1. Background

Alongside estimates of quarterly labour productivity for the UK, the Office for National Statistics (ONS) also publishes labour productivity for several industrial sections and sub-sections; defined by the Standard Industrial Classification 2007: SIC 2007. These figures use estimates of gross value added (GVA) taken directly from the UK National Accounts and estimates of labour input to calculate labour productivity. In this release, experimental estimates of labour productivity at a more detailed level are presented, primarily at the 2-digit SIC industry level, delivering a 46 industry breakdown in services, compared with the 11 industry breakdown previously provided.

We have been working to improve the range and detail of productivity data that we publish. In January 2017, we published updated estimates of labour productivity on a regional basis, at the NUTS1, 2 and 3 levels. In April 2017, we published experimental estimates of quarterly regional labour input on a consistent basis with equivalent UK-level metrics. The data published as part of this release extends this run of developments. This article introduces experimental estimates of labour productivity for a more detailed set of industries than has previously been available, and a companion article sets out new, experimental estimates of industry by region labour productivity on an annual basis. Each of these outputs has been designed to be consistent with our headline measures of output and employment. This improvement in the granularity of labour metrics and productivity measures allows more detailed analysis of productivity and is part of a broader work-programme being carried out by the ONS Productivity Teams.

This note introduces these experimental data. It provides some initial analysis demonstrating trends in the data and explains some of their advantages and disadvantages. Section 2 outlines the methodology that we use to estimate these series. Section 3 presents some of the main findings from these data.

As with all of our productivity outputs, we welcome user views on the possible uses and usefulness of these data. This is particularly relevant for these experimental series. These should be directed to our inbox: Productivity@ons.gov.uk. Subject to user feedback, it is our intention to publish these more detailed industry labour productivity metrics on a quarterly basis in the future.

Nôl i'r tabl cynnwys2. Methodology

Labour productivity estimates are derived by dividing measures of “output” by a measure of labour “input”. Most of the output measures used in the labour productivity statistical outputs are taken directly from the UK National Accounts and are measures of real (inflation-adjusted) gross value added (GVA), for the whole economy, industries and sub-industries of the economy.

Labour input can be measured in a number of different ways, including the number of workers, jobs or hours worked. This release uses our preferred measure of labour input – hours worked – to provide estimates of output per hour worked. This measure of labour input is calculated by estimating the number of jobs in a given industry and multiplying these by estimates of average hours worked per job in that same industry. Jobs estimates are primarily derived from several sources: employee jobs are taken from the Short-Term Employment Survey, the Business Register Employment Survey and Public Sector Employment; self-employed jobs are derived from Labour Force Survey (LFS) datasets; Her Majesty’s Forces (HMF) jobs come from the Ministry of Defence; Government-Supported Trainee jobs are derived from LFS datasets, as are Unpaid Family Worker jobs. Average hours data are derived solely from the LFS (excluding HMF). Finally, the aggregate of industry-level estimates of hours worked are constrained to non-seasonally adjusted whole-economy hours worked (as published in Labour Market Statistics), seasonally adjusted and constrained again to seasonally-adjusted whole-economy hours worked1.

This methodology reflects that used in the calculation of Labour Productivity National Statistics, but as these lower-level estimates are experimental they should be treated with care. In particular, the granularity of the data means individual series can be volatile relative to the movement of higher level industries. We recommend that users focus on long-term trends in these series and avoid concentration on specific quarterly movements. Data are presented quarterly to enable users who wish to utilise the granularity of this breakdown in their analyses, for example, to better understand the effect of industry composition on aggregate labour productivity movements. In this first release, these detailed industry metrics are presented for the period from 2009 onwards, indexed to their respective values in 2013. Subject to user feedback, we plan to extend this time series and to publish the relative levels of labour productivity in these more detailed industries in a future release.

Notes for: Methodology

- This process of constraint is undertaken to ensure productivity hours estimates sum to those published in Labour Market Statistics – creating consistent data across ONS publications.

3. Findings

The additional detail included in these metrics can support a wide variety of analytical work, of which only a small fraction is presented here. Labour productivity data were previously only available for 11 sections in services, whereas 46 estimates are now available – primarily at the division level1. The number of manufacturing series has increased more modestly from 10 to 13 – reflecting the more detailed data already available for this industry. For the first time, estimates of labour productivity for mining and quarrying, electricity, gas, steam and air conditioning supply, and sewage, waste management and remediation activities are also available, along with a breakdown of construction into three smaller components.

One important feature that stands out from this new dataset is the marked variation of productivity growth experiences within industry sections (that is, higher-level industry categories). To demonstrate this feature, Figure 1 shows the level of output per hour for section G (retail, wholesale, and motor trade) along with its three division level components, indexed to their respective values in 2013. While the lower, division level data can be more volatile, trends over the longer-term reveal the different experiences of G’s component industries. Since 2013, industry 45 (sale and repair of motor vehicles and motorcycles) grew faster than the other two components of G, but due to its relatively small weighting this has a relatively small effect on G as a whole. This stronger productivity growth was driven primarily by high gross value added (GVA) growth, as trends in hours worked were relatively similar across the three divisions.

Figure 1: Section G (Wholesale and retail trade) output per hour

UK, Quarter 1 (Jan to Mar) 2009 to Quarter 1 (Jan to Mar) 2017

Source: Office for National Statistics

Notes:

- Section G - Wholesale and retail trade; repair of motor vehicles and motorcycles.

- Industry 45 - Wholesale and retail trade and repair of motor vehicles and motorcycles.

- Industry 46 - Wholesale trade, except of motor vehicles and motorcycles.

- Industry 47 - Retail trade, except of motor vehicles and motorcycles.

Download this chart Figure 1: Section G (Wholesale and retail trade) output per hour

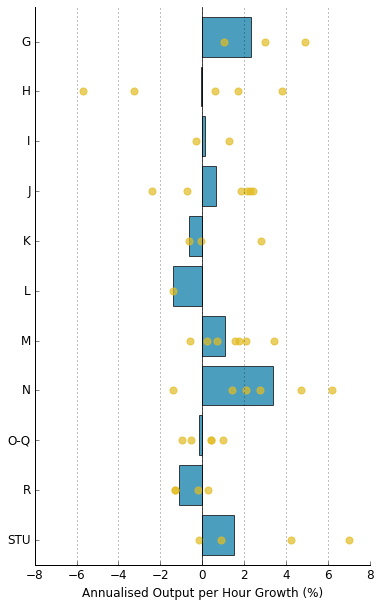

Image .csv .xlsThese differences within industry sections are replicated across the economy to varying extents. Figure 2 compares the average annual growth in output per hour for each services section between Quarter 1 (Jan to Mar) 2009 and Quarter 1 2017 (shown in the bars) with the growth rates of its component sub-industries (the dots). It shows that analysing trends at the division-level can yield quite different results compared with analysis of section-level data. For example, sections H (transportation and storage) and I (accommodation and food services) have both broadly maintained their levels of productivity over this period. However, in transportation and storage, the productivity growth of postal and courier services, land transport, and air transport was offset by falls in productivity in water transport and warehousing – which experienced the weakest productivity growth within services over the period. In accommodation and food services, by contrast, the experience of the two sub-industries was much more similar over this period. Looking at services as a whole, it is rare that all divisions within a section have productivity growth in the same direction – demonstrating the extent to which variation at the division level within each section is a widespread phenomenon.

Figure 2: Annualised output per hour growth in services

UK seasonally adjusted, Quarter 1 (Jan to Mar) 2009 to Quarter 1 (Jan to Mar) 2017

Source: Office for National Statistics

Notes:

- G - Wholesale and retail trade; repair of motor vehicles and motorcycles

- H - Transportation and storage

- I - Accommodation and food service activities

- J - Information and communication

- K - Financial and insurance activities

- L - Real estate activities

- M - Professional, scientific and technical activities

- N - Administrative and support service activities

- OPQ - Public administration and defence; compulsory social security, Education, Human health and social work activities

- R - Arts, entertainment and recreation

- STU - Other service activities, Activities of households as employers; undifferentiated goods- and services-producing activities of households for own use, Activities of extraterritorial organisations and bodies.

Download this image Figure 2: Annualised output per hour growth in services

.png (15.4 kB) .xls (27.6 kB){kind=link}

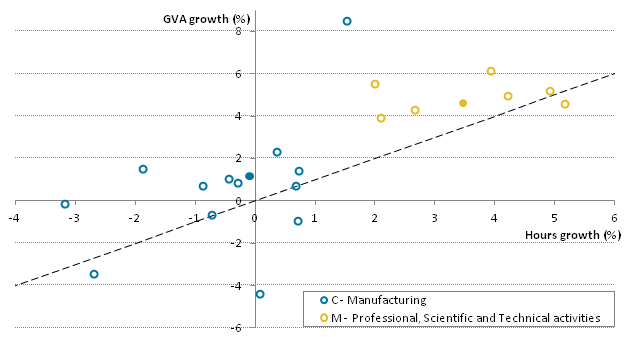

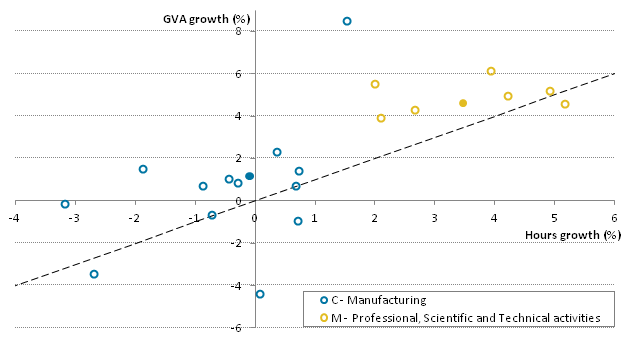

The new data also enable analysis of how different detailed industries achieve their labour productivity growth over a period, highlighting differences within and between industry sections2. Figure 3 shows the average annual growth of hours worked (horizontal axis) and GVA (vertical axis) for selected section-level industries (solid points) and their divisional-level industry components (hollow points). The diagonal line indicates combinations of hours and GVA growth that deliver no change in productivity: points above (below) the black line indicate positive (negative) average annual productivity growth. The variation in how different rates of productivity growth were achieved is striking. Average annual productivity growth in C (manufacturing) and M (professional, scientific and technical activities) over the 2009 to 2016 period was quite similar, at 1.3% and 1.1% respectively. In manufacturing, this was a result of largely stable total hours worked and modest growth in GVA. In industry M, by contrast, a similar rate of productivity growth was achieved by both stronger output and hours growth.

Figure 3: Average annual growth in hours versus average annual growth in gross value added

UK, Quarter 1 (Jan to Mar) 2009 to Quarter 1 (Jan to Mar) 2017

Source: Office for National Statistics

Download this image Figure 3: Average annual growth in hours versus average annual growth in gross value added

.png (12.1 kB) .xls (29.7 kB){kind=link}

The additional information in Figure 3 highlights that this range of experience at the section level is replicated at the division level. For instance, industry M’s labour productivity growth was the result of growing output and hours worked in each of its sub-industries: average annual growth in hours worked ranged between 2% and 5% over this period, with somewhat stronger GVA than hours growth in most sub-industries. As a result, all but one sub-industry experienced productivity growth over this period. However, the range of division level results in manufacturing is much broader. Three manufacturing sub-industries experienced productivity falls over this period; one sub-industry (manufacture of transport equipment) experienced a marked increase in productivity, while the remainder experienced more modest growth, driven largely by modest growth in gross value added (GVA) combined with a fall in hours worked. These results – and those available through the data published as part of this release – suggest that this increased granularity can aid user understanding of labour productivity at the industry level.

Notes for: Findings

For brevity, this article refers to the “division-level” to describe the level of detail provided in this new dataset, even though some data are provided at a higher level of aggregation.

A similar analysis was conducted for the UK economy as a whole – see the Quarter 4 (Oct to Dec) Productivity Introduction.

4. Uses for these data and next steps

The development of these experimental, more detailed labour productivity metrics for the industries and sub-industries of the UK should enable users to perform more detailed analysis than previously. Used appropriately, these data should provide a better understanding of how labour productivity varies within and between industries and should also enable analysis of how the changing composition of the UK economy has affected the overall rate of productivity growth.

As with all of our productivity outputs, we welcome user views on the possible uses and usefulness of these data. This is particularly relevant for these experimental series. These should be directed to our inbox: Productivity@ons.gov.uk. Subject to user feedback, it is our intention to publish these more detailed industry labour productivity metrics on a quarterly basis in the future.

Nôl i'r tabl cynnwys