | 0.0 | 0.0 | 0.0 | 0.0 | 0.1 | 0.0 | 0.0 | 0.0 |

| 2019 Jun | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 2019 Jul | -0.2 | 0.0 | 0.0 | 0.0 | 0.0 | -0.2 | 0.0 | 0.1 | 0.0 |

| 2019 Aug | -0.2 | 0.0 | 0.0 | 0.0 | 0.0 | -0.2 | 0.0 | 0.3 | 0.0 |

| 2019 Sep | -0.1 | 0.0 | 0.0 | 0.0 | 0.0 | -0.1 | 0.0 | 0.5 | 0.0 |

| 2019 Oct | 0.5 | 0.0 | 0.0 | 0.0 | 0.0 | 0.5 | 0.0 | 3.1 | 0.0 |

| 2019 Nov | 0.4 | 0.0 | 0.0 | 0.0 | 0.0 | 0.4 | 0.1 | 5.8 | 0.0 |

| 2019 Dec | 0.7 | 0.0 | 0.0 | 0.0 | 0.0 | 0.7 | 0.2 | 8.7 | 0.0 |

| 2020 Jan | 0.5 | 0.1 | 0.0 | 0.0 | 0.0 | 0.5 | 0.2 | 10.2 | 0.0 |

| 2020 Feb | 0.7 | 0.0 | 0.0 | 0.0 | 0.0 | 0.7 | 0.1 | 11.8 | 0.0 |

| 2020 Mar | 11.1 | 0.5 | 0.0 | 0.0 | 0.0 | 11.7 | 0.1 | 13.6 | 0.7 |

Download this table Table 2: Revisions to main aggregates

.xls .csvCentral government receipts

Tax receipts and National Insurance Contributions for the financial year ending March 2020 have been reduced by £6.6 billion and £2.0 billion respectively, compared with those published in our previous bulletin (published 23 April 2020). Of this £8.6 billion downward revision, £4.5 billion related to March 2020 alone, with the remaining portion spread across the other 11 months of the financial year.

To estimate borrowing, tax receipts are recorded on a national accounts (accrued) rather than on a cash receipt basis. In other words, we attempt to record receipts at the point where the liability arose, rather than when the tax is actually paid. This process means many receipts are provisional for the latest period(s) as they depend on both actual cash payments and on projections of future tax receipts based on official forecasts, which are "accrued" (or time adjusted) back to the current month(s).

The observed revisions reflect the uncertainty of the impact of coronavirus (COVID-19) on future cash tax receipts and further revisions are likely.

The update of HMRC's tax forecast based on the Office for Budget Responsibliity's (OBR) Coronavirus Reference Scenario published 14 May 2020 has led to improvements in the recording of many taxes recorded on a national accounts (accrued) basis. These data do not represent official forecasts but are best estimates made by OBR of the impact of COVID-19. The exceptional adjustments described in Section 3 remain in place for March 2020 and for earlier periods where relevant. These will be revisited when more information becomes available.

Due to the extended accruals period required to estimate Corporation Tax on a national accounts basis, these updated forecasts have also reduced expected Corporation Tax revenue by £0.8 billion in the financial year ending March 2019 which still relies on a portion of forecast cash receipts.

Central government expenditure

This month we have included the estimated expenditure associated with the Coronavirus Job Retention Scheme (CJRS) for the first time. Pending published statistical guidance, we have recorded CJRS payments as subsidies paid by central government. The subsidies paid by central government in March 2020 have therefore been increased by £7.0 billion to reflect the additional CJRS payments not previously recorded.

Local government borrowing

We have increased our previous estimate (published 23 April 2020) of local government borrowing in the financial year ending March 2020 by £0.6 billion due to a reduction in the estimate of grants received from central government. These payments net out at a public sector level and so have no impact on public sector borrowing.

Figure 6: How each element of the public sector contributes to the revision in full financial year net borrowing (PSNB ex)

Revisions to borrowing since the previous public sector finances bulletin (published on 23 April 2020), UK

Source: Office for National Statistics – Public Sector Finances

Notes:

- PSNBex – Public sector net borrowing excluding public sector banks.

- CGNB – Central government net borrowing.

- LGNB – Local government net borrowing.

- PCNB – Non-financial public corporations net borrowing.

- BoENB – Bank of England net borrowing.

- L&P – Land and property.

- I & W – Income and wealth.

- Contributions to EU – UK VAT, GNI and abatement contributions to the EU budget.

- NICs – National Insurance contributions

- o/w – Of which.

Download this image Figure 6: How each element of the public sector contributes to the revision in full financial year net borrowing (PSNB ex)

.png (89.5 kB) .xls (94.7 kB){kind=link}

Revisions to the net cash requirement and net debt of public sector banks

Estimates of the net cash requirement and net debt of public sector banks are derived from the balance sheet of these organisations, supplied to us by the Bank of England twice annually.

This month we have received the balance sheet data covering the period July to December 2019 for the first time, enabling us to update previous estimates associated with public sector banks. Further, our own estimates covering the period January 2020 to date have been updated to reflect this new information.

As a consequence of receiving these data, our previous estimate of the impact of the public sector banks on net debt at the end of March 2020 has increased by £2.5 billion, while their net cash requirement over the financial year ending March 2020 has reduced by £1.4 billion.

Nôl i'r tabl cynnwys10. Public sector finances data

Public sector finances borrowing by sub-sector

Dataset | Released 22 May 2020

An extended breakdown of public sector borrowing in a matrix format and estimates of total managed expenditure (TME).

Public sector finances tables 1 to 10: Appendix A

Dataset | Released 22 May 2020

The data underlying the public sector finances statistical bulletin are presented in the tables PSA 1 to 10.

Public sector finances revisions analysis on main fiscal aggregates: Appendix C

Dataset | Released 22 May 2020

Revisions analysis for central government receipts, expenditure, net borrowing and net cash requirement statistics for the UK over the last five years.

Public sector current receipts: Appendix D

Dataset | Released 22 May 2020

A breakdown of UK public sector income by latest month, financial year-to-date and full financial year, with comparisons with the same period in the previous financial year.

Impact of student loans, public sector-funded pension scheme changes and capital consumption changes introduced in September 2019: Appendix G

Dataset | Released 22 May 2020

Latest estimates of public sector net borrowing (PSNB) (and further into current budget deficit and net investment spending), net debt and net financial liabilities, with the impacts of changes to the accounting for student loans, public sector pensions and capital consumption introduced in September 2019.

All datasets related to this publication are available on our website.

11. Glossary

The public sector

In the UK, the public sector consists of six sub-sectors: central government, local government, public non-financial corporations, public sector pensions, the Bank of England (BoE) and public financial corporations (or public sector banks).

Public sector current budget deficit

Public sector current budget is the difference between revenue (mainly from taxes) and current expenditure, on an accrued basis; it is the gap between current expenditure and current receipts (having taken account of depreciation). The current budget is in surplus when receipts are greater than expenditure.

Public sector net investment

Net investment refers to the balance of acquisition less disposals of capital assets and liabilities.

Public sector net borrowing

Public sector net borrowing excluding public sector banks (PSNB ex) measures the gap between revenue raised (current receipts) and total spending (current expenditure plus net investment (capital spending less capital receipts)). Public sector net borrowing (PSNB) is often referred to by commentators as "the deficit".

Public sector net cash requirement

The public sector net cash requirement (PSNCR) represents the cash needed to be raised from the financial markets over a period of time to finance the government's activities. This can be close to the deficit for the same period; however, there are some transactions, for example, loans to the private sector, that need to be financed but do not contribute to the deficit. It is also close but not identical to the changes in the level of net debt between two points in time.

Public sector net debt

Public sector net debt excluding public sector banks (PSND ex) represents the amount of money the public sector owes to private sector organisations including overseas institutions, largely as a result of issuing gilts and Treasury Bills, minus the amount of cash and other short-term assets it holds. Public sector net debt (PSND) is often referred to by commentators as "the national debt".

Debt interest to revenue ratio

The debt interest to revenue ratio (DIR) represents the proportion of net interest paid (gross interest paid less interest received) by the public sector (excluding public sector banks), compared with the non-interest receipts it receives in a given period.

Other important terms commonly used to describe public sector finances are listed in the Public sector finances glossary.

Nôl i'r tabl cynnwys12. Measuring the data

The Monthly statistics on the public sector finances: a methodological guide provides comprehensive contextual and methodological information concerning the monthly public sector finances statistical bulletin. The guide sets out the conceptual and fiscal policy context for the bulletin, identifies the main fiscal measures, and explains how these are derived and interrelated. Additionally, it details the data sources used to compile the monthly estimates of the fiscal position.

More quality and methodology information on strengths, limitations, appropriate uses, and how the data were created is available in the Public sector finances QMI.

Departure from the EU

As the UK leaves the European Union (EU), it is important that our statistics continue to be of high quality and are internationally comparable. During the transition period, those UK statistics that align with EU practice and rules will continue to do so in the same way as before 31 January 2020.

These statistics, and our sector classification process, draw on the European System of Accounts (ESA) 2010, the Manual on Government Deficit and Debt, and associated guides.

After the transition period, we will continue to produce our public sector finance statistics in line with the UK Statistics Authority's Code of Practice for Statistics and in accordance with internationally agreed statistical guidance and standards.

To ensure comparability with other countries, the statistical aggregates within the Public sector finances release will continue to be produced according to the existing definitions and standards until further notice or those standards are updated.

Comparisons with official forecasts

The independent Office for Budget Responsibility (OBR) is responsible for the production of official forecasts for government. These forecasts are usually produced twice a year, in spring and autumn.

The most recent official forecasts, presented in the OBR's Supplementary forecast (13 March 2020) were made before the full effects of the Coronavirus (COVID-19) pandemic were apparent. It was widely recognised that these forecasts are likely to overstate future revenues. In turn, this made future downward revisions to revenues and upward revisions to borrowing more likely.

This month we have updated our presentations based on OBR's Coronavirus Reference Scenario published 14 May 2020. The reference scenario assumes a three-month lockdown period followed by a gradual return to normal over the subsequent three months. These data do not represent official forecasts but are the latest published estimates made by OBR of the impact of COVID-19 on future tax receipts.

Table 3 presents the headline public sector finance fiscal aggregates published in both OBR's Supplementary forecast (13 March 2020) and Coronavirus Reference Scenario published 14 May 2020.

| £ billion, unless otherwise stated (not seasonally adjusted) | |||||

|---|---|---|---|---|---|

| Current budget deficit | Net investment | Net borrowing | Net debt¹ | Net debt % of GDP | |

| Outturn 2019/20 | 13.6 | 49.1 | 62.7 | 1,804.0 | 93.3 |

| OBR forecast 2019/20² | -1.7 | 49.1 | 47.4 | 1,798.9 | 79.5 |

| Difference | 15.3 | 0.0 | 15.3 | 5.1 | 13.8 |

| OBR forecast 2020/21² | -4.9 | 59.7 | 54.8 | 1,818.3 | 77.4 |

| OBR scenario 2020/21³ | - | - | 298.4 | 2,230.3 | 95.8 |

| Outturn April 2020 | 54.7 | 7.4 | 62.1 | 1,887.6 | 97.7 |

| OBR scenario April 2020³ | - | - | 66.6 | 1,864.8 | 96.1 |

| Difference | - | - | -4.5 | 22.8 | 1.6 |

Download this table Table 3: How the latest outturn public sector figures compare with official OBR forecasts for the financial year ending March 2020, UK

.xls .csv13. Strengths and limitations

National Statistics status for public sector finances

On 20 June 2017, the UK Statistics Authority published a letter confirming the designation of the monthly Public sector finances bulletin as a National Statistic. This letter completes the 2015 assessment of public sector finances.

Local government

Local government data for the financial year ending (FYE) March 2020 are mainly based on budget data for England, Wales and Scotland, and estimates for Northern Ireland.

In recent years, planned expenditure initially reported in local authority budgets has been systematically higher than the final outturn expenditure reported in the audited accounts. We therefore include adjustments to reduce the amounts reported at the budget stage.

For the FYE March 2020, we include a £2.0 billion downward adjustment to England's current expenditure on goods and services, along with £0.7 billion and £0.2 billion adjustments to Scotland's and Wales' capital expenditure respectively. We apply a further £2.5 billion downward adjustment to current expenditure on benefits in the FYE March 2020, to reflect the most recently available data for housing benefits. Further information on these and additional adjustments can be found in the Public sector finances QMI.

Local government data for the FYE March 2021 are initial estimates, based on the Office for Budget Responsibility (OBR) forecasts. We have reflected our estimation of impact of coronavirus (COVID-19) in these data.

Current and capital transfers between local and central government are based on administrative data supplied by HM Treasury.

Non-financial public corporations

Public corporations data for the FYE March 2021 are initial estimates, based on the Office for Budget Responsibility (OBR) forecasts. Current and capital transfers between public corporations and central government are based on administrative data supplied by HM Treasury.

Public sector funded pensions

Pensions data for the FYE March 2020 are our estimates based on the latest available data. Some of these estimates rely on actuarial modelling; this is a complex process that most public sector schemes conduct every three to four years. Until such valuations become available, we forecast the change in pension liability using our knowledge of the economic climate. Pensions in the public sector finances: a methodological guide outlines both the theory and practice behind our calculation of pension scheme estimates.

Public sector banks

Unless otherwise stated, the figures quoted in this bulletin exclude public sector banks (that is, currently only Royal Bank of Scotland(RBS)). The reported position of debt, and to a lesser extent borrowing, would be distorted by the inclusion of RBS's balance sheet (and transactions). This is because the government does not need to borrow to fund the debt of RBS, nor would surpluses achieved by RBS be passed on to the government, other than through any dividends paid as a result of the government equity holdings.

Nôl i'r tabl cynnwys