1. Main points

The 12-month growth rate of the Consumer Prices Index including owner occupiers' housing costs (CPIH) was 1.5% in November 2019, unchanged from October 2019.

The output Producer Price Index (output PPI) grew by 0.5% in the 12 months to November 2019, down from 0.8% in the 12 months to October 2019.

The input Producer Price Index (input PPI) fell by 2.7% in the 12 months to November 2019, up from negative 5% in the 12 months to October 2019.

Inflation rates for retired and non-retired households have diverged in 2019.

Wholesale electricity and gas prices have fallen sharply since the beginning of 2019.

UK countries and English regions with higher average house prices tend to have seen lower differences in growth of house prices and rental prices since January 2015.

2. Statistician’s comment

Commenting on today’s inflation figures, ONS Head of Inflation Mike Hardie said:

“The headline rate of inflation remained steady with prices rising across a variety of goods and services such as chocolate, concert tickets and package holidays, offset by falling hotel costs and cigarette prices rising substantially slower than this time last year.

“UK house price growth slowed to its lowest annual rate in over seven years, with London again providing the biggest drag, offset by growth in Northern Ireland, Wales and Yorkshire.”

Nôl i'r tabl cynnwys3. Summary

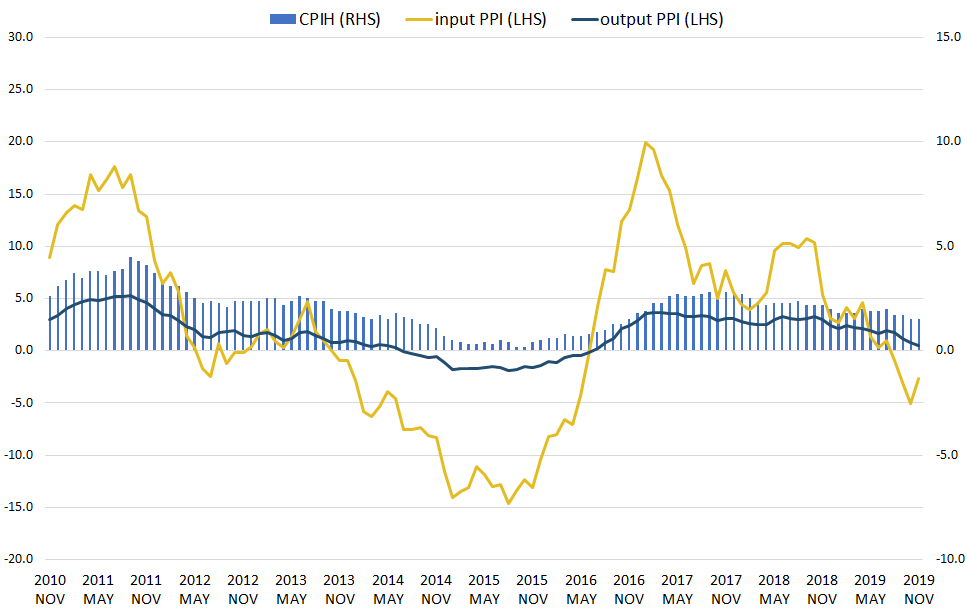

Today's inflation figures are in line with the Bank of England's inflation forecast. Figure 1 shows that the 12-month growth rate of the Consumer Prices Index including owner occupiers' housing costs (CPIH) was 1.5% in November 2019, unchanged from October 2019. The annual rate was last lowest in October 2016.

Upward contributions came from food and non-alcoholic beverages (particularly sugar, jams, syrups, chocolate and confectionery), with smaller contributions from recreation and culture, transport, housing and household services, and furniture, household equipment and maintenance. These were completely offset by downward contributions from restaurants and hotels, alcoholic beverages and tobacco, and clothing and footwear.

The output Producer Price Index (output PPI) grew by 0.5% in the 12 months to November 2019, down from growth of 0.8% in the 12 months to October 2019. Eight out of ten product groups provided upward contributions to the annual rate of output inflation, with petroleum, and chemicals and pharmaceuticals being the only groups providing a downward contribution.

The input Producer Price Index (input PPI) fell 2.7% in the 12 months to November 2019, up from a negative growth of 5% in the 12 months to October 2019. This is the fourth consecutive month that the rate has been negative, although it has picked up for the first time since July 2019. Crude oil provided the largest downward contribution to the annual rate of input inflation.

The Bank of England monitors inflation and growth in the UK economy in order to set the Bank interest rate. Currently, the Bank of England targets a Consumer Prices Index (CPI) 12-month growth rate of 2%. The Bank of England expects inflation in the UK to fall further next year, partly because of the recent falls in gas and electricity bills, the fall in sterling oil prices over the past year, and forecast falls in water bills in April 2020. Beyond that, it expects rising excess demand to increase inflationary pressures.

Figure 1: The 12-month growth rates of input PPI rose and output PPI fell in the year to November 2019

12-month growth rates for input Producer Price Index (PPI) (left-hand side), output PPI (left-hand side), and Consumer Prices Index including owner occupiers' housing costs (CPIH) (right-hand side) UK, November 2010 to November 2019, %

Source: Office for National Statistics – Producer Price Index and Consumer Prices Index including owner occupiers' housing costs

Notes:

- These data are also available within the Dashboard: Understanding the UK economy.

Download this image Figure 1: The 12-month growth rates of input PPI rose and output PPI fell in the year to November 2019

.png (37.0 kB) .xlsx (21.5 kB){kind=link}

4. Import intensity

Import intensity refers to the percentage of final household expenditure on a good or service that is either directly imported or contains imported components. Both estimates of import intensity are reflected in the final price consumers face, and include taxes, subsidies and margins.

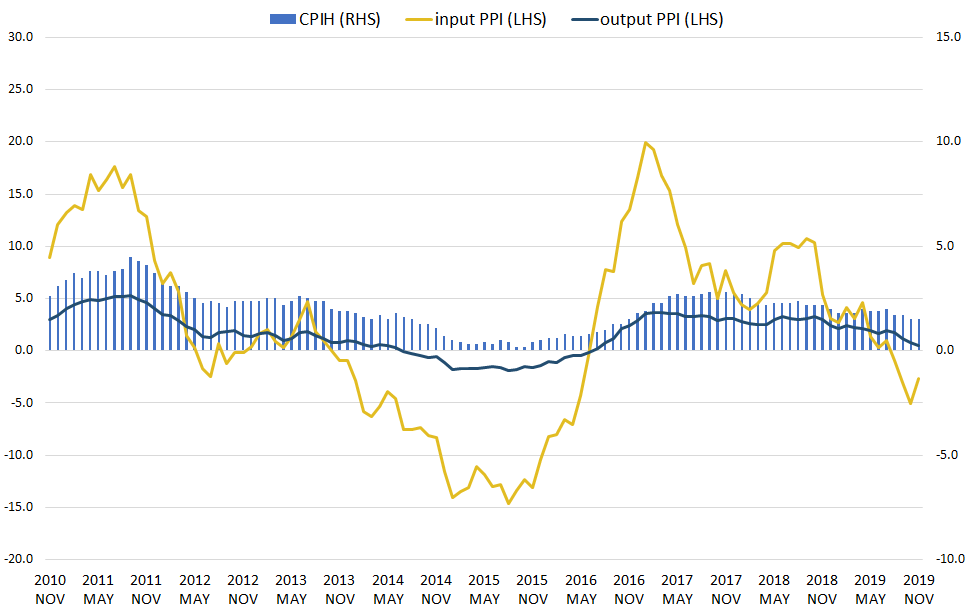

Figure 2: Falls in the 12-month growth rate of CPIH were driven by higher import intensity groups and energy

Contributions to the 12-month growth rate of Consumer Prices Index including owner occupiers' housing costs (CPIH) by import intensity, UK, January 2015 to November 2019

Source: Office for National Statistics – Consumer Prices Index including owner occupiers' housing costs and Bank of England - Monthly average Effective exchange rate index, Sterling (Jan 2005 = 100)

Notes:

- Contributions may not sum due to rounding.

Download this image Figure 2: Falls in the 12-month growth rate of CPIH were driven by higher import intensity groups and energy

.png (39.1 kB) .xlsx (20.7 kB){kind=link}

Figure 2 shows contributions to the 12-month growth rate of Consumer Prices Index including owner occupiers' housing costs (CPIH) (left-hand side) by import intensity groups as well as the 12-month inverted sterling effective exchange rate (right-hand side).

This figure is particularly insightful because of recent movements in the sterling effective exchange rate. A weaker pound makes imports relatively more expensive for UK consumers, but this depends upon the import intensity of consumer demand and the extent of the exchange rate passthrough. Analysis on the passthrough can be found in the July 2019 Economic review.

Over the last two years, the 12-month growth rate of CPIH has been gradually falling, from 2.8% in November 2017, to 1.5% in November 2019. This fall has been driven largely by high import intensity categories and energy, which combined have seen a fall in their contribution to CPIH from 1.29 percentage points in November 2017 to 0.20 percentage points in October 2019.

Lower import intensity categories, on the other hand, have made relatively stable contributions over the same period, ranging from 1.32 percentage points in January 2018 to a low of 1.01 percentage points in August 2019.

This could be explained, to some extent, by an approximate 26% drop in value of the inverted effective sterling exchange rate, between October 2016 and October 2017, which would have more impact on higher import intensity goods and services than those with lower import intensity. An inverted effective exchange rate index means that an increase on the chart corresponds to a fall in the value of sterling, which would be expected to increase the growth rate of inflation, all else being equal, while the opposite is true for a fall in the inverted effective exchange rate.

Contributions from energy over the last year reflect the introduction of a price cap by Ofgem on energy prices consumers pay, and changes in world prices for crude oil as mentioned in previous Prices economic commentaries for February and November.

Figure 3 shows a more detailed breakdown of how the 25 to 40% import intensity group has contributed to the 12-month growth rate of CPIH. Components of the 25 to 40% import intensity category have been grouped according to their classification of individual consumption by purpose (COICOP); recreation and culture, for example, includes those elements of recreation and culture that have an import intensity of 25 to 40%, and excludes those elements of recreation and culture that fall into a different import intensity category.

Figure 3: Food and non-alcoholic beverages have made relatively large contributions over recent months

Contributions to the 25 to 40% import intensity group, UK, January 2015 to November 2019

Source: Office for National Statistics – Consumer Prices Index including owner occupiers' housing costs

Notes:

- Contributions may not sum due to rounding.

- Other includes appliances and products for personal care; jewellery, clocks and watches; and other personal effects.

- Recreation and culture include equipment for the reception and reproduction of sound and pictures; photographic, cinematographic and optical equipment; equipment for sport and open-air recreation; gardens, plants and flowers; pets, related products and services; and cultural services.

- Furniture, household equipment and maintenance include furniture and furnishings; major appliances and small electric goods; tools and equipment for house and garden; and non-durable household goods.

- Food and non-alcoholic beverages include bread and cereals; fish; milk, cheese and eggs; oils and fats; sugar, jam, syrups, chocolate and confectionery; food products not elsewhere covered; coffee, tea and cocoa; and mineral waters, soft drinks and juices.

- Clothing includes garments; and other clothing and clothing accessories.

Download this chart Figure 3: Food and non-alcoholic beverages have made relatively large contributions over recent months

Image .csv .xlsMovements in the contribution of the 25 to 40% category have been largely driven by food and non-alcoholic beverages, furniture, household equipment and maintenance, and recreation and culture, which have all seen considerable variation over the period.

Figure 4 shows a more detailed breakdown of how the 40% plus import intensity group has contributed to the 12-month growth rate of CPIH. Components of the 40% plus import intensity category have been grouped according to their COICOP; transport, for example, includes those elements of transport that have an import intensity of 40% plus, and excludes those elements of transport that fall into a different import intensity category.

Figure 4: Transport has been the biggest driver of change in contributions for the 40% plus category

Contributions to the 40% plus import intensity group, UK, January 2015 to November 2019

Source: Office for National Statistics – Consumer Prices Index including owner occupiers' housing costs

Notes:

- Contributions may not sum due to rounding.

- Food includes meat; fruit, and vegetables including potatoes.

- Health includes pharmaceutical products and other medical products and therapeutic equipment.

- Transport includes motorcycles and bicycles; new cars; second-hand cars; and spare parts and accessories.

- Clothing and footwear include footwear including repairs.

Download this chart Figure 4: Transport has been the biggest driver of change in contributions for the 40% plus category

Image .csv .xlsClothing and footwear, and transport have been among the biggest drivers of changes to the contribution of the 40% plus category over the period. Footwear has contributed to negative contributions from the clothing and footwear component since July 2018.

Nôl i'r tabl cynnwys5. Consumer Prices Index including owner occupiers’ housing costs (CPIH) subgroups

Each quarter, the Office for National Statistics (ONS) publishes a set of CPIH-consistent inflation rates for different household subgroups. These are experimental statistics intended to complement the headline CPIH series, which carries the National Statistic badge. The subgroups covered in the release are retired and non-retired households, households with and without children, households grouped by tenure type, and households separated into income and expenditure deciles. Due to the unusual composition of the first and tenth deciles, the second decile is taken as representative of low income or expenditure households; while the ninth is taken to represent high income or expenditure households.

A summary of recent 12-month inflation rates for the various subgroups along with the long-term averages is presented in Table 1.

| Average 12-month growth rate (%) | ||

|---|---|---|

| 2006 to 2018 | 2019 year to date | |

| CPIH | 2.2 | 1.8 |

| Group | ||

| Expenditure deciles | ||

| Decile 2 | 2.4 | 1.8 |

| Decile 9 | 2.2 | 1.8 |

| Income deciles | ||

| Decile 2 | 2.3 | 1.8 |

| Decile 9 | 2.3 | 1.8 |

| Households by retirement status | ||

| Retired | 2.3 | 1.9 |

| Non-retired | 2.2 | 1.8 |

| Households with and without children | ||

| Households with children | 2.2 | 1.8 |

| Households without children | 2.3 | 1.9 |

| Households by tenure type | ||

| Subsidised rent | 2.4 | 1.8 |

| Renter households | 2.5 | 1.7 |

| Owner occupied | 2.2 | 1.9 |

Download this table Table 1: Average 12-month growth rates for selected groups, UK; average 2006 to 2018; average 2019 year to date

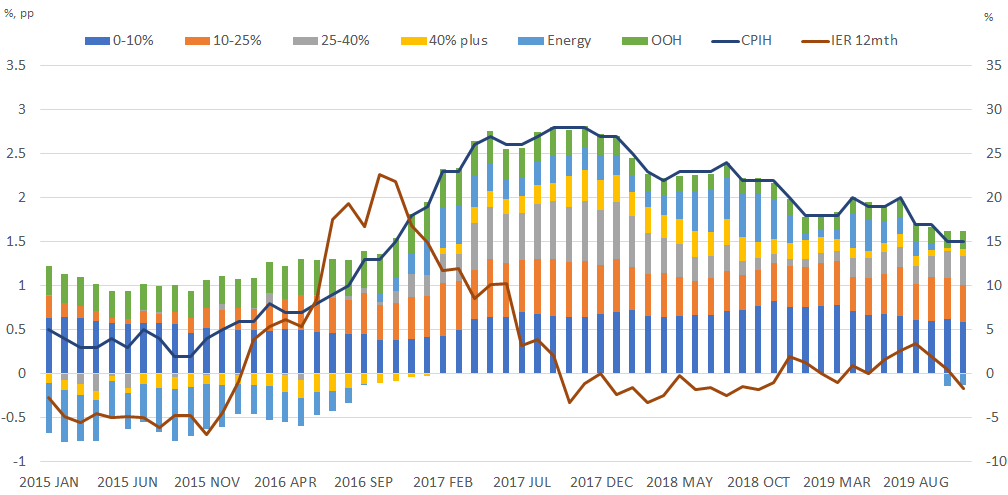

.xls .csvThe 2019 average values for all household subgroups are slightly below their equivalent long-term averages. Since 2006 all-households CPIH has been as high as 4.8% and as low as 0.2%. One trend that can be observed among the subgroups is an increasing divergence of inflation rates for retired and non-retired households. This can be seen beginning at the start of 2019 and becoming more pronounced from April onwards.

Figure 5: Inflation rates for retired and non-retired households have diverged in 2019

12-month growth rates for Consumer Prices Index including owner occupiers' housing costs (CPIH) inflation, retired and non-retired households, %, UK, January 2017 to September 2019

Source: Office for National Statistics, Consumer Prices Index including owner occupiers' housing costs (CPIH)-consistent inflation rate estimates for UK household groups, April to September 2019

Download this chart Figure 5: Inflation rates for retired and non-retired households have diverged in 2019

Image .csv .xlsDifferences in the inflation rates experienced by household groups can be explained by analysing the differences in contributions from the underlying components. There are three components that largely account for this divergence: slower growth due to transport, and recreation and culture for non-retired households relative to retired households, and a restoration in the difference in contributions from utilities starting in April 2019.

Figure 6: The divergence in growth rates for retired and non-retired households can be attributed to the transport, utilities and recreation categories

Contributions to difference in growth rates (percentage points), UK, January 2017 to September 2019

Source: Office for National Statistics, Consumer Prices Index including owner occupiers' housing costs (CPIH)-consistent inflation rate estimates for UK household groups: April to September 2019

Notes:

- Stacked bars reflect the percentage point contributions of each of the 87 class-level items to the difference in 12-month growth rates for retired and non-retired households. The contribution of each of the 87 class-level items is estimated separately, before being aggregated to seven distinct categories.

- Food and drink, alcohol and tobacco, transport and recreation and culture are categories reflecting the corresponding divisions in the COICOP classification system. Housing represents the cost of shelter, that is, owner-occupied housing costs or actual rents, plus Council Tax. Utilities and domestic fuel represents electricity, gas, water and sewerage supplies and solid and liquid fuels supplied to the home. The other category comprises all other classes included in CPIH.

- Differences in contributions may not sum due to rounding.

Download this chart Figure 6: The divergence in growth rates for retired and non-retired households can be attributed to the transport, utilities and recreation categories

Image .csv .xlsEach of these categories can be broken down further. Within transport, we can see that the trend in 2019 is driven mainly by the fuels and lubricants class. Non-retired households spend proportionally more than retired households in both categories, so movements in their prices will have a stronger effect on non-retired households’ inflation rates.

Figure 7: Fuel costs have narrowed the difference in growth rates because of transport since April 2019

Contributions to difference in growth rates (percentage points), UK, January 2017 to September 2019

Source: Office for National Statistics, Consumer Prices Index including owner occupiers' housing costs (CPIH)-consistent inflation rate estimates for UK household groups: April to September 2019

Notes:

- Stacked bars reflect the percentage point contributions of each of the 11 class-level items within transport to the difference in overall 12-month growth rates for retired and non-retired households.

- Contributions may not sum due to rounding.

Download this chart Figure 7: Fuel costs have narrowed the difference in growth rates because of transport since April 2019

Image .csv .xlsFuel prices fell between February and July of 2017, and again between September 2018 and February 2019. The contributions to difference in growth rate because of fuel can be seen to shrink during these periods. Fuel prices have been falling slowly since May 2019, so the contributions to difference from fuel have remained small compared with their recent historical average. Road passenger prices have had a steady upward trajectory since 2017, but this was slightly flatter in 2018 leading to a reduction in contributions to difference from this category.

Within recreation and culture, the longer-term trend is dominated by the package holidays category. This category has seen price increases of nearly 12% since January 2017 alongside a simultaneous pronounced increase in the proportion of expenditure by retired households, both in absolute terms and relative to non-retired households. More recently, falls in the prices of games, toys and hobbies since April 2019 have benefitted non-retired households more than retired households.

Figure 8: Games, toys and hobbies has added to the contributions to difference since April 2019

Contributions to difference in growth rates (percentage points), UK, January 2017 to September 2019

Source: Office for National Statistics, Consumer Prices Index including owner occupiers' housing costs (CPIH)-consistent inflation rate estimates for UK household groups: April to September 2019

Notes:

- Stacked bars reflect the percentage point contributions of each of the 87 class-level items to the difference in 12-month growth rates. The contribution of each of the 87 class-level items is estimated separately, before being aggregated to seven distinct categories.

- A reduction in the contribution of series to the annual rate of change need not imply falling prices but could also reflect a lower rate of increase than the previous year.

- Contributions may not sum due to rounding.

Download this chart Figure 8: Games, toys and hobbies has added to the contributions to difference since April 2019

Image .csv .xlsThe contributions from utilities have been influenced by two main factors since the start of 2019. The first is the relative change in expenditure shares on sewerage. Retired households have increased their expenditure share while non-retired households have decreased theirs. As a result, a relatively modest increase in sewerage costs in 2019 has led to a sizeable difference in contributions to the growth rate.

The other factor has been the price cap on gas and electricity prices applied by Ofgem. Retired households spend proportionally more on gas and electricity than non-retired households, so any price movement will have a greater effect on their inflation rate. The application of the price cap resulted in a fall in gas and electricity prices in the first three months of 2019, before rising again in April. While both categories of household benefitted from the price cap overall, retired households benefitted more from the gas cap while non-retired households benefitted from the electricity cap. After April the contributions pattern reverted to a more conventional picture of gas and electricity prices having a greater impact on retired households. This can clearly be seen in the Utilities contributions chart.

Figure 9: The price cap on gas and electricity prices had a greater benefit for retired households

Contributions to difference in growth rates (percentage points), UK, January 2017 to September 2019

Source: Office for National Statistics, Consumer Prices Index including owner occupiers' housing costs (CPIH)-consistent inflation rate estimates for UK household groups: April to September 2019

Notes:

- Stacked bars reflect the percentage point contributions of each of the 87 class-level items to the 12-month growth rate, or the difference in 12-month growth rates. The contribution of each of the 87 class-level items is estimated separately, before being aggregated to seven distinct categories.

- A reduction in the contribution of series to the annual rate of change may imply falling prices but could also reflect a lower rate of increase than the previous year.

- Contributions may not sum due to rounding.

Download this chart Figure 9: The price cap on gas and electricity prices had a greater benefit for retired households

Image .csv .xls6. Wholesale, producer and consumer electricity and gas prices

Figure 10 shows movements in Ofgem's wholesale prices for electricity, and the input Producer Price Index series representing purchases of materials and fuels for electricity production and distribution (excluding Climate Change Levy (CCL)) and electricity prices paid by manufacturers (including Climate Change Levy). It also shows the electricity component of the Consumer Prices Index including owner occupiers' housing costs (CPIH) between January 2012 and November 2019. Figure 11 shows the equivalent series for gas.

Consumer prices for electricity have moved broadly in line with prices paid by manufacturers over the period. Likewise, electricity suppliers' input costs have moved more in line with wholesale electricity prices than with consumer prices, although in recent months movements in suppliers' costs have been more muted than movements in wholesale prices.

At the beginning of the period, there were similar movements in all four series. This changed in early 2014 when wholesale and supplier input prices fell sharply, while consumer and manufacturers' prices remained relatively flat. This continued for around two years, after which wholesale and supplier input prices began to rise, with manufacturers' and consumer prices doing the same around a year later.

In January 2019, Ofgem introduced an energy price cap for the consumer market, putting an upper limit on the prices suppliers can charge consumers on default tariffs. Since April 2017 there has also been a price cap for consumers on prepayment meters. In response to the cap, consumer prices fell by around 5% between December 2018 and January 2019, then rose by around 11% in April 2019.

The Ofgem cap changed again in October 2019, resulting in around a 2% fall in the energy component of Consumer Prices Index including owner occupiers' housing costs (CPIH) from the month before. Manufacturers' electricity prices have continued to see similar movements since the cap was introduced; they remained relatively flat when the cap rose in April 2019, and increased slightly on the month to November when the cap was reduced in October 2019.

From December 2018 to September 2019, wholesale electricity prices fell by around 42%. Meanwhile, electricity producers' costs have remained relatively unchanged, with prices increasing by around 8% between December 2018 and April 2019, then falling back by around 5% by November 2019.

In addition to wholesale prices, consumer prices also account for transmission, distribution and regulatory costs, and profits for energy suppliers and others in the supply chain.

Figure 10: Consumer prices for electricity fell slightly in October, reflecting the change in Ofgem’s energy price cap

Price indices for wholesale electricity and the electricity components of input Producer Price Index (PPI), for suppliers and manufacturers, and Consumer Prices Index including owner occupiers' housing costs (CPIH), UK, January 2012 to November 2019

Source: Office for National Statistics – Producer Price Index and Consumer Price Index including owner occupiers’ housing costs, Office for Gas and Electricity Markets (OFGEM)

Notes:

- The latest data available for Ofgem wholesale electricity are September 2019.

Download this chart Figure 10: Consumer prices for electricity fell slightly in October, reflecting the change in Ofgem’s energy price cap

Image .csv .xlsFigure 11 shows movements in Ofgem’s wholesale prices for gas, and the input Producer Price Index series representing purchases of materials and fuels for gas production and distributions (excluding CCL) and gas prices paid by manufacturers (including CCL). It also shows the gas component of the CPIH between January 2012 and November 2019.

Figure 11: Recent movements in consumer prices for gas coincide with those of electricity, but fell by more on the month to October 2019

Price indices for wholesale gas and the gas components of input Producer Price Index (PPI), for suppliers and manufacturers, and Consumer Prices Index including owner occupiers' housing costs (CPIH), UK, January 2012 to November 2019

Source: Office for National Statistics – Producer Price Index and Consumer Price Index including owner occupiers’ housing costs, Office for Gas and Electricity Markets (OFGEM)

Notes:

- The latest data available for Ofgem wholesale gas are September 2019.

Download this chart Figure 11: Recent movements in consumer prices for gas coincide with those of electricity, but fell by more on the month to October 2019

Image .csv .xlsGas prices have shown similar movements to electricity prices over the period, with recent consumer prices moving in line with changes in the Ofgem energy price cap and gas suppliers' input costs showing similar movements to wholesale prices.

One notable difference is in the movement of manufacturers' gas prices, which fell by around 22% between January and September 2019, while consumer prices for gas rose by around 10% in April 2019. The fall in manufacturers' gas prices also contrasts with movements in manufacturers' electricity prices, which remained relatively unchanged over the period.

This may reflect differences in how gas and electricity are produced and stored. While electricity prices typically follow gas prices, with gas used in the production of electricity, electricity is more difficult to store than gas, and this may impact on their relative prices. Low demand for energy and an excess of supply of gas over the mild winter in early 2019 are cited as reasons for falling wholesale gas prices over the year.

Nôl i'r tabl cynnwys7. Housing and rental prices

Rental prices have increased in each country of the UK since January 2015. Average UK rental prices have increased by 8.1% from January 2015 to October 2019. At a country level the highest rental increase was in England (8.6%) and the lowest rental increase was in Scotland, where prices only increased by 2.5% over the period. For comparability with the latest house price data, this commentary will focus on the October 2019 rental data. The November 2019 rental data are available in the Private housing rental prices release.

Figure 12: Rental prices have steadily increased across the UK since January 2015

Index of Private Rental Prices indices, UK countries, January 2015 to October 2019, January 2015=100

Source: Office for National Statistics – Index of Private Housing Rental Prices

Notes:

- Data presented in this dataset are classified as Experimental Statistics and subject to revisions if improvements in the methodology are identified. Results should be interpreted with this in mind.

Download this chart Figure 12: Rental prices have steadily increased across the UK since January 2015

Image .csv .xlsThis slow and steady increase in rental prices since 2015 may reflect the conditions of increasing demand and falling supply, as reported by the Association of Residential Lettings Agents (ARLA) in their private rented sector reports. In their January 2016 report (PDF, 960.37KB) the average number of prospective tenants registered at letting agents increased, while the average number of properties managed per branch decreased. In February 2017 (PDF, 881.82KB) pressures continued with supply falling slightly and demand remaining the same. March 2018 (PDF, 1MB) saw a fall in supply year on year and again a rise in demand.

Average house prices have increased considerably more over the period than average rental prices and have also shown more variation across the countries of the UK. The UK average house prices have increased by 22.2% between January 2015 and October 2019. The UK country that experienced the biggest increase in average house prices was Northern Ireland where prices increased by 26.2% over the period. Scotland was the UK country where prices increased the least, with a 13.9% rise in average house prices since January 2015.

Figure 13: Average price increases have varied across the UK

House Price Index, UK countries, January 2015 to October 2019, January 2015=100

Source: HM Land Registry and Office for National Statistics – UK House Price Index

Notes:

- Not seasonally adjusted.

- The full House Price Index (HPI) release is available to download from HM Land Registry at GOV.UK.

Download this chart Figure 13: Average price increases have varied across the UK

Image .csv .xlsHousing market conditions are commented on by the Bank of England every quarter in the Agents Summary of Business Conditions report. According to this report, in the first half of 2015 the housing market grew strongly despite the low levels of supply. The 2016 Q3 report drew on the significant fall in London transactions, but housing market activity remained strong in the rest of the UK. Q2 2017 saw weaker demand relative to supply pushing the market closer to a balance. According to the report, equal forces of demand and supply were reached in Q2 2018; Help to Buy schemes may have supported a new-build market that was stronger than the secondary market over this period. In the latest report, Q3 2019, the housing market was described as soft, reflecting changes in demand and supply.

| Growth in House Price Index (%) from January 2015 to October 2019 | Growth in private rental prices (%) from January 2015 to October 2019 | Difference between house price growth and rental growth (pp) | Average house price (£) October 2019 | |

|---|---|---|---|---|

| UK | 22.2 | 8.1 | 14 | 233,000 |

| Northern Ireland | 26.2 | 8.8 | 17.4 | 140,000 |

| Wales | 22.1 | 3.9 | 18.2 | 166,000 |

| England | 22.7 | 8.6 | 14.2 | 249,000 |

| Scotland | 13.9 | 2.5 | 11.3 | 154,000 |

| East | 28.8 | 10.7 | 18.1 | 294,000 |

| North West | 22.1 | 5.5 | 16.6 | 166,000 |

| West Midlands | 25 | 8.6 | 16.4 | 198,000 |

| Yorkshire and The Humber | 22.6 | 7.4 | 15.2 | 167,000 |

| East Midlands | 26.3 | 12.1 | 14.3 | 194,000 |

| South West | 21.4 | 9.9 | 11.4 | 258,000 |

| South East | 22.1 | 11.1 | 11 | 323,000 |

| London | 17.2 | 7.3 | 9.9 | 472,000 |

| North East | 10.4 | 2.5 | 7.9 | 129,000 |

Download this table Table 2: Growth in rental prices and house prices from January 2015 to October 2019, the difference between the two, and average house prices

.xls .csvGenerally speaking, the countries and regions with the highest average house prices have seen the lowest difference between the growth of house prices and rental prices over the period. Exceptions to this are Scotland, the East of England and, most notably, the North East of England, which has the lowest average house prices and saw the lowest increase in both house prices and rental prices over the period. The North East also had the lowest difference in growth rates for house prices and rental prices.

The largest increase in house prices over the period was in the East of England, at 28.8%. The largest increase in rental prices over the period was in the East Midlands at 12.1%. Wales saw the largest difference between house price growth and rental growth – house prices grew at 22.1% over the period compared with rental price growth of only 3.9%.

Nôl i'r tabl cynnwys