1. Main points

In 2020, total retail sales volumes fell by 1.9% compared with 2019, the largest annual fall on record.

The impact on consumer retail sectors has varied with clothing and fuel volume sales seeing large falls of negative 21.5% and negative 22.2% respectively in 2020 and remain below pre-pandemic levels.

Overall, online sales rose to a record high of 33.9% as a share of all retail spending.

Insights from timely card transactions data show that the impact of England’s second and third lockdowns on card spending are similar, and significantly less severe than the first lockdown.

Card transaction data also suggests that during the second and third lockdowns, English online spending increased more in response to the fall in in-store spending than during the first lockdown.

As a whole, retail sales (in volume terms) in Great Britain have recovered from the large contraction in March and April 2020 but still saw the largest annual fall on record.

2. Retail industry in Great Britain

The retail industry is an important part of the economy, comprising almost 5.1% of UK GDP. The coronavirus (COVID-19) pandemic and the public health response have had large impacts on the UK and global economies. In particular, the retail industry has been impacted by the imposition of lockdown restrictions and social distancing, which have led to changes in the goods and services that we consume and how we consume them, with some areas of retail faring worse than others.

Policy measures introduced to contain the spread of the virus, such as public health restrictions and voluntary social distancing, had pronounced impacts on the retail industry. This included the closure of non-essential retail stores on 23 March 2020 as part of the first national lockdown that was introduced across the UK. Non-essential retailers were permitted to reopen in June with some variations across the UK nations - the earliest being in Northern Ireland (12 June) and the latest in Scotland (29 June) - although these stores were forced to shut once more as Tier 4 restrictions were introduced in certain areas across England and Scotland through autumn and a 17-day "firebreak lockdown" was introduced in Wales in late October.

The announcement of further lockdowns in England (5 November to 2 December and 5 January 2021 to present), as well as similar restrictions introduced across other UK nations1 from the end of 2020 till now has again seen the large-scale closure of non-essential retail. The impact of these restrictions has been reflected in footfall levels, in part capturing how the retail industry has been impacted in 2020.

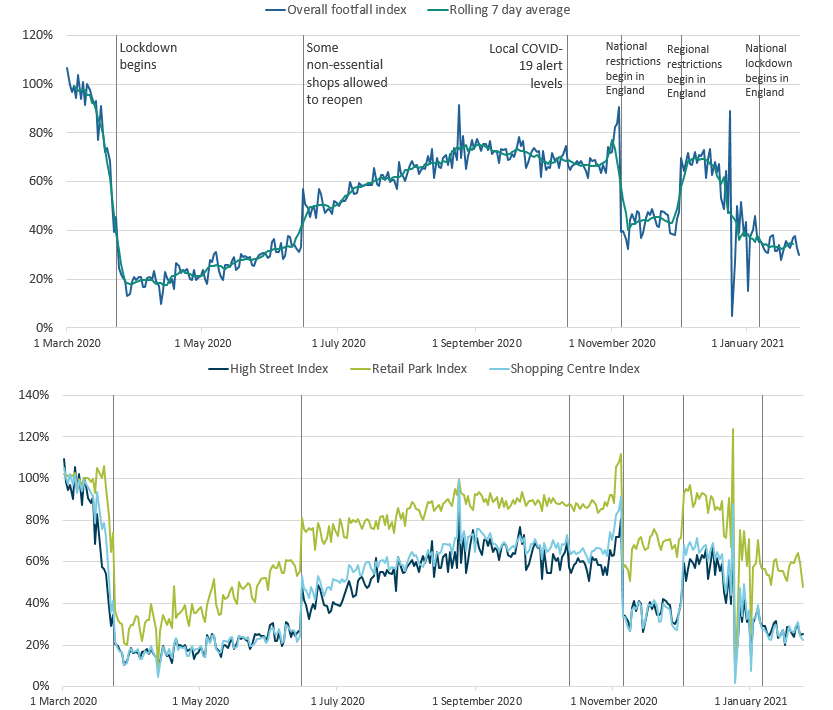

Figure 1: The restrictions on non-essential retail have been reflected in the impact on footfall

Volume of footfall, percentage change from the same day the previous year, UK, 1 March 2020 to 24 January 2021

Source: Springboard and the Department for Business, Energy and Industrial Strategy

Notes:

- The spike on Monday 24 August 2020 was caused by the comparison with 26 August 2019, which was bank holiday Monday with good weather. The bank holiday this year was a week later, on 31 August 2020.

Download this image Figure 1: The restrictions on non-essential retail have been reflected in the impact on footfall

.png (97.2 kB){kind=link}

The impact has been reflected in the official Retail sales figures. The total volume of retail sales in Great Britain fell by 1.9% in 2020 compared with 2019, the largest fall since records began. The impact has been particularly severe for non-essential retail. Figure 2 shows that retail sales volumes started to fall sharply in March 2020, and by April total retail sales volumes were 19% lower when compared with February levels. As these lockdown restrictions eased, there was a marked increase, which may have reflected some pent-up consumer demand. However, Figure 2 also shows that this in part reflects a change in how consumers have moved to online retailing. The rising use of online shopping has eased the impact of the pandemic on the retail sector. Online sales rose rapidly following the start of the pandemic and were 60% higher in May when compared with February's level. Total retail sales volumes recovered and since July have been above pre-pandemic (February 2020) levels. The latest figures show that total retail sales volume (excluding fuel) were 5.8% higher in December when compared with February.

It's worth noting that the volumes of sales fell again by 4.1% in November in response to the introduction of a second lockdown in England. The latest estimates show that total retail sales volume grew by 0.3% in December, as there were initially some easing restrictions in early December, although this was then followed by the re-imposition of tighter restrictions to non-essential retail later in the month.

Figure 2: Retail sales started falling sharply in March in response to the pandemic hit, before recovering later in the year as restrictions were lifted, while there was also a shift towards online retailing

Value of retail sales at curent prices, seasonally adjusted, Great Britain, Index Feb 2020=100

Source: Office for National Statistics – Monthly Business Survey

Notes:

- There is no available data for the sale of fuel online so fuel is excluded from all data in Figure 2.

Download this chart Figure 2: Retail sales started falling sharply in March in response to the pandemic hit, before recovering later in the year as restrictions were lifted, while there was also a shift towards online retailing

Image .csv .xlsNotes for Retail industry in the UK and Great Britain

- Similar restrictions to the lockdown introduced in England were announced across the UK throughout December: Wales (19 December to present), Scotland and Northern Ireland (26 December to present).

3. Retail sales around the world

The impact of the COVID-19 pandemic on the retail industry has been a global phenomenon, reflecting how governments across the world have introduced policy measures to reduce the spread of the virus. Figure 3 shows retail trends in 2020 across a selection of EU and G7 countries, which shows a similar within-year profile as there was a sharp decline in April when lockdown restrictions were largely imposed. However, the extent of falls and recovery varies by countries. The Understanding international comparisons of GDP article highlights how the timing and stringency levels of these restrictions have not been uniform, which might explain some of the differences in retail figures between countries1.

For the EU average, retail trade started to fall from March and by April was 20% below February's level. This was more severe in France (fall of around 27%), Spain and Italy (both falling by around 33%). By June, retail trade had recovered to pre-pandemic (February 2020) levels for the EU as a whole and remained above February's level, though this was not the case for all of the EU countries, with some of the countries that saw the most severe falls remaining below their February level.

In the USA, retail sales performed relatively better, declining less than seen across the EU. Nonetheless the US still saw a sharp fall following the start of the pandemic, with April's retail trade being around 16% lower than its pre-pandemic level. By June, it was 5% above its February levels.

Figure 3: International comparisons highlight that the public health response to the pandemic has impacted upon retail sales around the world, although to varying extents

Retail trade Index, Index = 100 at February, 2020

Source: Eurostat - Turnover and volume of sales in wholesale and retail trade, OECD - Revisions Analysis Dataset

Notes:

- Data for EU, Germany, Spain, France, Italy and UK is provided by Eurostat and is measured by index of deflated turnover of retail trade, except of motor vehicles and motorcycles.

- Data for Canada, Japan and USA are provided by the Organisation for Economic Co-operation and Development (OECD) and are measured by index of retail trade volume.

- There is no November data available for Canada, Japan and USA.

Download this chart Figure 3: International comparisons highlight that the public health response to the pandemic has impacted upon retail sales around the world, although to varying extents

Image .csv .xlsThe varying performance of the retail sector in different countries will likely reflect difference in the level of restrictions policies to contain the spread of the COVID-19 virus. Figure 4 shows that there is some evidence that the extent of restrictions introduced is associated with lower levels of retail sales. This is highlighted by the inverse relationship between the Retail Sales Index and the Oxford Government Response Tracker Index.

Figure 4: Observing the Oxford Government Response Tracker Index figures, there appears to be an inverse relationship with retail sales across EU and G7 countries

Value of Index of deflated turnover of retail trade, except of motor vehicles and motorcycles, Index of Retail Trade Volume, Oxford Government Response Index, 2020

Source: Eurostat - Turnover and volume of sales in wholesale and retail trade, Oxford COVID-19 Government Response Tracker

Notes:

- For further details on the methodology to calculate the Government Stringency Index, please see Methodology for calculating indices.

- Data for Retail Sales Index is the same as provided in Figure 3.

- The Oxford Government Response Tracker systematically collects information on several different common policy responses that governments have taken to respond to the pandemic.

- The Government Stringency Index is based on nine response indicators including school closures and travel bans to give a rescaled value from 0 to 100, (100= strictest response).

- Government Stringency Index figures are provided as an average for the given month.

Download this chart Figure 4: Observing the Oxford Government Response Tracker Index figures, there appears to be an inverse relationship with retail sales across EU and G7 countries

Image .csv .xlsNotes for: Retail sales around the world

- The Oxford Government Stringency Index is based on nine response indicators, including school closures and travel bans, to give a rescaled value from 0 to 100, (100 = strictest response).

4. Retail sales trends by retail sectors

The impact of the COVID-19 pandemic has been varied on the retail industry, reflecting the effects of voluntary and involuntary responses and the subsequent change in goods and services that we have consumed over the year. For example, there has been a sharp decline in spending on fuel, as the move to working from home and other restrictions on mobility limited the demand for fuel.

Figure 5 shows that all retail sectors experienced falls in volume sales from March 2020, except food stores and non-store retailing. The increase in food stores reflects that they were not impacted by store closure guidelines, as well as food being an essential purchase. Food stores saw strong growth in March 2020, which is likely to reflect stockpiling of essential foods due to concerns around disruptions to supply chains. In the EU, while the sales of non-food products dropped by 23.8% in April 2020 year-on-year, the sales of food, beverages and tobacco increased by 1.2%. Similarly, in the US, there were large falls in sectors such as accommodation and restaurants (PDF, 1.25MB). However, these declines were partly offset by the large rise in food and beverage store sales. Baker and others (2020) find evidence of stockpiling, followed by a reduction in spending near the end of March (PDF, 2.15MB) from household-level transaction data.

Figure 5: In December, clothing and fuel remain below their pre-pandemic level; both sectors have been hit by the pandemic and restrictions

Value of UK retail sales at current prices, by retail sector, seasonally adjusted, Great Britain, index February 2020=100

Source: Office for National Statistics – Monthly Business Survey

Download this chart Figure 5: In December, clothing and fuel remain below their pre-pandemic level; both sectors have been hit by the pandemic and restrictions

Image .csv .xlsExperimental faster indicators on spending on debit and credit cards help provide further insight into how restrictions have impacted on different types of consumer spending.

Figure 6 shows that in the UK spending across categories fell sharply from March 2020 with some variation in spending trends between categories throughout the rest of the year.

The spending categories are:

- staples - companies that sell essential goods that households need to purchase, such as food and utilities

- work-related - companies providing public transport or selling petrol

- delayable - companies selling goods whose purchase could be delayed, such as clothing or furnishings

- social - spending on travel and eating out

The sharpest decline was in social spending, as public health restrictions and voluntary social distancing were in effect for much of the year to varying extents. There was also a fall in work-related consumption, as there was a large shift towards working from home in response to the pandemic, in line with the official figures showing that there has been a sharp decline in spending on fuel.

Figure 6: In the week to 21 January 2021, the aggregate CHAPS-based indicator of debit and credit card purchases remained at 35% below its February 2020 average

Index February 2020 = 100, percentage change on a backward looking seven-day rolling average,13 January 2020 to 21 January 2021, non-seasonally adjusted, nominal prices, UK

Source: ONS and Bank of England calculations

Notes:

- The value of Clearing House Automated Payment System (CHAPS) is a faster indicator which records payments received by large UK companies from their credit and debit card processors. CHAPS provides an indicator of UK companies' transactions made by customers, both via physical and online platforms. More information on the indicator is provided in a Bank of England methodology article.

- Introduction of lockdowns and other restriction polices are expected to differ between the four UK nations.

Download this chart Figure 6: In the week to 21 January 2021, the aggregate CHAPS-based indicator of debit and credit card purchases remained at 35% below its February 2020 average

Image .csv .xls5. Online sales

The COVID-19 pandemic has appeared to accelerate the shift to online sales, especially with non-essential physical stores forced to close. Customers have turned to online platforms while retailers have responded by raising capacity to facilitate online shopping, click-and-collect services, and home deliveries. Figure 7 presents the overall trend for online sales, whose share of all retail spending rose sharply at the start of the pandemic. By May 2020, online sales reached a record high share of all retail spending of around 34%, climbing from 20% in February. Since then the share of online sales have fallen a little, which is likely to reflect re-opening of physical stores, though remain significantly above the pre-pandemic levels.

Another spike in online spending was noticeable following the introduction of the second lockdown in England in November, reinforcing how the closure of non-essential retail has led to a behavioural change in how we consume goods and services. The boost in online spending might also be explained by Black Friday promotions online, and consumers relying more on internet platforms for their Christmas shopping. The CBI reported that the pickup in online sales during November's lockdown was the fastest since October 2018, while growth in online sales continued above average rates in December for the third consecutive month, which signal consumers moving to online shopping from in-store purchases, as retailers and consumers continue to adapt to online shopping.

Figure 7: The share of online sales rose to a record high in May and continues to remain above pre-pandemic levels

Great Britain internet sales index: value seasonally adjusted internet sales as a proportion of all retailing, 2013 to 2020

Source: Office for National Statistics - Monthly Business Survey

Download this chart Figure 7: The share of online sales rose to a record high in May and continues to remain above pre-pandemic levels

Image .csv .xlsOnline spending: international comparisons

Figure 8 shows online sales growth trends with selected countries (France, Germany, Spain and Italy) and the EU, which reported strong monthly growth in online sales between March and May 2020. Spain saw growth of around 35% in online sales in April, with the EU average at 15%. Further evidence from literature finds that based on Spain's credit card transactions, in the period post-lockdown, online market share of total expenditure grew by around 50% (from around 12% to above 22%). For most countries, total online sales fell in June and July, as there was an easing of restrictions during the early summer period which led to some customers in these countries to return to in-store shopping. More recent figures show that online shopping sales picked up in October as some restrictions were re-imposed.

Figure 8: In April and May selected EU countries saw an upsurge in online sales, growth that slowed as restrictions loosened

Retail sales through mail order houses or by internet, index of deflated turnover as a percentage change on the previous period (monthly), 2020

Source: Eurostat - Turnover and volume of sales in wholesale and retail trade

Notes:

- Data are provided by Eurostat.

- There is no November data available for France.

Download this chart Figure 8: In April and May selected EU countries saw an upsurge in online sales, growth that slowed as restrictions loosened

Image .csv .xls6. Insights from using new timely transactions data

As part of our response to the coronavirus pandemic, we have developed a range of real-time indicators to provide more timely and higher-frequency insights into how the economy is evolving over time. We have been working collaboratively with the financial technology company Revolut1 to gain higher frequency data on consumer spending. Revolut customers tend to be younger and more metropolitan than average with a fast-growing customer base of several million in the UK, so spending may not be representative of the overall UK macroeconomic picture. To address this, we have applied weightings to adjust for user-base growth and sectoral representation. Also, as the attributes of the user-base are largely constant over time, a comparative analysis across periods (in a "difference-in-differences" fashion) can provide valuable insights into the relative impacts of different lockdowns.

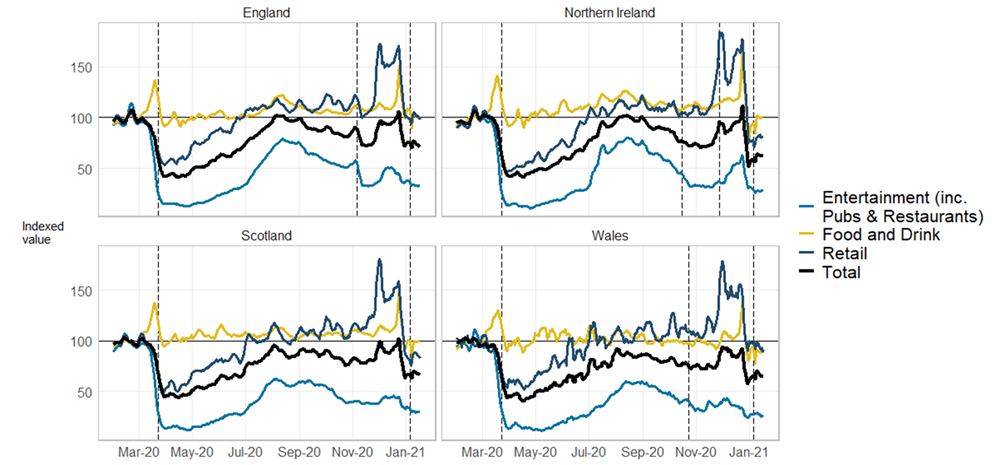

Total card spending

Figure 9 shows that the different restrictions and lockdown policies introduced in the home nations at various points in time have led to differences in card spending between nations and within merchant groups2. These variations arise partly from differences in introduction date, duration, and severity of these restrictions. Examples of this include the Wales fire-break lockdown, England's tier restrictions, Scotland's tier restrictions, and Northern Ireland's hospitality restrictions.

Figure 9: Daily total card expenditure by UK nation and sector

7-day rolling average of adjusted indexed values (100 = day of week average February 2020)

Source: Revolut, ONS calculations

Notes:

- Introduction of lockdowns and other restriction polices are expected to differ between the four UK nations.

- Geographic locations are defined by Revolut cardholder address rather than merchant location.

- Merchant category codes classify businesses dependent upon primary business categories, which can then be grouped up to higher, mutually exclusive sectoral levels. In this analysis, Entertainment includes pubs, restaurants, and social venues; Retail spending includes clothing and footwear, department stores, mixed retail businesses, household goods, and other retailers; Food and drink includes supermarkets, convenience stores, and other food and drink providers.

- UK: Lockdown 1 – 23 February 2020, Lockdown 3 – 5 January 2021; England: Lockdown 2 – 5 November 2020, Wales: Fire-break – 23 October 2020; Northern Ireland: Lockdown 2 – 19 October 2020, Lockdown 3 – 27 November 2020.

Download this image Figure 9: Daily total card expenditure by UK nation and sector

.png (195.5 kB){kind=link}

All nations saw a large reduction in card spending following the first national lockdown restrictions. Food and drink spending (which captures supermarket spending) sees a spike prior to the first lockdown, likely reflecting the effects of stockpiling amidst concerns around supply chain disruptions and increased time spent at home. There were subsequently smaller spikes for the second and third lockdowns, which might in part be due to reduced uncertainty around the availability of these goods and services. Food and drink spending activity has generally been above its pre-pandemic (February 2020) level throughout the year due to fewer restrictive policies on this sector and the shutting down of restaurants.

Entertainment spending - which contains pubs and restaurants spending - was consistently impacted most since March 2020. The impact on entertainment spending likely reflects how the hospitality industry has been subject to government policies to reduce the rate of virus transmission, such as complete closures and limits on the number of households that can mix in pubs and restaurants. The Eat Out to Help Out scheme in August 2020 drove a recovery in the sector but it reversed as restrictions were tightened from September.

Retail spending fell across nations in response to the first national lockdown, seeing increases over time and returned to pre-pandemic levels in late June 2020. Additionally, spending spikes were observed before and after the introduction of later restrictions such as the second England lockdown before Christmas, where some seasonal spending may have been displaced due to behavioural changes.

Table 1 shows how the value of total card transactions fell in the first 13 days of each of the lockdowns in England, relative to a pre-pandemic reference. It compares the impact on merchant categories using daily data to provide a breakdown at a total level. Overall, spending patterns of the second and third lockdown were broadly similar but less severe than the first lockdown, with entertainment and retail expenditure markedly less impacted during the latter lockdowns. This might reflect that the restrictions were generally more stringent in the first lockdown, while there may have been more adjustment to online activities by consumers and businesses in later lockdowns.

There is some tentative evidence that this improvement in the second lockdown was bolstered by Black Friday (27 November 2020) and Cyber Monday (30 November 2020) spending, as well as seasonally expected Christmas spend. This could reflect that some retailers adapted more effectively to new restrictions, for example by offering click-and-collect services during the second lockdown.

| Lockdown 1 | Lockdown 2 | Lockdown 3 | |

|---|---|---|---|

| Entertainment | -85% | -67% | -66% |

| Food and Drink | -5% | 8% | 2% |

| Retail | -44% | 2% | 1% |

| Total | -56% | -27% | -27% |

Download this table Table 1: Comparison of England lockdowns by merchant category code groupings

.xls .csvNotes:

- Lockdown 1 started on 23 March, Lockdown 2 started on 5 November, Lockdown 3 started on 5 January.

- Baseline, 100 = day of week average February 2020.

In-store and online card spending

Table 2 shows that in-store values for both entertainment and retail during lockdowns saw larger decreases from the pre-pandemic reference period than for online transactions, with retail performing better than entertainment during the second and third lockdowns. This might reflect the introduction of COVID-19 guideline measures that enabled increased in-store activity and the potential bringing forward of some early Christmas spend, with Black Friday and Cyber Monday also likely having some impact on spending levels during lockdown two retail and entertainment categories. In-store food and drink spending saw values close to the pre-pandemic levels during periods of lockdown, evidently in part due to the essential nature of supermarket spending and subsequently less targeted government policy on this sector.

Online card spending has overall been less impacted by the imposition of lockdown restrictions, as there has likely been a substitution away from in-store purchases throughout the lockdowns. This is reflected by much higher online spend for food and drink, as well as retail, where online delivery demand and capacities have likely increased since the first lockdown. The net impact of this would also reflect companies' capability and adaptability to provide consumers online alternatives to in-store spending, as well as how well consumers adjust to these alternatives.

| Lockdown 1 | Lockdown 2 | Lockdown 3 | ||||

|---|---|---|---|---|---|---|

| Instore | Online | Instore | Online | Instore | Online | |

| Entertainment | -97% | -32% | -82% | -2% | -84% | 11% |

| Food and Drink | -9% | 58% | 1% | 113% | -5% | 117% |

| Retail | -88% | 27% | -63% | 107% | -61% | 100% |

| Total | -71% | -20% | -51% | 34% | -52% | 38% |

Download this table Table 2: Comparison of England lockdowns by merchant category code groupings and by in-store and online

.xls .csvNotes

- Lockdown 1 started on 23 March, Lockdown 2 started on 5 November, Lockdown 3 started on 5 January.

- Baseline, 100 = day of week average February 2020.

Notes for: Insights from using new timely transactions data

- Geographic nations are defined by Revolut cardholder address rather than merchant location.

- Merchant category codes classify businesses dependent upon primary business categories, which can then be grouped up to higher, mutually exclusive sectoral levels. In this analysis, entertainment includes pubs, restaurants, and social venues. Retail spending includes clothing and footwear, department stores, mixed retail businesses, household goods, and other retailers. Food and drink includes supermarkets, convenience stores, and other food and drink providers.

7. Future developments

We will continue to analyse official retail sales estimates and complementary real time data to monitor developments in the retail sector. We expect the continued lockdown and easing of restrictions in the future to have further impacts on retail sales and consumption patterns. This could contribute to the evidence base of the pandemic’s impact on retail sector and inform policy decisions.

Nôl i'r tabl cynnwys