Cynnwys

- Main points

- Overview

- Your views matter

- UK non-financial business economy, Sections A to S (part)

- Non-financial services, Sections H to S (part)

- Distribution, Section G

- Construction, Section F

- Production, Sections B to E

- Manufacturing, Section C

- Agriculture (part), Forestry and Fishing, Section A

- Revisions to 2013 ABS regional data

- Quality and methodology

- Background notes

1. Main points

In 2014, the income generated by local activity of businesses in the UK, less the cost of goods and services used to create this income, was estimated to be £1,091.5 billion. This amount represents the approximate gross value added at basic prices (aGVA) by local activity of the businesses in the UK non-financial business economy.

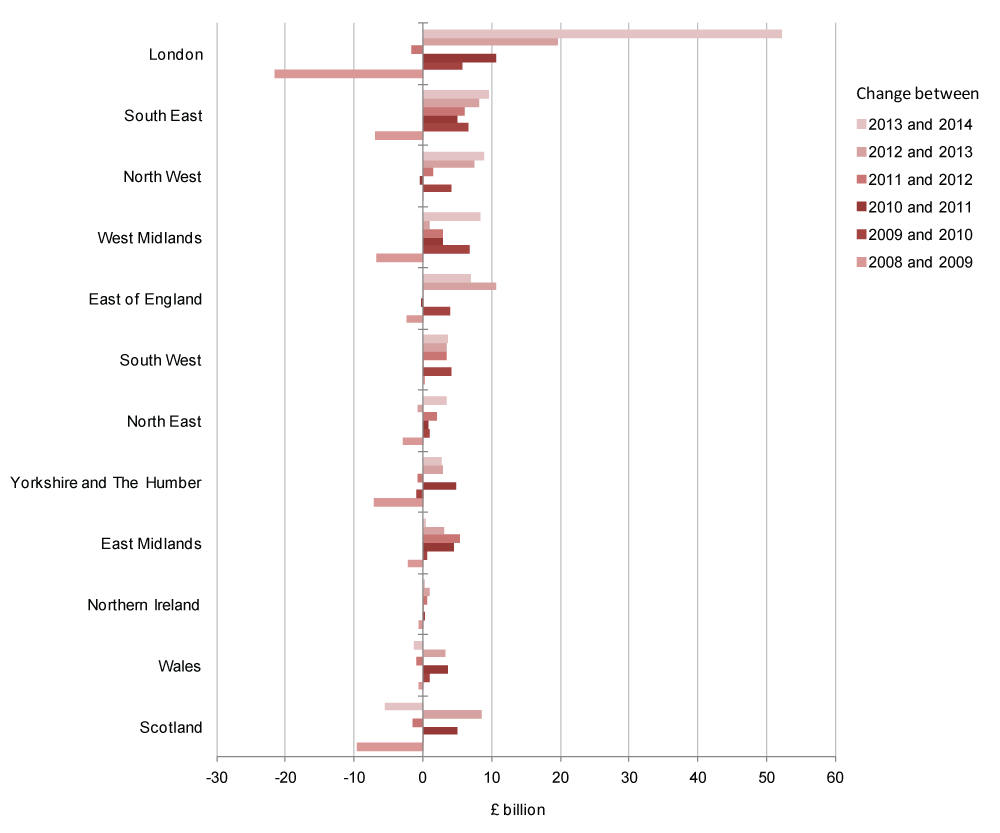

Between 2013 and 2014, aGVA increased by 9.0% (£89.7 billion). This increase is a continuation of the recovery seen between 2009 and 2013, and was due to an increase in turnover combined with a decrease in purchases. The increase in turnover was led by the East of England, while the decrease in purchases was mostly seen within London.

Out of the 12 UK regions, 10 saw growth in aGVA between 2013 and 2014, with the highest contribution to overall growth from London, the South East and the North West. The non-financial service sector has driven the growth in all 3 regions. Scotland and Wales are the only regions showing a decrease in aGVA, with the production sector contributing the most to the fall in both regions.

The region with the largest aGVA increase between 2013 and 2014 was London, with a rise of 23.0% (£52.1 billion), with growth in its non-financial service sector of 19.5% (£33.6 billion) contributing most. With 3 of the 5 industrial sectors showing a continuation of the recovery seen since 2009, aGVA in London is 30.2% (£64.7 billion) above the level seen in 2008.

The second largest aGVA increase of 6.1% (£9.7 billion) between 2013 and 2014 was in the South East where all industrial sectors contributed to growth. aGVA is now 20.6% (£28.5 billion) above its 2008 level, with the non-financial service sector the main contributor with an increase of 34.0% (£24.9 billion) between 2008 and 2014.

In 2014, the aGVA in 11 of the 12 UK regions is above that reported in 2008, with only Scotland again lower than its 2008 level. This followed a 6.0% (£5.5 billion) fall in Scotland’s aGVA between 2013 and 2014, due primarily to a decrease in the production sector.

Out of the 37 sub-regions of the UK, 25 showed growth in aGVA between 2013 and 2014, with Inner and Outer London and Cheshire dominating with a combined rise of £59.5 billion. Of the remaining 12 sub-regions showing a fall in aGVA, the largest were within North Eastern Scotland, Eastern Scotland and Derbyshire and Nottinghamshire with a combined fall of £7.1 billion.

Nôl i'r tabl cynnwys2. Overview

Estimates of the size and growth of the UK non-financial business economy for 2014, based on the local activity of businesses as measured by the Annual Business Survey (ABS), are presented in this release. It is the main resource for understanding the detailed structure, conduct and performance of businesses across the UK at a regional level. The release covers the following sectors:

Non-financial services (includes professional, scientific, communication, administrative, transport, accommodation and food, private health and education, and entertainment services)

Distribution (includes retail, wholesale and motor trades)

Production (includes manufacturing, oil and gas extraction, energy generation and supply, and water and waste management)

Construction (includes civil engineering, house building, property development and specialised construction trades such as plumbers, electricians and plasterers)

parts of Agriculture (includes agricultural support services and hunting), forestry and fishing

Together these industries represent the UK non-financial business economy and account for around two-thirds of the whole economy of the UK in terms of gross value added. Public administration and defence, public sector health and education, finance, farming and households make up the rest of the whole UK economy and are not covered by this release.

Regional ABS estimates are produced by apportioning the survey return from each reporting unit to its individual sites, and then summing them to the regional level. For the national ABS results, industry breakdowns are obtained by classifying enterprises to industries. For the regional ABS results, this classification is done for individual sites, so industry breakdowns at the UK level in the national release will not necessarily match those in the corresponding regional release. For example, an enterprise contributing wholly to production at the national level may have local units contributing to other sectors (e.g. wholesale) at the regional level. More information can be found under regional apportionment in background note 9 of this release.

Although the estimated total for the UK business economy in the regional ABS results is constrained to equal that in the corresponding national ABS results, the published totals for the UK non-financial business economy will not necessarily be the same following the removal of data for the Insurance and reinsurance industries (SIC2007 Groups 65.1 and 65.2) from the regional results after apportionment has taken place.

Insurance and reinsurance have been removed from this release since July 2014 due to ongoing volatility in the estimates. For more detail see background note 9.

As a result, an enterprise contributing wholly to insurance and reinsurance at the national level (and therefore removed from the national totals) may have local sites in other industries which will still contribute to the regional totals. Likewise, an enterprise contributing wholly to the Distribution sector (and therefore included in the national totals) may have a local site in insurance and reinsurance whose contribution will be removed from the regional totals.

Estimates published in this release include turnover, purchases, approximate gross value added at basic prices (aGVA) and employment costs. All data are reported at current prices (effect of price changes not removed). Therefore, users should note that unlike the constant prices published in the national accounts, ABS figures do not remove the effect of inflation on prices.

Data on purchases for 2012 onwards has been produced using a new methodology for apportioning reporting unit purchases to the local unit level. This has introduced a small discontinuity in the purchases and aGVA data series with 2008 to 2011 still calculated using the original method. Advance notification describing the change was published in an information paper on the 11 June 2015.

Where the economic downturn is mentioned, it refers to the contraction of gross domestic product (GDP) that started in 2008, the year from which a consistent ABS time series is available. For more information about the survey see the background notes.

The ABS has a wide range of uses: for example, ABS statistics are essential contributors to the UK National and Regional Accounts, including the measurement of GDP, they are supplied to Eurostat to meet the requirements of the European Structural Business Statistics (SBS) Regulation, and are used by the devolved administrations and central and local government to monitor and inform policy development.

ABS data were also recently published in our Exporters and Importers, Great Britain, 2014 release and contributed to the adhoc release Four facts about trade and business links between the UK and the Commonwealth. For other uses see background note 4.

Questions often asked of the ABS release are “What is aGVA?” and “How does the measure of aGVA differ from the GVA measure in the national and regional accounts?” For an overview of aGVA please see our infographic ‘What is aGVA?’. National Accounts carry out coverage adjustments, conceptual adjustments and coherence adjustments, in turn these estimates are used in the regional accounts. The national and regional accounts estimate of GVA uses input from a number of sources, and covers the whole UK economy, whereas ABS does not include farming, financial or public sectors. ABS total aGVA is around two-thirds of the national accounts whole economy GVA because of these differences. For further information on aGVA, see background note 9. There is also a recently published article A Comparison between ABS and National Accounts Measures of Value Added (462.3 Kb Pdf), which provides more detail.

We make every effort to provide informative commentary on the data in this release. Where possible, the commentary draws on evidence from businesses or other sources of information to help explain possible reasons behind the observed changes. However, it is difficult for businesses to provide detailed reasons for movements which are specific to a region; for example, businesses may state a “change in the nature of business activity across all sites”. Consequently, it is not possible for all data movements to be fully explained at a regional level. Users may benefit from reading the commentary in this release in conjunction with that in the UK non-financial business economy: 2014 revised results (national level) release, published on 9 June 2016. As the ABS regional estimates are produced by apportionment of the national results to a local level, all industry information noted in the National release will apply.

It is sometimes necessary to suppress figures for certain items in order to avoid disclosing information about an individual business. The ABS Technical Report (1.68 Mb PDF) describes the methods used to safeguard the information provided to us in confidence. In the same way our commentary must also avoid disclosing information about individual businesses.

Nôl i'r tabl cynnwys3. Your views matter

We constantly aim to improve this release and its associated commentary. We welcome any feedback you have, and are particularly interested to know how you make use of these data to inform your work. Please contact us using the contact information accompanying this release.

Nôl i'r tabl cynnwys4. UK non-financial business economy, Sections A to S (part)

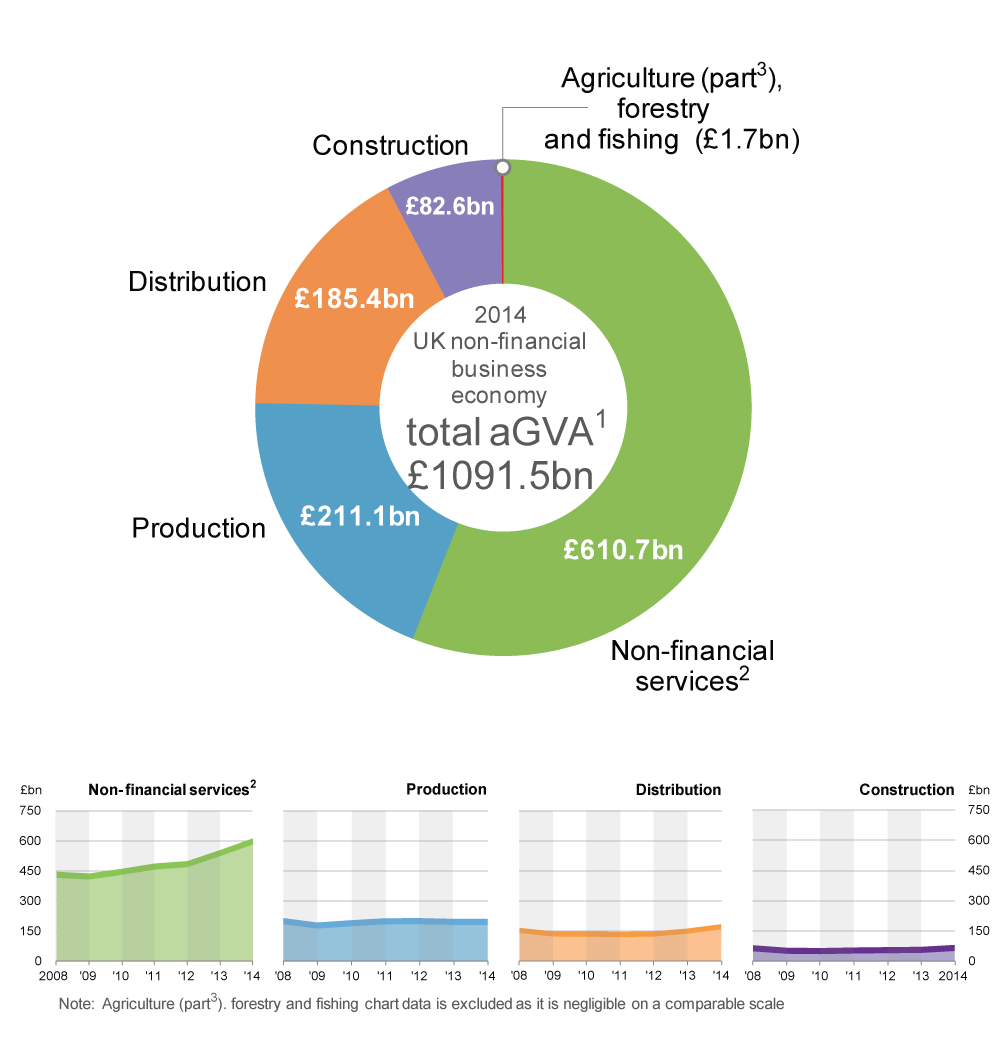

In 2014, the income generated by local activity of non-financial businesses in the UK, less the cost of goods and services used to create this income, was estimated to be £1,091.5 billion. This amount represents the approximate gross value added at basic prices (aGVA) of the UK non-financial business economy at a local activity level. Basic prices means the valuation of output includes net taxes (taxes minus subsidies) on production, such as business rates, but not net taxes on individual products that result from the production process, such as Value Added Tax (VAT).

Between 2013 and 2014, aGVA increased by 9.0% (£89.7 billion). This increase is a continuation of the recovery seen between 2009 and 2013 and takes aGVA to a level 20.1% (£182.6 billion) above that seen in 2008.

The main components of aGVA are:

Turnover (the main component of income).

Purchases (the main component of the consumed goods and services).

Between 2013 and 2014, turnover increased by 1.2% (£43.6 billion), while purchases of goods, materials and services decreased for the first time since 2009, by 1.3% (£33.4 billion). This has resulted in a 9.0% growth in aGVA. For further details on the components of aGVA see Calculation of gross value added estimates in background note 9.

All sectors of the UK non-financial business economy at a local activity level saw growth in aGVA between 2013 and 2014 (see Figure 1).

Non-financial services – the largest industry sector of the UK non-financial business economy – contributed most to the increase in aGVA, rising by 10.5% (£57.8 billion) between 2013 and 2014. This was the fifth consecutive annual increase, taking aGVA to £610.7 billion (see Figure 1).

Figure 1: UK non-financial business economy, local level aGVA by sector

2008 to 2014

Source: Office for National Statistics

Notes:

- Approximate GVA for the UK non-financial business economy in the regional release is different to that published in the national release (June 2016). More information can be found in background note 9

- Excludes Financial and insurance; Public administration and defence; Public provision of Education; Public provision of Health and all medical and dental practice activities

- Excludes crop and animal production

Download this image Figure 1: UK non-financial business economy, local level aGVA by sector

.png (71.5 kB) .xls (28.2 kB){kind=link}

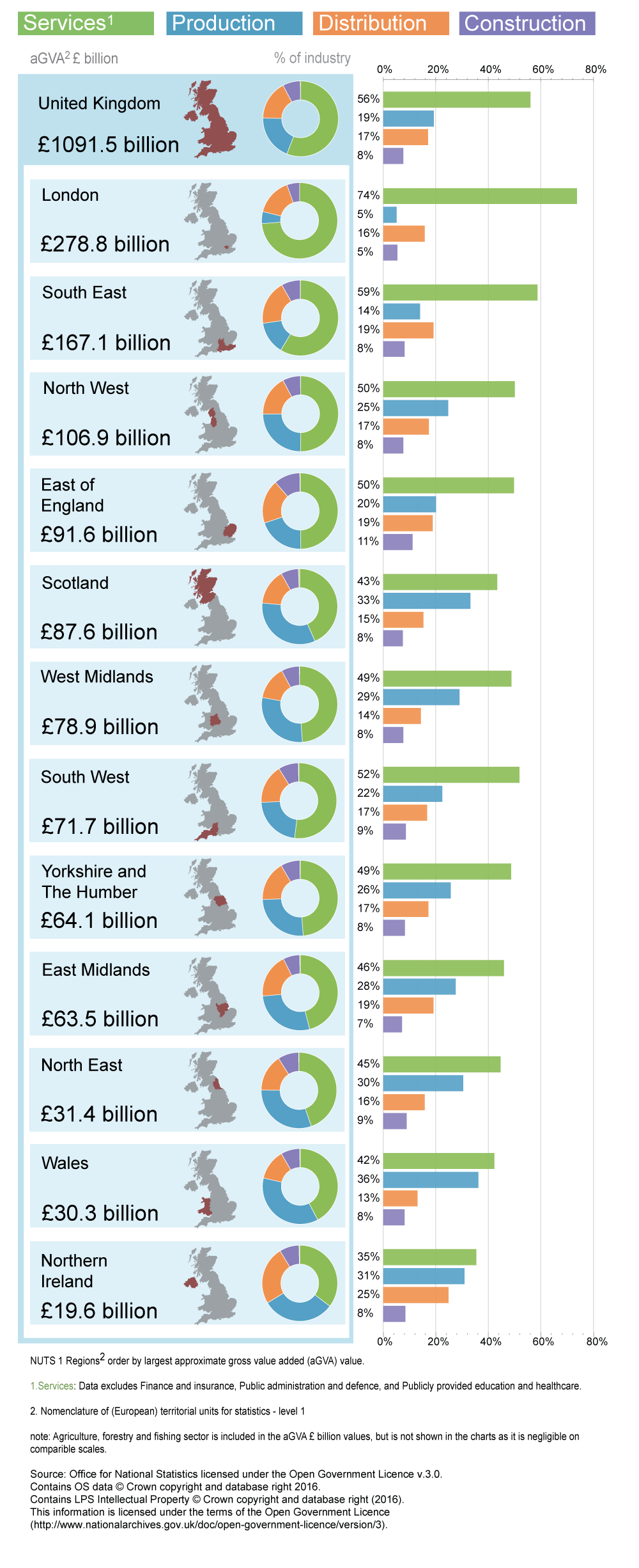

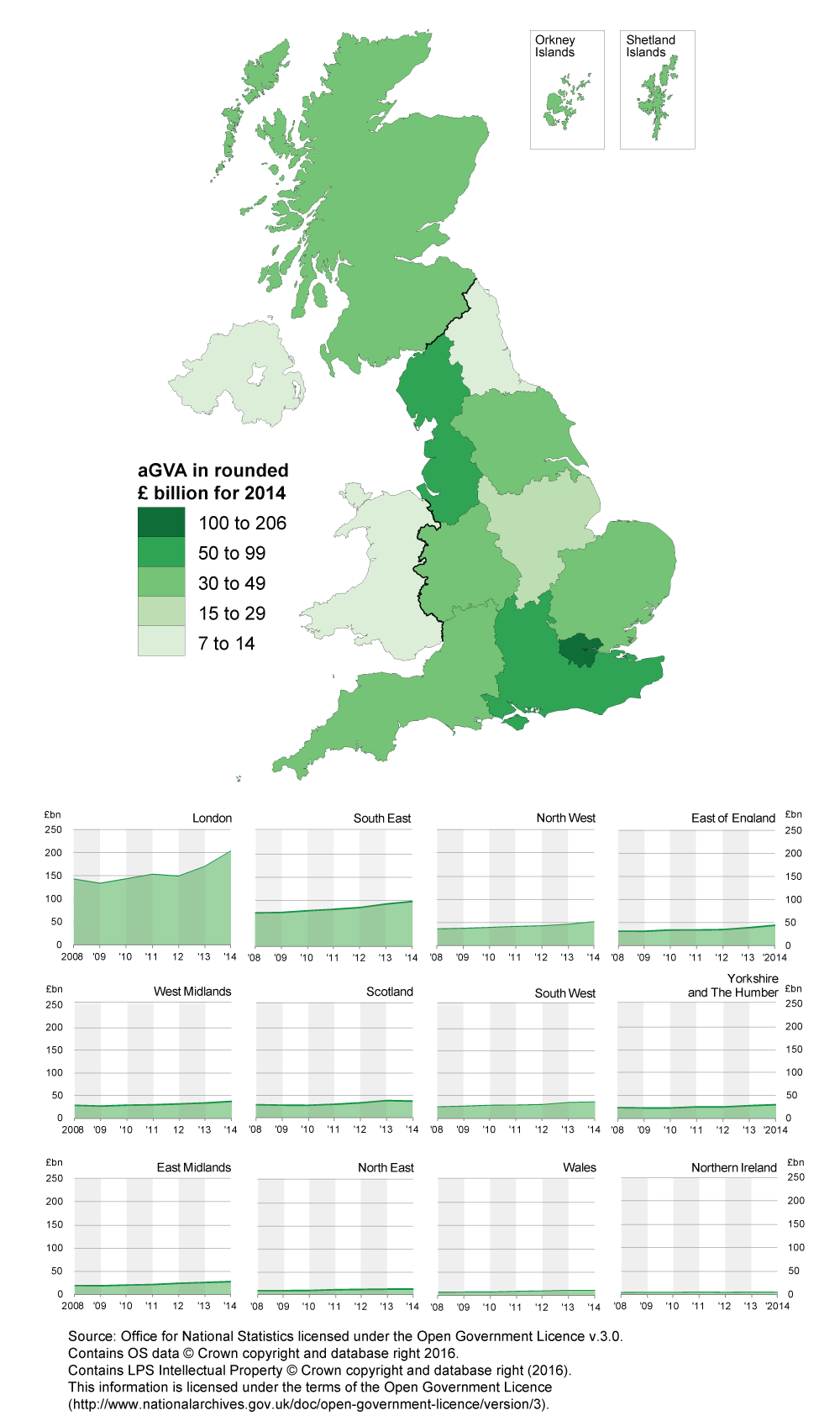

The regional picture

The industry composition of regions in the UK varies considerably. Wales and Scotland show similar contributions to their aGVA from both the Non-financial services (about a third) and Production sector (around two-fifths) in 2014, while other regions such as London have a dominant Non-financial services sector (around three-quarters of its aGVA in 2014) with a smaller share of value added being generated from all other sectors (see Figure 2).

Figure 2: UK non-financial business economy, local level aGVA, industry composition by NUTS 1 region

2014

Source: Office for National Statistics

Download this image Figure 2: UK non-financial business economy, local level aGVA, industry composition by NUTS 1 region

.png (288.0 kB) .xls (29.7 kB){kind=link}

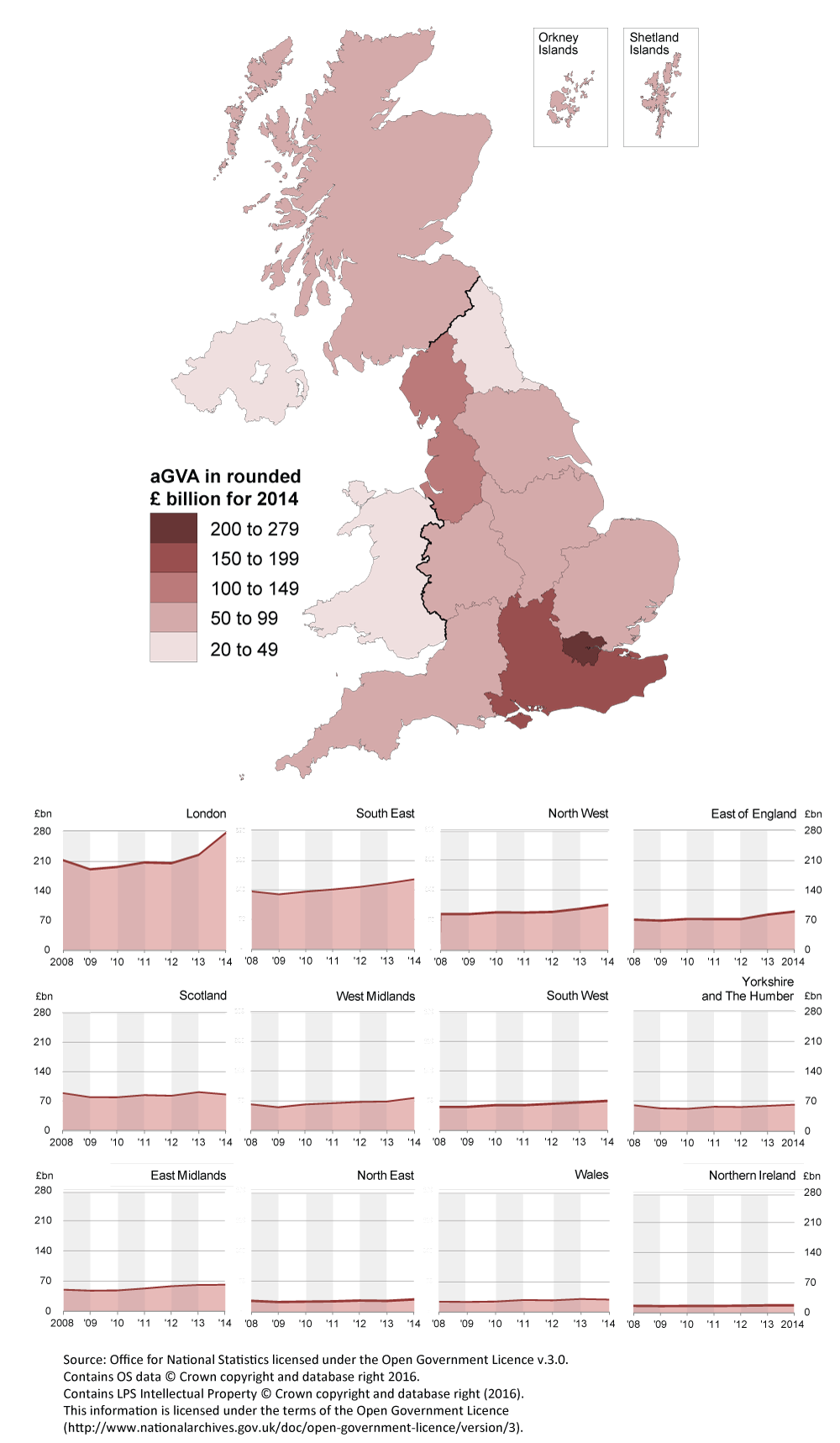

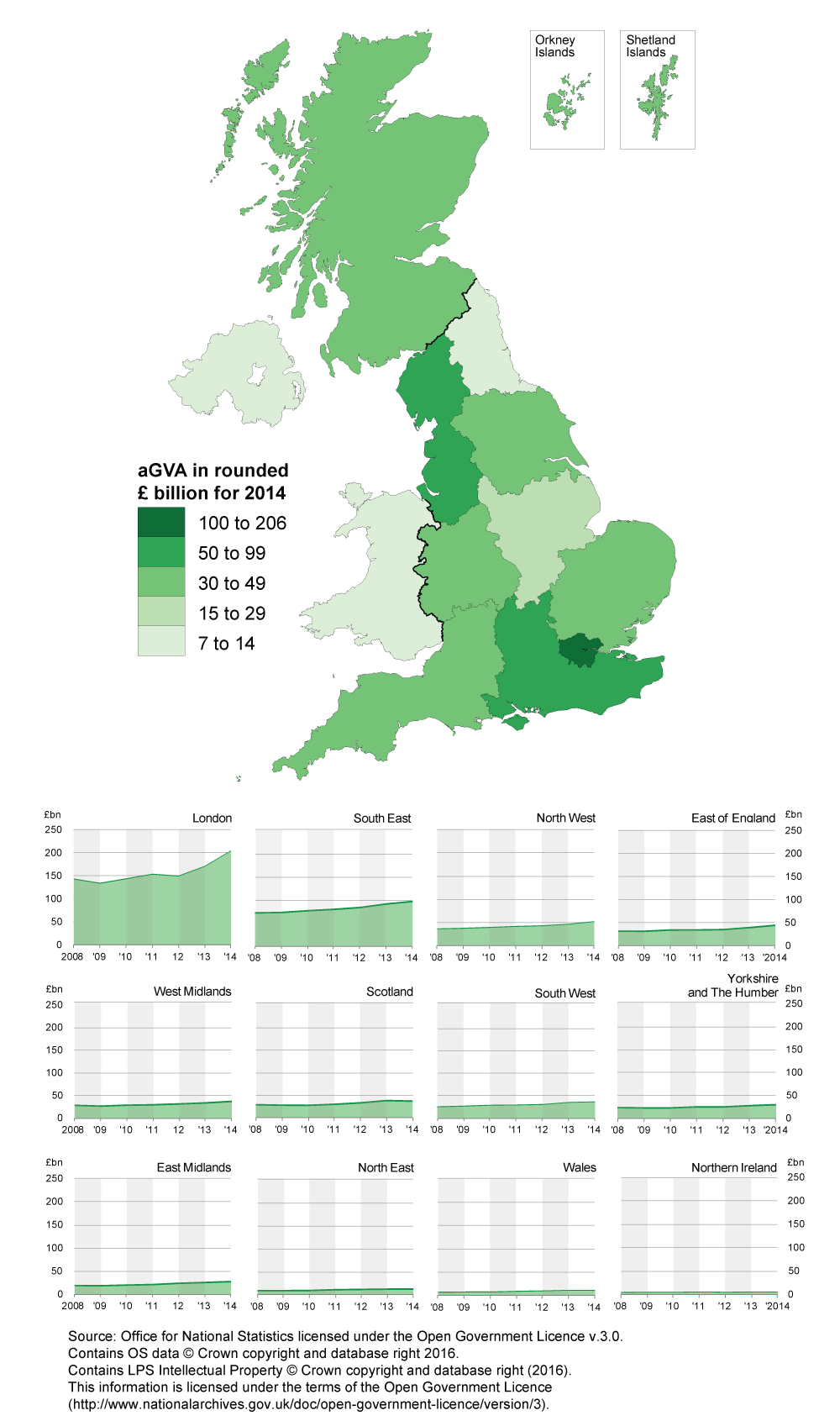

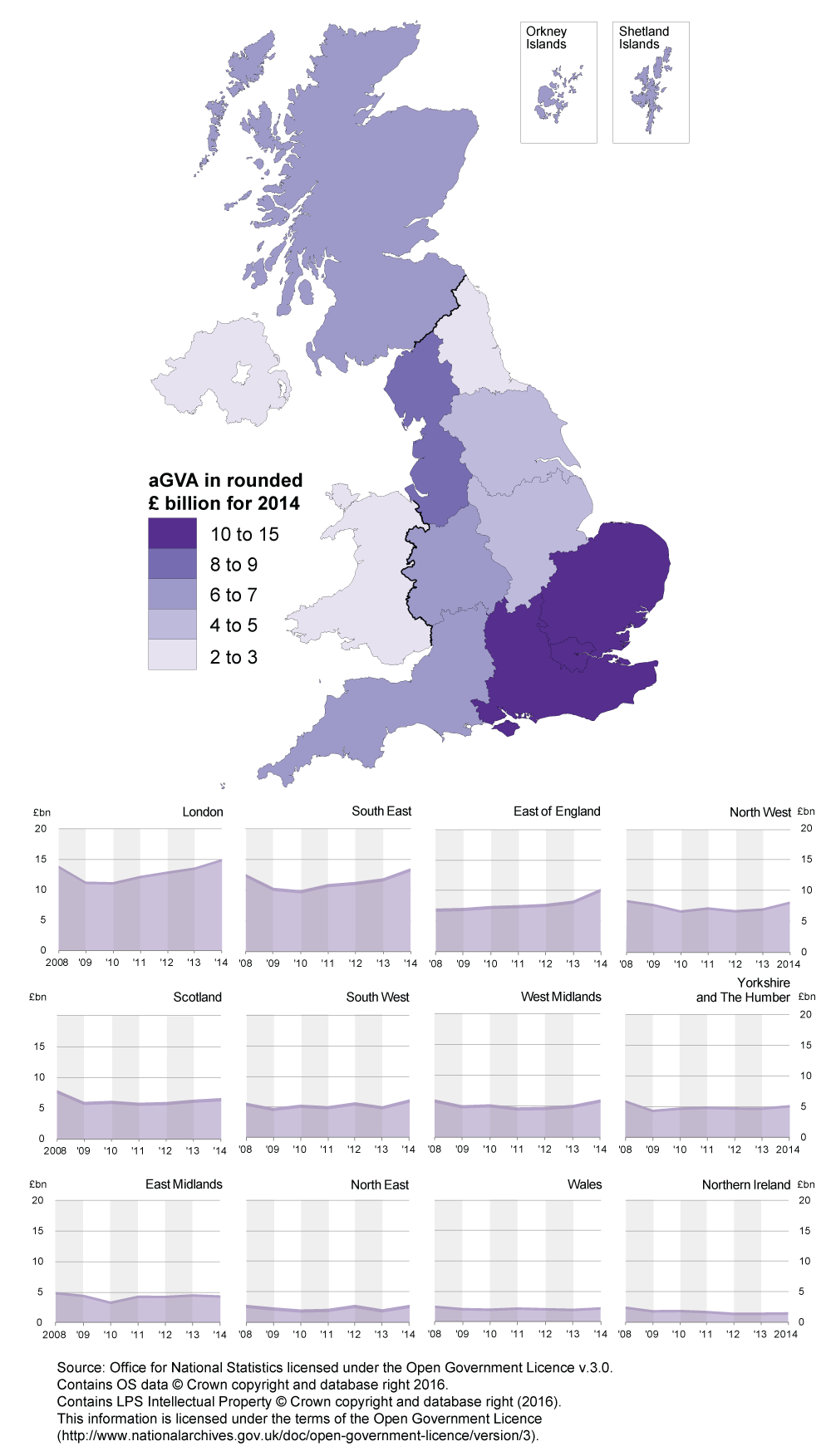

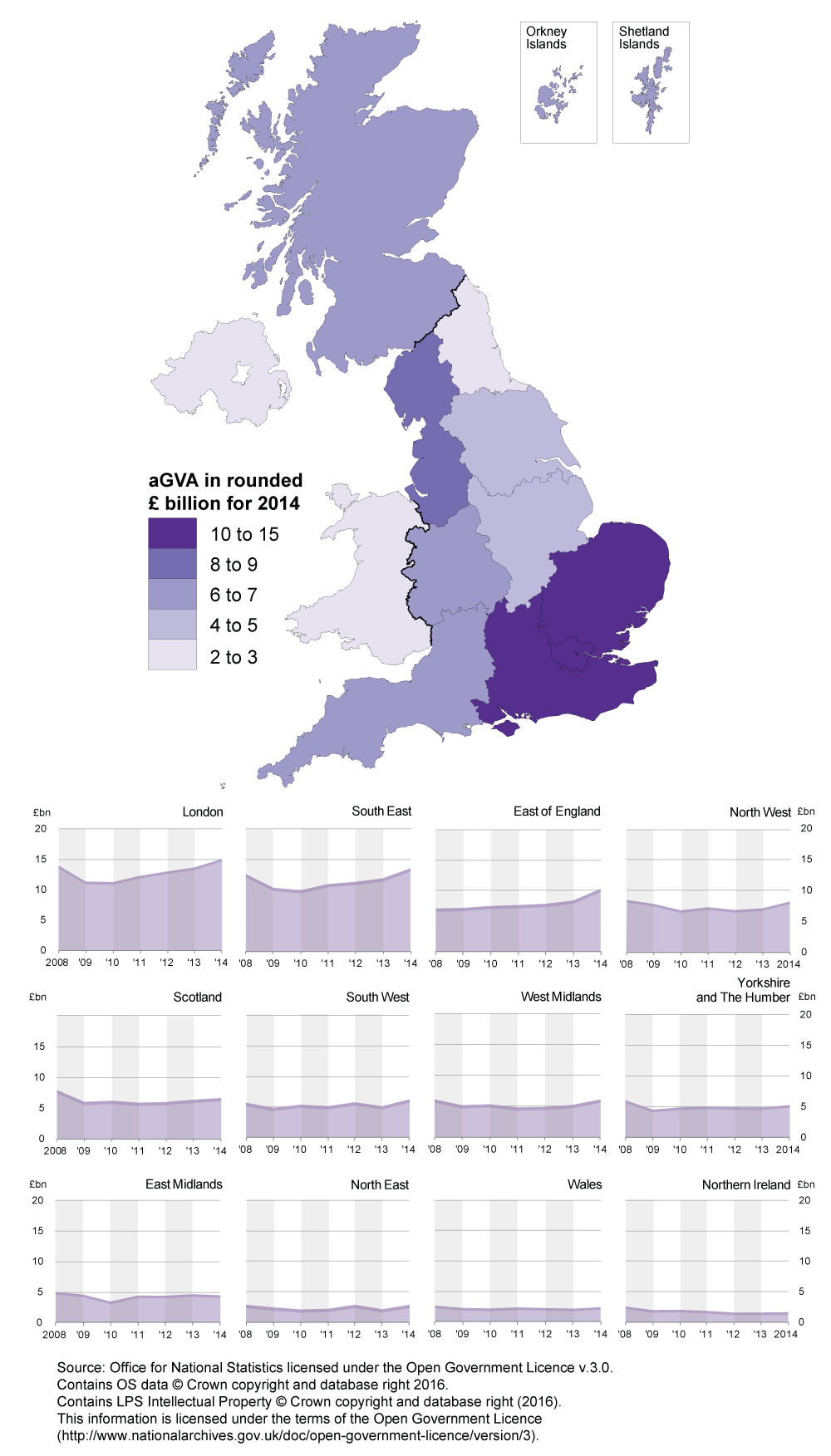

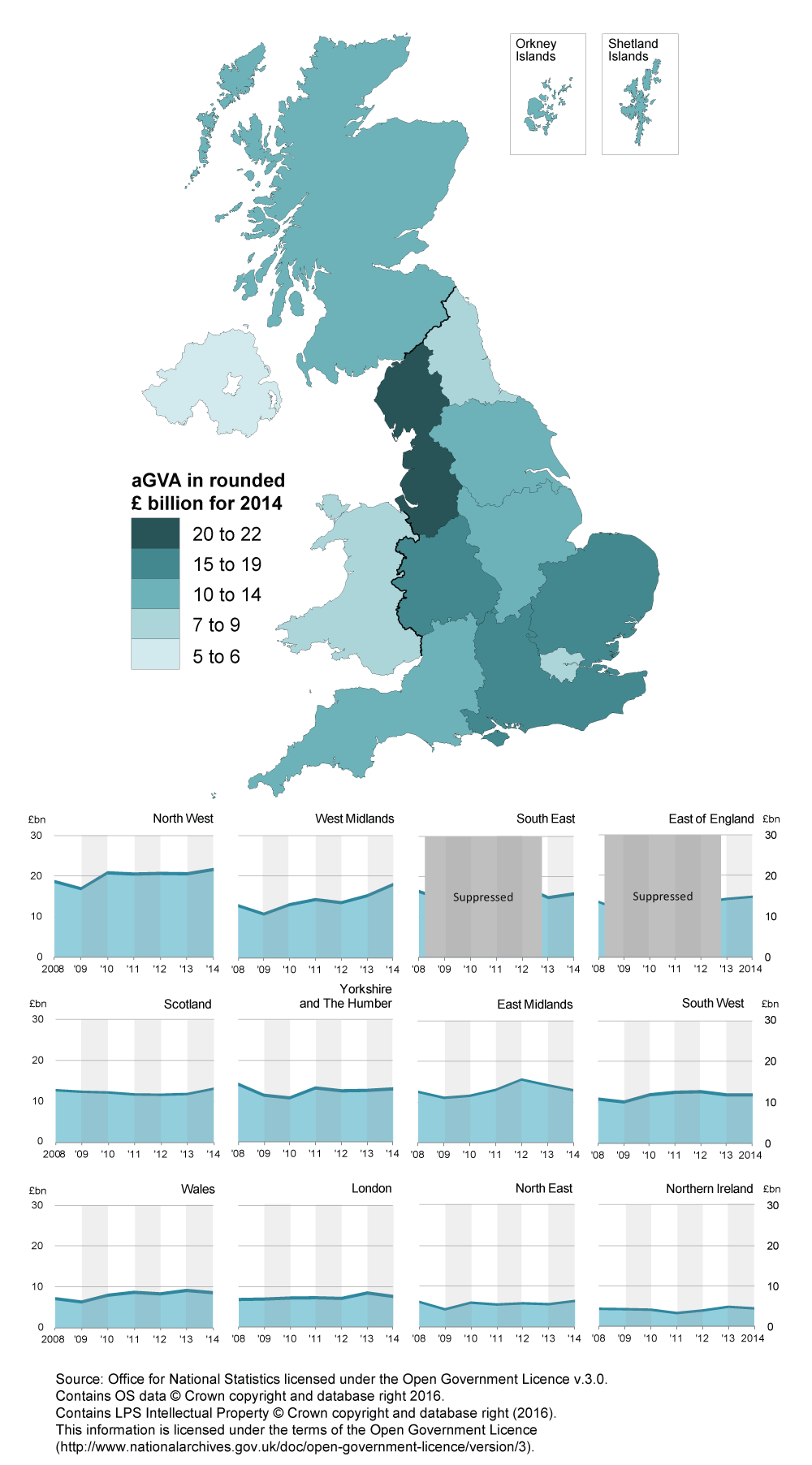

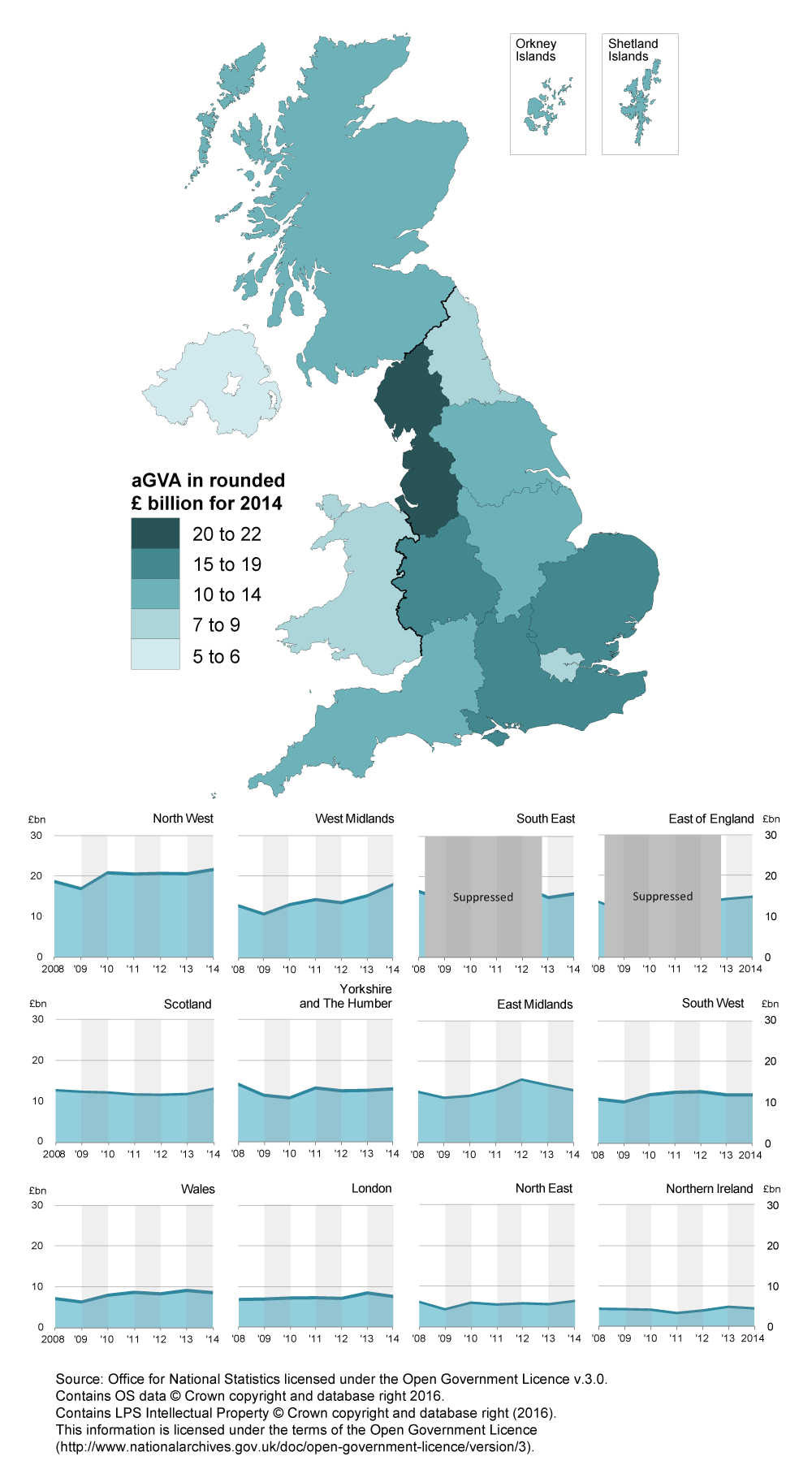

The largest 3 regions in terms of total aGVA were London, the South East and the North West, together contributing just over half of the total aGVA in the UK non-financial business economy (see Figure 3).

Figure 3: UK non-financial business economy, local level aGVA by NUTS 1 region

2008 to 2014

Source: Office for National Statistics

Download this image Figure 3: UK non-financial business economy, local level aGVA by NUTS 1 region

.png (326.6 kB) .xls (33.8 kB){kind=link}

Of the 12 regions, 10 saw growth in aGVA between 2013 and 2014 with London, the South East and the North West having the largest growth. Scotland and Wales are the only 2 regions to show a fall in aGVA between 2013 and 2014 (see Figure 4).

The East Midlands, West Midlands and the South East all saw a fifth consecutive year of growth in 2014, following falls between 2008 and 2009. The sub-national picture now shows only Scotland’s aGVA returning to a level marginally below that seen in 2008.

Selected regional summaries (in order of size of the value change in aGVA between 2013 and 2014)

London

London contributed the most to aGVA growth in the UK non-financial business economy between 2013 and 2014, increasing by 23.0% (£52.1 billion) (see Figure 4). Its growth was dominated by the Non-financial services sector (Sections H to S), the largest industry group in terms of aGVA, contributing £33.6 billion to the region’s total aGVA growth (a rise of 19.5%). The 2 main contributors to growth within Non-financial services were Arts, entertainment and recreation (Section R) and Professional, scientific and technical activities (Section M).

Within Arts, entertainment and recreation the main increase was in Gambling and betting activities (Division 92). However, the data for Section R (and Division 92 in particular) should be treated with caution, as the introduction of additivity within the purchases apportionment methodology (PAM) for 2012 onwards, has meant an increase in the volatility of the estimates at this level. For further details on work to make improvements to the methodology and estimates, to reduce this impact while maintaining the additivity, see background note 1.

For Professional, scientific and technical activities the main increase was in Activities of head offices; management consultancy activities (Division 70).

At the same time, the Production sector (Sections B to E) saw a decrease in aGVA of 11.6% (£1.9 billion) with the largest fall appearing within Extraction of crude petroleum and natural gas (Division 06). This is potentially linked to the sharp fall in commodity prices in the second half of 2014 as described in the chapter on Production.

South East

The South East made the second largest contribution to aGVA growth in the UK non-financial business economy between 2013 and 2014, increasing by 6.1% (£9.7 billion). All 5 industry sectors have contributed to the aGVA growth in the South East, with the largest contribution of 6.0% (£5.5 billion) from its Non-financial services sector (Sections H to S). The largest increase within this sector was in Professional, scientific and technical activities (Section M).

The Construction sector (Section F) made the next largest sector contribution to aGVA growth with a 13.6% (£1.6 billion) increase.

This is the fifth consecutive year of growth in aGVA for the South East, a growth of 20.6% (£28.5 billion) between 2008 and 2014.

North West

The aGVA in the North West grew by 9.2% (£9.0 billion) between 2013 and 2014. All sectors contributed to growth with the increase led by the Non-financial services sector (Sections H to S) which increased by 11.8% (£5.6 billion). The Production sector (Sections B to E), contributed a further £1.2 billion with the Construction (Section F) and Distribution (Section G) sectors each making a further £1.1 billion contribution to aGVA growth.

Within the region, it is only the Construction sector that has yet to return to a level above that recorded in 2008.

Scotland

The aGVA in Scotland fell between 2013 and 2014. Following a year of high growth in 2013, the region now shows a fall of 6.0% (£5.5 billion). The decrease in aGVA in 3 of the 5 sectors was led by the Production sector (Sections B to E) which fell by 12.6% (£4.2 billion). This is potentially linked to the sharp fall in commodity prices in the second half of 2014 as described in the chapter on Production.

The decrease brings the aGVA for Scotland back below the level recorded in 2008, with a fall of 3.5% (£3.2 billion) over the period.

Wales

Wales is the only other region showing a fall in aGVA of 4.3% (£1.3 billion) between 2013 and 2014. The decrease in aGVA in 3 of the 5 sectors was led by the Production sector (Sections B to E) which fell by 6.7% (£0.8 billion), followed by the Distribution sector (Section G) which fell by 16.3% (£0.8 billion).

Despite this overall decline, the region’s aGVA still remains above the level recorded in 2008.

Figure 4: UK non-financial business economy, local level aGVA change by NUTS 1 region

2008 to 2014

Source: Office for National Statistics

Download this image Figure 4: UK non-financial business economy, local level aGVA change by NUTS 1 region

.png (34.5 kB) .xls (34.3 kB){kind=link}

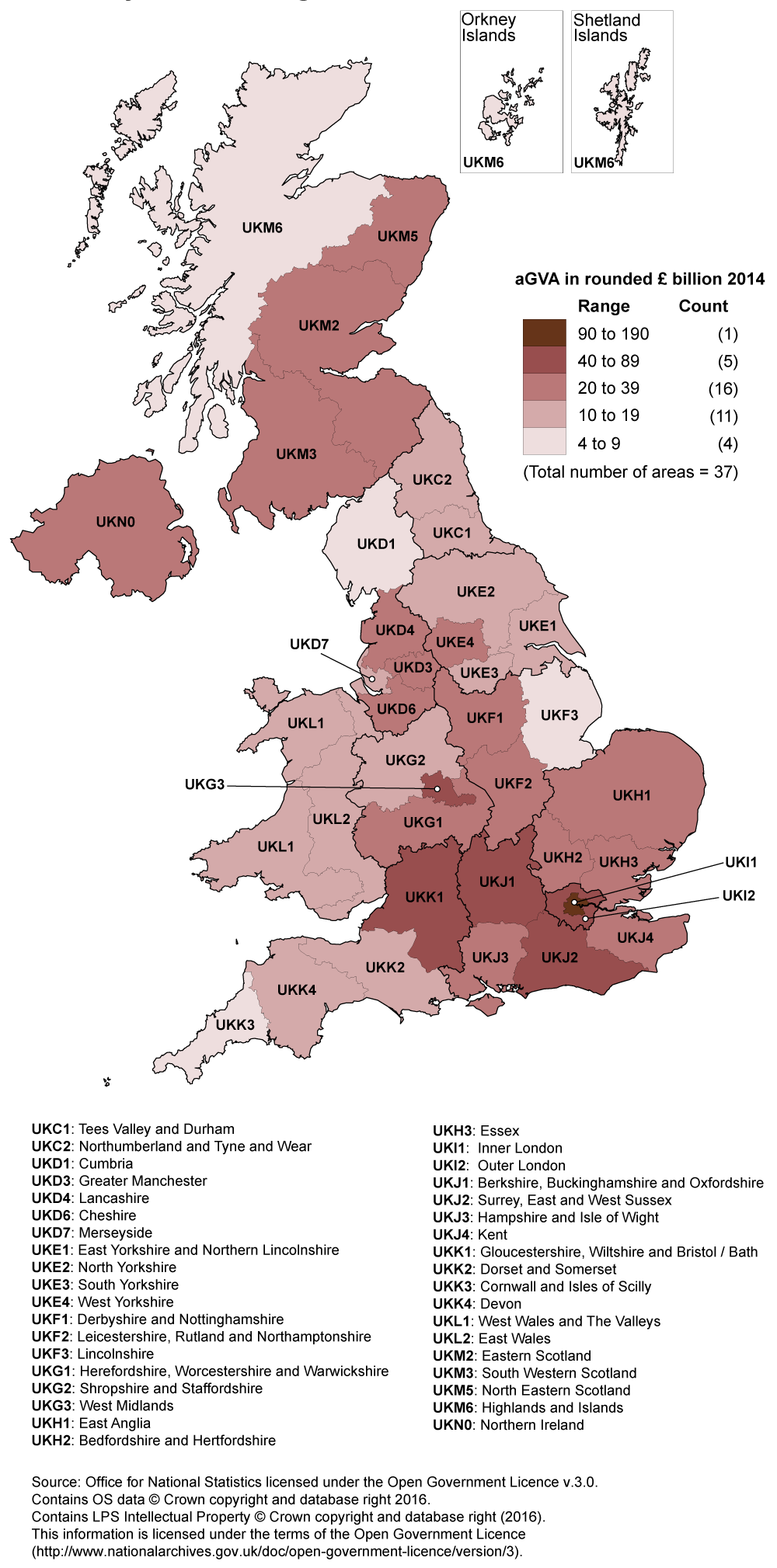

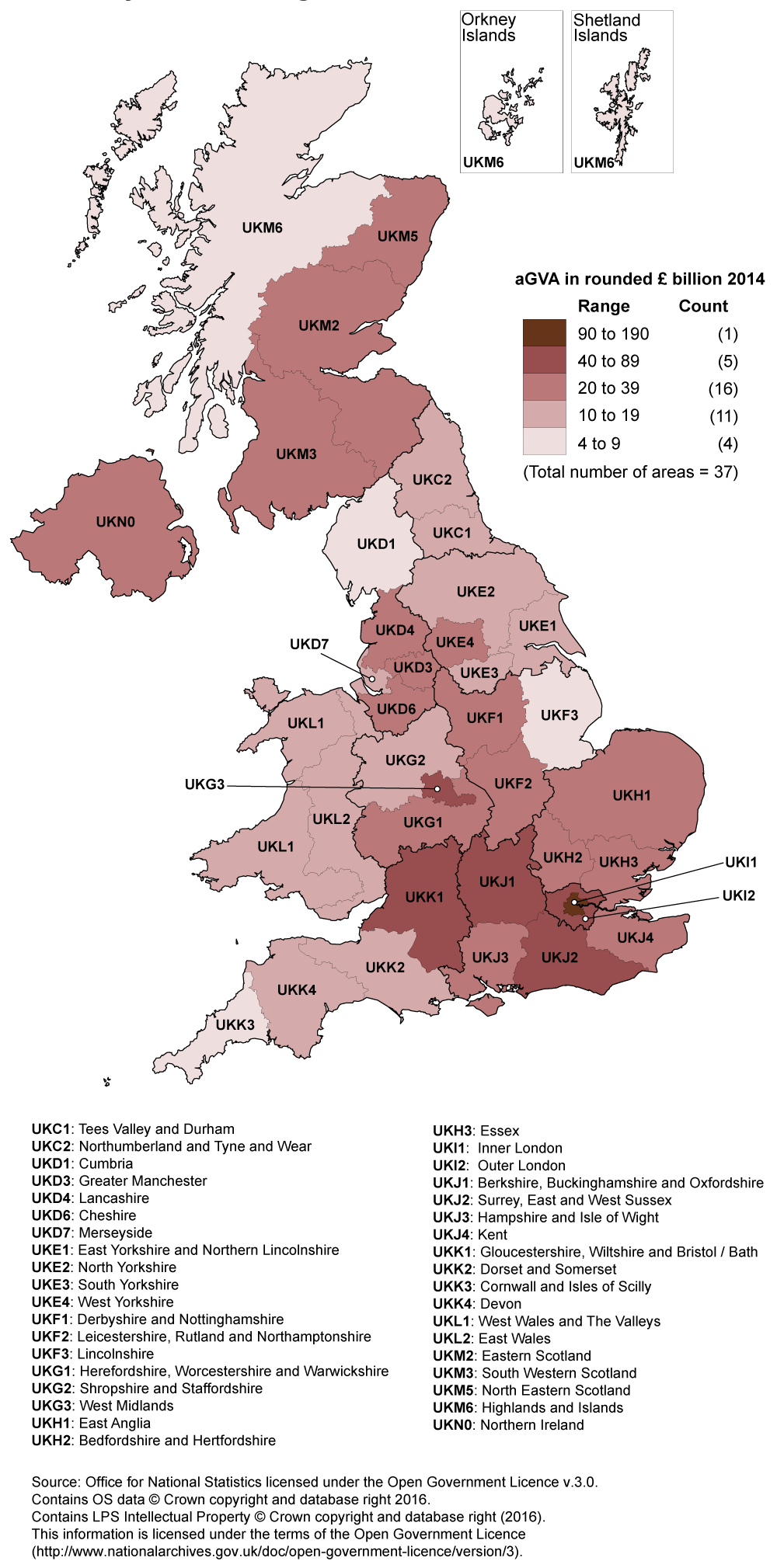

NUTS 2 sub-regional distribution of aGVA in the UK

The 12 statistical regions of the UK as mentioned previously refer to the NUTS 1 European regions (Nomenclature for Territorial Units for Statistics, level 1). These regions can be further subdivided to NUTS level 2 which has 37 sub-regions in the UK.

This greater level of detail shows where the aGVA within the NUTS 1 regions is geographically concentrated (see Figure 5). The largest sub-regions in the UK non-financial business economy, in terms of total local aGVA, were predominantly in London and the South:

Inner London (UKI1) with 17.5% of the UK total

Outer London (UKI2) with 8.1% of the UK total

Berkshire, Buckinghamshire and Oxfordshire (UKJ1) with 5.9% of the UK total

Surrey, East and West Sussex (UKJ2) with 4.4% of the UK total

Gloucestershire, Wiltshire and Bristol and Bath (UKK1) with 3.8% of the UK total

Figure 5: UK non-financial business economy, local level aGVA by NUTS 2 region

2014

Source: Office for National Statistics

Download this image Figure 5: UK non-financial business economy, local level aGVA by NUTS 2 region

.png (376.0 kB) .png (376.0 kB){kind=link}

In terms of the UK’s £89.7 billion aGVA growth between 2013 and 2014, 25 sub-regions showed a combined increase of £100.0 billion, with just under two-thirds concentrated within 3 sub-regions (see Figure 6):

- Inner and Outer London (UKI1 and UKI2)

- Cheshire (UKD6)

There were 12 sub-regions that showed a combined fall in aGVA of £10.3 billion, with the largest falls in:

- North Eastern Scotland (UKM5)

- Eastern Scotland (UKM2)

- Derbyshire and Nottinghamshire (UKF1)

While Figure 4 shows there is a £5.5 billion fall in aGVA for Scotland as a whole between 2013 and 2014, Figure 6 shows it is concentrated in North Eastern and Eastern Scotland (and to a lesser extent in the Highlands and Islands), while there is small growth of £1.1 billion in aGVA for South Western Scotland.

Figure 6: UK non-financial business economy, local level aGVA change by NUTS 2 region

2013 to 2014

Source: Office for National Statistics

Download this chart Figure 6: UK non-financial business economy, local level aGVA change by NUTS 2 region

Image .csv .xlsTo help identify the geography of each of the 37 NUTS 2 sub-regions, click on this searchable PDF map (841.8 Kb Pdf).

Nôl i'r tabl cynnwys5. Non-financial services, Sections H to S (part)

Between 2013 and 2014, turnover in the Non-financial services sector has grown by 4.6% (£52.6 billion). With purchases decreasing by 0.1% (£0.8 billion), this resulted in an aGVA increase of 10.5% (£57.8 billion). For further details on the components of aGVA see Calculation of gross value added estimates in background note 9.

This was the fifth consecutive annual increase in aGVA, with the 10.5% growth rate between 2013 and 2014 the second largest since the start of the recession in 2008.

The largest contribution to the growth between 2013 and 2014 came from Professional, scientific and technical activities (Section M), which increased by 11.2% (£16.4 billion): a second consecutive year of growth following a small fall in aGVA between 2011 and 2012.

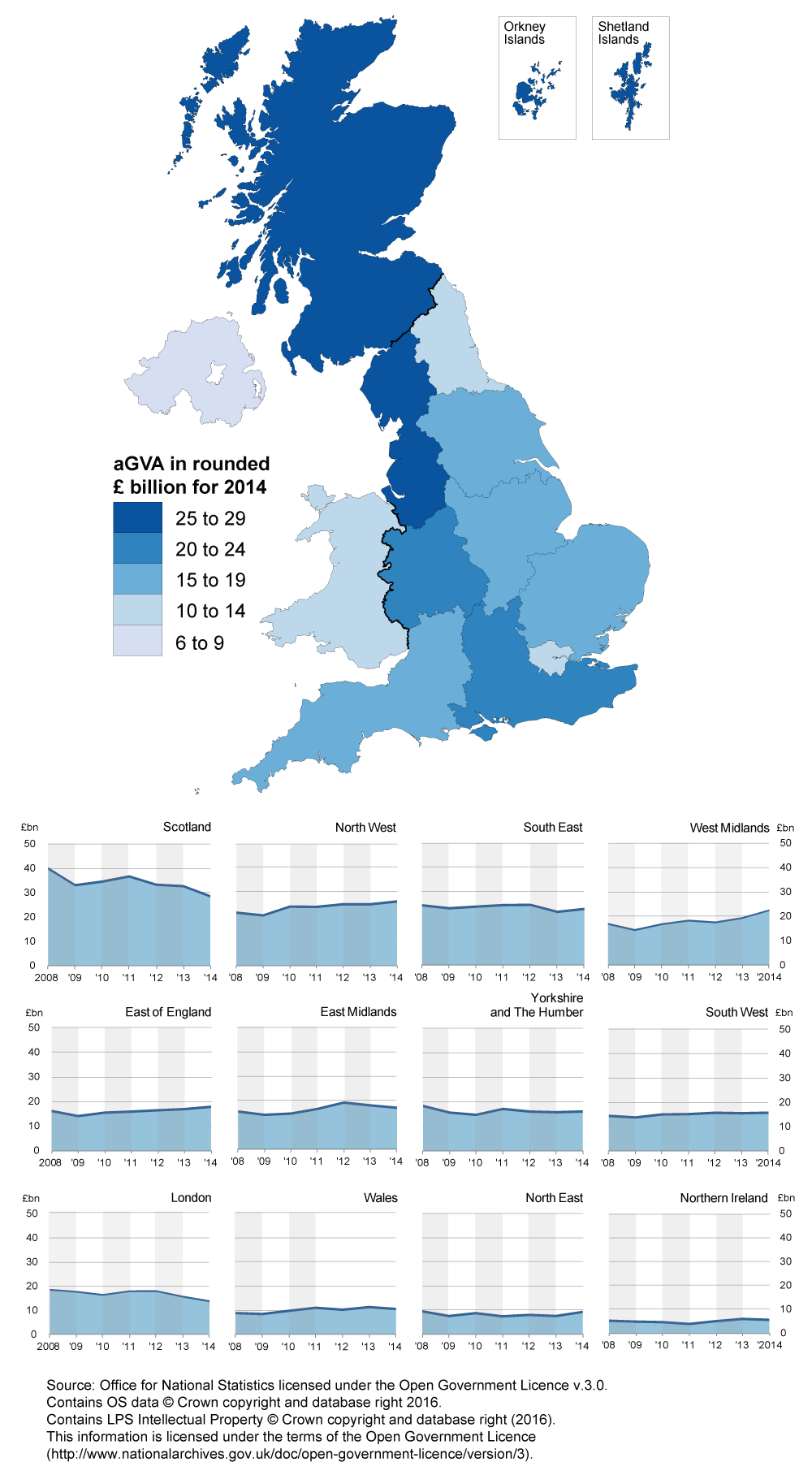

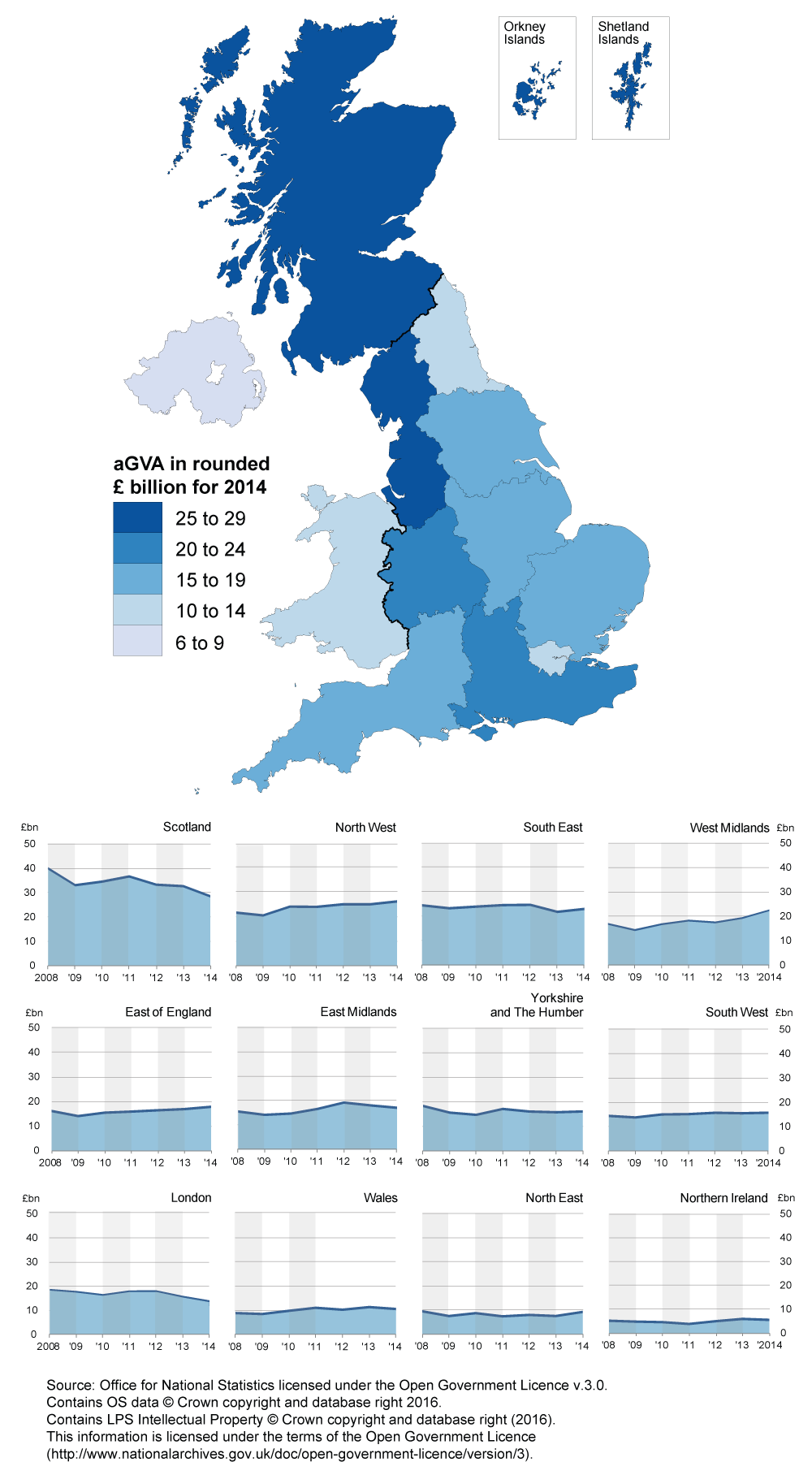

London (£205.6 billion) and the South East (£98.1 billion) made the largest contribution to aGVA in the Non-financial services sector in 2014 (see Figure 7).

Figure 7: UK non-financial services, local level aGVA by NUTS 1 region

2008 to 2014

Source: Office for National Statistics

Notes:

- Excludes Financial and insurance; Public administration and defence; Public provision of Education; Public provision of Health and all medical and dental practice activities

Download this image Figure 7: UK non-financial services, local level aGVA by NUTS 1 region

.png (215.3 kB) .xls (33.3 kB){kind=link}

Of the 12 regions, 10 have contributed to growth in the Non-financial services sector in 2014. London, the North West and the South East made the largest contributions to aGVA growth, with the only decreases in aGVA in Scotland and Wales. Despite the latter, the aGVA for all regions remains above the 2008 level (see Figure 8).

Arts, entertainment and recreation (Section R), contributes to the aGVA change in many of the regions between 2013 and 2014. However, the data for Section R (and Division 92 – Gambling and betting activities in particular) should be treated with caution, as the introduction of additivity within the purchases apportionment methodology (PAM) for 2012 onwards, has meant an increase in the volatility of the estimates at this level. For further details on work to make improvements to the methodology and estimates, to reduce this impact while maintaining the additivity, see background note 1.

London

London made the largest contribution to growth in Non-financial services’ aGVA between 2013 and 2014, with a rise of 19.5% (£33.6 billion) for the region to £205.6 billion. This is a continuation of the recovery of aGVA seen between 2009 and 2013.

The 3 main sectors driving growth between 2013 and 2014 were Arts, entertainment and recreation (Section R); Professional, scientific and technical activities (Section M); and Information and communication (Section J), contributing £9.1, £7.0 and £6.5 billion respectively to the growth in London’s Non-financial services sector aGVA.

The increase within the Arts, entertainment and recreation activities was driven by Gambling and betting activities (Division 92).

For the Professional, scientific and technical activities the increase was driven by Activities of head offices; management consultancy activities (Division 70). The growth shown by the ABS links to the Management Consultancies Association summary report for 2015, which reported strong growth in 2014 with an 8.4% increase in fee income.

Within Information and communication, the increase was driven by Computer programming, consultancy and related activities (Division 62), where across the UK general increases in business activity were reported. The industry as a whole, which includes the development of mobile phone applications, has shown consistent growth of above 5.0% in each of the last 3 years. The addition of mobile phone applications to the CPI and RPI Basket of Goods and Services, 2011 and increase in internet use on mobile devices indicates this activity has been increasing in importance in recent years. The Bank of England’s agents’ summary of business conditions suggests that some of the increase in demand for IT services may have come “from the finance sector and increased interest in cloud services from most sectors”.

North West

The North West made the second largest contribution to aGVA growth in the Non-financial services sector between 2013 and 2014, with a rise of 11.8% (£5.6 billion) for the region.

In the North West, Non-financial services recorded 6 consecutive years of annual growth above the level recorded in 2008, and continues to be both the dominant sector in terms of total aGVA contribution and growth in the region.

The 3 main sectors causing growth in the North West’s Non-financial services were Professional, scientific and technical activities (Section M); Administrative and support service activities (Section N); and Arts, entertainment and recreation (Section R), contributing £1.7, £1.3 and £1.2 billion respectively to the increase in aGVA.

South East

The South East contributed £5.5 billion to total aGVA growth in Non-financial services between 2013 and 2014, a rise of 6.0% for the region. This is a continuation of the recovery seen between 2008 and 2013 and the sixth consecutive annual increase in the region.

The Non-financial services’ growth in aGVA in the South East was driven by the increase in Professional, scientific and technical activities (Section M), which accounted for just over a third of the total growth in the sector.

The largest increase in aGVA within Professional, scientific and technical activities was seen in Activities of head offices; management consultancy activities (Division 70) which increased by £1.2 billion to £10.4 billion. The growth shown nationally in Division 70 by the Annual Business Survey (ABS) links to the Management Consultancies Association summary report for 2015, which reported strong growth in 2014 with an 8.4% increase in fee income.

Scotland

Scotland’s Non-financial services had a fall of £1.2 billion in aGVA between 2013 and 2014, a fall of 3.0% for the region. This follows 3 consecutive years of growth.

The Non-financial services’ decline in aGVA in Scotland was led by Arts, entertainment and recreation (Section R). The largest decrease within the sector was seen in Gambling and betting activities (Division 92), which decreased by £2.7 billion to £0.6 billion.

Figure 8: UK non-financial services, local level aGVA change by NUTS 1 region

2008 to 2014

Source: Office for National Statistics

Notes:

- Excludes Financial and insurance; Public administration and defence; Public provision of Education; Public provision of Health and all medical and dental practice activities.

Download this chart Figure 8: UK non-financial services, local level aGVA change by NUTS 1 region

Image .csv .xls6. Distribution, Section G

Turnover in the Distribution sector decreased between 2013 and 2014 by 1.9% (£28.9 billion). With purchases also decreasing by 3.7% (£48.7 billion), this resulted in an increase in aGVA of 13.4% (£21.9 billion). For further details on the components of aGVA see Calculation of gross value added estimates in background note 9.

This is the third consecutive year of growth for the sector, with aGVA above the level seen in 2008 for the first time.

Out of the 3 divisions in the Distribution sector, 2 contributed to the aGVA growth between 2013 and 2014, with the largest contribution of 35.5% (£22.3 billion) from Wholesale trade (except of motor vehicles and motorcycles) (Division 46) followed by Motor Trades (Wholesale and Retail) (Division 45) with 8.9% (£2.3 billion). The only decrease in aGVA is within the Retail trade (except of motor vehicles and motorcycles) with a fall of 3.7% (£2.8 billion) between 2013 and 2014.

At the regional level, London (£43.9 billion) and the South East (£31.9 billion) continue to make the largest contribution to Distribution sector aGVA in 2014 (see Figure 9).

Figure 9: UK distribution, local level aGVA by NUTS 1 region

2008 to 2014

Source: Office for National Statistics

Download this image Figure 9: UK distribution, local level aGVA by NUTS 1 region

.png (228.3 kB) .xls (32.3 kB){kind=link}

Of the 12 regions, 8 saw a rise in Distribution sector aGVA between 2013 and 2014, with the largest contributions coming from London and the South East (see Figure 10). The Wholesale industry shows the largest contribution to growth in London while the Motor Trades industry had the largest growth in the South East.

London

London contributed £19.0 billion to the increase in aGVA in the Distribution sector between 2013 and 2014, a rise of 76.8% for the region. This is the third consecutive year of growth in aGVA for the Distribution sector within the region and brings aGVA above the level recorded in 2008 for the first time.

The largest increase was in Wholesale trade (except of motor vehicles and motorcycles) rising by 180.2% (£17.8 billion). Businesses across the UK cited the fall in oil prices during 2014 as the reason for their fall in turnover and purchases (and the resulting rise in aGVA).

South East

The South East contributed £1.3 billion to the increase in UK Distribution aGVA between 2013 and 2014, a rise of 4.3% for the region. This is a continuation of recovery seen between 2009 and 2013 and the fifth consecutive annual increase in the region.

Out of the 3 Distribution divisions, 2 contributed to the regions aGVA growth. The largest contribution of 24.6% (£1.5 billion) to growth was from Motor Trades (Wholesale & Retail) followed by Wholesale trade (except of motor vehicles and motorcycles) contributing a further 0.9% (£0.1 billion).

Figure 10: UK distribution, local level aGVA change by NUTS 1 region

2008 to 2014

Source: Office for National Statistics

Download this chart Figure 10: UK distribution, local level aGVA change by NUTS 1 region

Image .csv .xls7. Construction, Section F

Turnover in the Construction sector increased by 10.5% (£20.4 billion) between 2013 and 2014 and purchases increased by 11.1% (£13.6 billion) over the same period. Together with increases in stocks and taxes, these have combined to increase aGVA by 13.0% (£9.5 billion) over the period. For further details on the components of aGVA see Calculation of gross value added estimates in background note 9.

This is the fourth consecutive year of growth for the Construction sector and brings aGVA to a level above that recorded in 2008 for the first time.

Of the 3 divisions within the Construction sector, 2 contributed to the aGVA growth between 2013 and 2014, with the largest contribution from Construction of building (Division 41) increasing by 22.5% (£6.0 billion). As was the case in the previous 2 years, the main reason for the growth in aGVA was in the Development of building projects across the UK. Specialised construction trades (Division 43) also contributed to the aGVA growth increasing by 11.2% (£3.8 billion).

At the regional level, London (£15.1 billion), the South East (£13.5 billion) and the East of England (£10.2 billion) made the largest contributions to aGVA in the Construction sector in 2014 (see Figure 11).

Figure 11: UK construction, local level aGVA by NUTS 1 region

2008 to 2014

Source: Office for National Statistics

Download this image Figure 11: UK construction, local level aGVA by NUTS 1 region

.png (218.5 kB){kind=link}

Of the 12 regions, 11 saw increases in aGVA in the Construction sector between 2013 and 2014. The largest increases were in the East of England and the South East (see Figure 12). In the East of England the largest growth was spread throughout the 3 construction divisions, while in the South East the growth was dominated by an increase in Construction of buildings (Division 41).

East of England

The East of England contributed 23.1% (£1.9 billion) to the growth in UK aGVA between 2013 and 2014. The largest growth was within Construction of buildings (Division 41), which grew by 28.4% (£0.8 billion), and Specialised construction trades (Division 43), which grew by 18.1% (£0.7 billion).

This is a continuation of recovery seen between 2008 and 2013 and the sixth consecutive annual increase in the region.

South East

The South East contributed 13.6% (£1.6 billion) to the growth in UK aGVA between 2013 and 2014, with the dominant increase in Construction of buildings (Division 41), which grew by 30.8% (£1.3 billion) and is the industry’s fourth consecutive year of increase within the region.

Figure 12: UK construction, local level aGVA change by NUTS 1 region

2008 to 2014

Source: Office for National Statistics

Download this chart Figure 12: UK construction, local level aGVA change by NUTS 1 region

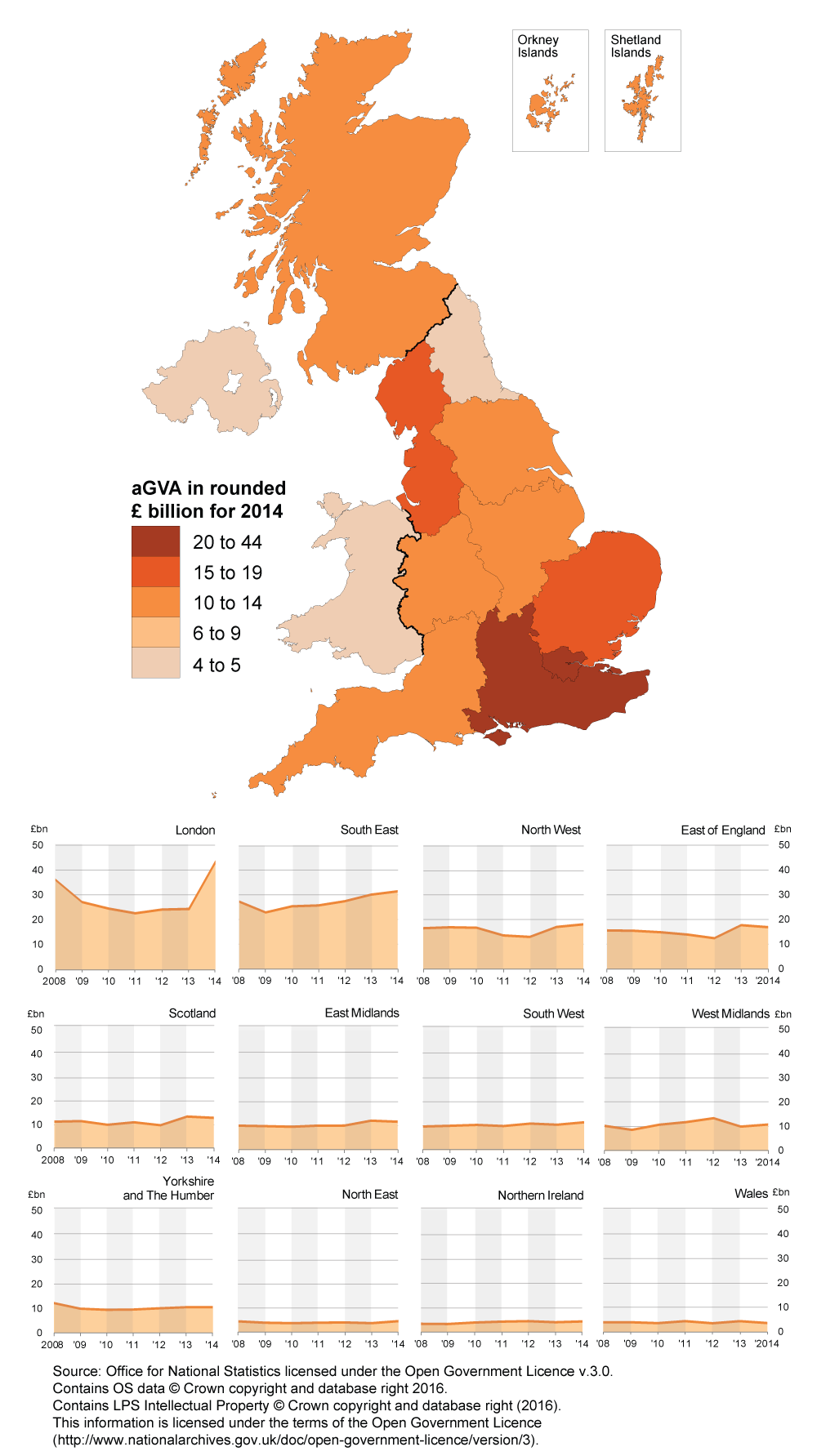

Image .csv .xls8. Production, Sections B to E

Purchases in the Production sector increased between 2013 and 2014 by 0.5% (£2.3 billion) while turnover decreased by 0.1% (£0.8 billion), with taxes and stocks change also showing a decrease over this period. This has resulted in a small increase in aGVA of 0.2% (£0.4 billion). For further details on the components of aGVA see Calculation of gross value added estimates in background note 9.

Despite the rise in aGVA between 2013 and 2014 the aGVA for the Production sector remains below the level recorded in 2008.

Of the 4 industrial sections, 3 combined to increase Production aGVA by £6.6 billion with Manufacturing (Section C) providing the largest increase of 3.2% (£4.7 billion). This increase is offset by a decrease within Mining and quarrying (Section B) of 27.4% (£6.2 billion).

The rise in Manufacturing aGVA is predominantly within Manufacture of motor vehicles, trailers and semi-trailers (Division 29), with a rise of 19.8% (£2.8 billion). Refer to manufacturing commentary for the West Midlands below for further detail.

Both the Manufacture of fabricated metal products, except machinery and equipment (Division 25); and Manufacture of food products (Division 10) contribute a further £1.2 billion each to the overall increase in aGVA.

The fall in Mining and quarrying aGVA is being dominated by Extraction of crude petroleum and natural gas (Division 06) with a decrease of 33.3% (£6.1 billion).

At the regional level, Scotland (£29.0 billion), the North West (£26.5 billion) and the South East (£23.4 billion) made the largest contributions to Production sector aGVA in 2014, (see Figure 13).

Figure 13: UK production, local level aGVA by NUTS 1 region

2008 to 2014

Source: Office for National Statistics

Download this image Figure 13: UK production, local level aGVA by NUTS 1 region

.png (230.7 kB) .xls (27.1 kB){kind=link}

Within the Production sector, 7 of the 12 regions showed a rise in aGVA between 2013 and 2014, with the largest increases in the West Midlands and the North East. The largest decrease was in Scotland, followed by London (see Figure 14).

West Midlands

The aGVA in the West Midlands has risen by £3.1 billion in the Production sector between 2013 and 2014, a rise of 15.8% for the region. This is a continuation of recovery after a slight fall between 2011 and 2012.

The aGVA increase is dominated by the rise in Manufacturing (Section C), mainly in Manufacture of motor vehicles, trailers and semi-trailers (Division 29). This industry shows a rise of £1.8 billion in aGVA between 2013 and 2014, a rise of 43.1%, with an increase in the volume of cars being sold reported by some businesses contributing to the rise. (Refer to manufacturing industries commentary for further detail).

North East

Production sector aGVA in the North East has risen by £1.7 billion between 2013 and 2014, a rise of 21.5% for the region, but remains at a level lower than that recorded in 2008.

The aGVA increase is led by a rise in Manufacturing (Section C), mainly in Manufacture of fabricated metal products, except machinery and equipment (Division 25) which has increased by 58.2% (£0.4 billion). The second largest sector increase is within Mining and quarrying (Section B), where aGVA in Extraction of crude petroleum and natural gas (Division 06) has increased, with businesses reporting a positive outcome to new projects as contributing to the rise.

Scotland

Scotland’s Production sector aGVA fell by £4.2 billion between 2013 and 2014, a fall of 12.6% for the region. This is the third consecutive year in decline in 2014, which means aGVA for the region has still not recovered to the level reported in 2008. This is despite growth of £1.3 billion in its Manufacturing (Section C) sector.

The aGVA decrease was mainly in Mining and quarrying (Section B), with Extraction of crude petroleum and natural gas (Division 06) falling by 42.0%: a decrease of £5.4 billion. Division 06 is an important industry in Scotland, representing 13.9% of Scotland’s total aGVA in 2013, falling to 8.6% in 2014. A potential factor behind this decrease was the sharp fall in commodity prices in the second half of 2014. For example, as reported in Figure 6 of our Economic Review: September 2015, crude oil prices fell from an average of £69.72 per barrel between 2011 and 2013 to £31.78 at the start of 2015. This is also supported by the Department of Energy and Climate Change (DECC) in Table 4.1.1 of their monthly release on fuel prices. Another contributing factor may be the slow-down in growth of emerging economies, which fell from 5.0% in 2013 to 4.6% in 2014 as reported by the International Monetary Fund in their July 2015 release of the World Economic Outlook.

Figure 14: UK production, local level aGVA change by NUTS 1 region

2008 to 2014

Source: Office for National Statistics

Download this chart Figure 14: UK production, local level aGVA change by NUTS 1 region

Image .csv .xls9. Manufacturing, Section C

Turnover in the Manufacturing sector increased between 2013 and 2014 by 1.3% (£6.8 billion). Purchases also increased, rising by 1.6% (£5.3 billion), which, when combined with decreases in both stocks and taxes of 43.8% (£0.7 billion) and 12.0% (£3.0 billion) respectively, has resulted in an increase in aGVA of 3.2% (£4.7 billion).

At the regional level, the North West (£22.0 billion), the West Midlands (£18.2 billion) and the South East (£16.1 billion) made the largest contributions to Manufacturing aGVA in 2014 (see Figure 15).

Figure 15: UK manufacturing, local level aGVA by NUTS 1 region

2008 to 2014

Source: Office for National Statistics

Notes:

- Data in the South East and the East of England for the years 2009 to 2012 have been suppressed to avoid disclosure.

Download this image Figure 15: UK manufacturing, local level aGVA by NUTS 1 region

.png (225.6 kB){kind=link}

Within the Manufacturing sector, 8 of the 12 regions showed a rise in aGVA between 2013 and 2014, with the largest increase of £2.7 billion in the West Midlands, followed by £1.3 billion in Scotland (see Figure 16).

West Midlands

The West Midlands contributed £2.7 billion to the total aGVA increase in Manufacturing between 2013 and 2014, a rise of 17.7% for the region. This is the fifth consecutive year that Manufacturing aGVA in the region has been above the level reported in 2008, despite a small fall between 2011 and 2012.

The aGVA increase is dominated by the rise seen in Manufacture of motor vehicles, trailer and semi trailers (Division 29). This industry shows an increase of 43.1% (£1.8 billion) in aGVA between 2013 and 2014.

Overall the increase in this industry for 2014 can again be attributed to the increase in production, sales and exports of cars, in particular high-end and luxury vehicles.

Our Economic Performance of the UK’s Motor Vehicle Manufacturing Industry release says growth in this industry has been largely due to the continued growth in exports of motor vehicles to countries outside the EU. The non-EU export market has seen growth for the last 6 years. Exports to non-EU countries are growing at a faster rate than exports to EU countries; this strong demand for exported UK cars is confirmed by reports from the car manufacturing trade body, the Society of Motor Manufacturers and Traders (SMMT). The SMMT report covering 2014 shows that the number of vehicles produced in the UK fell rapidly during the economic downturn, from 1.8 million in 2007 to 1.1 million in 2009. The industry has now partially recovered with 1.6 million vehicles being produced in 2014. Car output, the largest component of Division 29, rose to 1.53 million units, its highest level since 2007.

Figure 16: UK manufacturing, local level aGVA change by NUTS 1 region

2008 to 2014

Source: Office for National Statistics

Notes:

- Data in the South East and the East of England for the years 2008 to 2013 have been suppressed to avoid disclosure

Download this chart Figure 16: UK manufacturing, local level aGVA change by NUTS 1 region

Image .csv .xls10. Agriculture (part), Forestry and Fishing, Section A

The ABS covers only hunting, forestry, fishing and the support activities to agriculture. Commentary is therefore limited because the sector’s size in terms of economic output, as measured by the ABS, is small in comparison to the other sectors of the UK non-financial business economy. However, data for these parts of Section A can be found in the reference tables linked to this bulletin.

The other parts of agriculture, which include crop and animal production, are covered in the Agriculture in the United Kingdom release published annually by the Department for Environment, Food and Rural Affairs (DEFRA).

Note that the values quoted here for Section A are in £ millions.

The part of Section A covered at ABS local level showed a rise in turnover and purchases of 6.8% (£251 million) and 9.0% (£200 million) respectively between 2013 and 2014. Together with a rise in stocks and a decrease in taxes, these movements have combined to increase aGVA by 6.3% (£102 million) over the period. For further details on the components of aGVA see Calculation of gross value added estimates in background note 9.

The region contributing most to this growth between 2013 and 2014 was Scotland with an £88 million increase in aGVA. This was the largest contribution, with the next highest contributions from the West Midlands (£11 million) and the South West (£11 million).

Nôl i'r tabl cynnwys11. Revisions to 2013 ABS regional data

Due to the need to balance timeliness of the data with the accuracy, in-line with the ABS revisions policy, ABS regional results for 2013 were published in July 2015 with further quality assurance then leading to planned revisions to the data in this release.

These revisions usually arise from the receipt of additional data and the further validation and revision of existing data by businesses responding to the ABS, which may include restructures that can result in data being reallocated to a different industry. When compared with the ABS regional results published on 23 July 2015, the revised 2013 data in this release shows minimal revision for the UK non-financial business economy.

At the UK level, turnover generated by local activity of businesses for 2013 were revised upwards by 0.1% (£2.5 billion) and purchases revised downward by 0.1% (£1.6 billion). This resulted in aGVA upward revision of 0.1% (£0.8 billion).

Last year, the introduction of a change to the purchases apportionment process significantly contributed to the 2012 revised data. This year, with the methodology being consistent with the previous year, the 2013 revisions are greatly reduced. An impact assessment of this methodology change (at region and SIC division level) was also published.

Revisions to aGVA at the sub-national level are mixed, with 8 of the 12 regions showing upward revisions totalling £5.3 billion, with the largest revision in the East of England. This was offset by downward revisions totalling £4.5 billion in the 4 remaining regions (see Figure 17).

Figure 17: UK non-financial business economy, local level revisions by NUTS 1 region

2013

Source: Office for National Statistics

Download this chart Figure 17: UK non-financial business economy, local level revisions by NUTS 1 region

Image .csv .xls12. Quality and methodology

The Annual Business Survey Quality and Methodology Information document contains important information on:

- the strengths and limitations of the data

- the quality of the output: including the accuracy of the data, how it compares with related data

- uses and users

- how the output was created