Cynnwys

- Main points

- Company incorporations and voluntary dissolutions

- Business impact of the coronavirus

- Social impacts of the coronavirus on Great Britain

- Footfall

- Online job adverts

- Online price change for high-demand products (HDPs)

- Energy Performance Certificates

- Shipping

- Data

- Glossary

- Measuring the data

- Strengths and limitations

- Related links

1. Main points

Company incorporations per working day were lower than usual in April 2020 but above usual levels in June and July 2020, according to data from Companies House; company voluntary dissolution applications per working day were lower than usual throughout April to July 2020. See Section 2.

Of businesses currently trading, 45% reported their turnover exceeded their operating costs, compared with 16% who reported their operating costs exceeded their turnover, according to the Business Impact of Coronavirus (COVID-19) Survey (BICS). See Section 3.

The proportion of adults wearing a face covering when leaving the home continued to increase to 96% from 84% the previous week, according to the latest Opinions and Lifestyle Survey (OPN). See Section 4.

Between 27 July and 2 August, overall footfall continued to gradually increase, driven by an increase in footfall at retail parks. See Section 5.

Of the NUTS1 regions and countries, online Adzuna job adverts in Northern Ireland and London were the closest to their 2019 average, at 66% and 65% respectively. See Section 6.

The index for all food items within the HDP basket fell by 0.9% in the week beginning 27 July, the largest weekly decline since the series began in mid-March. See Section 7.

In the week commencing 27 July 2020, existing Energy Performance Certificate (EPC) lodgements have stabilised to levels observed at the end of February across all regions, while EPC lodgements for new dwellings remain 20% lower for a second consecutive week across England and Wales. See Section 8.

The Business Impact of COVID-19 Survey (BICS) is voluntary and currently unweighted, so it may only reflect the characteristics of those who responded. Online price change analysis is experimental and should not be compared with our regular consumer price statistics. Results presented are experimental.

2. Company incorporations and voluntary dissolutions

This section introduces new weekly indicators of company incorporations and voluntary dissolutions in the UK, using data from Companies House in collaboration with the Office for National Statistics (ONS). We have also published new Experimental Statistics on business creations and closures in the UK from the Inter-Departmental Business Register (IDBR).

In these statistics, companies and businesses are not the same - companies are legal entities, as registered with Companies House; businesses are statistical entities, arranged by the ONS on the IDBR, which better reflect their economic activity. Data are presented per working day to allow comparison between quarterly data and weekly data.

Incorporations

Figure 1 shows during April 2020 and the start of May 2020, the number of company incorporations per working day in the UK was lower than the average number per working day in Quarter 2 (Apr to June) 2019, with 2,372 on average between 4 April and 22 May 2020, compared with 2,786 per working day in Quarter 2 2019.

Between 6 June and 31 July 2020, the average number of incorporations per working day rose to 3,529. As a result, the average figure for Quarter 2 2020 was higher than Quarter 2 2019; 2,887 per working day in Quarter 2 2020 compared with 2,786 per working day in Quarter 2 2019.

These observed fluctuations coincide with government instigated lockdown measures and the subsequent easing of them in response to the coronavirus (COVID-19) pandemic. This is in line with official statistics published by Companies House on 30 July 2020.

Figure 1: Company incorporations per working day were lower in April 2020 compared with the average number in Quarter 2 2019

Company incorporations per working day, UK, quarterly and weekly, Quarter 1 2019 to Quarter 2 2020, and w/c Saturday 28 February 2020 to w/c Saturday 25 July 2020

Source: Companies House and Office for National Statistics

Notes:

- Data presented per working day to allow comparison between quarterly data and weekly data, and account for processing differences associated with Bank Holidays.

- Quarterly data from Companies House official statistics release, divided by number of working days, presented at the mid-point of the Quarter.

- Weekly data are weeks from Saturday to Friday, as incorporation requests received on Saturdays and Sundays are typically processed on subsequent weekdays. Dates shown are Saturdays for the forthcoming week.

- Processing of incorporations occasionally takes place at weekends for incorporation requests received that same weekend – no adjustment for weekend working or overtime is made when dividing by number of working days.

- Incorporations are recorded on the date of acceptance to the Companies House register, which is usually within the same week that the request is received.

Download this chart Figure 1: Company incorporations per working day were lower in April 2020 compared with the average number in Quarter 2 2019

Image .csv .xlsExperimental estimates of new VAT reporters and Experimental Statistics of business births and deaths from the IDBR both suggest business creation remained subdued in Quarter 2 2020. The difference may be the result of differences in methodology and definition, since some types of company are present with Companies House but not on the IDBR or in VAT returns, such as single-person limited companies. For more details, see Section 12.

Voluntary dissolutions

Companies House has continued to accept voluntary dissolution applications during the coronavirus pandemic, which is when a company voluntarily registers its intention to cease trading. Voluntary dissolutions account for just over half of all company closures historically. It should be noted that at present Companies House will not be striking companies applying for voluntary dissolution off the register until 10 September 2020 (see here for more information on this process).

Figure 2 shows between the weeks commencing 4 April and 25 July 2020, the average number of voluntary dissolution applications received per working day was at 942, lower than the average number of applications per working day in Quarter 2 and Quarter 3 (July to Sept) 2019 (1,091 and 1,008 respectively).

Figure 2: Company voluntary dissolution applications per working day were lower in April to July 2020, compared with Quarter 2 and 3 2019

Company voluntary dissolutions applications per working day, UK, quarterly and weekly, Q1 2019 to Q2 2020, and w/c Saturday 28 February 2020 to w/c Saturday 25 July

Source: Companies House and Office for National Statistics

Notes:

- Data presented per working day to allow comparison between quarterly data and weekly data, and account for processing differences associated with Bank Holidays. Quarterly data are presented at the mid-point of the quarter.

- Weekly data are weeks from Saturday to Friday, as voluntary dissolution requests received on Saturdays and Sundays are typically processed on subsequent weekdays. Dates shown are Saturdays for the forthcoming week.

- Data reflect the date at which the voluntary dissolution application is accepted by Companies House, but it often takes 2 to 3 months longer to remove the company from the register in order to give creditors time to register objections. The date of the filing for voluntary dissolution is 3 months after the company has ceased trading.

- Since March 2020, some voluntary dissolutions are automatically accepted when filed, including on weekends. Where checks are required, these are carried out by Companies House on weekdays. No adjustment for weekend working, overtime or automatic acceptance over the weekend is made when dividing by number of working days.

Download this chart Figure 2: Company voluntary dissolution applications per working day were lower in April to July 2020, compared with Quarter 2 and 3 2019

Image .csv .xlsOther measures of company closure not presented

In response to the coronavirus (COVID-19) pandemic, a set of easements were announced by Companies House on 16 April 2020. They included the temporary pause of the strike-off process to give companies affected by the pandemic the time needed to update their records filed with Companies House.

As a result, the compulsory dissolution process was paused. Compulsory dissolution is where companies who fail to fulfil their statutory obligations with Companies House are struck off the register. With this in mind, the overall level of company closures throughout April to July 2020 is lower at present than it would normally be, although these companies may be dissolved via another route, or at a later date.

Another route of company closure not presented here is insolvency, where a company cannot pay its creditors and its affairs are wound up by an insolvency practitioner. Insolvencies make up a small fraction of all company closures, although they tend to be the most high-profile. Insolvencies are not considered in these measures, but monthly data on insolvencies are available from the Insolvency Service.

Voluntary dissolutions presented in Figure 2 are consistent with data from the Insolvency Service, which shows that the number of insolvencies was also lower than usual during April to June 2020. This could be for a few reasons: difficulty for insolvency practitioners in filing for insolvency because of social distancing measures; reduced processing of insolvencies by Companies House and the Insolvency Service because of workplace safety restrictions; and government support for companies during the pandemic. Data from the IDBR, published today, also show a lower rate of business closures in Quarter 2 2020 than usual.

Other countries have likewise not seen a substantial increase in company closures. For instance, Statistics Netherlands reports no substantial change to the level of business bankruptcies in the months to June 2020, the Bank of France reports a substantial fall in corporate bankruptcies in April and May 2020, and Destatis (the German statistical office) also reported a fall in business insolvencies in April 2020. Bankruptcies in the United States are only a little higher in May and June 2020 than in previous years, although the US system is very different to that of the UK.

More about coronavirus

3. Business impact of the coronavirus

This section includes initial results from Wave 10 of the Business Impact of Coronavirus (COVID-19) Survey (BICS) for the period 13 July to 26 July 2020, which closes on 9 August 2020. Out of 24,464 businesses sampled, 19% had responded as of 4 August 2020.

As a user of BICS data, the ONS would like to hear your thoughts on the future of the survey. If you would like to provide your views, please complete this short questionnaire to help shape the future of BICS. The survey will remain open until 21 August 2020.

Figure 3: Two-fifths of businesses who had furloughed staff provided pay top-ups to the Coronavirus Job Retention Scheme

Headline indicators from the Business Impact of Coronavirus (COVID-19) Survey, 13 July to 26 July, UK

Embed code

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes

- All percentages are a proportion of the number of businesses who responded apart from the workforce percentages on furlough leave and receiving pay top-ups, which are proportions of employees for each responding business.

Of all responding businesses:

90% had been trading for more than the last two weeks

3% had started trading again within the last two weeks after a pause in trading

1% had paused trading but intend to restart trading in the next two weeks

4% had paused trading and do not intend to restart in the next two weeks

Of businesses currently trading, 6% of the total workforce had returned to the workplace from furlough in the last two weeks, and 4% had moved from remote working to the normal workplace. Of businesses currently trading or intending to restart in the next two weeks, 4% of the workforce are expected to return from furlough and 4% are expected return from remote working in the next two weeks.

Figure 4 shows how businesses responded when asked how their turnover compared with their operating costs.

Figure 4: Of businesses currently trading, 16% reported their operating costs exceeded their turnover

Percentage of businesses currently trading, UK, 13 July to 26 July 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- The percentages in this chart might not sum to 100% because of rounding.

Download this chart Figure 4: Of businesses currently trading, 16% reported their operating costs exceeded their turnover

Image .csv .xlsA further breakdown of the financial performance of businesses currently trading is shown in Table 1.

| All Industries | |

|---|---|

| Turnover has decreased by more than 50% | 12% |

| Turnover has decreased between 20% and 50% | 20% |

| Turnover has decreased by up to 20% | 22% |

| Turnover has not been affected | 29% |

| Turnover has increased by up to 20% | 7% |

| Turnover has increased between 20% and 50% | 3% |

| Turnover has increased by more than 50% | 1% |

| Not sure | 6% |

Download this table Table 1: Over half (54%) of businesses currently trading reported a decrease in turnover compared with what is expected for this time of year

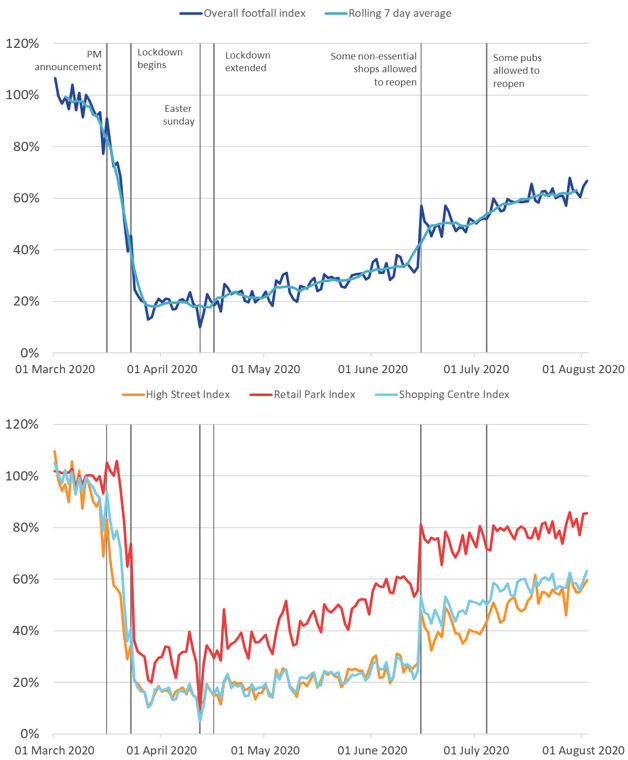

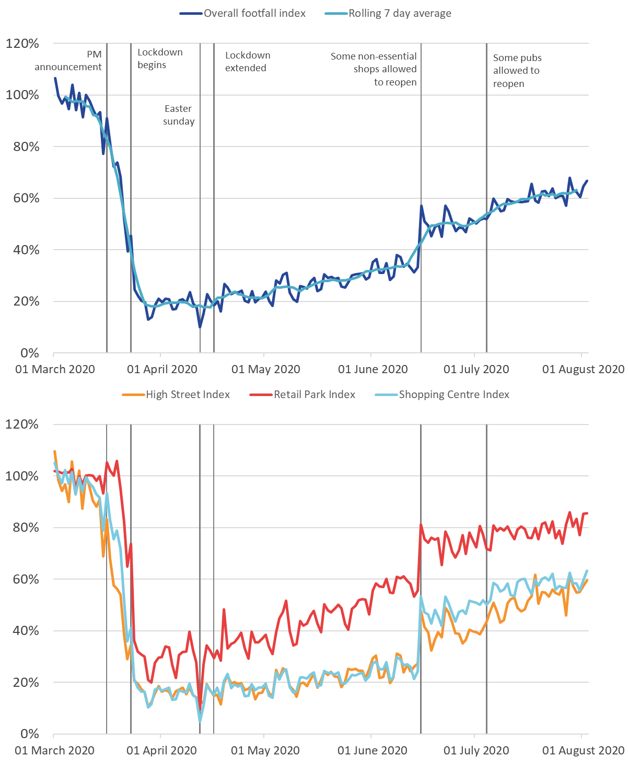

.xls .csv5. Footfall

These figures are provided by Springboard, a provider of data on customer activity. They measure the volume of footfall compared with the same day the previous year at the overall level and across the categories of high streets, retail parks and shopping centres. For example, Tuesday 14 July 2020 was compared with Tuesday 16 July 2019.

Figure 6 shows the overall footfall seven-day average continued to increase in the week 27 July to 2 August 2020, at over 60% when compared with its previous level on the same day a year ago. This continues the gradual increase in footfall seen since the re-opening of non-essential shops and businesses in England, on 15 June.

The increase in overall footfall was driven by an uplift in the retail park index in the latest week, to around 85% of its level in the previous year, compared with around 80% in the week before. High street and shopping centre footfall remained relatively steady at around 55% and 60% respectively, similar to their levels in the previous week.

Figure 6: Between 27 July and 2 August, overall footfall continued to gradually increase

Volume of footfall, UK, 1 March to 2 August 2020, year-on-year percentage change between footfall on the same day

Source: Springboard and the Department for Business, Energy and Industrial Strategy

Notes:

- Many essential shops were allowed to open on 15 June 2020 in England, 12 June 2020 in Northern Ireland and 22 June in Wales. In Scotland, some non-essential shops were allowed to reopen from 29 June, and more from 13 to 15 July.

- “Prime Minister’s announcement” refers to the advisory announcement on 16 March 2020 to avoid non-essential travel, bars, restaurants and other indoor leisure venues, and to work from home if possible.

- Pubs were allowed to reopen on 4 July in both England and Northern Ireland, with beer gardens allowed to reopen on 6 July in Scotland and 13 July in Wales. Pubs were also allowed to reopen indoors in Scotland on 15 July.

Download this image Figure 6: Between 27 July and 2 August, overall footfall continued to gradually increase

.PNG (128.4 kB){kind=link}

6. Online job adverts

These figures use job adverts provided by Adzuna, an online job search engine. For the first time, we are able to include estimates of online job adverts by UK country and NUTS1 regions. These estimates are experimental and will be developed over the coming weeks. The number of job adverts over time is an indicator of the demand for labour.

Figure 7: Between 24 and 31 July 2020, the total volume of online job adverts held steady at just above 50% of its 2019 average

Total weekly job adverts on Adzuna, UK, 4 January 2019 to 31 July 2020: index 2019 average = 100

Embed code

Notes:

The observations were collected on a roughly weekly basis; however, they were not all observed at the same point in each week, leading to slightly irregular gaps between each observation.

These series have a small number of missing weeks, mostly in late 2019, and the latest is in January 2020. These values have been imputed using linear interpolation. The data points that have been imputed are clearly marked in the accompanying dataset.

Further category breakdowns are included in the Online job advert estimates dataset, and more details on the methodology can be found in Using Adzuna data to derive an indicator of weekly vacancies.

Overall, between 24 and 31 July the total volume of online job adverts remained broadly in line with the previous week, increasing slightly from 52% to 53% of its 2019 average. It has stayed close to half the 2019 average since early June, indicating online job adverts have been slow to recover from their low point on 1 May 2020 (42% of the 2019 average).

More than three quarters of Adzuna categories increased compared with the previous week. In particular, the volume of online job adverts in the category of transport, logistics, and warehousing increased five percentage points to 71% of its 2019 average. This increase continues a trend seen over the previous four weeks, starting from a value of just 33% of its 2019 average four weeks ago.

The categories presented here were selected because of user interest, or because they more closely track trends in the Office for National Statistics (ONS) vacancies data. Note that the Adzuna categories used do not correspond to Standard Industrial Classification (SIC) categories, so these values are not directly comparable with the ONS Vacancy Survey.

Figure 8 shows the latest volume of online job adverts in each NUTS1 region and country compared with the 2019 average, the percentage point change from the 2019 average to the lockdown minimum (which may be a different date for each region and country), and the percentage point change from the lockdown minmum to the latest value.

Figure 8: Of the NUTS1 regions and countries, online job adverts in Northern Ireland and London were the closest to their 2019 average, at 66% and 65% respectively

Total weekly job adverts on Adzuna, UK, 4 January 2019 to 31 July 2020: index 2019 average = 100, percentage points

Source: Adzuna

Notes:

- Full series for each country and the NUTS1 regions are available in the accompanying dataset.

Download this chart Figure 8: Of the NUTS1 regions and countries, online job adverts in Northern Ireland and London were the closest to their 2019 average, at 66% and 65% respectively

Image .csv .xlsOn 31 July, of the UK’s countries and NUTS1 regions, online job adverts were closest to their 2019 average in Northern Ireland and London, where they were respectively 34% and 35% below their 2019 averages.

The regions with the lowest job adverts compared with their 2019 averages were Yorkshire and The Humber, and the East of England, where online job adverts were both 58% below their 2019 averages.

The yellow bars in Figure 8 show the size of the fall in adverts from the 2019 average to the lockdown minimum. Note that immediately before lockdown the volume of online job adverts was not exactly at its 2019 average level, so these values cannot be directly interpreted as the fall during lockdown.

The East of England reached the lowest lockdown level compared with its 2019 average at 68% below, followed by the South East which fell to 65% below.

The blue bars in Figure 8 show the change from the lockdown minimum to the latest value, expressed as percentage points of the 2019 average. The strongest recoveries since each region’s lockdown low were in Northern Ireland (22 percentage points) and London (21 percentage points). The weakest recoveries in online job adverts were in Yorkshire and The Humber (six percentage points) followed by the East of England (10 percentage points).

Nôl i'r tabl cynnwys7. Online price change for high-demand products (HDPs)

A timely indication of weekly price change for high-demand products (HDPs) has been developed, covering the period 16 March to 2 August 2020. A timeline of developments for these indicators can be found in Online price changes of high-demand products methodology. This analysis is experimental and should not be compared with our regular consumer price statistics.

Figure 9: The index for all food items within the HDP basket fell by 0.9%, the largest weekly decline since the series began in mid-March

Online price change of high-demand products, UK, percentage change between Week 19 (20 to 26 July) and Week 20 (27 July to 2 August)

Source: Office for National Statistics – Faster indicators

Notes:

- As well as food, and household and hygiene products, the all items index contains items such as pet food and medicines which mean that the all items index sometimes moves differently to the two subseries.

- More information on the strengths and limitations of the online price changes data is available in the Online price changes of high-demand products methodology article.

Download this chart Figure 9: The index for all food items within the HDP basket fell by 0.9%, the largest weekly decline since the series began in mid-March

Image .csv .xlsFigure 9 shows that while the overall index and the all household and hygiene index both increased by 0.1%, the all food index decreased by 0.9%, the largest weekly decline since the series began in mid-March. The decline in prices in the latest week was driven by several food items decreasing in price, and in particular a large decrease in the price of pasta sauce (negative 3.5%) as several retailers put these products on promotion.

Figure 10 shows that the three main indices remain below the starting point of the series (16 March), with the overall index at 1.2 percentage points below the starting point, the all household and hygiene index at 1.9 percentage points below, and the all food index at 1.1 percentage points below. This is the second consecutive week that the food index has been below the Week 1 level in mid-March.

Figure 10: The all food index has remained below its Week 1 level (16 March to 22 March) for the second consecutive week

Online price change of selected high-demand products 16 March to 2 August: index Week 1 (16 to 22 March) = 100, UK

Source: Office for National Statistics – Faster indicators

Notes:

- Index movements may not be exactly the same as percentage changes shown in Figure 9 as a result of rounding.

- Week 1 refers to the period 16 to 22 March 2020, and Week 20 refers to the period 27 July to 2 August.

- The time series for all individual HDP items are published in a dataset alongside this release.

Download this chart Figure 10: The all food index has remained below its Week 1 level (16 March to 22 March) for the second consecutive week

Image .csv .xls8. Energy Performance Certificates

This release includes weekly Energy Performance Certificates (EPCs) for new and existing domestic properties in England and Wales, split by NUTS1 English regions. The EPCs for domestic properties are published weekly by the Ministry of Housing, Communities and Local Government (MHCLG). As such, they can be used as a timely indicator for the number of completed constructions and number of transactions.

More information on the EPC methods, strengths and limitations is available in the accompanying methodology article.

Figure 11 shows in the week commencing 27 July 2020, existing EPC lodgements have stabilised to levels observed at the end of February across all regions. EPC lodgements for new dwellings remain 20% lower for a second consecutive week across England and Wales combined. A reduction in construction would contribute to the slower recovery in EPC assessments of new dwellings.

The spike in the number of EPCs for existing dwellings seen in Wales during the weeks commencing 8 and 15 June 2020 was caused by local authorities in Wales reviewing their social housing stock.

Figure 11: In the week commencing 27 July 2020, existing EPC lodgements across all regions have stabilised to levels observed at the end of February

Existing and new Energy Performance Certificates lodgements by region, non-seasonally adjusted, February 2020 to July 2020. Percentage change since week commencing 24 February 2020

Embed code

Source: Ministry of Housing, Communities and Local Government (MHCLG) Domestic Energy Performance Certificate Register

Notes:

Further notes are available in the weekly EPCs for domestic properties dataset.

Week commencing 24 February 2020 is when the time series begins; we will look to expand this in the future.

Wales shown on a different scale.

9. Shipping

These shipping indicators are based on counts of all vessels, cargo and tanker vessels and passenger vessels. As discussed in Faster indicators of UK economic activity: shipping, we expect the shipping indicators to be related to the import and export of goods.

Figure 12: Between 27 July and 2 August there was an average of 389 daily visits from all ships, compared with 384 in the previous week

Daily movements in shipping visits, UK, seasonally adjusted, 1 January to 2 August 2020

Source: exactEarth

Download this chart Figure 12: Between 27 July and 2 August there was an average of 389 daily visits from all ships, compared with 384 in the previous week

Image .csv .xls

Figure 13: Between 27 July and 2 August, there was an average of 92 daily visits for passenger ships, the same as the previous week

Daily movements in shipping visits, UK, seasonally adjusted, 1 January to 2 August 2020

Source: exactEarth

Notes:

- The number of visits for Hull are included in these data from 1 June 2020 onwards.

- The seasonally adjusted and trend estimates are estimated using a modified version of the seasonal adjustment method TRAMO-SEATS. More information is available in the Coronavirus and the latest indicators for the UK economy and society methodology

- The seasonal adjustment method may be limited as this is a short time series.

- Daily and weekly shipping visits and unique visits are available by port in the dataset, along with non-seasonally adjusted aggregate series.

Download this chart Figure 13: Between 27 July and 2 August, there was an average of 92 daily visits for passenger ships, the same as the previous week

Image .csv .xls10. Data

Weekly and daily shipping indicators

Dataset | Released 6 August 2020

The weekly and daily shipping indicators dataset associated with the faster indicators of UK economic activity.

Online price changes for high-demand products

Dataset | Released 6 August 2020

Weekly online price changes of selected high-demand products (HDPs).

Online job advert estimates

Dataset | Released 6 August 2020

Experimental job advert indices covering the UK job market.

11. Glossary

Faster indicator

A faster indicator provides insights into economic activity using close-to-real-time big data, administrative data sources, rapid response surveys or Experimental Statistics, which represent useful economic and social concepts.

High-demand product (HDP) basket

The HDP basket contains everyday essential items that were identified at the beginning of the crisis to have high consumer demand, including items from food, health and hygiene categories. The selection of these items was based on anecdotal evidence on patterns of consumer spend. The basket does not cover all items within these categories.

Incorporations Company

Incorporations are when a company is added to the Companies House register of limited companies. This can also include where an existing business applies to become a limited company, where it was not one before.

Voluntary dissolutions

A voluntary dissolution is when a company applies to begin dissolution proceedings. As such, they effectively chose to be removed from the Companies House register. For a company to be eligible to voluntarily dissolve, it should not have completed any trading activity for a period of three months.

Nôl i'r tabl cynnwys12. Measuring the data

Detailed information on the data sources, quality and methodology of the different indicators included in this bulletin is available in the Coronavirus and the latest indicators of the UK economy and society methodology.

Detailed information on the new weekly indicators of company incorporations and voluntary dissolutions is available in Weekly indicators of company creations and closures from Companies House methodology: August 2020.

Detailed information on the new regional breakdowns of Adzuna job adverts data is available in Using Adzuna data to derive an indicator of weekly vacancies: Experimental Statistics.

We will summarise any crucial updates to the quality or methodology in this section in the future.

Nôl i'r tabl cynnwys13. Strengths and limitations

Detailed information on the strengths and limitations of the different indicators included in this bulletin is available in the Coronavirus and the latest indicators of the UK economy and society methodology.

Detailed information on the strengths and limitations of the new weekly indicators of company incorporations and voluntary dissolutions is available in Weekly indicators of company creations and closures from Companies House methodology: August 2020.

Detailed information on the strengths and limitations of the new regional breakdowns of Adzuna job adverts data is available in Using Adzuna data to derive an indicator of weekly vacancies: Experimental Statistics.

We will summarise any crucial updates or warnings in this section in the future.

Nôl i'r tabl cynnwys

4. Social impacts of the coronavirus on Great Britain

This section includes some headline results from Wave 20 of the Opinions and Lifestyle Survey (OPN) covering the period 29 July to 2 August 2020. The full results will be published in Coronavirus and the social impacts on Great Britain on 7 August 2020.

Figure 5 shows that the proportion of adults wearing a face covering in the previous week when leaving the home continued to increase, from 84% when asked between 22 to 26 July 2020, to 96% when asked between 29 July to 2 August. This continues an increasing trend after face coverings became mandatory on public transport in England on 15 June, and in other enclosed public spaces in England on 24 July. In Scotland, face coverings on public transport were mandated on 22 June, and in shops on 10 July. In Wales, face coverings on public transport were mandated on 27 July.

The proportion of adults shopping for necessities including food and medicine decreased to 64% from 71% the previous week, while the proportion shopping for items other than food and medicine remained stable this week at 22%. The proportion of people travelling to work decreased slightly to 51%, while the proportion working from home exclusively remained stable at 25%.

Figure 5: The proportion of adults wearing a face covering when leaving the home increased to 96% from 84% the previous week

Proportion of adults, Great Britain, 14 May to 2 August 2020

Source: Office for National Statistics – Opinions and Lifestyle Survey

Notes:

Download this chart Figure 5: The proportion of adults wearing a face covering when leaving the home increased to 96% from 84% the previous week

Image .csv .xls