Cynnwys

- Main points

- Things you need to know about this release

- Outline of improvements to the Blue Book 2017 consistent GFCF and business investment datasets

- GFCF and business investment main figures

- Which sectors and assets are contributing to growth in GFCF in Quarter 2 (Apr to June) 2017?

- How has GFCF performed over a longer period?

- What other information can tell us more about investment?

- How has business investment performed over a longer period?

- Asset contributions to business investment in Quarter 2 (Apr to June) 2017?

- Business investment in the wider economy

- What’s new in this release

- Links to related statistics

- Quality and methodology

1. Main points

Gross fixed capital formation (GFCF), in volume terms, was estimated to have increased by 0.6% to £81.2 billion in Quarter 2 (Apr to Jun) 2017 from £80.7 billion in Quarter 1 (Jan to Mar) 2017.

Business investment was estimated to have increased by 0.5% to £45.7 billion in Quarter 2 2017 from £45.4 billion in Quarter 1 2017.

Between Quarter 2 2016 and Quarter 2 2017, GFCF was estimated to have increased by 2.4%, from £79.3 billion and business investment was estimated to have increased by 2.5%, from £44.5 billion.

The sectors contributing most to GFCF growth between Quarter 1 2017 and Quarter 2 2017 were general government and business investment.

The asset that contributed most to GFCF growth for the same period was ICT equipment and other machinery and equipment. This was slightly offset by dwellings and other buildings and structures and transfer costs.

Between 2015 and 2016 GFCF was estimated to have increased by 1.3%.

Business investment fell by 0.4% between 2015 and 2016, an upwards revision of 1.1 percentage points compared with the previously published estimate.

Estimates in this bulletin are consistent with the UK National Accounts, Blue Book 2017 edition to be published on 31 October 2017. All data have been revised from their start point and the reference year for the chained volume estimates has now moved on from 2013 to 2015.

2. Things you need to know about this release

The estimates in this release are short-term indicators of investment in non-financial assets in the UK, such as dwellings (residential buildings), transport equipment (planes, trains and automobiles), machinery (electrical equipment), buildings (non-residential buildings and roads), intellectual property products (assets without physical properties – formerly known as intangibles) and transfer costs (costs associated with buying or selling an asset for example legal fees). This release covers not only business investment, but asset and sector breakdowns of total gross fixed capital formation (GFCF), of which business investment is one component.

Business investment is net investment by private and public corporations. These include investments in transport, information and communication technology (ICT) equipment, other machinery and equipment, cultivated assets (such as livestock and vineyards), intellectual property products (IPP, which includes investment in software, research and development, artistic originals and mineral exploration), and other buildings and structures.

Business investment does not include investment by central or local government, investment in dwellings, or the costs associated with the transfer of non-produced assets (such as land). Business investment is not an internationally recognised concept and it should not be used to make international comparisons, however, GFCF is an internationally recognised standard and is therefore internationally comparable. Please see A short guide to GFCF and business investment for more detailed information, including asset and sector hierarchies.

All investment data referred to in this bulletin are estimates of seasonally adjusted chained volume measures. To see a time series of the data please use our time series datasets.

This is a UK National Accounts, Blue Book 2017-consistent release. Each year in the Blue Book-consistent publications of business investment we incorporate methodological and data changes that will impact on the business investment and GFCF datasets. For more information on the updates included as part of this year’s Blue Book update, please see section 3.

Nôl i'r tabl cynnwys3. Outline of improvements to the Blue Book 2017 consistent GFCF and business investment datasets

This business investment release is the first publication of gross fixed capital formation (GFCF) data consistent with the Blue Book 2017 dataset. The full Blue Book 2017 dataset is to be released on 31 October 2017. We have introduced a number of changes to GFCF. Some of these have previously been discussed in the Annual improvements to gross fixed capital formation source data for Blue Book 2017, published 16 February 2017. There are also regular annual updates to seasonal adjustment models and annual business survey data, as well as the full integration of the new GFCF estimation system.

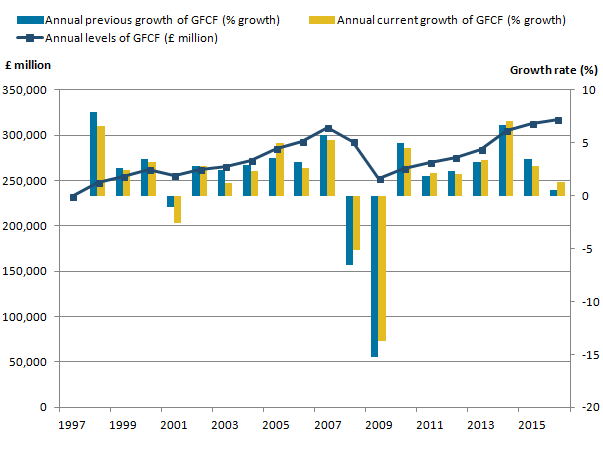

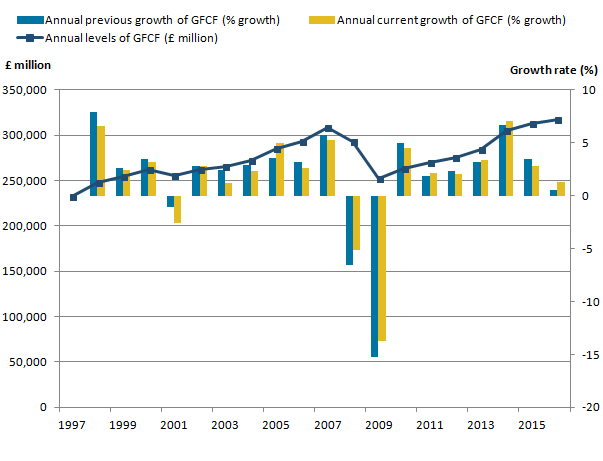

Overall, the changes introduced have reduced the level of GFCF between 1997 and 2016 by an average of £3.5 billion annually. Figure 1 shows the annual levels and growth of GFCF compared with those previously published.

Figure 1: Annual GFCF levels and growth, chained volume measure, seasonally adjusted

Reference year: 2015 Coverage: UK

Source: Office for National Statistics

Notes:

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

The data in this chart covers 1997 to 2016.

Download this image Figure 1: Annual GFCF levels and growth, chained volume measure, seasonally adjusted

.png (18.0 kB) .xls (21.5 kB){kind=link}

On average, annual business investment is £0.3 billion higher in 2016 than in 1997. The changes are not as uniform as those for GFCF. A detailed breakdown of the revisions to GFCF and business investment can be seen in the tables published alongside this bulletin.

Regular blue book changes

At each Blue Book publication, we take the opportunity to review our seasonal adjustment models to make sure that they are appropriate. As a result, the seasonally adjusted series will all revise to some extent. When these new models are applied to series where we have introduced new methodology, the change can be large. This is outlined in the sections that follow, particularly in relation to the transport equipment and other buildings and structures and transfer costs series.

We have also introduced updated data from the annual business survey (ABS), which will impact on the levels of GFCF from 2014 onwards.

Integration of the new GFCF system

In February 2017, we produced our first estimates of GFCF using the new GFCF estimation system. Information on the new methodology and impacts of the new system can be found here. Gross fixed capital formation (GFCF) new system deployment and data impact assessment and Changes to the Gross Fixed Capital Formation methodology and processing.

In order to be consistent with National Accounts revisions policy, changes from the new system impacting on 2015 and earlier were previously constrained out.

As this Blue Book 2017 consistent publication opens up those earlier years for revision then we are now able to integrate estimates for the new estimation system for the period prior to Quarter 1 (Jan to Mar) 2016.

As a result, there are changes from:

- the introduction of more detailed deflation for all assets

- improved seasonal adjustment methodology

- improved benchmarking to annual survey data

- improvements made to the sector breakdown

Here we will link the changes to the revised series by asset.

Dwellings

The largest change to dwellings in Blue Book 2017 is due to the reclassification of Housing Associations from private non-financial corporations to public corporations from Quarter 3 (July to Sep) 2008. This can be seen in the data as an upward revision to public corporations dwellings and a downward revision to private dwellings investment since Quarter 3 2008. The average current price annual increase to public corporations dwellings is £3.4 billion. This change does not affect the total level of dwellings or GFCF.

We have also made improvements to the deflation of dwellings data, using more appropriate deflators to differentiate between public and private sector investment, as well as different deflators for new dwellings and repair and maintenance of existing dwellings.

Transport

There are two main changes to the transport series in Blue Book 2017. These are the introduction of improved source data for investment in aircraft from 2013 and the introduction of more up to date annual business survey data for 2014 and 2015. Both changes contribute to the large increase in the level of investment in transport equipment from 2013 and the change to the quarterly path from 2015. In particular, the aircraft data has changed the underlying profile of the transport series by introducing new peaks in the series in early 2015 and Quarter 3 2016

Intellectual property products

Intellectual property products (IPP) consists of four assets – software and databases, artistic originals, research and development, and mineral exploration. Two changes have been introduced for this release. The first relates to software and databases impacting 1997 to 2015. In the Quarter (Apr to June) 2016 business investment release, an error was identified in the methodology used to calculate purchased software within GFCF which led to some double counting. Correcting this has reduced the level of software and databases in all years, on average by £3.8 billion annually.

The second change relates to artistic originals. We have taken on revised estimates for data from 2009, causing an increase in the level from this point in the series.

ICT equipment and other machinery and equipment

Following the introduction of the new Quarterly Acquisitions and Disposals of Capital Assets Survey (QCAS) in 2015, we received feedback from respondents indicating that they had previously been misreporting their asset breakdown and were correcting this on the new questionnaire. We found that some respondents had been reporting other construction work as other capital equipment. In order to remain consistent, we applied adjustments to the current price data from 2015 Quarter 1 onwards to reduce the level of new construction work and increase the level of other capital equipment. In this Blue Book 2017 dataset, we have taken the opportunity to correct the back series in line with the new survey information and remove the adjustments from 2015 onwards. As a result, the current price level of information and communication technology (ICT) equipment and other machinery and equipment has been reduced.

Other buildings and structures and costs of ownership transfer

As discussed as part of the ICT equipment and other machinery and equipment revisions, feedback from respondents following the introduction of the QCAS survey identified misreporting of asset breakdowns. As a result, the current price level of other buildings and structures has increased.

As well as the more detailed deflation introduced by the new GFCF system, specific improvements have also been made to the deflators used to deflate buildings data. These improvements are discussed in more detail in the Impact of Improvements to Construction Statistics article.

These changes have altered the underlying trend of the other buildings and structures series, resulting in an altered profile to for the seasonally adjusted series.

Three changes have been made to the costs of ownership series (sometimes referred to as transfer costs) in this Blue Book consistent dataset. We published an article in February 2017, Review of costs of ownership transfer and treatment in the UK National Accounts, discussing an issue with the calculation of transfer costs that was identified as part of the National Statistics Quality Review of National Accounts and Balance of Payments. Following a methodological review, it was determined that transfer costs were by definition positive, which was counter to some of the sector estimates we produced. A new sector breakdown was introduced using the sector breakdown of dwellings and other buildings and structure data as a proxy. This has not changed the total level of transfer costs, but has impacted on the sector breakdown of other buildings and structures and transfer costs. It is this impact which explains why the business investment revisions are less uniform than the GFCF series, as transfer costs are not included in the calculation of business investment and so do not offset the changes to other buildings and structures.

The two remaining changes have changed the total level of transfer costs. Firstly, we use the House Price Index (HPI) as part of the calculation of transfer costs. The methodology in the production of the HPI has been improved, which has caused changes back to 1997. The overall impact has been to reduce the level of transfer costs from 1997 to 2017, though growth has remained broadly the same. More information on the change to the HPI can be found in the article Explaining the impact of the new UK House Price Index: 2016.

Finally, in line with international best practice, we have for the first time estimated the transfer costs associated with the sale of footballers. It should be noted that this does not refer to the transfer fee that a football club would pay, but rather costs associated with the sale such as agents’ fees. This change has increased the level of transfer costs from 1997 to 2017, but is much smaller than the impact of the HPI change.

Nôl i'r tabl cynnwys4. GFCF and business investment main figures

Table 1: Gross fixed capital formation and business investment headline figures by sector and by asset, UK, Quarter 2 (Apr to June) 2017, chained volume measure, seasonally adjusted

| % change | % change | £ million | ||

| Most recent quarter on previous quarter | Most recent quarter on same quarter a year earlier | Most recent level | ||

| Gross fixed capital formation | 0.6 | 2.4 | 81,183 | |

| GFCF by sector | Business investment | 0.5 | 2.5 | 45,661 |

| General government | 6.1 | 1.6 | 13,178 | |

| Public corporations dwellings | -0.1 | -5.8 | 1,929 | |

| Public corporations cost of ownership transfer on non-produced assets | 50.6 | 12.1 | 232 | |

| Private sector dwellings | -1.8 | 2.3 | 15,996 | |

| Private sector cost of ownership transfer on non-produced assets | -6.6 | 6.8 | 4,187 | |

| GFCF by asset | Transport equipment | -1.5 | -1.1 | 6,398 |

| ICT equipment and other machinery and equipment | 8.1 | 0.1 | 13,890 | |

| Dwellings | -1.6 | 1.4 | 17,941 | |

| Other buildings and structures and transfer costs | -0.6 | 6.5 | 27,850 | |

| Intellectual property products | 0.0 | -0.1 | 15,104 | |

| Source: Office for National Statistics | ||||

Download this table Table 1: Gross fixed capital formation and business investment headline figures by sector and by asset, UK, Quarter 2 (Apr to June) 2017, chained volume measure, seasonally adjusted

.xls (29.2 kB)5. Which sectors and assets are contributing to growth in GFCF in Quarter 2 (Apr to June) 2017?

Between Quarter 1 (Jan to Mar) 2017 and Quarter 2 (Apr to June) 2017, gross fixed capital formation (GFCF) increased by 0.6%. On a sector basis, general government contributed 0.9 percentage points to overall GFCF growth, while business investment contributed 0.3 percentage points. (Figure 2). The largest negative contributors to GFCF for the same period growth were private sector transfer costs and private sector dwellings, which each contributed negative 0.4 percentage points.

Figure 2: Contributions to growth in gross fixed capital formation by sector for Quarter 2 (Apr to June) 2017, chained volume measure, seasonally adjusted

Reference year: 2015 Coverage: UK

Source: Office for National Statistics

Notes:

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

The data in this chart covers Quarter 2 (Apr to June) 2017.

Download this chart Figure 2: Contributions to growth in gross fixed capital formation by sector for Quarter 2 (Apr to June) 2017, chained volume measure, seasonally adjusted

Image .csv .xlsBetween Quarter 2 2016 and Quarter 2 2017, GFCF increased by 2.4%. Business investment was the biggest factor in this increase, contributing 1.4 percentage points to the increase. Private sector dwellings, private sector transfer costs and general government also increased, contributing 0.5, 0.3 and 0.3 percentage points respectively to the increase in GFCF. No sectors saw a significant fall when compared with the same quarter a year earlier.

On an asset basis, information and communication technology (ICT) equipment and other machinery and equipment contributed 1.3 percentage points to the 0.6% increase in GFCF in Quarter 2 2017 (Figure 3).

This was partially offset by falls in dwellings, other buildings and structures and transfer costs and transport equipment, which contributed negative 0.4, 0.2 and 0.1 percentage points respectively. The contribution of transport equipment is less negative than provisionally estimated, while the contribution of other buildings and structures and transfer costs has been revised down. Both of these series have been revised as part of the annual Blue Book update described in section 3 of this bulletin.

Figure 3: Contributions to growth in gross fixed capital formation by asset for Quarter 2 (Apr to June) 2017, chained volume measure, seasonally adjusted

Reference year: 2015 Coverage: UK

Source: Office for National Statistics

Notes:

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

The data in this chart covers Quarter 2 (Apr to June) 2017.

Download this chart Figure 3: Contributions to growth in gross fixed capital formation by asset for Quarter 2 (Apr to June) 2017, chained volume measure, seasonally adjusted

Image .csv .xlsThe 2.4% quarter on same quarter a year ago increase in GFCF, for Quarter 2 2017, saw a large positive contribution from other buildings and structures and transfer costs. Dwellings also contributed positively. Transport contributed a negative 0.1 percentage points for the same period, revised up from the provisionally estimated contribution of negative 1.5 percentage points, again for the reasons described in section 3 of this bulletin.

Nôl i'r tabl cynnwys6. How has GFCF performed over a longer period?

Gross fixed capital formation (GFCF) is now 7.8% above the pre-economic downturn peak of Quarter 1 (Jan to Mar) 2008 and 31.2% above the level seen at the trough of the financial crisis in Quarter 2 (Apr to June) 2009.

The upward revisions to quarter on quarter growth in 2016 in these estimates are mainly due to the introduction of revised estimates for government investment and improved source data for transport equipment, providing modest quarter on quarter growth.

Figure 4: Quarterly levels and quarter-on-quarter growth of gross fixed capital formation, chained volume measure, seasonally adjusted.

Reference year: 2015 Coverage: UK. Quarter 1 (Jan to Mar) 2008 to Quarter 2 (Apr to June 2017)

Source: Office for National Statistics

Notes:

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

The data in this chart covers Quarter 1 (Jan to Mar) 2008 to Quarter 2 (Apr to June) 2017.

Download this chart Figure 4: Quarterly levels and quarter-on-quarter growth of gross fixed capital formation, chained volume measure, seasonally adjusted.

Image .csv .xlsIn 2016, GFCF increased by 1.3% compared with 0.5% previously estimated, the weakest growth for a calendar year since 2009. Total GFCF growth has been slowing since 2014. Quarter on same quarter a year ago growth averaged 7.2% in 2014, fell to 2.8% in 2015, and then fell further to 1.4% for 2016.

Figure 5 shows the quarterly GFCF growth compared to that published in the provisional business investment release. Revisions from Quarter 1 2016 onwards are due to the combined impact of the updated methods, outlined in section 3, and also the taking on of later data which usually happens during a revised estimate. The revisions to growth in 2017 Quarter 2 are largely due to the Blue Book improvements outlines in section 3. The assets which are having the greatest impact on the revision to GFCF growth in this quarter are transport equipment and other buildings and structures and transfer costs.

Figure 5: Quarterly GFCF growth compared with previously published GFCF growth, chained volume measure, seasonally adjusted

Reference year: 2015 Coverage: UK

Source: Office for National Statistics

Notes:

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

The data in this chart covers Quarter 1 (Jan to Mar) 2015 to Quarter 2 (Apr to June) 2017.

Download this chart Figure 5: Quarterly GFCF growth compared with previously published GFCF growth, chained volume measure, seasonally adjusted

Image .csv .xls7. What other information can tell us more about investment?

Developments in the housing market can be an important indicator of investment and wider activity in the economy. Construction output fell by 1.2% in the three months to July 2017 (see Construction output in Great Britain: July 2017 for more information). This was mainly driven by a decrease in new building work, reflected in the decrease of private sector dwelling when compared with Quarter 1 (Jan to Mar) 2017.

Nôl i'r tabl cynnwys8. How has business investment performed over a longer period?

Business investment annual growth has now been falling since 2014 from 5.1% in 2014 to 3.7% in 2015 and negative 0.4% in 2016 – the weakest annual growth since 2009 (negative 16.4%) (Figure 6). Business investment annual growth for 2016 has been revised up from negative 1.5 to negative 0.4 percentage points. This upward revision was mainly due to changes to the transport equipment asset previously outlined in section 3 of this bulletin, as well as a higher level of investment in other buildings and structures.

Figure 6: Annual business investment levels and growth, chained volume measure, seasonally adjusted

Reference year: 2015 Coverage: UK

Source: Office for National Statistics

Notes:

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

The data in this chart covers 1997 to 2016.

Download this chart Figure 6: Annual business investment levels and growth, chained volume measure, seasonally adjusted

Image .csv .xlsFigure 7 shows that business investment has remained broadly unchanged since Quarter 1 (Jan to Mar) 2016. Business investment in 2016 saw two consecutive quarters of positive growth in Quarter 2 (Apr to June) 2016 (0.9%) and Quarter 3 (July to Sep) 2016 (1.4%) and two quarters of more negative growth in Quarter 1 2016 (negative 0.1%) and Quarter 4 (Oct to Dec) 2016 (negative 0.1%).

Figure 7: Quarterly levels and quarter-on-quarter growth of business investment, chained volume measure, seasonally adjusted

Reference year: 2015 Coverage: UK. Quarter 1 (Jan to Mar) 2008 to Quarter 2 (Apr to June) 2017

Source: Office for National Statistics

Notes:

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

The data in this chart covers Quarter 1 (Jan to Mar) 2008 to Quarter 2 (Apr to June) 2017.

Download this chart Figure 7: Quarterly levels and quarter-on-quarter growth of business investment, chained volume measure, seasonally adjusted

Image .csv .xlsFigure 8 shows quarterly business investment growth compared with previously published. The large revisions to growth in 2015 and 2016 are due to revisions to the underlying transport equipment asset which have changed the profile of the series and subsequently the seasonally adjusted path.

The revisions to growth in 2017 Quarter 2 are largely due to the Blue Book improvements outlined in section 3. The assets which are having the greatest impact on the revision to business investment growth in this quarter are transport equipment and ICT equipment and other machinery and equipment.

Figure 8: Quarterly business investment growth compared with previously published business investment growth, chained volume measure, seasonally adjusted

Reference year: 2015 Coverage: UK

Source: Office for National Statistics

Notes:

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

The data in this chart covers Quarter 1 (Jan to Mar) 2015 to Quarter 2 (Apr to June) 2017.

Download this chart Figure 8: Quarterly business investment growth compared with previously published business investment growth, chained volume measure, seasonally adjusted

Image .csv .xls9. Asset contributions to business investment in Quarter 2 (Apr to June) 2017?

The assets that contributed positively to the 0.5% increase in business investment between Quarter 1 (Jan to Mar) 2017 and Quarter 2 (Apr to June) 2017 were information and communication technology (ICT) equipment and other machinery and equipment and buildings. These contributed 0.4 and 0.3 percentage points to growth respectively. This was slightly offset by a fall in transport equipment of negative 0.2 percentage points.

Figure 9: Contributions to growth in business investment by asset for Quarter 2 (Apr to June) 2017

Reference year: 2015 Coverage: UK

Source: Office for National Statistics

Notes:

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

The data in this chart covers Quarter 2 (Apr to June) 2017.

Download this chart Figure 9: Contributions to growth in business investment by asset for Quarter 2 (Apr to June) 2017

Image .csv .xlsQuarter on same quarter a year ago data show that business investment has increased by 2.5% compared with Quarter 2 2016. Other buildings and structures and intellectual property products both showed positive contributions compared with Quarter 2 2016. The largest of these was other buildings and structures, which contributed 2.9 percentage points. Positive contributions in these assets were slightly offset by a negative 0.8 percentage points contribution from ICT equipment and other machinery and equipment and transport equipment.

Nôl i'r tabl cynnwys10. Business investment in the wider economy

Quarter 2 (Apr to June) 2017 marks one year since the UK voted to leave the EU. The Bank of England recently stated that investment intentions had “strengthened a little further” in its most recent Agents’ summary of business conditions. However, it is also noted in the publication that heightened uncertainty is playing a part in some firms’ unwillingness to invest. In its most recent inflation report, the Bank of England also states that sterling’s depreciation is likely to increase the cost of investment for most firms, as investment is relatively import intensive.

Another important factor to consider when looking at business investment is the availability or supply of credit. In the most recent Bank of England Credit Conditions Review, the supply of lending to firms was found to have remained broadly unchanged in Quarter 2 2017, and no change is expected leading in to Quarter 3 (July to Sept) 2017. Lenders reported increased demand for both small and medium-sized firms over Quarter 2 2017, the first increase reported for either since Quarter 2 2016. However, demand for credit from large firms “fell significantly” in the same period and this is expected to continue into Quarter 3 2017.

Nôl i'r tabl cynnwys11. What’s new in this release

Alongside this business investment release we are publishing headline business investment data prior to 1997, consistent with Blue Book 2017 estimates. This time series goes back to 1965 and contains business investment current price seasonally adjusted and chained volume measure seasonally adjusted data. These pre-1997 data are to be regarded as indicative only, due to methodological limitations. They do not, for example, reflect any impact that the introduction of annual methods improvements, might have had on the annual and quarterly path of Business Investment, such as the inclusion of research and development. These limitations have been explained in more detail within the spreadsheet, which can be found in the User requested data section of our website.

Nôl i'r tabl cynnwys13. Quality and methodology

The Business investment Quality and Methodology Information (QMI) report contains important information on:

- the strengths and limitations of the data and how it compares with related data

- uses and users

- how the output was created

- the quality of the output including the accuracy of the data

The changes signposted in this bulletin have not yet been reflected in either the Quarterly Acquisitions and Disposals of Capital Assets Survey QMI or the Business investment QMI, but changes will be incorporated into revised QMIs in the future.

In February 2017, we introduced an improved gross fixed capital formation (GFCF) estimation system, which incorporated methodological changes including improved deflation and seasonal adjustment. A data impact assessment of the new GFCF system for the periods Quarter 1 (Jan to Mar) 2016 to Quarter 3 (July to Sept) 2016 can be found in an accompanying article: Gross fixed capital formation (GFCF) new system deployment and data impact assessment. This is the first time the improved methodology can be seen throughout the time series.

Further information on the methods changes introduced in the new GFCF estimation system can be found in the article Changes to the Gross Fixed Capital Formation methodology and processing.

Adjustments

Large capital expenditure tends to be reported later in the data collection period than smaller capital expenditure. This means that larger expenditures are often included in the revised (month 3) results, but are not reported in time for the provisional (month 2) results, leading to a tendency towards upwards revisions in the later estimates for business investment and gross fixed capital formation (GFCF). Following investigation of the impact of this effect, from Quarter 3 (July to Sept) 2013, in the provisional estimate a bias adjustment is introduced to business investment and its components. We have removed the bias adjustment from our provisional results published in August.

Survey response rates

Table 2 presents the provisional (month 2) and revised (month 3) response rates for the Quarterly Acquisitions and Disposals of Capital Assets Survey (QCAS). The estimates in this release are based on the Quarter 2 (Apr to June) 2017 provisional survey results.

Table 2: UK response rates for quarterly acquisitions and disposals of capital assets survey for Quarter 4 (Oct to Dec) 2015 to Quarter 2 (Apr to June) 2017

| At month 2 (provisional) | At month 3 (revised) | |||||

| Period | Survey response rates/% | Period | Survey response rates/% | |||

| 2015 | Q4 | 68.6 | 2015 | Q4 | 89.8 | |

| 2016 | Q1 | 69.2 | 2016 | Q1 | 89.4 | |

| Q2 | 71.4 | Q2 | 89.1 | |||

| Q3 | 72.8 | Q3 | 83.5 | |||

| Q4 | 68.5 | Q4 | 84.5 | |||

| 2017 | Q1 | 68.2 | 2017 | Q1 | 87.8 | |

| Q2 | 70.8 | Q2 | 84.8 | |||

| Source: Office for National Statistics | ||||||

| Notes: | ||||||

| 1. Q1 is Quarter 1 (Jan to Mar) | ||||||

| 2. Q2 is Quarter 2 (Apr to June) | ||||||

| 3. Q3 is Quarter 3 (July to Sept) | ||||||

| 4. Q4 is Quarter 4 (Oct to Dec) | ||||||