Cynnwys

- Main points

- Introduction

- Natural capital accounting at a glance

- Achievements and progress made since the last roadmap

- Momentum for natural capital accounting is growing in the UK and internationally

- The issues we still need to address

- Communication and engagement

- What you said about the accounts

- Priorities for the final phase of the project: roadmap to 2020

- Annex 1: External stakeholder questionnaire

- Annex 2: Summary of outputs to deliver by 2020

1. Main points

- This article presents a review of the joint Office for National Statistics (ONS) and Department for Environment, Food and Rural Affairs (Defra) project to develop natural capital accounts for the UK; this project aims to incorporate natural capital into the UK Environmental Accounts by 2020.

- A revised roadmap is also presented, outlining priorities and outputs to be delivered by 2020.

- To date, natural capital accounts for several broad habitats and aggregated UK accounts are published and frequently updated; these accounts will continue to be developed further in the final phase of the project and will look to include several new ecosystem services.

- By 2020, a complete suite of accounts for broad habitats in the UK will be developed, including initial accounts for marine and coastal areas.

2. Introduction

In 2011 the government committed to working with Office for National Statistics (ONS) to incorporate natural capital into the UK Environmental Accounts by 2020 so that the benefits of nature would be better recognised . This commitment has recently been reiterated in the UK Government’s 25 Year Environment plan.

In 2012, in partnership with the Department for Environment, Food and Rural Affairs (Defra), ONS published a roadmap setting out early priorities for scoping and developing various types of accounts.

The project can be thought of in three stages, the initial phase, which set the direction for the project, explored new data sources, developed tangible principles to follow and trialled some account production.

The second phase, in which the initial accounts and principles were developed further and concrete steps were taken toward more robust and less experimental accounts.

Now the project is entering the third and final stage. This article presents a revised roadmap to take the project to 2020. The revised roadmap has been developed following an interim review of the entire project informed by:

- a systematic review of project outputs

- an external stakeholder survey

- structured feedback from the Natural Capital Accounting Steering Group (which includes strong support from representatives from devolved governments as well as members of the UK Natural Capital Committee)

The 2015 roadmap explained what natural capital accounts are and the benefits of producing them. Explanation has not been replicated in this article, but how the accounts fit with the emerging global agenda for measuring natural capital is discussed and updated.

Notes for: Introduction

- For more information, see the HMG White Paper, The Natural Choice: securing the value of nature, published in 2011.

3. Natural capital accounting at a glance

Natural capital is the term encompassing all the UK’s natural assets that form the environment in which we live. Natural capital accounts offer a coherent, comprehensive and consistent framework in which to organise and analyse statistical evidence from disparate sources. The organisation of information provides an immediate benefit, which facilitates monitoring, international comparability and identification of gaps.

The accounts record the size and condition of our natural assets and the physical and monetary values of the services provided to us by nature. For example, they tell us there are 3.2 million hectares of woodland in the UK and this woodland removed 16.5 million tonnes of carbon dioxide in 2015, which was valued at £1 billion – using this carbon price. They enable us to monitor the services we receive from our natural assets and track changes to them over time.

The natural capital accounts use the same accounting approach as used in the measurement of the economy, allowing comparability between environmental and economic information. However, natural capital accounting goes beyond conventional accounting measures in two important ways:

- they account for a wider range of outputs and services than gross domestic product (GDP), although some benefits of ecosystems will be implicit in measures of GDP

- they measure the contribution of ecosystems to standard measures of economic activity, such as GDP and national income, and assess of the role played by ecosystems in providing a range of other benefits to human well-being that are commonly unpriced and not considered in national-level economic reporting and analysis

The natural capital accounts are developed in line with international thinking, in particular, the principles set out in the United Nations System for Economic-Environmental Accounting Experimental Ecosystem Accounting (SEEA EEA) framework. This framework was developed to respond to the growing demand for information in policy areas such as sustainable development, resource use and land management.

The strategic case for natural capital accounting is strong. Our economy’s GDP only tells part of our economic story. We need also to account nationally not just for market output, buildings and roads but also for our natural capital, the ecosystems, green spaces and landscapes that provide us with a range of economic and non-economic benefits. This includes changes to extent and condition of the physical environmental assets, such as wetlands and forests, and to the value of services provided by healthy ecosystems, such as timber, carbon sequestration, air filtration and recreation.

In previously published roadmaps (2012 and roadmap 2015), Office for National Statistics (ONS) and the Department for Environment, Food and Rural Affairs (Defra) proposed to develop three types of natural capital accounts:

- broad aggregate estimates of UK natural capital – estimates of physical and monetary ecosystem service flow and asset accounts

- more detailed habitat-based ecosystem accounts (for example, woodland, freshwater) based on UK National Ecosystem Assessment (NEA) classification; these include the extent and condition of the habitat, as well as estimates of the ecosystem services provided

- cross-cutting or enabling accounts for important natural assets such as land, carbon and water that feed into the habitat and aggregate accounts

4. Achievements and progress made since the last roadmap

In the 2015 review, it was recognised that the accounts should have early practical application and should inform decision making by:

- shining a light on the losses and gains in natural capital and the relative importance of services provided by natural assets

- connecting economic growth with environmental pressures and informing consideration of overall sustainability of economic growth; this is achieved by being compatible with the System of National Accounts 2008: SNA 2008

- enabling the relationship between natural asset and ecosystem service delivery to be better understood through spatial disaggregation

During the second phase of the project, progress was made in a number of areas to develop existing and create new accounts, both in-house, through collaborative work with external organisations and commissioning experts.

Focusing on the three points detailed previously, further work to improve the structure of statistical bulletins to highlight important changes in the service flows and condition of natural assets has been conducted to enable losses and gains in natural capital to be highlighted. The relative importance of different services, particularly between cultural, regulating and provisioning services can now be readily derived from the accounts. For example, the woodland account shows that the value of cleaner air and recreational opportunity provided by woodland is nine times more than the value of timber produced.

In the latest aggregate UK accounts, both non-monetary and monetary ecosystem service estimates are presented together to help understand the link between physical changes in production of services and changes in value. Additionally, in the UK habitat accounts the condition and ecosystem service accounts are presented together to enable the relationship between natural asset and ecosystem service delivery to be better understood.

It was also identified in the 2015 roadmap that for the accounts to be used, a number of issues would need to be addressed, including:

- production of a reasonable time series, spatial disaggregation and assessment of the condition of stocks (assets) and the nature of flows (services) to understand sustainability further

- the accounts and the underlying data need to reflect changes in resource management, ecosystem condition and service delivery

- the merit and feasibility of including restoration or maintenance cost information within the accounting framework

Significant progress has been made since the 2015 review. In general, existing accounts and methodology has been improved to improve quality and reliability of the accounts. The time series has been extended in the UK Natural Capital accounts publication, annual flows for many services are now available back to 1997. Further, production systems have been developed to enable quicker annual account production and regular publications.

A number of the accounts were quality reviewed by environmental experts to improve quality, including experts at Natural England and Forestry Commission. New data sources have been included in the accounts, in particular, through recent work with the Centre for Ecology and Hydrology and Ordnance Survey.

The 2015 roadmap set out outputs to be developed by 2017 and 2020. Table 1 provides a quick evaluation of progress; the comments indicate developments since the 2015 roadmap (phase 2).

Table 1: Progress made against important milestones published in the 2015 roadmap

| Account | At least initial accounts | Scoping study only | Developments made in Phase 2 | |

|---|---|---|---|---|

| UK Natural Capital Accounts (Overall) | Y | Initial accounts revised in 2016 and 2018. Systems put in place for annual production | ||

| Broad Habitat | ||||

| Woodland | Y | Initial accounts revised in 2016 and 2017. Further work needed on condition account but systems in place for annual production. | ||

| Farmland | Y | Scoping and initial accounts published in 2016 and revised in 2017. | ||

| Further work needed on condition account but systems in place for annual production. | ||||

| Freshwater | Y | Initial accounts revised in 2017. Further work needed on condition account but systems in place for annual production. | ||

| Urban areas | Y | Scoping account published in 2017. Accounts for Great Britain to be published in summer 2018. Includes new estimates for urban cooling, noise reduction and a bundle of cultural services (recreational and aesthetic appreciation). | ||

| Semi-natural grassland | Y | Scoping study published in 2018. | ||

| Coastal Margins | Y | Scoping study published in 2016. | ||

| Marine | Y | |||

| Mountains, moorland and heath | Y | Scoping study published in 2017. | ||

| Ecosystem (biotic, living) service accounts | ||||

| Agricultural biomass provision | Y | Annually updated at UK level. | ||

| Timber production | Y | Annually updated at UK and country level. | ||

| Water provisioning | Y | Annually updated at UK and country level. | ||

| Fish production | Y | Annually updated at UK level. | ||

| Carbon sequestration (removal) | Y | Annually updated at UK level and select habitats. | ||

| Flood protection | Y | Scoping study published in 2016, further work being conducted by Forestry Commission. | ||

| Urban cooling | Y | GB estimate for 2015 in development. | ||

| Air filtration | Y | Data available to 2015 at UK, country local authority level. Spatial data to 1km grid square available. | ||

| Noise reduction | Y | GB estimate for 2015 to be published in summer 2018. | ||

| Recreation | Y | Annually updated at UK level, further work needed incorporate free trips and devolved country data. | ||

| Abiotic (Non-living) service accounts | ||||

| Energy provision | Y | Annually updated at UK level, for oil, gas and renewable energy. | ||

| Mineral provision | Y | Annually updated at UK level for many minerals. | ||

| Thematic accounts/methodology | ||||

| Land cover and land use | Y | |||

| Carbon Stock | Y | Initial accounts published 2016. | ||

| Protected areas | Y | Initial pilot accounts published 2015. | ||

| Peatlands | Y | |||

| Other related accounts | ||||

| Restoration cost accounts | Y | Scoping study and two pilot accounts sent to Eurostat in 2017. A slide share summarising the work is available. Full report available upon request. | ||

| Source: Office for National Statistics | ||||

| Notes: | ||||

| 1. Y = Developed | ||||

| 2. Marine and peatland scoping studies and land cover and land use initial accounts were developed in Phase 1. | ||||

Download this table Table 1: Progress made against important milestones published in the 2015 roadmap

.xls (42.5 kB)We have also developed the principles for natural capital accounting in the UK, publishing a second version in 2017 and made significant progress improving our engagement by:

- developing a 600 plus stakeholder list ensuring regular communication via quarterly newsletters

- leading and contributing to international discussions to develop standards and frameworks

- presenting the accounts at numerous international and national events to promote the project and build relationships

Not every milestone on the roadmap was achieved, but a degree of flexibility was expected to adapt to changing priorities and unforeseen issues. Resources were reprioritised to enable development work to take place on existing methodology or new accounts. For example, cross-cutting soil and biodiversity accounts were not developed, however, air filtration and restoration cost accounts were.

Restoration cost accounts were identified as a priority area and a roadmap has been developed to identify how these accounts can be developed alongside the natural capital accounting project. Two pilot restoration cost accounts for peatland were produced, for more information please see the SlideShare.

Nôl i'r tabl cynnwys5. Momentum for natural capital accounting is growing in the UK and internationally

Since the 2015 roadmap, the natural capital accounting approach to valuing our environment has built momentum in the UK, with increased support in both public and private arenas.

In early 2018, the UK government released the 25-year Environment Plan, which cited various estimates from the accounts published to date, and more generally adopted a natural capital approach throughout, with real thought given to the importance and value of all the services provided by our natural surroundings. The plan pledges the government’s continued support for the development of UK natural capital accounts “that are widely understood and shared internationally”. They should complement and support the monitoring framework being developed for the plan to “provide a much richer picture of changes to the environment over time”. Transparent reporting of progress is crucial to the success of the various goals in the plan and a full set of natural capital accounts should be available to inform decisions during the 25-year journey and beyond.

Internationally, the United Nations Statistical Division is in the process of revising their guidance on ecosystem accounting in the light of the work completed in the recently published Technical Recommendations. The UK accounts follow the UN System of Environmental-Economic Accounting (SEEA) international guidelines, which provide a framework, based on the System of National Accounts 2008: SNA 2008, for the development of environmental and ecosystem accounts. By adopting the UN SEEA frameworks and through the UK’s involvement in the development of international standards, the UK accounts are expected to be consistent with emerging standards.

The revision aims to reach agreement on as many aspects of ecosystem accounting as possible by 2020. The Department for Environment, Food and Rural Affairs (Defra) and Office for National Statistics (ONS) are actively involved in this process and will be helping to lead work on valuation issues. The work will be managed by a Technical Committee on which the UK is represented. At various points over the next two years the work in progress will go out to wider consultation.

As well as the development of the UN SEEA frameworks, the natural capital accounts are also featured in several other global initiatives to improve sustainability.

Wealth accounting

This incorporates other capitals such as social and human capital. Wealth accounting is well recognised as a useful means to supplement traditional macroeconomic indicators and some estimates have been produced by the World Bank for 150 countries. The winners of the 2017 Indigo Prize both suggested a wealth accounting approach when asked to design a new economic measure to fully acknowledge social and economic factors (Global Perspectives, 2017).

“WAVES” project (World Bank)

The “WAVES” project assists a number of partner countries, with UK support, to implement natural capital accounting. There are a growing number of ecosystem accounts being developed in various countries.

UN Sustainable Development Goals (SDGs)

Target 15.9 of the UN Sustainable Development Goals states: “By 2020, integrate ecosystem and biodiversity values into national and local planning, development processes, poverty reduction strategies and accounts.”

EU KIP-INCA project (Knowledge Innovation Project – Integrated system for Natural Capital and ecosystem services Project)

The project will help establish sound methods of accounting for natural capital with a strong focus on ecosystems and their services. Aims include establishing an accounts system at the EU level and to support member states in developing accounts at national level.

Nôl i'r tabl cynnwys6. The issues we still need to address

Methodological issues and research needs

As discussed in the previous review and roadmap, the project is about learning-by-doing with the starting point as the UN System of Environmental-Economic Accounting Experimental Ecosystem Accounts (SEEA-EEA) international guidelines. To overcome the challenge of applying an experimental framework consistently, Office for National Statistics (ONS) and the Department for Environment, Food and Rural Affairs (Defra) published methodological guidance on the accounts (Principles of Natural Capital Accounting, first published in 2014 and updated in 2017). This guidance defines principles that are currently followed by ONS and Defra when developing the accounts and documents our assumptions and thinking behind assumptions.

The Principles guide has proven valuable for the project team and external researchers developing national or subnational accounts. Stakeholder feedback has indicated that this guide is very useful, but could be made more accessible with practical examples and less technical language. In phase 3 of the project a methodology handbook and practical guide to natural capital accounting will be developed to help users understand the UK accounts and assist practitioners in producing their own accounts. As well as the guide, there are also several overarching methodological issues that need further exploration. Three important cross-cutting issues that will need further work before 2020 are detailed in this section.

Spatial disaggregation

Clarify how disaggregated accounts should be, identifying what the minimum level of aggregation is needed to compile comprehensive ecosystem service and condition accounts. A further issue that needs to be considered is how information is reported, as this becomes more difficult, the more spatially disaggregated the accounts are.

Valuation based on welfare or exchange values

There are a range of ways to value ecosystem services and the Principles guide and UN SEEA frameworks recommend “exchange values” as the type of valuation that should be favoured for inclusion in the accounts. The type of valuation approach used should be consistent across ecosystem services, but currently a mix between the two is typical.

Monetary asset valuation

Asset valuation presents many challenges. In phase 2 of the project the asset life and choice of discount rate were reviewed. Further work is needed to predict future flows of ecosystem services. Further work is also needed to understand the drivers of changes in asset values over time, establishing if changes are a result of price changes or changes in the expected supply and demand for services.

Ownership of ecosystems and beneficiaries

It is important to identify the asset owners and the beneficiaries of the ecosystem services. This is not currently included in the accounts and further work would be needed to identify who the users and beneficiaries are.

Spatial data and data gaps

In the 2015 review, important data gaps in economic and environmental data were noted, including up-to-date land cover and condition indicators. Many data sources did not have a sufficient spatial resolution or a consistent time series needed to monitor change over time.

Since 2015, we have reviewed the data we use and further data gaps have been identified. More engagement with data source owners has been made, including with the Centre for Ecology and Hydrology, Natural England and Ordnance Survey. Through work with the Natural Capital Coalition and the Institute of Chartered Accountants in England and Wales (ICAEW), a project is also in progress to establish if there are business data that can be used for natural capital accounting purposes.

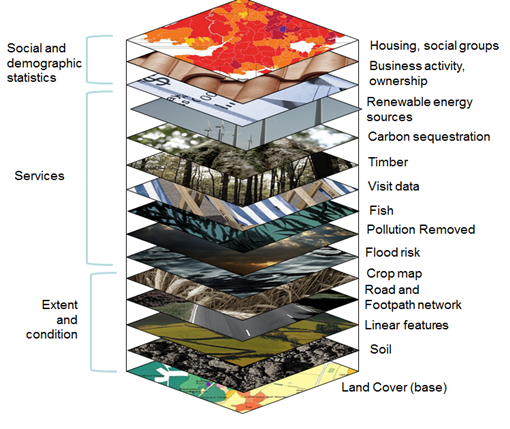

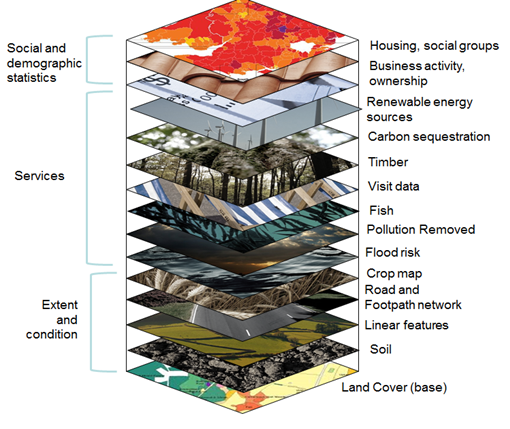

In developing natural capital accounts, the spatial data vision presented in Figure 1 is being worked towards. The image does not display all data maps needed, but does display currently identified maps needed for the accounts, some of which have already been included. It is not expected that all maps will be obtained and in use by 2020, this is a long-term goal and vision to work towards. An additional complexity is the maps not only need detailed resolution but also need to be consistently updated on a consistent spatial resolution to monitor changes over time.

Figure 1: Layered approach to developing spatial data

Source: Office for National Statistics

Download this image Figure 1: Layered approach to developing spatial data

.png (260.1 kB){kind=link}

Further work is needed in phase 3 to identify more spatial data sources of relevance and actively promote data gaps to enable others to help fill them. An important data gap already identified that will need attention in phase 3 is the extent of small areas of vegetation, which enable measurement of vegetation on transport corridors and linear features such as street trees and hedgerows. This information will be of particular importance to urban areas, also when measuring ecosystem connectivity and fragmentation.

Work is also needed to establish how the collection of spatial maps should be stored and made available to users.

Nôl i'r tabl cynnwys7. Communication and engagement

The 2015 roadmap identified the need for further external engagement with the wider community of interest in accounting. It was suggested engagement would occur through newsletters, non-technical guides, workshops, reforming the website, international engagement and a dedicated advisory group.

Since the 2015 roadmap, the project has engaged with a diverse range of stakeholders and devoted time to actively promote the accounts. The project has identified and engaged with stakeholders in several ways:

- condensed bulletins, social media interaction and visual pieces have enabled the accounts to be more accessible and main messages to be picked up quickly; our bulletins meet the ONS Style guidelines and feedback is regularly requested in each output

- established a stakeholder and communication list, with over 600 members from academia, local authorities, public bodies, private bodies and the general public

- newsletters are sent quarterly to communicate new publications and request contact and involvement in upcoming projects; newsletters have proved a quick and successful method of communication

- annual conference held to promote natural capital accounting, learn from others work and engage more widely in a personal format

- membership and engagement with other UK natural capital bodies, including becoming a member of UK Environmental Observation Framework (UK EOF), Natural Capital Coalition and continued support from and engagement with the Natural Capital Committee

- continued international engagement, not only through the process of revising the SEEA EEA, but also including close involvement with the United Nations London Group and engagement with the European MAES and KIP-INCA projects; informal and formal bilateral relationships have also been formed with other countries leading in this work

Going forward, these engagement initiatives will be continued. It is recognised that the project has engaged primarily with national bodies, but going forward those wishing to compile accounts at more local levels, such as local authorities and land owners, should be engaged more.

Nôl i'r tabl cynnwys8. What you said about the accounts

A short survey was sent to our stakeholders asking for feedback on the project and the accounts developed so far. The aim of the questionnaire was to determine areas for improvement and areas of importance for stakeholders. The questionnaire contained eight questions (provided in full in Annex 1) and there were 62 respondents from 52 organisations. Important findings from the survey show:

- 89% of respondents said natural capital had become increasingly important in the last two years

- 89% of respondents were interested in both the monetary and physical accounts

- 92% of respondents identified at least one of the habitat or cross-cutting accounts being extremely relevant to their work

- 45% have used at least one of the accounts

Respondents were asked which areas they would like to see the project make better progress in and Table 2 shows the themes that emerged with the following actions to be taken.

Table 2: Stakeholder feedback – themes and actions

| Feedback from stakeholders | Response and actions to be taken in Phase 3 | |

|---|---|---|

| Provide more guidance for others producing accounts, including worked examples and case studies. Also ensure relevance for local/regional decision makers and accounts outside of the UK. | In Phase 3 of the project a methodology handbook and practical guide to natural capital accounting will be developed to help users understand the UK accounts and assist practitioners in producing their own accounts. | |

| Bulletins should be more digestible with less technical language and further analysis. | A lot of work has already been undertaken to improve the usability of statistical bulletins, in line with changes made across ONS. Further work will be undertaken to ensure bulletins are as digestible as they can be and all technical terms explained. | |

| Explain the links with other ONS outputs, particularly the Environmental Accounts and Social Capital. | Further thought will be given to highlight the similarities and differences between the Environmental accounts, the wider wealth accounts and the natural capital accounts. | |

| Provide greater co-ordination with stakeholders, including ministerial engagement and engagement with local authority planning teams. | With limited resources there is a limit to the amount of engagement the project can provide. In Phase 3 the project team will explore further the idea of a Centre of Excellence for Natural Capital Accounting, of which one of the aims will be to engage more widely. | |

| The engagement strategy should be made publicly available and when others are providing quality assurance more time should be given for external review and comment on the accounts. | The team will endeavour to send timelines to quality assurers to ensure enough time has been allocated for quality assurance. | |

| Generally, more further development made in the following areas; condition measurement, monetary valuation, biodiversity (including the value of the diversity of wildlife) and soil. | Further work on condition measurement, which includes biodiversity indicators, and improvements to monetary valuation are included in outputs in the phase 3 roadmap. | |

| Peatland accounts are in development and condition indicators include aspects of soil quality, however a specific soil account will not be produced in Phase 3. | ||

| Source: Office for National Statistics | ||

Download this table Table 2: Stakeholder feedback – themes and actions

.xls (38.4 kB)9. Priorities for the final phase of the project: roadmap to 2020

The 2015 roadmap identified outputs to deliver by 2017 and by 2020. This section revises those priorities, provides the revised outputs to be delivered by 2020 and suggests what will be needed for account maintenance beyond 2020.

Given limited resources, we still intend to adopt a balanced strategy of making broad progress across a wide range of accounts, whilst at the same time focusing development effort on a few important accounts where the policy interest is likely to be greatest and real progress can be made. The goal by 2020 is for a full set of accounts to be developed and integrated as far as possible with the UK Environmental Accounts. The degree of progress is expected to vary between accounts depending upon relative data and methodological challenges, and we will need to be flexible to optimise progress as new issues, data and policy opportunities emerge.

By 2020, the UK Natural Capital accounts and all eight broad habitat ecosystem accounts will be developed to at least initial account level. The accounts are still expected to be classed as Experimental Statistics, but the quality will be improved. The accounts will be timelier, have greater spatial disaggregation and methodology standardised so that revisions are minimised.

It is expected that the accounts will have regular users and the stakeholder network created will be expanded further. The project will also be taking a greater lead in providing standards and advice for others to follow.

The aggregate account and existing habitat account publications will be updated regularly but not annually. This will enable the complete suite of habitat accounts to be developed by allowing time for development of initial semi-natural grassland, marine and coastal margin ecosystem accounts. Mountain, moorland and heath accounts and accounts for urban areas are already in development.

Additionally, links with metrics for the government’s 25 Year Environment Plan and the Sustainable Development Goals (SDGs) will be explored with the expectation that several indicators relevant to the SDGs will be developed. Select natural capital accounts for Scotland and Wales will also be developed in 2018 to 2019 thanks to funding from Scottish Government and Welsh Government.

Finally, as well as the outputs presented in Table 3, further work will be conducted to promote the accounts, maintain regular communication with users and show international leadership by engaging in discussions and working groups to standardise international guidelines.

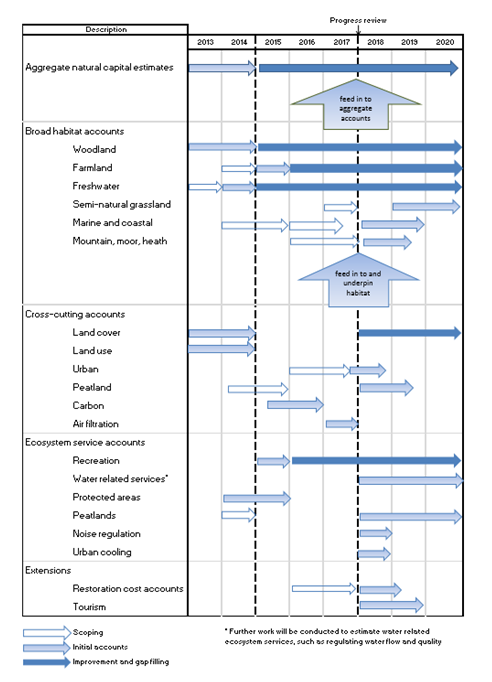

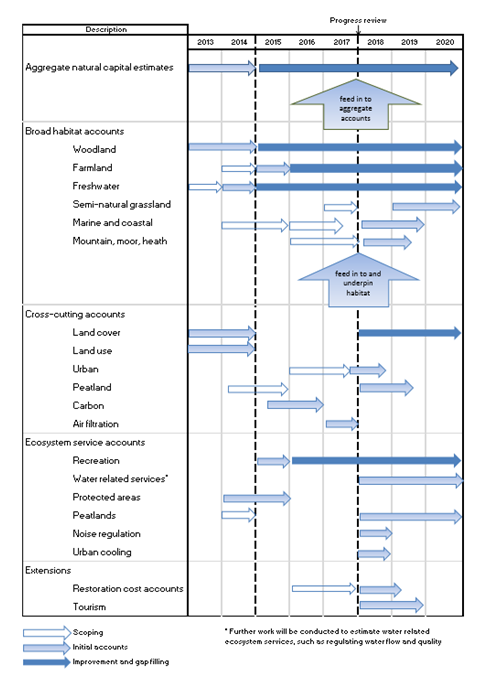

Table 3 summarises outputs that will be delivered by 2020, while Annex 2 provides this in a visual format and provides an idea of timings.

Table 3: Outputs to be delivered by 2020

| Type of account | Activity | Specific outputs in Phase 3 |

|---|---|---|

| Aggregate Natural Capital accounts | Maintenance and mainstreaming of aggregate accounts | Two further bulletins will be published, including an updated land cover accounts. |

| Each iteration of the accounts improves the maintenance and mainstreaming of the accounts. | ||

| Development of and research into new and existing ecosystem services | Inclusion of at least four substantive non-provisioning services developed – for example, flood protection, noise reduction, urban cooling and services to the tourism industry. | |

| Development of country level accounts | Accounts for Scotland only. | |

| Habitat based accounts | Maintenance and mainstreaming of existing habitat accounts | Two further bulletins published containing woodland, farmland and freshwater accounts. |

| Development and research into existing habitat accounts. | Substantial development of condition indicators, involving a review of indicators to be used in the natural capital accounts. | |

| New habitats to be developed into initial accounts | Initial accounts published for mountain moorland and heath, semi-natural grassland, and marine and coastal margins. | |

| Development of country level accounts | Woodland, farmland and freshwater accounts for Wales only. | |

| Extensions | New cross-cutting accounts to be scoped or developed | Initial accounts for urban areas will be developed. The scoping of peatland accounts will be developed into initial accounts. |

| Further work to develop restoration cost accounts | Initial restoration cost accounts for the mountain, moorland and heath habitat and for peatland will be published. | |

| Improve transparency and communication of methodology. | A methodology handbook and practical guide to be published. It will aim to help users understand the UK accounts and assist practitioners in producing their own accounts. | |

| Link with other reporting frameworks | Further work will be conducted to link the natural capital accounts to the SDG indicators. It is expected that a number of indicators from the natural capital accounts will be included in SDG reporting by 2020. | |

| Source: Office for National Statistics | ||

Download this table Table 3: Outputs to be delivered by 2020

.xls (38.4 kB)Beyond 2020

The project will complete in December 2020; however, the accounts are not expected to be final at this stage. A set of robust underlying methodological principles are expected, as well as a good set of initial accounts covering all habitats will be developed and useable. Further developmental work on particular ecosystem services and habitats that have proved more difficult due to their nature or data limitations will be needed. Additionally, work will be required to ensure the revised United Nations System for Economic-Environmental Accounting Experimental Ecosystem Accounting (SEEA EEA) guidance (and in due course, international standards) is adopted.

Like any set of statistics, the accounts will need to be maintained and gaps, such as for particular ecosystem services, addressed. All accounts will need to be regularly reviewed to incorporate new conceptual developments and data availability. It is expected that all accounts will still need to improve the degree of spatial disaggregation and work will continue to seek and create new data sources and methods to allow for this.

Nôl i'r tabl cynnwys10. Annex 1: External stakeholder questionnaire

Question 1:

Please rank the importance of natural capital within your work (1 being of no importance and 5 being crucially important)

Question 2:

In the last 2 years, within your work, has natural capital accounting become more or less important? If it has become more or less important, please explain.

Question 3:

Are you interested in physical or monetary accounts?

Question 4:

The following are habitat and cross-cutting accounts that have been developed, are under development or planned to be developed within the ONS-Defra Natural Capital Project.

Please choose the option for each account which corresponds most to you and your work. (This question displayed as an answer matrix for each account giving the choice of extremely relevant, quite relevant or little or no relevance.)

A. Farmland

B. Flood protection

C. Carbon stock

D. Woodland

E. Freshwater

F. MMH

G. Grassland

H. Peatlands

I. Recreation

J. Urban

K. Coastal margins

L. Marine

Question 5:

Have you utilised any accounts published by ONS and Defra to date? If yes, please explain.

Question 6:

Are there any areas which you would like to see better progress from the ONS-Defra Natural Capital Project? If yes please explain.

Question 7:

How satisfied are you with the engagement from ONS-Defra on natural capital accounting? If dissatisfied or have any suggestions, please comment below.

Question 8:

Finally, please briefly describe your involvement with natural capital accounting.

Nôl i'r tabl cynnwys11. Annex 2: Summary of outputs to deliver by 2020

Annex 2: Summary of outputs to deliver by 2020

{kind=link}