Cynnwys

- Abstract

- Author

- Acknowledgements

- Introduction

- Part 1: The UK’s International Investment Position (IIP)

- Part 2: Drivers of the changes to the net international investment position (IIP)

- Terminology of flows and other changes

- Other changes and the net IIP

- Conclusion

- Annex A: Decomposition of international investment position (IIP) changes: methodology and assumptions

- Annex B: Further focus on exchange rate effects

- Annex C: Further focus on equity prices effects

1. Abstract

The paper describes the UK’s international investment position (IIP) with the rest of the world, breaking the IIP down into assets and liabilities, which both grew between 1999 and 20141. At the end of 2014, the stock of liabilities outstripped the stock of assets, leading to a UK net liability position of 17.6 per cent of gross domestic product (GDP). The paper breaks down the changes in net IIP, assets and liabilities over the period 1999 to 2014 into the drivers of these changes. These include changes in the capital flows into and out of the UK (or the net acquisition of financial assets and net incurrence of financial liabilities) and “other changes”. It shows, for example, that in 2008, exchange rate effects had a large impact on the UK IIP, because sterling depreciated sharply against other major currencies. This is an extension of information provided in tables 8 and 10 of the Pink Book and previous work on the UK IIP conducted by Damian Whittard2.

Notes

- The analysis excludes 2015 as this data has not yet been benchmarked to annual surveys and so some of the data required for this analysis is not yet available.

- ‘The UK’s External Balance Sheet – The International Investment Position (IIP)’ by Damian Whittard – March 2012

3. Acknowledgements

The author would like to acknowledge the contributions from Craig Taylor, Richard McCrae, Sumit Dey-Chowdhury, Louise Skilton, Ewelina Thomas, Penil Chhiba and Parsa Mohammadpour.

Nôl i'r tabl cynnwys4. Introduction

This article is split up into two main parts. The first section describes the changes to the UK’s gross and net international investment position (IIP) between 1999 and 2014, including a breakdown of these changes by functional category.

The second discusses the two mechanisms that drive changes in the external balance sheet: financial flows into and out of the UK and other changes to the stock of the UK’s external assets and liabilities. These include currency and price effects, which do not reflect a change in the underlying volume of foreign assets or liabilities, but rather reflect a change in its valuation. A breakdown of these changes is then provided for the years 1999 to 2014.

Within the UK balance of payments publications (quarterly Balance of Payments statistical bulletin and annual Pink Book), the UK’s Rest of the World financial account and IIP is provided, but a breakdown of other changes in the IIP is not published. This article therefore provides additional information as a result of ad-hoc analysis that is not available within regular publications.

Nôl i'r tabl cynnwys5. Part 1: The UK’s International Investment Position (IIP)

The balance of payments provides the economic transactions for a specific time period between the residents of an economy and the rest of the world, and includes the current account, capital account and financial account.

The current and capital accounts

The current account is a key economic statistic and together with the capital account determines whether a country is a net lender (surplus) or net borrower (deficit). If a country is a net borrower, then there needs to be a net inflow of money within the financial account to finance this deficit.

The UK is traditionally a net borrower. Figure 1 presents the sum of the current and capital account balances, which for 2014, was -£85.4 billion1.

Figure 1: Sum of the current and capital account balances, 1999 to 2014

Source: Office for National Statistics

Download this chart Figure 1: Sum of the current and capital account balances, 1999 to 2014

Image .csv .xlsThe financial account

Since the UK is traditionally a net borrower, then it needs to service this outflow with an inflow of money on its financial account. The Financial Account records the net acquisition of financial assets and net incurrence of financial liabilities within a particular period, capturing the financial flows into and out of the UK. The balance is presented as the net acquisition of assets minus net acquisition of liabilities. For 2014, the financial account shows a net inflow of £78.6 billion. The slight difference between the inflow recorded in the financial account and the sum of current and capital account balances is attributable to net errors and omissions in the accounts.

The IIP

In contrast, the IIP is the counterpart stock position of these financial flows. The IIP is a statement of:

- the holdings of (gross) foreign assets by UK residents (UK assets)

- the holdings of (gross) UK assets by foreign residents (UK liabilities)

The difference between the assets and liabilities shows the net position of the IIP and represents the level of UK claims on the rest of the world over the rest of the world’s claims on the UK. The IIP therefore provides us with the UK’s external financial balance sheet at a specific point in time. The net IIP is an important barometer of the financial condition and creditworthiness of a country.

The relationship between balance of payments and the IIP

The current account consists of three key areas:

- trade in goods and services

- primary income

- secondary income

The largest component of primary income is investment income, which is in turn broken down by the following functional categories:

- foreign direct investment

- portfolio investment

- other investment

- reserve assets

Changes in the earnings of investment income (which are captured within the primary income account) can only be explained by either a change in the rate of return on investment, or a change in the stock of assets and liabilities (the IIP). If the rate of return and stock of assets and liabilities between one period and the next remain constant, then the amount of investment income earnings between the two periods would also remain constant. However, it is usual for the rate of return on different investments to vary by asset type and over time. The stock of assets and liabilities also generally change from one period to the next, in turn driven by the amount of investment (the financial account flows) and other changes.

The UK’s IIP includes the following functional categories:

- direct investment (DI) occurs when a resident in one economy obtains a lasting interest in an enterprise in another economy, has a significant degree of influence and owns at least 10 per cent equity

- portfolio investment (PI) includes equity and debt securities in the form of bonds and notes, and money market instruments; equity securities are recorded when an investment is made representing less than 10 per cent of the equity capital

- other investment (OI) is all investment other than that included in the four other functional categories; it includes trade credit, loans, currency and deposits, and other assets and liabilities

- financial derivatives (FD) are financial instruments that derive their value from underlying assets, events or conditions; they include options, futures, warrants, and currency and interest swap rates; no income associated with financial derivates directly feed into the primary income account; employee stock options are a privilege granted to specified employees of a company

- reserve assets (RA) are the UK’s official holdings of short term assets that can be very quickly converted into cash; it includes gold, convertible currencies, special drawing rights and changes to the UK reserve position in the IMF

Figure 2 shows the level of the UK’s net assets, from 1999 to 2014, broken down by functional category. It is expressed as a percentage of GDP, to present these figures relative to the size of the economy. It can be seen that the UK has predominantly run a net liability position, as it has incurred more external liabilities than the stock of external assets it has accumulated. This is consistent with the UK running a current account deficit over this period, which it has had to finance by increasing its net liabilities with the rest of the world.

Figure 2: UK net IIP breakdown by functional categories, as a percentage of nominal GDP, 1999 to 2014

Source: Office for National Statistics

Download this chart Figure 2: UK net IIP breakdown by functional categories, as a percentage of nominal GDP, 1999 to 2014

Image .csv .xlsBetween 1999 and 2014, the net liability positions for PI and OI more than offset the net asset position for DI, FD and RA, except for in 2008, where the UK experienced its only net asset position during the series at 9.0% of GDP. During the early part of this period, OI was the main driver of the UK’s net liability position experiencing a net liability position between 17.7% and 32.4% of GDP. From 2006, PI became the main driver behind the UK’s net liability position, as a result of an increase in both OI loans and deposits assets and PI liabilities. DI reached its lowest net asset position of the series in 2014 at 1.9% of GDP, compared with its largest net asset position in 2008, at 31.6% of GDP. PI reached a net liability position of 33.8% of GDP in 2009, the largest for any functional category during the series. Reserve assets experienced a net asset position during each year of the series, whereas, financial derivatives experienced a net liability position between 2004 and 2007, before reaching its largest net asset position in 2008 of 8.0% of GDP.

Net IIP ranged between -22.4% of GDP and 9.0% of GDP during the series, as a result of the fluctuations in the level of assets and liabilities. The level of assets and liabilities both reached values 7 times the size of GDP during the series. The size of the UK’s assets and liabilities reflects the role of the financial sector in the UK. It is also a reason why revaluation effects play a large role in influencing the UK’s IIP.

Figure 3 shows the level of the UK’s assets, from 1999 to 2014, broken down by functional category. The functional category that made up the largest proportion of UK assets was OI, at between 107.2% and 266.0% of GDP.

Figure 3: UK assets breakdown by functional categories, as a percentage of GDP, 1999 to 2014

Source: Office for National Statistics

Download this chart Figure 3: UK assets breakdown by functional categories, as a percentage of GDP, 1999 to 2014

Image .csv .xlsGrowth in the level of UK assets was driven mainly by OI (in particular loans and deposits), as well as FD. Prior to 2008, the level of UK assets, PI assets and OI assets were steadily increasing, as a percentage of GDP, apart from in 2002, when the levels decreased. During the period 2000 to 2007, the level of DI remained relatively unchanged as a percentage of GDP, whereas there was a very large increase in the level of financial derivative assets. Since 2008, the level of UK assets has been relatively constant, in £ billion terms, and hence falling as a percentage of GDP. This decrease was a result of falls in DI, OI and FD, as a percentage of GDP, whereas there has been a rise in the level of PI assets. These changes resulted in the stock of UK assets falling from 727.0% of GDP in 2008 to 569.2% of GDP in 2014. The level of RA during the series remained relatively small at around 2% to 4% of GDP.

Figure 4 shows the level of the UK’s liabilities, as a percentage of GDP, from 1999 to 2014, broken down by functional category. The functional category that made up the largest proportion of UK liabilities was OI, at between 138.8% and 276.9% of GDP.

Figure 4: UK liabilities breakdown by functional categories, as percentage of GDP, 1999 to 2014

Source: Office for National Statistics

Download this chart Figure 4: UK liabilities breakdown by functional categories, as percentage of GDP, 1999 to 2014

Image .csv .xlsThe functional category with the largest increase during the series was DI, in particular DI equity capital and reinvested earnings. However, DI only makes up, on average, 11.5% of total UK liabilities, so has a limited effect on the overall stock of liabilities. Between 2002 and 2008, the level of total UK liabilities increased year-on-year, as a percentage of GDP, reaching the highest level of the series at 718.0% of GDP in 2008. Since 2008, the level of UK liabilities has been relatively constant, in £ billion terms, and hence falling as a percentage of GDP. This decrease has been as a result of a fall in OI and FD, as a percentage of GDP, which was partially offset by a rise in the level of DI and PI assets. These changes resulted in the stock of UK liabilities falling from 718.0% of GDP in 2008 to 586.9% of GDP in 2014.

Notes:

- The capital account deficit makes up less than 5% of the total current and capital account deficits

6. Part 2: Drivers of the changes to the net international investment position (IIP)

The second part of this article explains the sizeable movements in the UK’s net IIP, between 1999 and 2014, by disaggregating the changes into their constituent parts. The change in the net IIP is explained by the net acquisition of financial assets and net incurrence of financial liabilities within a particular period (what we refer to as the financial flows) and also other changes, which includes currency changes, price changes and other changes in volume. Revaluations effects, for example, do not reflect a change in the underlying volume of foreign assets or liabilities, but rather reflect a change in their valuation. These changes can be significant for countries like the UK which have a large stock of gross assets and liabilities (Figures 3 and 4).

Figure 5: UK net IIP and cumulative flows, as a percentage of GDP, 1966 to 2014

Source: Office for National Statistics

Download this chart Figure 5: UK net IIP and cumulative flows, as a percentage of GDP, 1966 to 2014

Image .csv .xlsBy looking at the long-run movement in cumulative financial flows, we can appreciate the interconnections between flows and the net IIP. Figure 5 presents both net IIP and the long-run movement in cumulative flows, standardised as a percentage of GDP, for the period 1966 to 2014. Financial investors use the net IIP to GDP ratio to gauge the creditworthiness of a country. As the financial flows are linked to the IIP through a flow-stock relationship, it is not surprising that over the long-term cumulative flows drive the changes to the net IIP. There are, however, also sizeable short-term fluctuations where the net IIP diverges from the cumulative flows, which is where other changes drive the overall change in net IIP.

Nôl i'r tabl cynnwys7. Terminology of flows and other changes

Flows measure transactions in financial assets and liabilities over a specific period (showing how a current account surplus or deficit is financed). The financial flows are presented in the financial account of the balance of payments.

Other changes can be broken down into revaluation effects and other change in volume.

Revaluation effects do not reflect a change in the asset or liability itself but record a change in valuation. These are split between exchange rates and other price changes.

Exchange rate effects occur as the UK’s IIP is denominated in sterling, while assets, and to a lesser extent liabilities, are denominated in a foreign currency. This means that, all else being equal, a depreciation (appreciation) of sterling against foreign currencies will improve (worsen) the UK’s net stock position. Therefore, currency changes have an effect on the stock of UK assets and liabilities. For example, UK residents may hold €2,000 of German assets purchased at an exchange rate of £1: €2. This is recorded as £1,000 of UK owned foreign assets in the UK’s IIP. At the end of the period, if the sterling exchange rate had depreciated to £1: €1, the UK still owns €2,000 of foreign assets, but they are now worth £2,000 because of exchange rate movements. The result is an increase of £1,000 to the UK’s net IIP although the quality of the asset has not changed. In this example, German liabilities are unaffected; they are still recorded as €2,000 in the German IIP.

Price effects arise from changes in the market values of assets and liabilities1, which are traded on world stock markets. For example, a UK household could own £5,000 worth of shares in an Oil and Gas company. Due to its excellent sales performance over the past year, the Oil and Gas company’s shares increased by 20 per cent. The shares are now worth £6,000. The result is that the UK’s assets, and hence the UK’s net IIP, have increased by £1,000. Due to the nature of stock markets, price movements tend to be less pronounced than exchange rate movements, because UK and other world stock markets generally move in a similar direction.

Examples of other changes in volume include debt cancellation and write-offs, reclassifications, entities changing residence, and changes in actuarial assumptions. The financial crisis was a recent example of when resident and non-resident banks wrote off billions from their balance sheets due to the provision of bad debt.

Notes:

- Which include both equities and bonds

8. Other changes and the net IIP

To understand what was driving the divergence in the IIP from the cumulative financial flows (Figure 5), the Office for National Statistics (ONS) has created a model to estimate how much of the change in the IIP was attributed to flows and how much to other changes. Other changes were then subsequently broken down into exchange rate effects, price effects and other changes in volume. The breakdown of changes was calculated for both gross UK assets and gross UK liabilities for the three functional categories. The gross results for UK assets and liabilities were then aggregated and net changes calculated1.

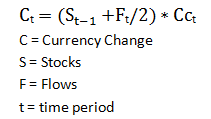

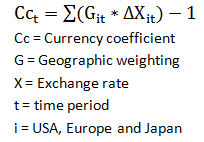

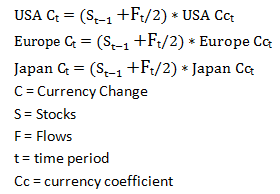

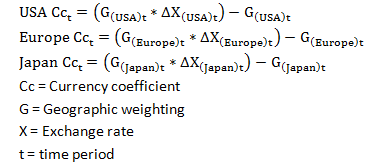

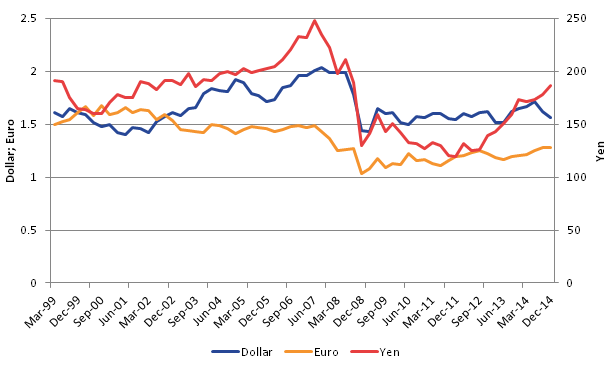

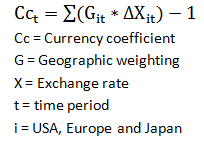

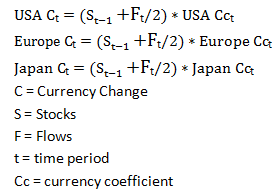

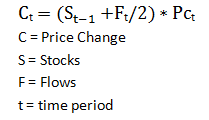

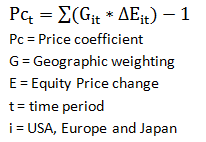

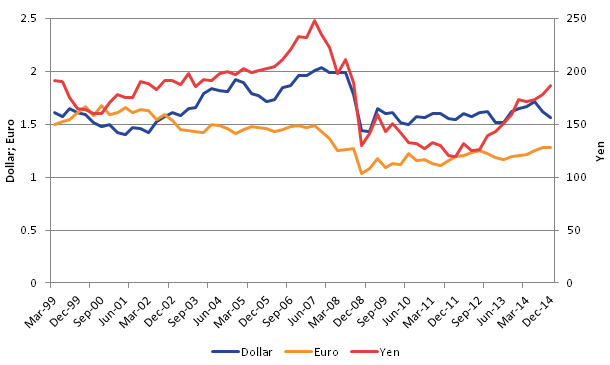

Table 1 shows the net IIP and breakdown of changes, from 2000 to 2014. The first column reports the net IIP, calculated by subtracting liabilities from assets. Changes from the previous year’s IIP are reported in the second column. The changes are then attributed to flows, currency changes, price changes and other changes in volume. Currency changes are calculated using sterling exchange rate movements against the dollar, and against the yen. Annex B goes into more detail on how currency changes are derived in our model and what effect different exchange rates have on DI, PI and OI assets. Price changes are modelled using a combination of stock and bond indices, including end-quarter share prices for the Dow Jones, Euro Stoxx, FTSE and Nikkei exchanges. Annex C provides more detail on how price changes are derived in our model and what effect equity prices had on UK assets and liabilities.

Table 1: The UK’s net IIP and change in IIP, broken down by type of change, £ billion, 2000 to 2014

| (£ billion) | ||||||

| Net IIP | Change in net IIP | Flows | Currency changes | Price changes | Other changes in volume | |

| 2000 | -103 | 95 | -16 | 27 | -21 | 104 |

| 2001 | -139 | -36 | -19 | -18 | 41 | -40 |

| 2002 | -104 | 35 | -21 | 45 | 20 | -9 |

| 2003 | -68 | 36 | -18 | 56 | 1 | -3 |

| 2004 | -142 | -74 | -20 | 0 | -23 | -30 |

| 2005 | -97 | 45 | -7 | -12 | -42 | 106 |

| 2006 | -149 | -52 | -8 | -68 | 22 | 1 |

| 2007 | -148 | 2 | -55 | 117 | -1 | -60 |

| 2008 | -18 | 129 | -160 | 624 | 38 | -373 |

| 2009 | -270 | -252 | 3 | -167 | -182 | 94 |

| 2010 | -170 | 100 | -11 | -8 | -147 | 267 |

| 2011 | -206 | -36 | -31 | -10 | -63 | 68 |

| 2012 | -454 | -248 | -23 | -88 | -54 | -83 |

| 2013 | -381 | 73 | -95 | -46 | 144 | 70 |

| 2014 | -402 | -20 | -85 | -38 | 27 | 75 |

| Cumulative total | -204 | -566 | 413 | -239 | 188 | |

| Source: Office for National Statistics | ||||||

| Notes: | ||||||

| 1. Net IIP figures are not consistent with others published in BoP, as these figures do not include financial derivatives and reserve assets. | ||||||

Download this table Table 1: The UK’s net IIP and change in IIP, broken down by type of change, £ billion, 2000 to 2014

.xls (27.6 kB)Table 1 shows that the UK has consistently been in a net liability position in all years, as shown in Figure 2, with a cumulative fall in the NIIP of £204bn. Over this period, the UK has incurred net financial liabilities of £566bn. However, in terms of the stock position, this has been partially offset by other changes. Between the end of 2007 and the end of 2008, the net liability reduced by £129 billion. This was despite the UK continuing to borrow £160 billion from the rest of the world. The reason it was able to reduce its net liability position, whilst simultaneously increasing borrowing, was mainly due to a positive £624 billion currency effect.

Figure 6 shows the breakdown of the change in UK assets, as a percentage of GDP. The total change in the level of assets was positive in 11 out of the 15 years in the series, meaning that in monetary terms, UK assets increased in the majority of the periods shown.

Figure 6: Change in UK assets breakdown, as a percentage of GDP, 2000 to 2014

Source: Office for National Statistics

Download this chart Figure 6: Change in UK assets breakdown, as a percentage of GDP, 2000 to 2014

Image .csv .xlsFlows made up the largest proportion of the change in assets during the early part of the series, with the largest single change of 61.7% of GDP occurring in 2007. However, in 2008 the 27.8% depreciation of sterling, against the dollar, raised the sterling value of overseas assets, seen by the positive currency change of 133.7% of GDP, which more than offset the negative other changes. Between 2009 and 2014, the level of assets fluctuated, with there being no main driver in the changes in the level of UK assets. Price changes were relatively small throughout the series, but were an offsetting factor in 7 out of the 15 years in the series.

Figure 7 shows the breakdown of the change in UK liabilities, as a percentage of GDP. The total change in the level of liabilities was positive in 12 out of the 15 years in the series, meaning that in monetary terms, UK liabilities increased in the majority of the years shown.

Figure 7: Change in UK liabilities breakdown, as a percentage of GDP, 2000 to 2014

Source: Office for National Statistics

Download this chart Figure 7: Change in UK liabilities breakdown, as a percentage of GDP, 2000 to 2014

Image .csv .xlsFlows made up a large proportion of the changes in UK liabilities during the early part of the series, with the largest change of 65.3% of GDP occurring in 2007. However, in 2008, currency changes more than offset the negative other changes, with an increase of 93.8% of GDP. Between 2009 and 2014 the level of liabilities fluctuated, with no main driver attributed to these changes. Price changes tended to be the second largest effect on the level of UK liabilities throughout the series, with the largest change of 22.4% of GDP occurring in 2009. The positive price effects imply that there was an upward improvement in the UK equity market. Whereas, other changes in volume tended to have the smallest effect on UK liabilities, but were an offsetting factor in 9 out of the 15 years in the series.

Notes:

- See Annex A for more information on model used

9. Conclusion

At the end of 2014, the UK stock of liabilities outstripped the stock of assets, resulting in a net liability position of 17.6% of GDP. Portfolio investment (PI) and other investment (OI) were the functional categories contributing to the net liability position, outweighing the net asset positions in direct investment (DI), financial derivatives (FD) and reserve assets (RA). There is a similar trend seen throughout the series, except for 2008, where PI and OI were outweighed by the other functional categories, creating a net asset position for the UK. This net asset position was primarily caused by the large positive currency affect of £624 billion in 2008, as a result of a sharp depreciation in the sterling exchange rate against other major currencies. Other changes have had a sizeable impact on the UK’s net IIP, particularly when there are large gross assets and liabilities, creating a divergence in the flow-stock relationship.

Nôl i'r tabl cynnwys

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}