Cynnwys

- Main points

- Statistician’s comment

- Summary

- The rise in the 12-month growth rate of the Consumer Prices Index including owner occupiers’ housing costs (CPIH) in January 2020 reflects rises in both core and non-core components

- Components other than crude oil drove the increase in the 12-month growth rate of the input Producer Price Index (PPI) to 2.1% in January 2020

- Increased London house price growth may reflect a larger shift in the type of properties being sold than usual, with more sales of very high value properties

- Authors

1. Main points

The 12-month growth rates of the Consumer Price Index including owner occupiers' housing costs (CPIH), the input Producer Price Index (PPI) and the output PPI all rose in January 2020.

The annual growth rate of the UK House Price Index (HPI) rose to 2.2% in December 2019.

The rise in the 12-month growth rate of the Consumer Prices Index including owner occupiers’ housing costs (CPIH) in January 2020 reflects rises in both core and non-core components.

While crude oil has remained the largest contributor to the 12-month growth rate in input PPI, recent changes are driven mainly by changing contributions from components other than crude oil.

Increased London house price growth may reflect a larger shift in the type of properties being sold than usual, with more sales of very high value properties.

2. Statistician’s comment

Commenting on today’s inflation figures, ONS Head of Inflation Mike Hardie said:

“The rise in inflation is largely the result of higher prices at the pump and airfares falling by less than a year ago. In addition, gas and electricity prices were unchanged this month, but fell this time last year due to the introduction of the energy price cap.

“Annual house prices grew across all regions of the UK, the first time this has happened in nearly two years, with London seeing its strongest growth since October 2017.”

Nôl i'r tabl cynnwys3. Summary

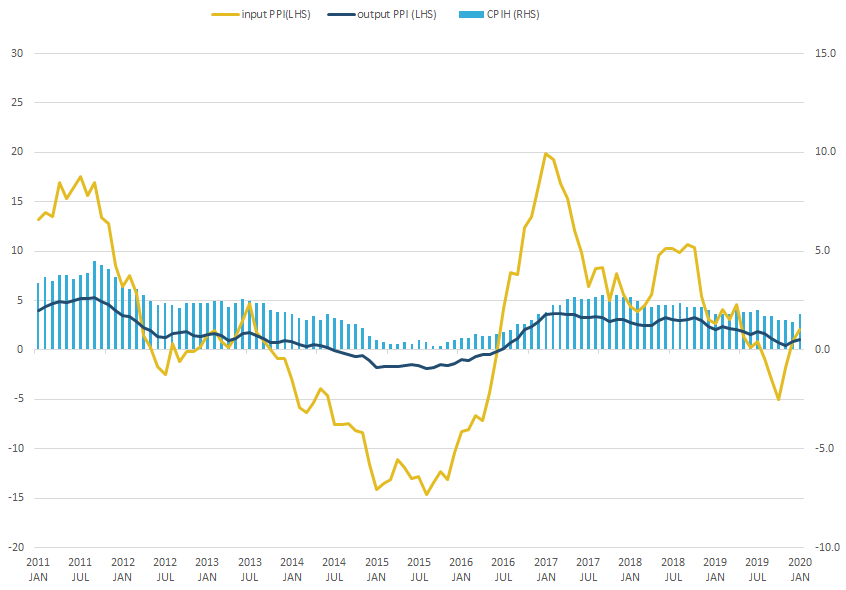

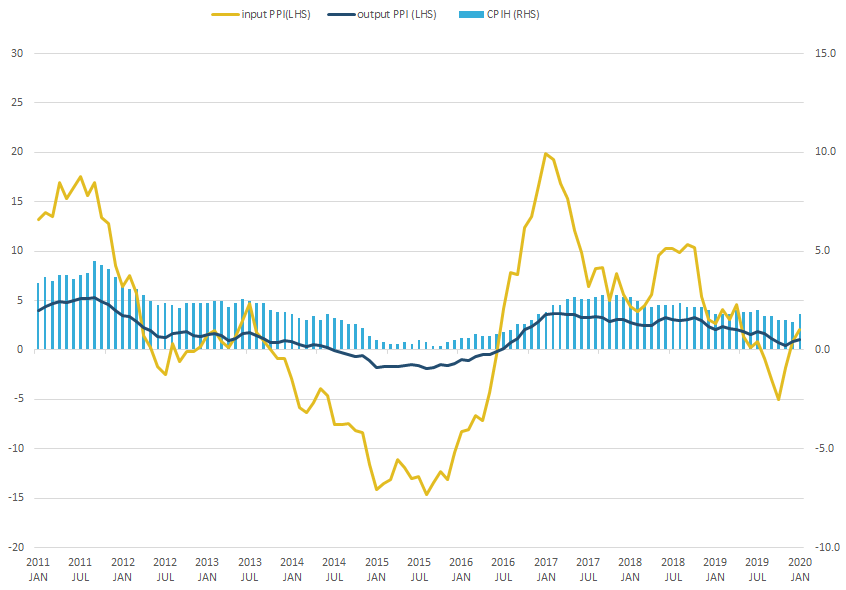

Figure 1 shows the 12-month growth rate of the Consumer Prices Index including owner occupiers’ housing costs (CPIH), which was 1.8% in January 2020, increasing from 1.4% in December 2019.

Upward contributions came from housing and household services, transport, clothing and footwear, and restaurants and hotels. Downward contributions came from furniture, household equipment and maintenance; and food and non-alcoholic beverages.

The output Producer Price Index (PPI) grew by 1.1% in the 12 months to January 2020, up from 0.9% in December 2019. This is the highest rate since September 2019, with nine out of ten groups providing upward contributions to the annual rate of output inflation.

The input Producer Price Index (PPI) rose by 2.1% in the 12 months to January 2020, up from 0.9% in December 2019. This is the highest rate since April 2019, with crude oil providing the largest upward contribution to the annual rate of input inflation.

Figure 1: The 12-month growth rates of input PPI, output PPI, and CPIH rose between December 2019 and January 2020

12-month growth rates for input Producer Price Index (PPI) (left-hand side), output PPI (left-hand side), and Consumer Prices Index including owner occupiers' housing costs (CPIH) (right-hand side) UK, January 2011 to January 2020, %

Source: Office for National Statistics – Producer Price Index and Consumer Prices Index including owner occupiers' housing costs

Notes:

- These data are also available within the Dashboard: Understanding the UK economy.

Download this image Figure 1: The 12-month growth rates of input PPI, output PPI, and CPIH rose between December 2019 and January 2020

.png (33.9 kB) .xlsx (21.5 kB){kind=link}

4. The rise in the 12-month growth rate of the Consumer Prices Index including owner occupiers’ housing costs (CPIH) in January 2020 reflects rises in both core and non-core components

The consumer prices index including owner occupiers’ housing costs (CPIH) can be split into core and non-core components. Core CPIH strips out some of the most volatile components of CPIH to show underlying trends in the rest of the basket. Core components make up around 84% of the CPIH basket, and non-core the remaining 16%.

In January 2020, the 12-month growth rate of CPIH was 1.8%, increasing from 1.4% in December 2019, its highest rate since July 2019. This change was driven by both core and non-core CPIH, which have increased by 0.2 and 1.5 percentage points respectively, from December 2019 to January 2020.

Figure 2: 12-month growth rates of CPIH, core CPIH, and non-core CPIH all increased in January 2020

12-month growth rates for all items CPIH, core CPIH and non-core CPIH, UK, January 2016 to January 2020, %

Source: Office for National Statistics – Consumer Prices Index including owner occupiers’ housing costs

Notes:

- Non-core CPIH includes: food and non-alcoholic beverages; alcohol and tobacco; electricity, gas, liquid fuels, solid fuels; and fuels and lubricants.

- Core CPIH includes: clothing and footwear; housing and water; furniture and household goods; health; transport excluding fuels and lubricants; communication; recreation and culture; education; restaurants and hotels; and miscellaneous goods and services.

Download this chart Figure 2: 12-month growth rates of CPIH, core CPIH, and non-core CPIH all increased in January 2020

Image .csv .xlsFigure 3 shows the contributions of non-core CPIH components to the 12-month growth rate of CPIH in each month since January 2016. The contribution from the energy component rose sharply in January 2020, becoming positive after three months of negative contributions from October to December 2019.

This sharp increase in contribution from energy is the result of a base effect, as prices remained unchanged between December 2019 and January 2020, but fell between December 2018 and January 2019. The Office of Gas and Electricity Markets (Ofgem) introduced an initial cap on consumer prices for energy in January 2019, with price falls for both gas and electricity. The cap was then increased in April 2019 and lowered again in October 2019.

The negative contributions from energy between October and December 2019 indicate that the current level of energy prices (which includes both capped prices for gas and electricity, and prices for fuels and lubricants) is lower than the prices consumers faced before the initial introduction of the gas and electricity price cap in January 2019. The positive contribution from energy in January 2020, however, reflects that the current price level is higher than the level when the initial cap was in effect from January to April 2019.

Figure 3: Energy made a positive contribution to the 12-month growth rate of CPIH in January 2020

Contributions to the 12-month growth rate of all items CPIH from non-core CPIH components, UK, January 2016 to January 2020, percentage points

Source: Office for National Statistics – Consumer Prices Index including owner occupiers’ housing costs

Notes:

- Energy includes: electricity, gas, liquid fuels, solid fuels and fuels and lubricants.

Download this chart Figure 3: Energy made a positive contribution to the 12-month growth rate of CPIH in January 2020

Image .csv .xlsFigure 4 shows contributions to the 12-month growth rate of CPIH from the core CPIH components since January 2016. The net contribution from core components of CPIH has been positive across the period and relatively stable when compared with non-core CPIH.

Housing (including rents, owner occupiers’ housing costs (OOH), repair and maintainence, and Council Tax or rates), and water (and sewerage) have consistently been one of the largest contributors to the 12-month growth rate across the period. All core components made positive contributions to the 12-month growth rate of CPIH in January 2020, and all made higher contributions than in December 2019 except for furniture and household goods, and recreation and culture.

Figure 4: All components of core CPIH have made positive contributions in January 2020

Contributions to the 12-month growth rate of all items CPIH from core CPIH components, UK, January 2016 to January 2020, percentage points

Source: Office for National Statistics – Consumer Prices Index including owner occupiers’ housing costs

Notes:

- Housing and water is the component “housing and household services” excluding gas, electricity and other fuels, which are part of the non-core component energy.

- Other goods and services includes health, communication, education, and miscellaneous goods and services.

Download this chart Figure 4: All components of core CPIH have made positive contributions in January 2020

Image .csv .xlsThe contribution from transport has broadly fallen over recent months, picking up slightly in January 2020 from its lowest contribution of the period at 0.06 percentage points in December 2019. Even when excluding fuels and lubricants, transport remains one of the more volatile components of CPIH as it contains elements that are also affected by fuel prices, such as passenger transport by air. Although oil prices rose in the first four months of 2019, they have fluctuated and generally fallen since.

Recreation and culture is one of the most volatile components of core CPIH. Its contributions have ranged from negative 0.02 percentage points in March 2016 to 0.43 percentage points in August 2019.

Volatility in recreation and culture is largely driven by computer games, likely explaining the decreased contribution to the 12-month growth rate of CPIH between August and December 2019. The period marked consistent negative contributions from computer games, last seen in the same period in 2016, which also resulted in relatively low contributions from recreation and culture.

Nôl i'r tabl cynnwys5. Components other than crude oil drove the increase in the 12-month growth rate of the input Producer Price Index (PPI) to 2.1% in January 2020

The 12-month growth rate of Input PPI was 2.1% in January 2020, up from 0.9% in December 2019, its highest rate since April 2019 when prices grew 4.6% on the year. This is the second successive month of positive price growth in input producer prices following four months in which prices fell on the year.

Five out of the nine components made positive contributions to the 12-month growth rate of input PPI in January 2020. Crude oil made the largest upward contribution in January 2020, at 1.80 percentage points, while imported chemicals made the largest downward contribution at negative 0.96 percentage points.

Figure 5: The 12-month growth rate of input PPI rose between December 2019 and January 2020

Contributions to the 12-month growth rate of input PPI, the 12-month growth rates of input PPI and the inverted sterling effective exchange rate (IER), UK, January 2015 to January 2020

Source: Office for National Statistics – Producer Prices Index and Bank of England - Monthly average Effective exchange rate index, Sterling (Jan 2005 = 100)

Notes:

- Contributions may not sum to the 12-month growth rate because of rounding.

Download this chart Figure 5: The 12-month growth rate of input PPI rose between December 2019 and January 2020

Image .csv .xlsCrude oil has remained the largest contributor to the 12-month growth rate accounting for at least one-third of the movement in the overall growth rate in every month since June 2019. Its contribution remained relatively unchanged between December 2019 and January 2020.

Oil prices are affected by a range of global events, which can cause sudden large price movements. As these events are often not regular or seasonal, the 12-month growth rate can amplify the effect of these sudden price changes, as the rate reflects changes in both the current year and the previous year.

Figure 6: Crude oil has remained the largest contributor to the 12-month growth rate of input PPI, but recent changes are driven mainly by other components

Contribution of crude oil, and all other components of input PPI to the 12-month growth rate UK, January 2015 to January 2020

Source: Office for National Statistics – Producer Prices Index

Notes:

- Other components includes: fuel (including Climate Change Levy); home-produced food; imported food; other home-produced material; imported metals; imported chemicals; other imported parts and equipment; other imported materials.

- Contributions may not sum to the 12-month growth rate because of rounding.

Download this chart Figure 6: Crude oil has remained the largest contributor to the 12-month growth rate of input PPI, but recent changes are driven mainly by other components

Image .csv .xlsNet contributions from all components of input PPI, excluding crude oil, have switched from negative 0.89 percentage points in December 2019 to 0.30 percentage points in January 2020. Contributions from crude oil over the same period remained relatively unchanged, increasing slightly from 1.79 percentage points to 1.80 percentage points.

This increase in the contribution from other components is partly driven by the recent jump in imported metals prices, which rose 15.8% on the year in January 2020, up from 6.6% in December 2019. In January 2020, imported metals made their largest contribution to the overall annual growth rate of input producer prices since September 2017.

One such imported metal is palladium, a precious metal used in catalytic converters for petrol-fuelled and hybrid cars. Demand for palladium has outstripped supply for the past decade, alongside increasing drive from governments and consumers to reduce carbon emissions. As palladium is a secondary product of mining platinum and nickel, suppliers have little flexibility in stepping up production in response to high prices. Palladium reached its highest ever price on record in January 2020, peaking at $2582.19 per ounce.

Nôl i'r tabl cynnwys6. Increased London house price growth may reflect a larger shift in the type of properties being sold than usual, with more sales of very high value properties

In December 2019, average house prices in London grew by 2.3% on the year, the highest rate since October 2017. This is a sharp increase from growth of 0.4% in the year to November 2019, and the fall in average prices of 1.2% seen in the year to October 2019.

An increase in the average growth rate does not necessarily reflect an increase in prices across the board, and could instead be the result of a larger than usual shift in the type of properties being sold. This is particularly relevant in London where there is large variation in property prices, and a considerable number of very high value properties, sales of which could affect average price growth.

Purchases of very high value properties may be particularly affected by considerations such as uncertainty, including around the effects of the UK’s withdrawal from the EU, expectations of actual or potential tax changes, and other factors that may have an impact on their ongoing value.

Figure 7 shows sales volumes, as a proportion of total sales, by price bracket, for properties in inner London for October, November and December 2019, with Figure 8 showing the same for outer London. Property prices are generally higher in inner London than outer London – in December 2019 average prices were £574,800 in inner London and £429,500 in outer London.

Figure 7: The proportion of property transactions in inner London over £900,000 rose sharply in December 2019

Proportion of property transactions per month, by price bracket, inner London, October 2019 to December 2019, %

Source: HM Land Registry and Office for National Statistics – UK House Price Index

Notes:

- Inner London includes the following boroughs: City of London, Camden, Greenwich, Hackney, Hammersmith and Fulham, Islington, Kensington and Chelsea, Lambeth, Lewisham, Newham, Southwark, Tower Hamlets, Wandsworth, and Westminster.

Download this chart Figure 7: The proportion of property transactions in inner London over £900,000 rose sharply in December 2019

Image .csv .xls

Figure 8: For outer London there was a slight increase in the proportion of property transactions over £900,000 in November and December 2019

Proportion of property transactions per month, by price bracket, outer London, October 2019 to December 2019, %

Source: HM Land Registry and Office for National Statistics – UK House Price Index

Notes:

- Outer London includes the following boroughs: Barking and Dagenham, Barnet, Bexley, Brent, Bromley, Croydon, Ealing, Enfield, Haringey, Harrow, Havering, Hillingdon, Hounslow, Kingston, Merton, Redbridge, Richmond, Sutton, and Waltham Forest.

Download this chart Figure 8: For outer London there was a slight increase in the proportion of property transactions over £900,000 in November and December 2019

Image .csv .xlsOuter London has had a higher concentration of property transactions at the lower end of the price scale. Inner London has had prices that are more spread, and a considerably higher proportion of transactions at the higher end of the price scale. For example, at no point in the last three months did inner London have more than 50% of property transactions in any one price bracket. For outer London, almost 60% of transactions were in the £300,000 to £600,000 price bracket in all three months.

Between November and December 2019, inner London saw a fall in the proportion of transactions in the three lowest price brackets (up to £900,000) and increases in all the higher price brackets, except for £2.7 million to £3.0 million, which saw a slight decrease.

Overall, around 27% of transactions in December 2019 were of properties over £900,000. This is considerably higher than in October and November 2019 when, respectively, around 21% and 20% of transactions were of properties over £900,000. This suggests that there may be some compositional effect in the increase in house price growth in December 2019.

For outer London, the proportion of transactions below £300,000 fell between November and December 2019, while the proportions in the £300,000 to £600,000 and £600,000 to £900,000 brackets remained almost unchanged. Outer London also saw a slight increase in the proportion of transactions over £900,000 from around 8% in October 2019, to 9% in November and 10% in December.

Nôl i'r tabl cynnwys