Cynnwys

- Main points

- Size of the area covered by woodland

- Condition of UK woodlands

- Overall quantity and value of woodland ecosystem services

- Provisioning ecosystem services: quantity and value

- Regulating ecosystem services: quantity and value

- Cultural ecosystem services: quantity and value

- Asset value of woodlands

- Woodland ecosystem services data

- Glossary

- Measuring the data

- Strengths and limitations

- Related links

1. Main points

There were an estimated 475 million visits to woodlands in 2017, on which the public spent £515.5 million collectively.

The non-market benefits of woodland exceed the market benefits of timber by approximately 12 times; timber represents £275.4 million out of £3.3 billion total annual value of woodland in 2017.

The asset value of UK woodlands was estimated as £129.7 billion in 2017, with timber representing £8.9 billion (6.9%).

The removal of air pollution by woodland in the UK equated to a saving of £938.0 million in health costs in 2017.

Woodland in the UK removed 18.1 million tonnes of carbon dioxide equivalent in 2017, equating to a value of £1.2 billion; this is equivalent to 4% of total UK greenhouse gas emissions in 2017.1

Urban woodlands cooled 11 city regions sufficiently on hot days to save £229.2 million in labour productivity and avoided air conditioning costs during 2018.

Woodlands occupy 13% of the land area of the UK with 3.2 million hectares.

Notes for: Main points

- Total greenhouse gas emissions in 2017 were 460 MtCO2e.

2. Size of the area covered by woodland

Woodlands in the UK are tree-covered areas, which include plantation forests, more natural forested areas, and lower density or smaller stands of trees.

The natural world is valued in many different and important ways, but it can be valued as a set of assets supplying goods and services that the economy and society benefit from. For example, food, water or clean air. These habitat capital accounts monitor the size and condition of woodland assets as well as the quantity and value of the services supplied.

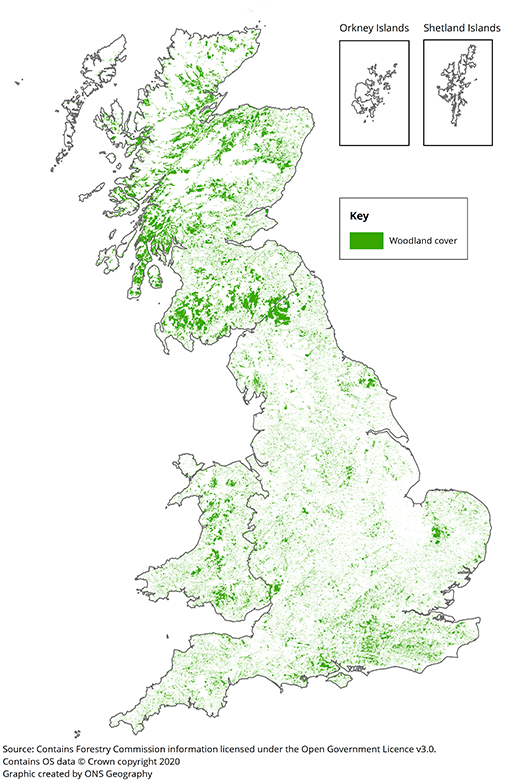

Figure 1: Extent of Great Britain woodland, 2018

Source: Forestry Commission – National Forest Inventory

Download this image Figure 1: Extent of Great Britain woodland, 2018

.png (342.5 kB){kind=link}

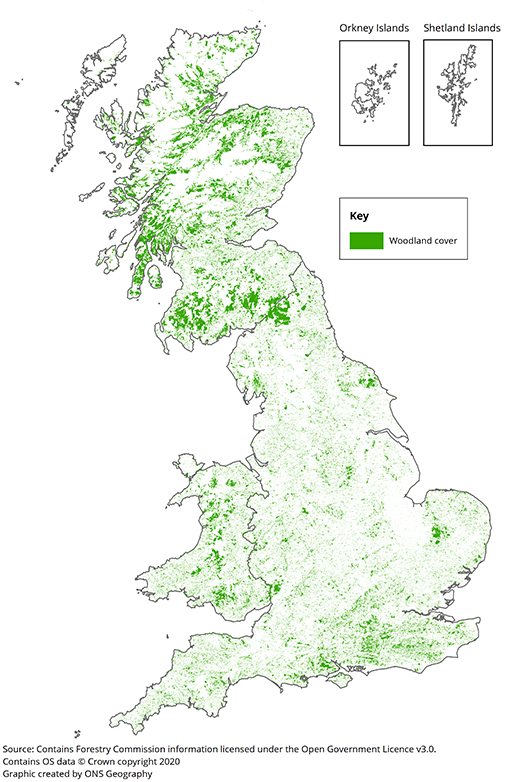

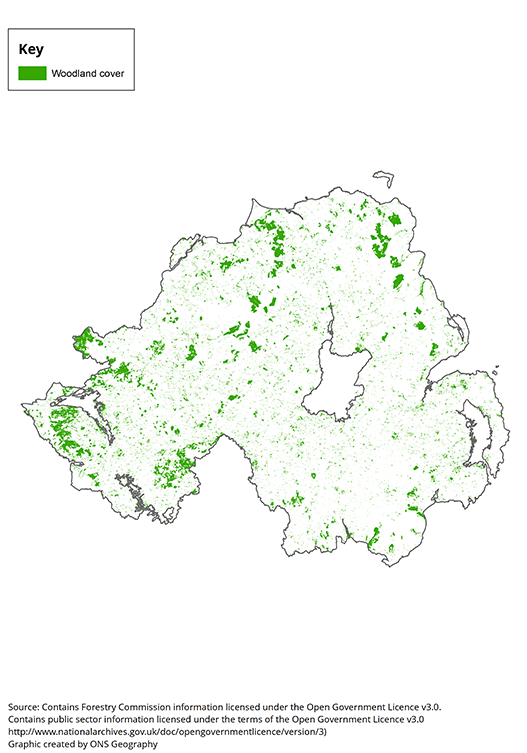

Figure 2: Extent of Northern Ireland woodland, 2018

Source: Forestry Commission – National Forest Inventory

Download this image Figure 2: Extent of Northern Ireland woodland, 2018

.png (232.0 kB){kind=link}

Land covered by forestry (Figures 1 and 2) has increased steadily by 4.4% from 3.05 million hectares in 2009 to 3.19 million hectares in 2019. Scotland has 46% of the UK’s woodlands, England has 41%, Wales has 10% and Northern Ireland has 4%. As a percentage of the total land area, woodlands account for:

13% of the UK

10% of England

15% of Wales

18% of Scotland

8% of Northern Ireland

Conifers account for approximately half (51%) of the UK woodland area in 2019 (Figure 3), with just over half (55%) of these conifers privately owned. In contrast, the majority (92%) of broadleaved woodland is privately owned.

The proportion of woodland that is publicly owned fell slightly in the past 10 years, from 29% (872,000 hectares) of total woodland in 2009 to 27% (863,000 hectares) of total woodland in 2019, with the private ownership proportion rising from 71% (2,182,000 hectares) in 2009 to 73% (2,325,000 hectares) in 2019.

National Forest Inventory (NFI) statistics from the Forestry Commission have been used for the extent account as it provides the most up-to-date dataset focussing solely on woodland. Currently, only woodland used for forestry that is over 0.5 hectares in extent and greater than 20 metres in width is included in the extent account. This includes areas recently felled but expected to be replanted and open space within woodland.

Figure 3: Conifers accounted for 51% of UK woodland area in 2019

Extent of woodland, UK, 2007 to 2019

Source: Forest Research – National Forest Inventory

Download this chart Figure 3: Conifers accounted for 51% of UK woodland area in 2019

Image .csv .xlsIn addition to woodland areas, the Forestry Commission estimates there are 390,000 hectares of small woods in Great Britain (non-NFI wooded areas of over 0.1 hectare in extent). There are also 255,000 hectares of groups of trees (that is, clusters and linear tree features of less than 0.1 hectare in extent) and an estimated total canopy cover of 97,000 hectares from lone trees in Great Britain (Figure 4). For Great Britain, that is a total woodland area of 3,719,000 hectares.

Figure 4: Lone trees represented 2.6% of woodland area in 2019 for Great Britain

Total woodland extent, UK and Great Britain, 2019

Source: Forest Research and Forestry Commission – National Forest Inventory

Download this chart Figure 4: Lone trees represented 2.6% of woodland area in 2019 for Great Britain

Image .csv .xls3. Condition of UK woodlands

The health of woodlands can be measured through a range of metrics. Woodland age structure, the variety of trees present, presence of different mammals and birds, the understory vegetation, and the presence of deadwood all reflect woodland ecological health.

Ecologists regularly use a simple set of descriptive words to summarise the overall status of a habitat or species: “Favourable” being good, “Unfavourable” being bad, and “Destroyed” meaning the habitat at a site is no longer present and there is no prospect of being able to restore it. These descriptions are based on an assessment of an appropriate set of metrics dependent on what is being measured.

While certified woodlands and access are increasing, several indicators of woodland condition are unfavourable or in decline (Table 1). Out of the seven NFI condition indicators, two are considered unfavourable across the majority of woodland: the presence of veteran trees and deadwood (Figure 5).

The butterfly and bird indices for woodlands are both in a long-term decline, having a negative impact on biodiversity. Woodland fires in the UK also have a negative impact. There has been a significant rise in the area of woodlands having large fires over the last decade, with 29,396 hectares affected during 2019 to 2020 (Table 7). There has been an increase in the area of Forest Stewardship Council (FSC) certified woodlands and increased access to woodlands for the population. An estimated 74% of the population have access to woodland within four kilometres of their home, as of 2017.

| Type | Indicator | Condition | Long term trend | Short term trend |

|---|---|---|---|---|

| Biodiversity | Butterfly index UK | Long term decline 1990 to 2018 | Declining | Little or no change |

| Woodland bird index UK | Decrease of 29% between 1970 to 2018 | Declining | Declining | |

| Tree age structure GB | NFI first assessment 42% area unfavourable | |||

| Regeneration GB | NFI first assessment 0% area unfavourable | |||

| Veteran trees GB | NFI first assessment 99% area unfavourable | |||

| Tree health GB | NFI first assessment 85% area favourable | |||

| Deadwood GB | NFI first assessment 77% area unfavourable | |||

| Herbivores & grazing GB | NFI first assessment 49% area favourable | |||

| Invasive plant species GB | NFI first assessment 92% area favourable | |||

| Certified woodlands | Area FSC certified woodlands UK | Improvement 32% from 2001 to 2019 | Increasing | Increasing |

| Space for people | Access to woodlands UK | Improvement 0.1% from 2012 to 2016 | Increasing | Increasing |

| Protected sites | Scotland SSSIs/SACs | 51% favourable in 2018 | ||

| England SSSIs | 37% favourable 2018/19 | |||

| Pressure indicators | Wildfires UK | 2019-20 29,396 hectares affected (EFFIS data) | Increasing | Increasing |

Download this table Table 1: Summary of the condition of UK woodlands

.xls .csvThere is significant variation in condition scores across various metrics. For example, very few forests are “favourable”, but 85% of woodland is favourable for tree health (Figure 5).

Figure 5: 85% of woodlands are in a favourable condition for tree health in Great Britain

Summary of National Forest Inventory (NFI) condition indicators 2010 to 2015 survey cycle, percentage of area classified as unfavourable, intermediate or favourable

Source: Forest Research – National Forest Inventory

Download this chart Figure 5: 85% of woodlands are in a favourable condition for tree health in Great Britain

Image .csv .xlsBiodiversity

Biodiversity, though its impact is hard to quantify, lies at the heart of or at least affects all woodland ecosystem services. Examples of biodiversity include the roles of fungi and bacteria, nutrient cycles, and culturally important mammals and birds. Increasing biodiversity improves the provision and sustainability of ecosystem services (ZIP, 2.67MB). The ecology of woodlands is mainly determined by the amount of light beneath the canopy, if the tree species are native or non-native, the age of the trees, and the number of different microhabitats available. The Forestry Commission identified (PDF, 259KB) that while there is no definitive relationship between tree age and biodiversity, there is evidence of an increase in biodiversity with stand age. The analysis for mammals and birds revealed that after a short initial increase, as trees grow from saplings, there is a decline in biodiversity until the trees reach 20 years of stand age, then it increases.

Indicators of biodiversity in woodlands investigated in this publication include the woodland butterflies and bird indices, age of the trees, presence of veteran trees, health of the trees, and impacts from herbivore grazing and invasive plant species.

Butterfly index

The number of woodland butterflies has been decreasing over time. In 2012, it began to flatten, showing little to no change in the index, as seen in the smoothed data. According to the Department for Environment, Food and Rural Affairs’ (Defra’s) Butterflies in England report, this long-term decline is largely because of fewer open spaces within woodland and a lack of management of these woodlands. This includes thinning trees within woodlands to allow sufficient light in, thereby helping with the growth of multiple food sources. When unmanaged, these food sources do not grow sufficiently, leaving butterfly species without the necessary nutrients to survive within the woodland.

The unsmoothed (raw) index for butterflies shows fluctuation throughout the entire time series (Figure 6). This is because of the butterflies’ response to weather conditions, such as the summer heatwave in 2018. This change in weather caused around two-thirds of species to increase that season.

The State of the UK’s Butterflies 2015 report observes that many butterfly species have been declining since 1976. But there are three species that have shown a positive response: the ringlet, orange-tip and peacock.

Figure 6: The woodland butterfly population is in a long-term decline

Woodland Butterfly Index, UK, 1990 to 2018

Source: Butterfly Conservation; Centre for Ecology and Hydrology; Department for Environment, Food and Rural Affairs – Woodland Butterfly Index

Download this chart Figure 6: The woodland butterfly population is in a long-term decline

Image .csv .xlsBird index

Woodland bird populations decreased by 29% between 1970 to 2018, a very similar decrease to that of the butterfly population but at a much slower rate. We can see that there was a steep decrease in the 1990s, with the index then beginning to flatten. That is, until 2012, when the index once again began to decline (Figure 7). Some possible reasons for this decline are outlined in the following, but none of these can be confirmed and the Royal Society for the Protection of Birds (RSPB) is investigating for a more concrete explanation.

The majority of woodland bird species have either decreased (32%) or had no change at all (46%) over the long term, with a minority of 22% increasing over time such as the great spotted woodpecker and the nuthatch. According to Defra’s Wild Bird Populations in the UK, 1970 to 2018, this decrease may be a result of a lack of woodland management along with increased deer-browsing pressure. Both of these result in a lack of diversity within woodland and few suitable nesting habitats.

The willow tit species has experienced the largest decline at 94% since 1970. While the reason for this large decline is unclear, the RSPB’s managing willow tit habitat project highlights changes in habitat structures and the drying out of woodland soils as possible reasons for this, among others.

Figure 7: Woodland bird populations decreased by 29% between 1970 to 2018

Woodland Bird Index, UK, 1990 to 2018

Source: British Trust for Ornithology; Royal Society for the Protection of Birds; Department for Environment, Food and Rural Affairs – Woodland Bird Index

Download this chart Figure 7: Woodland bird populations decreased by 29% between 1970 to 2018

Image .csv .xlsBats

Some bat species are heavily dependent on woodlands and so can also be used as a biodiversity condition indicator for woodlands. The Bat Conservation Trust has identified six species that are woodland specialists. These are Bechstein’s bats, barbastelles, Natterer’s bats, noctules, lesser horseshoe bats and brown long-eared bats. The Bat Conservation Trust will be instigating monitoring of woodland bat populations in summer 2020, with an initial baseline index value available in spring 2021 and a provisional trend available from spring 2023.

National Forest Inventory (NFI) condition indicators

The NFI survey is based on data collected between 2009 and 2015. Full details on the Forest Research’s NFI survey methods are available.

| Unfavourable | Intermediate | Favourable | |

|---|---|---|---|

| Invasive species | 7.3 | 0.8 | 91.9 |

| Tree health | 2.6 | 12.9 | 84.5 |

| Herbivores and grazing | 40.0 | 11.4 | 48.6 |

| Regeneration | 0.0 | 89.4 | 10.6 |

| Age distribution | 42.0 | 46.9 | 11.2 |

| Deadwood | 76.6 | 17.3 | 6.1 |

| Veteran trees | 99.3 | 0.2 | 0.5 |

Download this table Table 2: Summary NFI condition indicators for Great Britain, 2010 to 2015 survey cycle

.xls .csvA varied tree age structure in woodland benefits biodiversity as differently aged trees provide different ecological habitats. As a percentage of the total trees in Great Britain:

- 24.3% of trees are aged 20 years or younger

- 33.0% of trees are aged 21 to 40 years

- 23.9% of trees are aged 41 to 60 years

- 18.8% of trees are aged 61 years or older

For a woodland to be classified as favourable, it needs to have young, intermediate and old trees present.

Regeneration is an important indicator of biodiversity to predict the future health of woodlands. It is an assessment of seedlings, saplings and young trees. To be classed as favourable, the woodland areas sampled need to have trees with a 4cm to 7cm diameter as well as having saplings and seedlings present.

Tree diseases and pests can have a negative impact on woodland biodiversity. While dead and decaying wood provides more light to reach the forest floor and an important micro-habitat, rapid widespread tree death can harm ecological health.

The NFI investigated tree health. This was calculated using a combination of survey data on tree mortality, tree health indicator of crown dieback and tree diseases for a condition calculator.

A Statutory Plant Health Notice (SPHN) is issued to fell diseased trees to prevent the spread of diseases and pests.

| Year | England | Wales | Scotland | Northern Ireland | UK |

|---|---|---|---|---|---|

| 2010 to 2011 | 114 | 46 | 1 | 10 | 171 |

| 2011 to 2012 | 131 | 90 | 14 | 16 | 251 |

| 2012 to 2013 | 168 | 89 | 123 | 15 | 395 |

| 2013 to 2014 | 244 | 272 | 76 | 28 | 620 |

| 2014 to 2015 | 140 | 71 | 9 | 17 | 237 |

| 2015 to 2016 | 73 | 57 | 34 | 3 | 167 |

| 2016 to 2017 | 75 | 53 | 71 | 0 | 199 |

| 2017 to 2018 | 43 | 153 | 71 | 14 | 281 |

| 2018 to 2019 | 136 | 215 | 491 | 0 | 842 |

Download this table Table 3: Number of sites where a Statutory Plant Health Notice has been served, UK, between 2010 to 2011 and 2018 to 2019

.xls .csv

| Year | England | Wales | Scotland | Northern Ireland | UK |

|---|---|---|---|---|---|

| 2010 to 2011 | 1.2 | 0.8 | 0.0 | 0.3 | 2.3 |

| 2011 to 2012 | 0.5 | 0.5 | 0.1 | 0.1 | 1.1 |

| 2012 to 2013 | 0.5 | 1.5 | 0.4 | 0.2 | 2.5 |

| 2013 to 2014 | 0.8 | 4.6 | 0.3 | 0.5 | 6.2 |

| 2014 to 2015 | 0.3 | 0.4 | 0.0 | 0.0 | 0.7 |

| 2015 to 2016 | 0.2 | 1.5 | 0.1 | 0.0 | 1.8 |

| 2016 to 2017 | 0.3 | 0.2 | 0.2 | 0.0 | 0.7 |

| 2017 to 2018 | 0.1 | 1.3 | 0.3 | 0.1 | 1.7 |

| 2018 to 2019 | 0.6 | 1.9 | 1.4 | 0.0 | 3.8 |

Download this table Table 4: Felling areas under Statutory Plant Health Notices, thousand hectares, UK, between 2010 to 2011 and 2018 to 2019

.xls .csvInvasive species are one of the major causes of biodiversity loss. One estimate put the cost of invasive non-native species in the UK at £1.8 billion per year. The NFI estimates 221,723 hectares are classified as unfavourable for invasive species. For example, rhododendron is a prominent invasive species in UK woodlands.

Damage from herbivores may impact biodiversity when there is excessive browsing, especially from deer, as it can impact on natural regeneration. The NFI investigated the damage done by herbivores from browsing and stripping the bark damage and found woodlands classified as unfavourable for grazing and herbivore damage account for 40% of total woodlands (Table 2).

The presence of veteran trees in a woodland is considered a boost to biodiversity as they create unique micro-habitats supporting a wide range of other organisms. Forest Research uses Natural England’s definition of a veteran tree (PDF, 339KB) as “A tree that is of interest biologically, culturally or aesthetically because of its age, size or condition”. The NFI considers a woodland as being in a favourable condition when two or more veteran trees are present per hectare. The inventory only classified 0.5% of all woodland area as favourable for veteran trees (Table 2). However, veteran trees are commonly found outside of woodlands in parklands, hedgerows and wood pasture, which are not currently included as they do not meet the NFI’s classification of a woodland.

Deadwood is important for woodland biodiversity. It provides an important habitat for small animals, cavity-nesting birds, insects dependent on decomposing wood and decomposer fungi. The NFI considers a favourable condition for deadwood to be greater than or equal to 80 cubic metres per hectare for volume of deadwood lying or standing. Of all woodland in Great Britain, 6.1% is considered favourable for deadwood (Table 2).

Certified woodlands

In the UK, certified woodland has been independently audited against the UK Woodland Assurance Standard (UKWAS). One certification scheme is the FSC. In March 2019, 1.4 million hectares of woodland in the UK were FSC certified. This represented 44% of the total UK woodland area and is an increase of 32% since December 2001. To be FSC certified, woodland managers are required to meet certain standards to ensure the forest is being managed in a way that preserves the natural ecosystem. Another scheme is the Programme for the Endorsement of Forest Certification (PEFC). At present, all woodlands in the UK that are certified under PEFC are also certified under FSC.

Access to woodlands

Accessible woodland is an indicator of the ability to supply recreational services to the population. It is defined as “any site that is permissively accessible to the general public for recreational purposes”. The area of accessible woodland increased slightly (0.1%) between the years 2012 to 2016 (Table 5). The estimated percentage of the UK population with access to 20 hectares of woodland within four kilometres of their home also increased, from 61% in 2007 to 74% in 2017.

| Area accessible woodland hectares | % | ||

|---|---|---|---|

| Region | 2012 | 2016 | change |

| England | 382,407 | 397,149 | 3.9 |

| Wales | 121,192 | 120,317 | -0.7 |

| Scotland | 780,484 | 765,204 | -2.0 |

| Northern Ireland | 73,696 | 75,929 | 3.0 |

| UK total | 1,357,779 | 1,358,599 | 0.1 |

Download this table Table 5: Area of recorded accessible woodland, hectares, UK, 2012 and 2016

.xls .csvProtected sites

There are several formal designations, including Special Areas of Conservation (SACs) or Sites of Special Scientific Interest (SSSIs) in Great Britain and Areas of Special Scientific Interest (ASSIs) in Northern Ireland. An SSSI or ASSI is an area of interest to science that has rare fauna or flora present or important geological or physiological features. In Northern Ireland, the area of woodland with a protected site designation of SSSI or ASSI and SAC is 4.4% of total woodland; for Great Britain, this is 8.3% of total woodland.

In 2018, Scottish Natural Heritage identified 50% of its broadleaved, mixed and yew woodland SSSIs and SACs as being in a favourable condition. Of Scotland’s coniferous woodland protected areas, 61% are in favourable condition. There were improvements across all broad woodland types in protected areas from 2007, when only 46% of broadleaved, mixed and yew woodlands were favourable and 53% of coniferous sites were favourable. Scottish investigations by the Joint Nature Conservation Committee (JNCC) revealed no obvious differences in the underlying pressures and issues affecting the condition of coniferous woodlands in comparison with broadleaved woodlands.

The most frequently reported activity for unfavourable condition is over-grazing. Over-grazing leads to a lack of regeneration. Forestry England identified for 2018 to 2019 that 37% of woodland SSSIs are in favourable condition, 61% are in unfavourable recovering conditions and 1% are in unfavourable declining conditions with high deer populations browsing the native flora.

| SAC | SSSI/ASSI | Total | |

|---|---|---|---|

| Broad leaved and mixed | |||

| Favourable condition | 25% | 45% | 43% |

| Monitoring coverage | UK | England, Scotland, Northern Ireland | |

| Coniferous | |||

| Favourable condition | 38% | 55% | 50% |

| Monitoring coverage | Scotland only | Scotland only |

Download this table Table 6: Summary statistics for protected sites for broadleaved and mixed woodlands for the UK and coniferous woodlands for Scotland, 2005

.xls .csvOnly 25% of the reported SAC features were in a favourable condition in 2005 for the UK broadleaved and mixed woodlands, and 38% of the coniferous SACs in Scotland were in a favourable condition (Table 6).

Pressure indicators

Pressure indicators are defined here as damage inflicted on woodlands by humans. We can report on litter, fly tipping, dog fouling, vandalism and farm waste. Wildfires can also be considered a pressure indicator; most UK wildfires are started by people, with and without intent.

Wildfires are increasingly in the news worldwide as climate change leads to hotter and drier springs and summers. In some parts of the world, fire has long been an important part of natural and human ecological management. This is especially true for woodlands. However, in the UK woodlands, fires almost all have negative impacts.

Most UK wildfires are set by humans rather than natural. The vast majority of UK wildfires occur in open landscapes. Most of the prominent wildfires in recent years within the UK have occurred on mountains, moors, heaths and grasslands.

Climate change is expected to increase the number of woodland wildfires in the UK. Management of forests is being adapted to cope with this, including more broken up planting, training of fire services and species changes.

There are two main sources of data on wildfires: reported fires and satellite data. Reported fires catch wildfires of all sizes attended by England’s Fire and Rescue Services but may miss some remote fires that are addressed by land managers. Satellite data capture fires in both built up and remote places but might miss smaller fires under 30 hectares. Forestry Commission estimates (PDF, 275KB) of woodland fires are based on reported data from incidents attended by Fire and Rescue Services and so may miss some remote fires. EU-wide reporting on overall forest wildfires is based on satellite data. For this reason, the two datasets are not directly relatable, but comparison can be useful (Table 7).

Satellite data for the most recent years in the UK saw an apparent increase in the number and area of burning incidents. The two datasets appear to show some correlation for wildfires in earlier years and later years with the correlation of mild winters with higher temperatures, heatwaves, and prolonged dry periods across spring and summer. Periods of low wildfires correlate with heavy periods of rainfall in spring and summer as well as wetter winters. A large number of small fires are excluded from the European Forest Fire Information System (EFFIS), meaning the number of fires is smaller.

| FC Woodland Fires England | EFFIS recorded Fires UK | |||

|---|---|---|---|---|

| Year | Number | Area hectares | Number | Area hectares |

| 2010 to 11 | 7,986 | 1,276 | 0 | 0 |

| 2011 to 12 | 8,917 | 8,675 | 44 | 17,197 |

| 2012 to 13 | 2,454 | 423 | 0 | 0 |

| 2013 to 14 | 5,058 | 1,508 | 16 | 5,445 |

| 2014 to 15 | 3,138 | 881 | 1 | 85 |

| 2015 to 16 | 5,067 | 1,410 | 4 | 2,127 |

| 2016 to 17 | 4,186 | 804 | 9 | 1,197 |

| 2017 to 18 | 19 | 5,126 | ||

| 2018 to 19 | 79 | 18,031 | ||

| 2019 to 20 | 137 | 29,396 | ||

Download this table Table 7: The total area of woodland fires in both datasets appear to correlate with woodland fires increasing in size, England and UK, between 2010 to 2011 and 2019 to 2020

.xls .csv4. Overall quantity and value of woodland ecosystem services

This section assesses the contribution woodland services provide to the economy and society.

| Type service | Provisioning | Regulating | Cultural | ||||

|---|---|---|---|---|---|---|---|

| Year | Timber | Woodfuel | Carbon Sequestration | Pollution removal | Noise reduction | Recreation | Recreation |

| Total fellings (000's m3 overbark standing) | Million tonnes | Thousand tonnes | Number buildings benefited 000s | Visits (millions) | Time at habitat (million hours) | ||

| 2010 | 10,363 | 1,544 | 19 | 274 | 356 | 388 | |

| 2011 | 11,345 | 1,544 | 19 | 273 | 371 | 414 | |

| 2012 | 11,263 | 1,666 | 17 | 277 | 370 | 492 | |

| 2013 | 11,983 | 1,972 | 18 | 278 | 399 | 496 | |

| 2014 | 12,405 | 2,277 | 18 | 277 | 435 | 564 | |

| 2015 | 11,255 | 2,400 | 18 | 273 | 448 | 544 | |

| 2016 | 11,455 | 2,339 | 18 | 271 | 466 | 655 | |

| 2017 | 11,564 | 2,622 | 18 | 269 | 167 | 475 | 718 |

Download this table Table 8: Woodland annual physical flow by service, UK, 2010 to 2017

.xls .csvThe value of woodland ecosystem services was estimated at £3.3 billion in 2017 (Figure 8). Data are only available for the seven ecosystem services annual valuations in 2017. This is a partial valuation with potentially significant exclusions such as food and Christmas trees.

Figure 8: Woodland ecosystems services were valued at £3.3 billion in 2017

Annual values woodland ecosystem services, UK, 2010 to 2018

Source: Office for National Statistics – Woodland natural capital accounts

Download this chart Figure 8: Woodland ecosystems services were valued at £3.3 billion in 2017

Image .csv .xls5. Provisioning ecosystem services: quantity and value

Provisioning ecosystem services creates products. Within woodlands, these products include timber, food and bioenergy sources.

Timber fellings

Between 2000 and 2018, there was a 51% increase in timber production (Figure 9), with 14,797,496m3 overbark standing timber fellings in 2018.

Figure 9: There was a 51% increase in timber production between 2000 and 2018

Total timber fellings, UK, 1976 to 2018

Source: Forestry Commission – Forestry Statistics 2019

Download this chart Figure 9: There was a 51% increase in timber production between 2000 and 2018

Image .csv .xlsScottish production has driven the UK trend, with production increasing 72% between 2000 and 2018 (Figure 9). In 2018, 62% of timber was sourced from Scotland, 23% from England, 11% from Wales and 3% from Northern Ireland.

Figure 10: Timber production in the UK increased in recent years caused by a rise in private timber production

Total timber fellings by public and private sector, UK, 1976 to 2018

Source: Forestry Commission – Forestry Statistics 2019

Notes:

- Hardwood includes broadleaved trees such as oak, birch and beech.

- Softwood includes coniferous trees such as spruce, pine and larch.

Download this chart Figure 10: Timber production in the UK increased in recent years caused by a rise in private timber production

Image .csv .xlsPrivate sector production has driven much of the increase in timber fellings. In 2000, 62% of timber came from the public sector; this reduced to 38% in 2018 (Figure 10). The change is primarily because of differences in the age structure and timing of timber production between woodlands on the public and private forest estates. This is a result of a period of high levels of planting by the private sector in Scotland between 1970 and the late 1980s. The proportion of timber that is softwood and hardwood has remained fairly constant. In 2000, 93% of timber removed was softwood, rising to 94% in 2018.

Figure 11: Woodfuel increased to 21% of total timber in 2018

Total fellings showing proportion wood fuel, UK, 2000 to 2018

Source: Forestry Commission – Forestry Statistics 2019

Download this chart Figure 11: Woodfuel increased to 21% of total timber in 2018

Image .csv .xlsThe proportion of timber used for wood fuel increased from 3% in 2000 to 21% in 2018 (Figure 11). However, data collection methods have improved, and this may account for some of the increase. The other uses of wood processors include wood-based panel mills, pulp, paper mills and exports.

Figure 12: With increasing removals and increasing prices, timber had a series high in 2018

Timber provisioning excluding wood fuel annual value, UK, 2000 to 2018

Source: Forestry Commission – Forestry Statistics 2019

Download this chart Figure 12: With increasing removals and increasing prices, timber had a series high in 2018

Image .csv .xlsFigure 12 shows the value of timber excluding that which is used for wood fuel; this is presented in the following Energy: wood fuel subsection. The annual value of timber had a series high in 2018 at £288 million. Fluctuations in value were because of changes in stumpage price. The stumpage price is the price paid per standing tree for the right to harvest it. Using projected timber removals over the next 100 years, the asset valuation of the timber provisioning service excluding wood fuel reached £8 billion in 2018. Observing recent trends and Forestry Commission forecasts, valuations are expected to increase in the coming years as timber price and production continues to grow.

Energy: wood fuel

Energy from fuels created directly from plant matter or waste food are referred to as biofuels and are part of the renewable energy ecosystem service. Wood makes up a significant part of the market in biofuels in the UK, being used in domestic fires, modern pellet-burning boilers and even large electricity-generating power stations. In 2018, the generation of electricity from bioenergy, including wood fuel, accounted for 31.6% of renewable electricity generation.

Since the mid-2000s, there has been an increase in the amount of timber used for wood fuel (Figure 11). Deliveries of UK-grown softwood and hardwood timber for wood fuels rose from 289 thousand cubic metres (2.9% of total timber) in 2000 to 3,100 thousand cubic metres (20.9% of total timber) in 2018. One of the reasons for the increase could be the UK Government’s Renewable Heat Incentive (RHI), which started in 2014 and provided a financial incentive for renewable heat generated.

Figure 13: With increasing removals and price rises, the value of wood fuel continues to rise

The annual value of the total timber sold as wood fuel, UK, 2000 to 2018

Source: Forestry Commission – Forestry Statistics 2019

Download this chart Figure 13: With increasing removals and price rises, the value of wood fuel continues to rise

Image .csv .xlsThe annual value for timber used for biofuels rose significantly between 2000 and 2018, from £3.3 million to £76.4 million (a series high) (Figure 13). Using projected timber removals over the next 100 years, the asset valuation of the timber-provisioning service for wood fuel reached £2 billion in 2018.

Bioenergy has been increasing steadily since 2011. New wood-burning power plants are opening to supply increased demand, the largest being Lynemouth Power Station, a former coal-powered station that was converted to a wood-burning power plant in 2018. As biofuels are transportable, there is a significant proportion of wood pellets being imported, as the demand for wood fuel far exceeds supply in the UK. For example, Drax, which has four biomass power plants in the UK, reported using 7,171,074 tonnes of biomass pellet feedstock in 2018 with only 1% (47,740 tonnes) being sourced from the UK. Of their wood fuel, 99% is imported with 62% comes from the USA.

Food

Trees can both produce food directly (such as apples) and form an active part of farms in practices known as agroforestry, in which trees can be combined with livestock, crops or mixed farming. Supporters of this approach state that this land management approach has benefits that include increasing wildlife, enhancing soil health, improving animal welfare and contributing to climate change mitigation through sequestering of carbon. In the UK, this includes hedgerows and buffer strips, silvoarable cropping where alleys of trees are grown on arable land, and silvopasture where there is a mix of trees and livestock (the trees provide shade and shelter for the grazing livestock).

The Department for Environment, Food and Rural Affairs (Defra) estimates there are 551,700 hectares of agroforestry in the UK, based on a very broad definition. Livestock agroforestry is the largest area of agroforestry, at 547,600 hectares, where there is a mix of trees and livestock (Table 9). Included in the Defra estimate for livestock agroforestry are 50,700 hectares of shrubland with sparse tree cover and 239,300 hectares of grassland with sparse tree cover. Full methodology can be found in the AGFORWARD report.

| Type agroforestry | Area thousand hectares | % land area |

|---|---|---|

| Arable | 2.0 | 0.0 |

| Livestock | 547.6 | 3.3 |

| High value tree | 14.2 | 0.1 |

| Total | 551.7 | 3.3 |

Download this table Table 9: The vast majority of existing uptake in the UK is agroforestry associated with livestock

.xls .csvOne proxy used by the Committee on Climate Change (CCC) on areas of agroforestry is the use of hedges and trees for buffer strips. Around 1% of agricultural land is estimated to be hedgerows in the UK.

How we include food from agroforestry in these accounts will require some thought and methodological development. For example, we note that The Agroforestry Handbook includes potential net revenue gains for swapping conventional farming to selected agroforestry schemes. We need to consider whether the full food production from agroforestry is appropriate or merely the potential uplift from the regulating service provided by trees.

Woodlands also contain wild foods such as mushrooms, fruit and foliage that are harvested on a non-commercial and commercial basis. Research in Scotland found that around 200 different non-timber forest products are sourced from woodlands, with 110 being edible. Other products included those for craft and medicinal use. The wild food is mainly being used by the gatherers for their households. Owing to the free nature of these foraging products, it is difficult to assess their value. However, there is a small number of gatherers who make an income from this activity.

Game from hunting provides both food and recreation. Scottish research suggests approximately a quarter of red deer live in woodland. According to a Public and Corporate Economic Consultants (PACEC) 2014 survey, out of 1.8 million hectares of land managed for shooting purposes, 500,000 hectares are woodland. From 1,110 sites sampled in 2012 to 2013, on average the typical area of a hunting site that is woodland is 22%. The survey suggested 184,000 deer were shot in 2012 to 2013 in the UK across all habitats, including woodland. The PACEC survey suggests on average 97% of all game shot was destined for the food chain, from a sample of 1,050 providers. The PACEC report states that there is a small amount of income from the venison market but that this will rarely be enough to cover the costs of hunting. Forestry England also state that because of the variation in the price of venison, the costs of wildlife management exceed any income received in some years. For this reason, we are not actively developing game as a monetary account but will continue to look for overall production data.

Christmas trees

It is estimated that there are approximately 320 Christmas tree suppliers in the UK, selling around 7 million trees annually according to the British Christmas Tree Growers Association (BCTGA). The BCTGA has also stated that the Christmas tree market was worth £7 million as of 1980, but there are no current data on the value of the market as at 2019. We found no verifiable data on the number of Christmas trees grown in the UK.

Nôl i'r tabl cynnwys6. Regulating ecosystem services: quantity and value

This section discusses the benefits provided by the regulation of natural processes, including air quality regulation, climate regulation, and natural hazard regulation such as flood mitigation.

Carbon sequestration

The amount of carbon sequestrated by UK woodland was greater between 1998 to 2010 but fell in 2012 and has not recovered to 2011 levels (Figure 14). According to the UK Greenhouse Gas Inventory annual report, the variation in the net sink is caused by afforestation in earlier decades and the effect on the age structure of the present forest area, particularly conifer plantations. There were high levels of conifer afforestation between 1950 and 1990, but these forests are now reaching harvesting age; this means the older trees are replaced by younger trees, which have a much lower rate of carbon absorption.

Figure 14: Harvesting of forests lead to lower levels of carbon sequestrated by UK woodland in the last decade relative to 2000 to 2009

Carbon sequestration by woodland, UK, 1998 to 2017

Source: National Atmospheric Emissions Inventory

Download this chart Figure 14: Harvesting of forests lead to lower levels of carbon sequestrated by UK woodland in the last decade relative to 2000 to 2009

Image .csv .xlsDespite carbon sequestration reducing over the time series, the annual value of the service has generally increased year-on-year between 1998 and 2017, reaching a high of £1.2 billion in 2017 (Figure 15).

Figure 15: The annual value of carbon sequestration by woodland in the UK reached a peak of £1.2 billion in 2017

Annual value of carbon sequestered by woodlands, UK, 1998 to 2017

Source: Office for National Statistics – Woodland natural capital accounts; National Atmospheric Emissions Inventory

Download this chart Figure 15: The annual value of carbon sequestration by woodland in the UK reached a peak of £1.2 billion in 2017

Image .csv .xlsThis is because of increases in the non-traded carbon prices, which are estimated to keep increasing until 2080. Consequently, the asset value of carbon sequestration by UK woodland was estimated to increase year on year, reaching £54.6 billion in 2017.

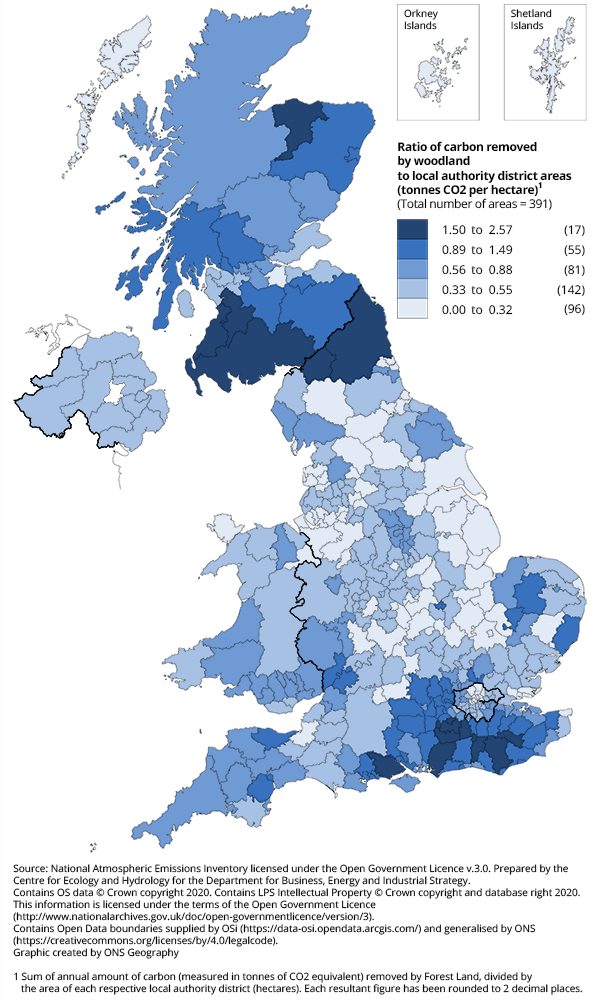

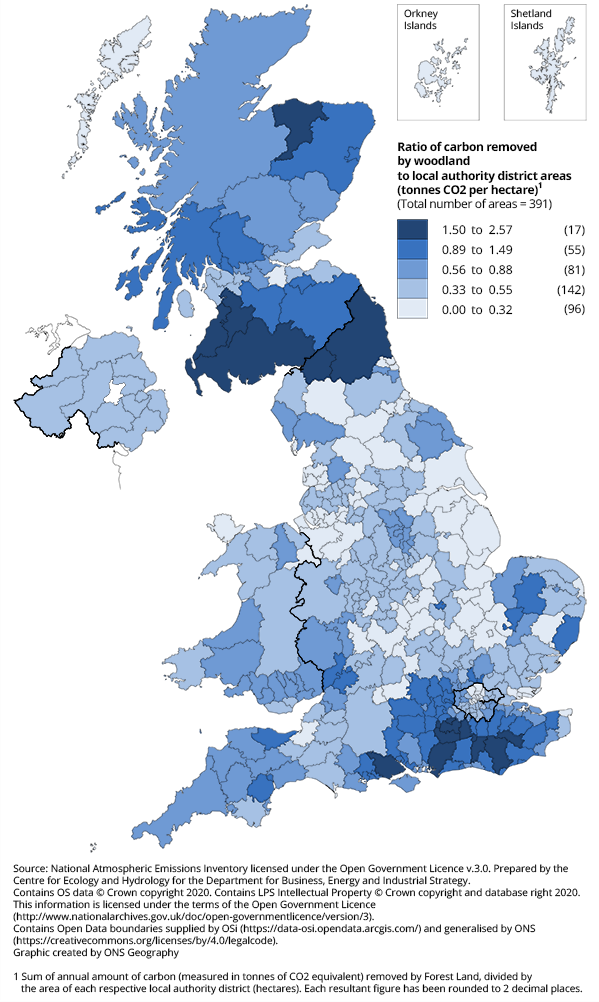

Figure 16: From the top 17 local authorities that sequestrated 1.5 tonnes CO2 per hectare or greater in 2017, 13 of them were in England

Ratio of the forest carbon sink to the local authority area, UK, 2017

Source: National Atmospheric Emissions Inventory – prepared by the Centre for Ecology and Hydrology for the Department for Business, Energy and Industrial Strategy

Download this image Figure 16: From the top 17 local authorities that sequestrated 1.5 tonnes CO2 per hectare or greater in 2017, 13 of them were in England

.png (307.9 kB){kind=link}

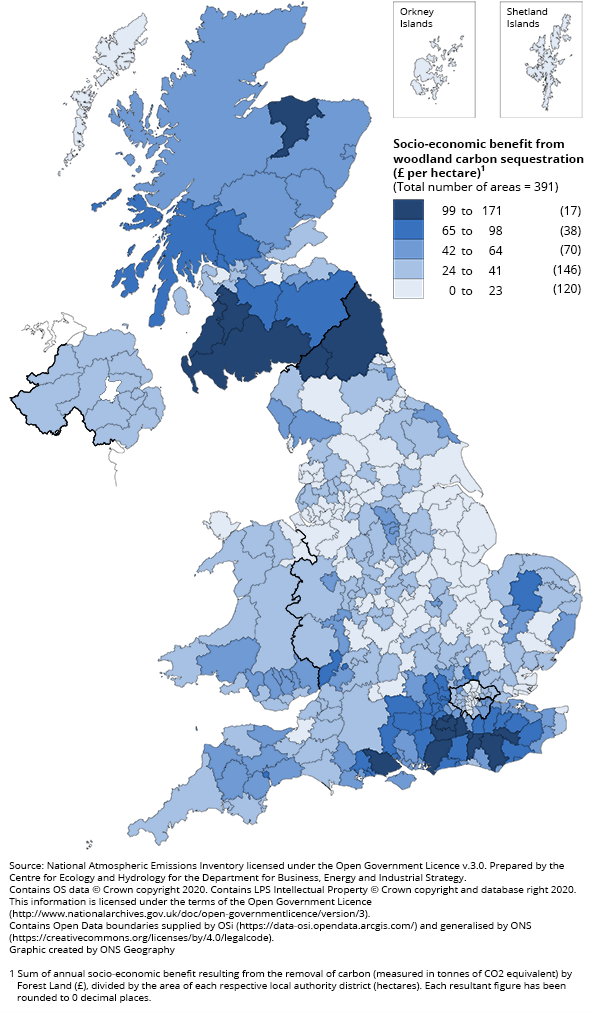

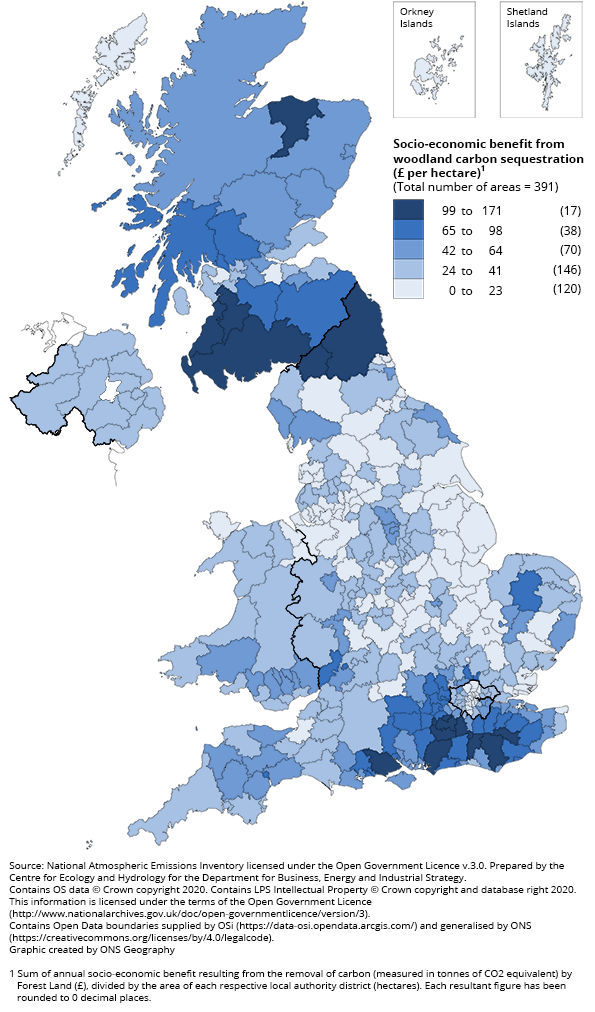

We can also look at which local authorities in the UK provide the greatest amount of carbon sequestration from woodland per hectare (Figure 16). From the top 17 local authorities that sequestrated 1.5 tonnes CO2 per hectare or greater in 2017, 4 of them were in Scotland and 13 of them were in England. The ratio of woodland sequestration to the local authority area in 2017 was highest in South Ayrshire in Scotland (2.57 tonnes of CO2 equivalent by hectare), this equated to a value of £170 per hectare in 2017.

Figure 17: South Ayrshire benefitted the most from carbon removal during 2017 (based on the amount of carbon removed per hectare of local authority)

Socio-economic benefit from woodland carbon sequestration per unit area of local authorities (£ per hectare), UK, 2017

Source: National Atmospheric Emissions Inventory – prepared by the Centre for Ecology and Hydrology for the Department for Business, Energy and Industrial Strategy

Download this image Figure 17: South Ayrshire benefitted the most from carbon removal during 2017 (based on the amount of carbon removed per hectare of local authority)

.png (298.2 kB){kind=link}

To show the importance of woodland, we can look at the amount of carbon that is released into the atmosphere from forest land being converted into different land types such as cropland, grassland and settlements. From the UK Greenhouse Gas Inventory, we can see that owing to woodland being converted into cropland, grassland and settlement, 1.4 million tonnes of carbon dioxide were emitted into the atmosphere in 2017 equating to a negative externality (cost) of £94.1 million.

Air pollution removal

In 2017, the removal of pollution by woodland in the UK equated to a saving of £938 million in health costs.

The World Health Organization (WHO) estimated that air pollution contributed to 7.6% of all deaths in 2016 worldwide. Vegetation can play a useful role in lessening this danger by removing air pollution. Polluting gases are absorbed by leaves’ stomata, and particulate matter, suspended in polluted air, settles onto leaves.

This physical flow account estimates the quantity of pollutants removed from the atmosphere by woodland. An annual time series from 2007 to 2017 is available in the Data section.

In 2017, woodland in the UK removed 268.7 thousand tonnes of PM10, SO2, NO, NH3 and O3 (excludes PM2.5 as a subset of PM10) (Figure 18). Ground-level ozone (O3) represented the majority of total pollution removal by mass (79%) in 2017, with PM10 the second largest.

Figure 18: Ground level ozone represents the majority of pollutants removed by woodland

Pollution removal, UK, 2017

Source: Office for National Statistics – Woodland natural capital accounts; Centre for Ecology and Hydrology

Download this chart Figure 18: Ground level ozone represents the majority of pollutants removed by woodland

Image .csv .xlsIt is estimated that in 2017, the avoided health costs in the form of avoided deaths, avoided life years lost, fewer respiratory hospital admissions and fewer cardiovascular hospital admissions from the removal of harmful pollutants amounted to a substantial £938 million (Figure 19). Although the removal of PM2.5 represents only 7% of the total mass of pollutants removed, the majority (97%) of the avoided health impacts are because of the reductions in PM2.5 concentrations.

This is because PM2.5 (fine particulate matter with a diameter of less than 2.5 micrometres, or 3% of the diameter of a human hair) is the most harmful pollutant by mass. PM2.5 can bypass the nose and throat to penetrate deep into the lungs, leading to potentially serious health effects and healthcare costs.

Figure 19: The removal of PM2.5 by woodland in the UK made up 97% of total avoided health costs in 2017 owing to air pollutant removal

Avoided health costs from the removal of pollutants, UK, 2017

Source: Office for National Statistics – Woodland natural capital accounts; Centre for Ecology and Hydrology

Download this chart Figure 19: The removal of PM2.5 by woodland in the UK made up 97% of total avoided health costs in 2017 owing to air pollutant removal

Image .csv .xlsThe present long-term asset value of woodlands calculated over a 100-year period with income uplift and population growth was £31.7 billion in 2017 (2018 price base).

Flood mitigation

Forests are known to reduce flood flows, according to a systemic review done by the UK Centre for Ecology and Hydrology, which looked at 71 studies. There is broad support for the conclusion that increased tree cover in catchments results in decreasing flood peaks, while decreased tree cover results in increasing flood peaks. Therefore, woodlands reducing the risk of a flood can be captured as a regulating ecosystem service.

To capture the flood regulating service for woodland in Great Britain, Forest Research examined how much it would cost to have flood water storage (that is, reservoirs) in an area where there was no woodland; they looked at the substitution costs of having no woodland. For more information on the method, see the methodology report.

An annual average was estimated at £218.5 million per year for Great Britain: it would cost an estimated £218.5 million per year to create reservoirs able to capture that water if woodland in flood risk catchment (FRC) areas were replaced with grassland. In this study, 83% of the land area in Great Britain fell within a FRC area. The country with the largest annual value was England (£139.6 million), owing to the country having more people and settlements at risk of flooding. Some areas in Scotland were not included in the study as they were not deemed as FRC areas. The total Great Britain asset valuation of this service over 100 years equated to £6,513 million. However, there are a number of caveats with this calculation. For all limitations with this research, see the methodology report.

Temperature regulation

Woodlands can cool urban environments, which benefits the economy by avoiding labour productivity losses and reducing the use of artificial cooling, such as air conditioning.

Economics for the Environment Consultancy (EFTEC) and others estimated in 2018 the cooling effect provided by woodlands for 11 city regions across Great Britain in Scoping UK Urban Natural Capital Accounts: Extension to develop temperature regulation estimates (PDF, 834KB). The aggregate cooling effect varies between 0.15 and 0.39 degrees Celsius (Figure 20). This variation is because of the amount of woodland relative to the size of the city region; this is why Scottish regions have the highest cooling effects of all city regions.

Figure 20: Edinburgh city region observed the greatest cooling effect owing to the region having the greatest amount of woodland relative to the size of the urban area

Average annual cooling effect of woodland in each of Great Britain’s city regions, 2014 to 2018

Source: EFTEC and others – Scoping UK Urban Natural Capital Account

Download this chart Figure 20: Edinburgh city region observed the greatest cooling effect owing to the region having the greatest amount of woodland relative to the size of the urban area

Image .csv .xlsThe cooling effect is valued through the estimated cost savings from air conditioning and the benefit from improved labour productivity. The benefit from improved labour productivity makes up most of the value, with avoided air conditioning energy costs only accounting for a small fraction. For more information on the method, see the Methodology section of the EFTEC and others 2018 report (PDF, 834KB).

London gains the most as it has the biggest economy and the greatest number of hot days (22.9 days out of a total of 67.6 hot days in 2018, as seen in Table 10). “Hot days” throughout this section refers to any days equal to or between 28 degrees Celsius and 35 degrees Celsius.

The £141.2 million increase in value from 2017 to 2018 was caused by a threefold increase in hot days from 2016 (Table 10). The London city region, the largest economy in this study, saw 22.9 hot days in 2018, more than double the 8.2 hot days experienced in 2016. Also, the Scottish regions of Edinburgh and Glasgow went from having 0 hot days and therefore no avoided costs in 2017 to having a joint total of 1.5 hot days and £1.3 million in avoided costs in 2018. While most city regions saw a significant increase in their annual value over the two years, the North East was the only region to experience fewer hot days.

| City region | Number of hot days | ||

|---|---|---|---|

| 2016 | 2017 | 2018 | |

| Cardiff | 1.3 | 3.1 | 5.0 |

| Edinburgh | 0.2 | 0.0 | 0.5 |

| Glasgow | 0.2 | 0.0 | 1.0 |

| Greater Manchester | 1.0 | 0.9 | 4.3 |

| Liverpool | 1.0 | 2.2 | 6.2 |

| London | 8.2 | 7.4 | 22.9 |

| North East | 0.4 | 0.0 | 0.1 |

| Sheffield | 2.4 | 1.9 | 5.7 |

| West Midlands | 2.8 | 4.6 | 10.6 |

| West of England | 1.6 | 4.6 | 8.5 |

| West Yorkshire | 1.1 | 1.0 | 2.8 |

| Total | 20.2 | 25.7 | 67.6 |

Download this table Table 10: The number of hot days increased significantly in 2018 to 67.6 days over the 11 city regions

.xls .csv

| City region | Avoided costs | ||

|---|---|---|---|

| 2016 | 2017 | 2018 | |

| Cardiff | 1,195 | 1,812 | 1,448 |

| Edinburgh | 119 | - | 185 |

| Glasgow | 146 | - | 1,118 |

| Greater Manchester | 2,692 | 636 | 3,164 |

| Liverpool | 1,203 | 379 | 1,282 |

| London | 84,776 | 74,681 | 205,328 |

| North East | 108 | 27 | 33 |

| Sheffield | 1,209 | 1,122 | 2,713 |

| West Midlands | 4,116 | 5,140 | 8,228 |

| West of England | 1,607 | 3,483 | 2,967 |

| West Yorkshire | 1,723 | 725 | 2,675 |

| Total | 98,894 | 88,005 | 229,141 |

Download this table Table 11: The total annual value of cooling from urban woodland in 2018 was valued at £229.2 million

.xls .csvThe total asset value increased by 54% from £4 billion to £6.1 billion between the 2012 to 2016 and 2014 to 2018 five-year averages (Figure 21). The number of hot days had significantly increased by 47 days.

Figure 21: The asset value of the urban cooling effect increased between the 2016 and 2018 averages by 54% owing to a rise in the number of hot days

Total asset value of the environmental assets for each city region in Great Britain over three five-year averages, 2012 to 2018

Source: EFTEC and others – Scoping UK Urban Natural Capital Account; Met Office

Download this chart Figure 21: The asset value of the urban cooling effect increased between the 2016 and 2018 averages by 54% owing to a rise in the number of hot days

Image .csv .xlsWe can now examine the potential productivity benefits of converting one percentage point of the urban area into woodland. An increase in woodland by one percentage point in all city regions (relative to the urban area) could lead to an estimated saving in labour productivity of at least £12.8 million. These numbers are calculated using the five-year hot-day average (2014 to 2018). As expected, we have seen an increase of just over £3 million from the previous five-year hot-day average (2013 to 2017) owing to the progress of climate change.

| City region | Avoided labour productivity costs | |

|---|---|---|

| 2013 to 2017 | 2014 to 2018 | |

| Cardiff | 115,480 | 126,540 |

| Edinburgh | 4,470 | 4,730 |

| Glasgow | 5,180 | 28,330 |

| Greater Manchester | 196,750 | 249,170 |

| Liverpool | 91,850 | 128,430 |

| London | 7,784,330 | 10,988,470 |

| North East | 9,010 | 7,890 |

| Sheffield | 131,430 | 173,860 |

| West Midlands | 589,130 | 640,630 |

| West of England | 261,650 | 280,500 |

| West Yorkshire | 137,190 | 172,190 |

| Total | 9,326,470 | 12,800,740 |

Download this table Table 12: A one percentage point rise in woodland relative to the urban area can lead to an overall saving in labour productivity of at least £12.8 million in 2018

.xls .csvNoise reduction

Vegetation acts as a buffer against noise pollution, in particular road traffic noise. Noise pollution causes adverse health outcomes through lack of sleep and annoyance. EFTEC and others reported in 2018 (PDF, 834KB) initial estimates of the benefits of noise reduction from vegetation, which just includes woodland. Urban vegetation includes both large (greater than 3,000 square metres) and smaller (less than 3,000 square metres) woodlands but does not include very small woodlands (less than 200 square metres).

These estimates are considered minimum values, but further work is needed to develop more refined and robust estimates. According to the noise action plan in urban areas published by the Department for Environment, Food and Rural Areas (Defra), 8,022,000 people were in agglomerations where road traffic was greater than 60 decibels. An example of sound that produces 60 decibels or more is normal speech. These are considered minimum values, but further work is needed to develop more refined estimates.

The total number of buildings in UK urban areas that benefitted from a reduction in noise in 2017 was 167,000.

| Noise band in noise metric by decibel | Number of buildings benefiting from noise mitigation by urban vegetation (rounded to the nearest thousand) | ||||

|---|---|---|---|---|---|

| England | Scotland | Wales | Northern Ireland | UK | |

| Greater than or equal to 80 | - | - | - | - | 0 |

| 75.0 to 79.9 | 1,000 | - | - | - | 1,000 |

| 70.0 to 74.9 | 8,000 | - | 1,000 | - | 9,000 |

| 65.0 to 69.9 | 36,000 | 1,000 | 3,000 | 1,000 | 41,000 |

| 60.0 to 64.9 | 98,000 | 6,000 | 8,000 | 4,000 | 116,000 |

| Total | 143,000 | 7,000 | 12,000 | 5,000 | 167,000 |

Download this table Table 13: 167,000 buildings in the UK benefited from noise reduction owing to woodland

.xls .csvThe total annual value of noise reduction in the UK was £15.3 million in avoided loss of quality adjusted life years (QALY) during 2017 (Table 14). Valuations based on QALY are economic welfare values, which look into how noise reduction affects people’s social welfare.

| Noise band | Annual value of noise mitigation of 1dBA (£ million) | ||||

|---|---|---|---|---|---|

| England | Scotland | Wales | Northern Ireland | UK | |

| Greater than or equal to 80 | 1,000 | - | - | - | 1,000 |

| 75.0 to 79.9 | 148,000 | - | 11,000 | 2,000 | 161,000 |

| 70.0 to 74.9 | 1,104,000 | 8,000 | 106,000 | 56,000 | 1,274,000 |

| 65.0 to 69.9 | 4,026,000 | 124,000 | 313,000 | 141,000 | 4,604,000 |

| 60.0 to 64.9 | 7,778,000 | 481,000 | 672,000 | 324,000 | 9,255,000 |

| 55.0 to 59.9 | - | - | - | - | 0 |

| 50.0 to 54.9 | - | - | - | - | 0 |

| 45.0 to 49.9 | - | - | - | - | 0 |

| Total | 13,057,000 | 613,000 | 1,102,000 | 523,000 | 15,295,000 |

Download this table Table 14: Noise mitigation provided by small woodlands in the UK led to a saving of £15.3 million in avoided loss of quality adjusted years associated with adverse health outcomes

.xls .csvThe asset value for noise reduction based on estimated future benefits over 100 years was worth £833 million (Table 15). A number of assumptions are also made when estimating the future flow of the noise mitigation value by urban vegetation and woodland. For more information on these, see Scoping UK Urban Natural Capital Account – Noise extension (PDF, 2.37MB).

| Noise band | Annual value of noise mitigation of 1dBA (£million/year) | ||||

|---|---|---|---|---|---|

| England | Scotland | Wales | Northern Ireland | UK | |

| Greater than or equal to 80 | - | - | - | - | 0 |

| 75.0 to 79.9 | 8 | - | 1 | - | 9 |

| 70.0 to 74.9 | 60 | - | 6 | 3 | 69 |

| 65.0 to 69.9 | 219 | 7 | 17 | 8 | 251 |

| 60.0 to 64.9 | 423 | 26 | 37 | 18 | 504 |

| Total | 710 | 33 | 61 | 29 | 833 |

Download this table Table 15: The asset value for noise regulation in England provided by urban woodland had an estimated worth of £710 million in 2017

.xls .csv7. Cultural ecosystem services: quantity and value

Cultural ecosystem services provide non-material benefits like enjoyment of the landscape, recreation in woodlands, education and cultural heritage.

Recreation

In 2017, there were an estimated 475.2 million visits to and 718 million hours spent in UK woodlands. This service was valued at £515.5 million. Recreational visits in nature are valued based on expenditure per trip (that is, fuel, public transport costs, admission costs and parking fees). For more information on how we calculate the annual value, see Woodland natural capital accounts methodology guide, UK: 2020. Visits and time spent in woodland areas have generally gradually increased over the time series, with an especially steep increase in the average time spent in woodland habitat from 2015 to 2017 (Figure 22).

Figure 22: Visits to UK woodlands have increased by 39% since 2009

Number of visits and hours spent in woodlands, UK, 2009 to 2017

Source: Monitor of Engagement with the Natural Environment Survey, The Welsh Outdoor Recreation Survey, and Scotland’s People and Nature Survey

Download this chart Figure 22: Visits to UK woodlands have increased by 39% since 2009

Image .csv .xlsThe reason behind the steep increase seen in Figure 22 is a combination of increases in both travel times to and from woodland sites and the time spent within the habitat. Time spent within the habitat has increased by 165 million hours over the period of 2015 to 2017. Forestry England identified that 99.9% of England’s population are within 60 minutes’ drive time to access one of their forests or woodlands and 48.4% of the population are within six miles of Forestry England land, as of 2018 to 2019. The UK 2019 Public Opinion of Forestry survey had 63% of respondents saying they had visited woodlands in the last few years for recreational use, including walking and picnics.

Much of the fluctuation in woodland values are because of data limitations. Further information on these can be found in Woodland natural capital accounts methodology guide, UK: 2020.

Looking at the country breakdown, visits to woodland in England made up on average two-thirds of all trips in the UK. Visits to woodland in Scotland and Wales made up similar proportions of the total UK average, with both averaging 15% of total UK woodland trips over the time series. English woodland visits are valued at £362.2 million, Scottish woodland visits at £63 million and Welsh woodland visits at £79 million.

As explained in Woodland natural capital accounts methodology guide, UK: 2020, Great Britain data are scaled up for the UK. Currently, the only available data for Northern Ireland are information from Forest Service Northern Ireland where they collect data on sites where there is an admission charge. There were 532,000 visits to Forest Service sites with admission charges in Northern Ireland in 2018 to 2019.

Woodlands have become more accessible to the population for recreation purposes (Table 5), with 1.4 million hectares accessible in the UK in 2016. It is estimated for 2017 that 74% of the UK population had woodlands 20 hectares or greater in size within 4km of their home.

Education

The natural world provides a wide range of opportunities for education, but this service tends to receive less attention in natural capital analyses owing to data and valuation challenges. The Office for National Statistics (ONS) has begun the process of collating outdoor activity data but can currently only provide a qualitative overview. There are a wide range of providers of outdoor education in woodlands – from specialists like forest schools to individual lessons run by groups and educators using free resources provided by organisations such as the Woodland Trust.

Forest schooling is a specialised learning approach that occurs within outdoor environments, specifically woodlands. The Forest School Association (FSA) offers training to teachers and other professionals to aid them in implementing this approach into students’ schooling.

The FSA is a part of the Institute for Outdoor Learning (IOL), the professional body for those who conduct learning in the outdoors. The IOL has over 600 organisational members and over 1,000 individual members.

The Woodland Trust offers “the Green Tree Schools Award” to encourage primary and secondary schools to take part in projects that help the environment. So far, more than 12,000 UK schools have taken part. The Woodland Trust also states that outdoor learning can boost the physical and mental health of children taking part.

In 2019, the Bringing Children Closer to Nature survey was published by the Sylva Foundation, based mainly in England with a few respondents located in the rest of the UK. It focused on how barriers to children being able to take part in outdoor education, particularly forest schooling, can be overcome. Over 1,000 people took part, including both school and non-school educators along with private woodland owners. Most of the education taking place is aimed at those aged 0 to 5 years old, with the biggest barrier mentioned being the funding available for establishing and sustaining forest schools. This explains why the older the student becomes, the less likely they are to be taking part in forest school practices.

The Northern Ireland Forest School Association (NIFSA) also has 54 qualified and 183 trainee schools in their forest school programme, from 2016 (when their Forest School Awards began) to February 2020.

Future research is needed to get total numbers participating in forest schools in the UK and the value of the ecosystem service it provides, to be included in future publications.

Science

We are continuing to develop our estimates on scientific research in UK woodlands. This is the value of “what scientific examination of woodlands can teach us”. Research into woodlands could provide a range of benefits. It could help us to solve major scientific questions, answer fundamental questions about how the world works, or lead to innovations in industry. Woodlands can also provide useful training opportunities for postgraduate students and future researchers.

One way of estimating the value of scientific research is through estimating the value of research grants awarded. We source data on publicly funded research grants from the UK Research and Innovation (UKRI) gateway. Table 16 shows funding grants for research on UK woodlands from 2006 to 2019, as of 17 December 2019. Grant funding appears to peak in 2015, but we only include allocated spend.

We do not know when grant amounts are paid for every year and which deflators to use. Values reported under scientific research are therefore nominal.

| Year | Amount spent on publicly funded research (£) |

|---|---|

| 2006 | 30,301 |

| 2007 | 45,143 |

| 2008 | 14,841 |

| 2009 | 278,915 |

| 2010 | 590,993 |

| 2011 | 506,575 |

| 2012 | 695,631 |

| 2013 | 880,036 |

| 2014 | 1,745,648 |

| 2015 | 2,361,214 |

| 2016 | 2,266,012 |

| 2017 | 1,574,985 |

| 2018 | 601,880 |

| 2019 | 1,171,167 |

Download this table Table 16: Estimates of amount spent (£, current prices) on publicly funded research on UK woodlands, 2006 to 2019

.xls .csvOur estimates of scientific research in UK woodlands remain highly experimental. The decision to include or exclude a research project represents a value judgement. Meanwhile, use of the UKRI Gateway data source risks excluding studies from abroad that focus on UK woodlands. UKRI Gateway also focuses on publicly funded studies, omitting privately funded studies.

Heritage

Examples of potentially historic natural woodland environments include:

- ancient hedgerows or trees, such as the Major Oak in Sherwood Forest

- geological features

- sawpits

- banks

- charcoal platforms

- relict field boundaries

- woodland forts

- barrows

- woodland gardens

Nearly 5,000 scheduled ancient monuments (ZIP, 8.39MB) are in British forests, but the number of sites with archaeological interest is unknown. Historic England has registered 1,245 sites as scheduled ancient monuments and 1,022 sites as park and gardens Grades I and II as at January 2020 for woodlands.

By understanding the historical character of a landscape, it can help to identify the supporting services that makes places special for wildlife and people.

Nôl i'r tabl cynnwys8. Asset value of woodlands

The asset account includes selected woodland ecosystems services, valued at £130 billion for 2017 (Table 17). The asset value of the regulating services make up 77% of the overall value of woodlands, the recreation (cultural) asset value is 18% of the overall, and only 6% of the value is from the provisioning of timber and fuel. Some of the recreation and carbon sequestration value will be realised by woodland managers. However, it is likely that over 90% of the value of our woodlands is non-market.

| Service | 2017 |

|---|---|

| Timber | 7,306 |

| Wood fuel | 1,656 |

| Carbon Sequestration | 54,620 |

| Pollution removal | 31,673 |

| Urban woodland cooling | 4,608 |

| Flood prevention GB | 6,513 |

| Noise reduction | 833 |

| Recreation | 22,534 |

| Total | 129,743 |

Download this table Table 17: Woodland ecosystem asset values, £ million (2018 prices), UK, 2017

.xls .csv9. Woodland ecosystem services data

Woodland natural capital accounts, UK: supplementary information

Dataset | Released 28 February 2020

Physical (non-monetary) and monetary estimates of services provided by natural assets in the UK between 2000 and 2018.

10. Glossary

Asset

Asset valuation is an estimate of the stream of services that are expected to be generated over the life of the asset. It looks at the pattern of expected future flows and the time period over which the flows of values are expected to be generated.

Ecosystem services

Ecosystem services are the flows of benefits that people gain from natural ecosystems. This includes provisioning services such as food and water; regulating services such as flood protection and pollution removal; and cultural services such as recreational and heritage.

Natural capital

Natural capital is a way of measuring and valuing the benefits that the natural world provides society. These benefits from natural resources include food, cleaning the air of pollution, sequestering carbon and cleaning fresh water.

Woodlands

Woodlands in the UK are tree-covered areas that include plantation forests, more natural forested areas, and lower density or smaller stands of trees.

Nôl i'r tabl cynnwys11. Measuring the data

In this release, the woodland habitat accounts are presented in four sections:

the size of the area covered by woodland (extent account)

indicators of the quality of the woodland ecosystem and ability to continue supplying services (condition account)

quantity and value of services supplied by the woodland ecosystem (physical and monetary ecosystem service flow accounts)

value of woodland as an asset, which represents the stream of services expected to be provided over the lifetime of the asset (monetary asset account)

The data underpinning woodlands natural capital come from a range of sources with different timeliness and coverage. This release is based on the most recent data as at January 2020.

Data sources include:

- British Trust for Ornithology (BTO)

- Butterfly Conservation (BC)

- Department for Business, Energy and Industrial Strategy

- Department for Environment, Food and Rural Affairs (Defra)

- Economics for the Environment Consultancy (EFTEC)

- European Forest Fire Information System (EFFIS)

- Forest Research

- Forestry Commission

- Forestry England

- Joint Nature Conservation Committee (JNCC)

- Met Office

- Natural England

- Natural Resources Wales

- Royal Society for the Protection of Birds (RSPB)

- Scottish Natural Heritage

- UK Centre for Ecology and Hydrology

- UK National Atmospheric Emissions Inventory (NAEI)

- UK Research and Innovation (UKRI)

- Woodland Trust

Deatiled methodology on the calculations of ecosystem services can be found in the Woodland natural capital accounts methodology guide, UK: 2020.

The Office for National Statistics’ (ONS’) natural capital accounts are produced in partnership with the Department for Environment, Food and Rural Affairs (Defra).

12. Strengths and limitations

Data quality

The ecosystems services are experimental statistics. Currently, there is no single data source for the UK for the individual ecosystem services. They are calculated from data from the four countries with different timeliness.

Ecosystems provide a diverse range of services and not all have been included in this publication, either owing to unavailability of data or the need for new methods of evaluation. We intend to continue to develop our ability to report on all services. Our progress can be seen in what services are included and excluded (Table 18).

| Services | Included quantitative | Included qualitative | Not included |

|---|---|---|---|

| Provisioning | Timber | Food | Wild animals |

| Energy - woodfuel | Christmas trees | ||

| Regulating | Carbon sequestration | Waste water cleaning | |

| Air pollution removed | Mediation of smell, and visual pollutants | ||

| Temperature | Water condition regulation | ||

| Flood mitigation | |||

| Noise reduction | |||

| Cultural | Recreation | Education | Symbolism of certain plants and animals |

| Scientific research | Value placed on nature simply existing | ||

| Heritage |

Download this table Table 18: UK environmental services included in this publication

.xls .csvMethodology

Details of methodologies for woodlands can be found in Woodland natural capital accounts methodology guide, UK: 2020. Further details on the concepts and methodologies underlying the UK natural capital accounts can be found in Principles of Natural Capital Accounting.

Nôl i'r tabl cynnwys