Cynnwys

- Main points

- Overview

- Your views matter

- Interactive Wheel for the UK non-financial business economy

- UK non-financial business economy, Sections A-S (part)

- Non-financial service industries, Sections H-S (part)

- Production industries, Sections B-E

- Distribution industries, Section G

- Construction industries, Section F

- Agriculture (part), forestry and fishing, Section A

- Background notes

- Methodoleg

1. Main points

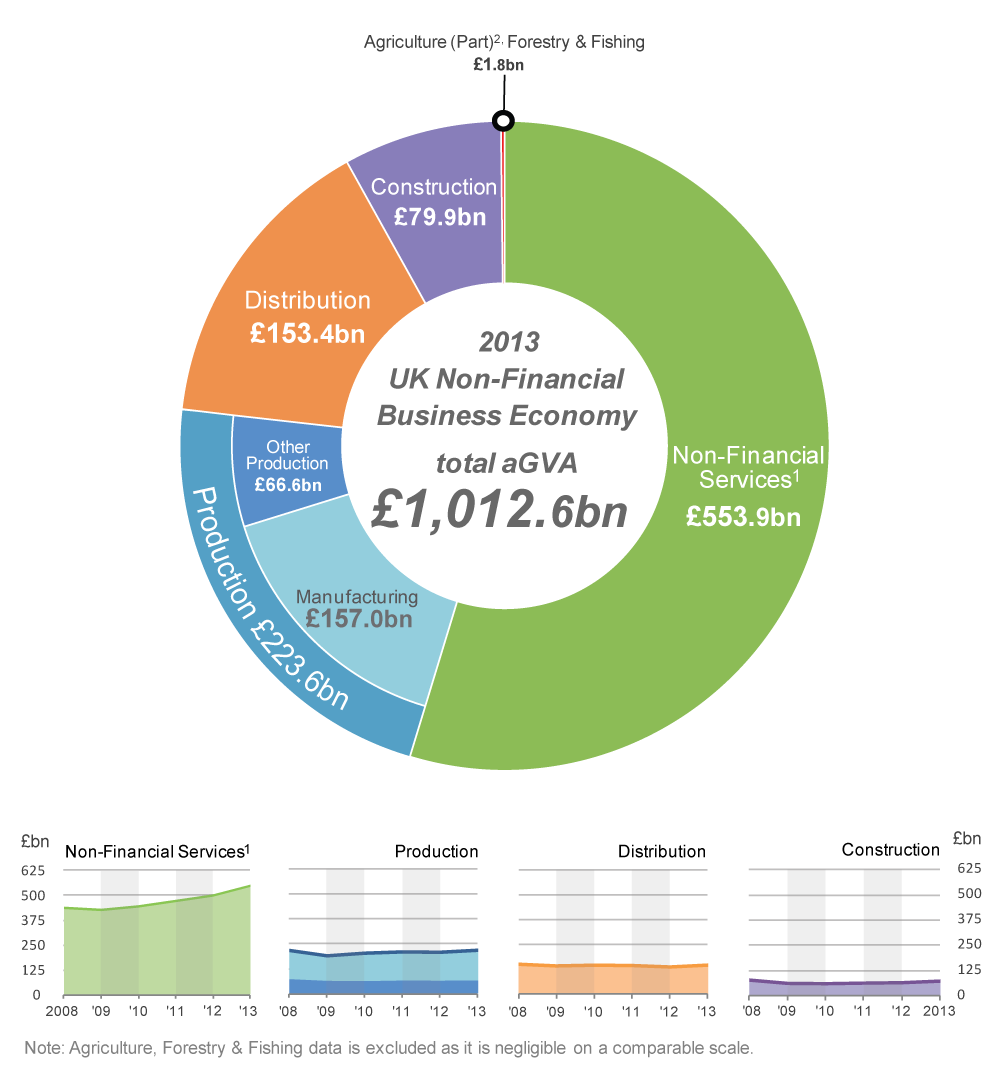

In 2013 the approximate Gross Value Added at basic prices (aGVA) of the UK Non-Financial Business Economy reached £1 trillion for the first time, with an estimated value of £1,012.6 billion. This amount represents the income generated by businesses in the UK, less the cost of goods and services used to create this income

Between 2012 and 2013, aGVA increased by 8.1% (£76.3 billion), the largest annual percentage increase since 1997. This increase is a continuation of the recovery seen between 2009 and 2012 and takes aGVA to a level 11.3% (£103.0 billion) above that seen in 2008, at the start of the recession

For the first year since the start of the recession in 2008 all sectors of the UK Non-Financial Business Economy, as measured by the Annual Business Survey (ABS), saw growth in aGVA between 2012 and 2013

The Non-Financial Service sector, which accounts for over half (54.7%) of aGVA in the UK Non-Financial Business Economy, contributed most to the increase in aGVA. The sector’s increase of 9.7% (£48.9 billion) between 2012 and 2013 was the fourth consecutive annual increase, taking it to 25.1% (£111.1 billion) above the level seen in 2008

The Production sector, which accounts for just over a fifth of aGVA in the UK Non-Financial Business Economy, saw an increase in aGVA of 4.7% (£10.0 billion) between 2012 and 2013. The increase sees Production sector aGVA above the level in 2008 for the first time

The Distribution sector, which accounts for just over a seventh of aGVA in the UK Non-Financial Business Economy, also saw an increase in aGVA of 6.5% (£9.3 billion) between 2012 and 2013. This follows two consecutive annual decreases between 2010 and 2012, with the level in 2013 remaining below the level seen in 2008

The Construction sector, which accounts for 7.9% of aGVA in the UK Non-Financial Business Economy, saw an increase in aGVA of 10.7% (£7.7 billion) between 2012 and 2013. This is the third consecutive year of growth, which leaves Construction aGVA £4.9 billion lower than the level in 2008

2. Overview

Estimate of the size and growth of the UK Non-Financial Business Economy for 2013 as measured by the Annual Business Survey (ABS), are presented in this release. It is the key resource for understanding the detailed structure, conduct and performance of businesses across the UK. The release covers:

non-financial services (includes professional, scientific, communication, administrative, transport, accommodation and food, private health and education, entertainment services)

distribution (includes retail, wholesale and motor trades)

production (includes manufacturing, oil and gas extraction, energy generation and supply)

construction

parts of agriculture (includes agricultural support services, forestry and fishing)

Together these industries represent the UK Non-Financial Business Economy and account for around two thirds of the whole economy of the UK in terms of Gross Value Added. Public administration and defence, public sector health and education, finance and farming make up the difference between the UK Non-Financial Business Economy and the whole economy.

Estimates published in this release include turnover, purchases, approximate Gross Value Added at basic prices (aGVA) and employment costs. All data are reported at current prices (effect of price changes included).

Where the recession is mentioned it refers to the contraction of Gross Domestic Product (GDP) that started in 2008, the year from which a consistent ABS time series is available. For more information about the survey see the background notes.

The ABS has a wide range of uses: for example, ABS statistics are essential contributors to the UK National Accounts, including the measurement of GDP , they are supplied to Eurostat to meet the requirements of the European Structural Business Statistics (SBS) Regulation, and are used by the devolved administrations and central and local government to monitor and inform policy development.

The ABS also recently published its Exporters and Importers, GB, 2013 and Business Ownership in the UK, 2012 releases. For other uses see background note 3.

Questions often asked of the ABS release are 'What is aGVA?' and ‘How does the measure of aGVA differ from the GVA measure in the National Accounts?’. For an overview of aGVA please see our new infographic 'What is aGVA?'. National Accounts carry out coverage adjustments, conceptual adjustments and coherence adjustments. The National Accounts estimate of GVA uses input from a number of sources, and covers the whole UK economy, whereas ABS does not include farming, financial or public sectors. ABS total aGVA is around two thirds of the National Accounts whole economy GVA because of these differences. For further information on aGVA, see background note 8. There is also a recently published article ‘ A Comparison between ABS and National Accounts Measures of Value Added’ (462.3 Kb Pdf) which provides more detail.

ONS makes every effort to provide informative commentary on the data in this release. Where possible, the commentary draws on evidence from businesses or other sources of information to help explain possible reasons behind the observed changes. However, in some places it can prove difficult to elicit detailed reasons for movements, for example, businesses may state a ‘change in the nature of business activity’. Consequently, it is not possible for all data movements to be fully explained.

Nôl i'r tabl cynnwys3. Your views matter

We constantly aim to improve this release and its associated commentary. We would welcome any feedback you might have, and would be particularly interested in knowing how you make use of these data to inform your work. Please contact us via email: abs@ons.gov.uk or telephone Jon Gough on +44 (0)1633 456720.

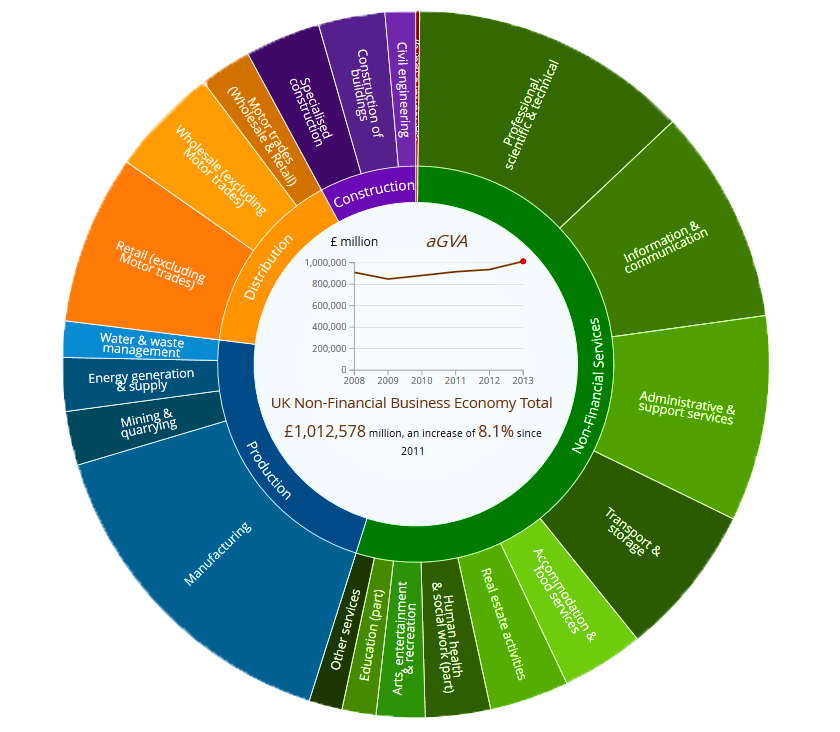

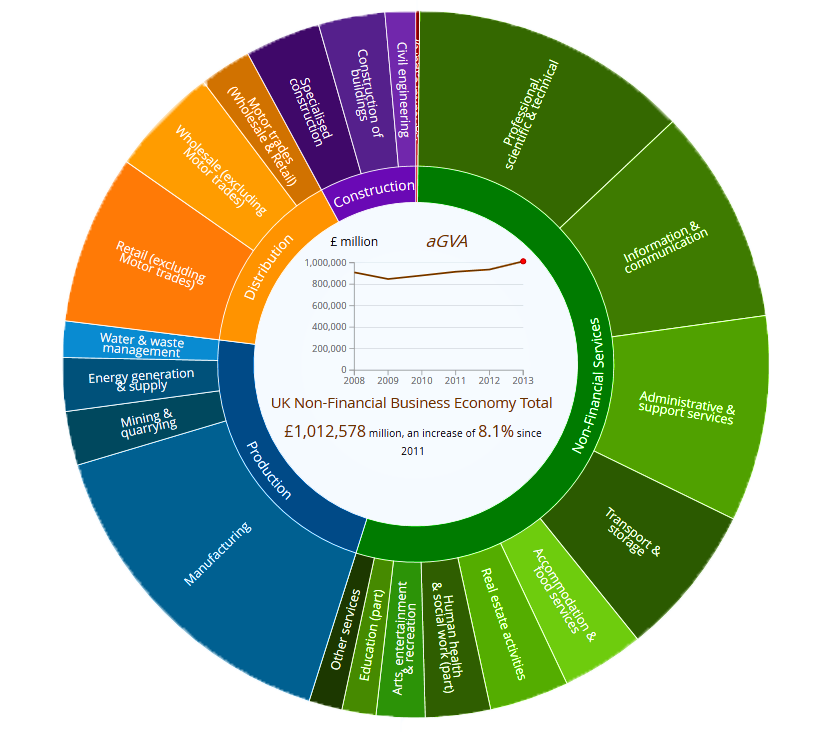

Nôl i'r tabl cynnwys4. Interactive Wheel for the UK non-financial business economy

Use the Interactive Wheel to investigate which sectors contribute most to the UK Non-Financial Business Economy. Focus on the Business Economy as a whole or each sector and switch between aGVA, Turnover and Purchases.

Interactive Wheel for the UK Non-Financial Business Economy

Download this image Interactive Wheel for the UK Non-Financial Business Economy

.png (1.8 MB){kind=link}

5. UK non-financial business economy, Sections A-S (part)

In 2013, the income generated by businesses in the UK, less the cost of goods and services used to create this income was estimated to be £1,012.6 billion. This amount represents the approximate Gross Value Added at basic prices (aGVA) of the UK Non-Financial Business Economy. Between 2012 and 2013 aGVA increased by 8.1% (£76.3 billion); a continuation of the recovery seen between 2009 and 2012. This increase resulted in aGVA reaching £1 trillion for the first time, and was 11.3% (£103.0 billion) above the level seen in 2008, at the start of the recession.

The main components of aGVA are:

turnover (the main component of income)

purchases (the main component of the consumed goods and services)

The consecutive annual increases seen in aGVA follow a similar pattern of increases in both turnover and purchases. Turnover increased by 6.8% (£225.6 billion) between 2012 and 2013, while purchases of goods, materials and services increased at a similar rate of 6.9% (£161.0 billion), resulting in an 8.1% growth in aGVA. As with aGVA, turnover and purchases were above levels seen in 2008 at the start of the recession for the third consecutive year (see Figure 1).

The recession and recovery described by the ABS between 2008 and 2013 is broadly in line with Gross Domestic Product (GDP) figures published in the National Accounts. Both the ABS aGVA estimates and the latest National Accounts GDP estimates (taken from the Preliminary Estimate for Q3 2014 show a fall between 2008 and 2009 and now four consecutive annual increases from 2009 to 2013 led by the Service sector.

A list of industries which are included in the ABS measure of the UK Non-Financial Business Economy, can be found in background note 8.

Figure 1: UK Non-Financial Business Economy(1), details of income and expenditure and resulting aGVA, 2008-2013

Provisional 2013 United Kingdom data

Source: Office for National Statistics

Notes:

- A list of industries which are included in the ABS measure of the UK Non-Financial Business Economy, can be found in background note 8

Download this chart Figure 1: UK Non-Financial Business Economy(1), details of income and expenditure and resulting aGVA, 2008-2013

Image .csv .xlsFor the first year since the start of the recession in 2008 all sectors of the UK Non-Financial Business Economy, as measured by ABS, saw growth in aGVA between 2012 and 2013 (see Figures 2 and 3).

Non-Financial Services, the largest industry sector of the UK Non-Financial Business Economy contributed most to the increase in aGVA. The Non-Financial Service sector aGVA rose by 9.7% (£48.9 billion) between 2012 and 2013, the fourth consecutive annual increase, taking aGVA to £553.9 billion.

The Production sector saw an increase of 4.7% (£10.0 billion) in aGVA following a slight fall between 2011 and 2012. This increase sees aGVA for the Production sector at £223.6 billion which is above the £222.5 billion seen in 2008, at the start of the recession, for the first time.

The Distribution sector experienced an increase in aGVA for the first time in three years, with a rise of 6.5% (£9.3 billion) between 2012 and 2013. This increase took aGVA to £153.4 billion, which is still below the £157.8 billion seen in 2008.

The Construction sector experienced growth in aGVA for the third consecutive year, increasing by 10.7% (£7.7 billion) from £72.2 billion in 2012 to £79.9 billion in 2013. However, as with the Distribution sector, aGVA still remains below the level seen in 2008 (£84.8 billion).

The Agriculture (part), forestry and fishing sector experienced the largest percentage rise in aGVA of all the sectors, with a 28.4% (£0.4 billion) increase between 2012 and 2013. At £1.8 billion, aGVA for the industry is now above the level seen in 2008 for the first time.

Figure 2: UK Non-Financial Business Economy, details of aGVA by sector, 2008-2013

Source: Office for National Statistics

Notes:

- Excludes Financial and insurance; Public administration and defence; Public provision of Education; Public provision of Health and all medical and dental practice activities

- Agriculture (part: excluding crop and animal production), forestry & fishing data are excluded from the line charts as the values are negligible on a comparable scale

Figure 3: UK Non-Financial Business Economy(1), details of aGVA growth by sector, 2008-2013

Source: Office for National Statistics

Notes:

- A list of industries which are included in the ABS measure of the UK Non-Financial Business Economy, can be found in background note 8

Download this chart Figure 3: UK Non-Financial Business Economy(1), details of aGVA growth by sector, 2008-2013

Image .csv .xls6. Non-financial service industries, Sections H-S (part)

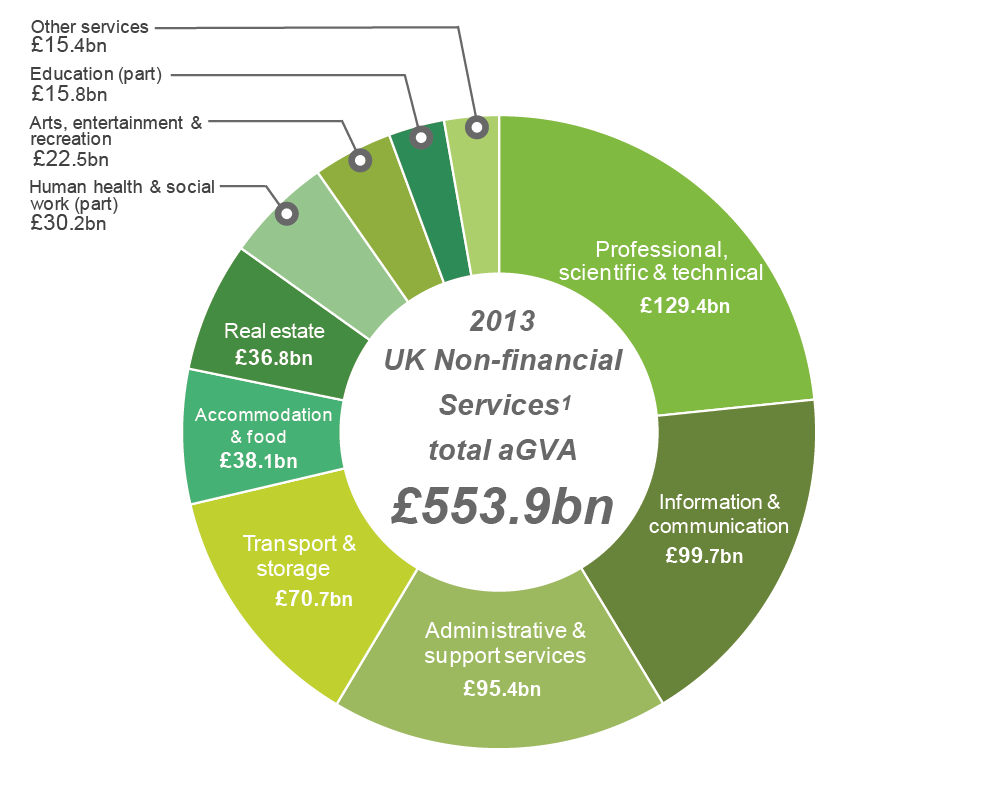

Over half (54.7%) of the estimated aGVA total of £1,012.6 billion in 2013 for the UK Non-Financial Business Economy was generated by the Non-Financial Service industries.

Between 2012 and 2013 Non-Financial Service turnover increased at a higher rate than purchases, 7.0% (£74.9 billion) compared to 5.6% (£31.3 billion). Together with a rise in stock levels and changes in subsidies and taxes, this resulted in aGVA rising by 9.7% (£48.9 billion). This is the fourth consecutive year of growth in aGVA for the sector, following the fall between 2008 and 2009. Turnover, purchases and aGVA are now well above the level seen in 2008 at the start of the recession (see Figure 4).

Figure 4: Non-Financial Services, details of turnover and purchases and resulting aGVA, 2008-2013

Source: Office for National Statistics

Notes:

- A list of industries which are included in the ABS measure of the UK Non-Financial Business Economy, can be found in background note 8

Download this chart Figure 4: Non-Financial Services, details of turnover and purchases and resulting aGVA, 2008-2013

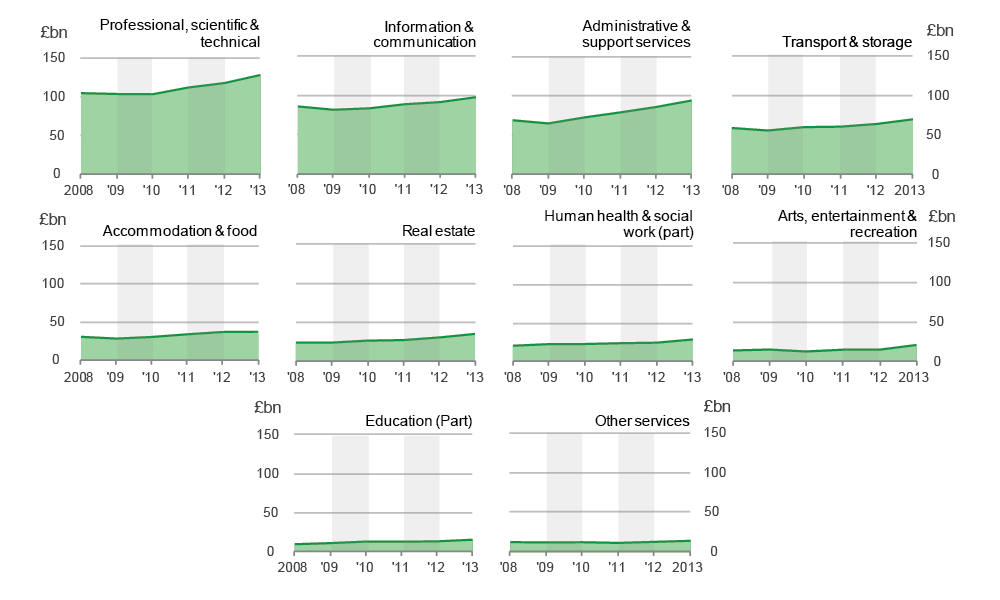

Image .csv .xlsAll of the industry sections within the Non-Financial Service sector continued to see increases in aGVA between 2012 and 2013 (see Figures 5 and 6).

Those industries which have made the largest contributions to growth are:

professional, scientific & technical activities (Section M)

administrative & support service activities (Section N)

information & communication (Section J)

arts, entertainment & recreation (Section R)

transport & storage (Section H)

These industries, which together accounted for an increase in aGVA of £30.7 billion, are described in more detail after Figure 5b.

Figure 5a: Non-financial services, details of aGVA by section, 2013

Source: Office for National Statistics

Notes:

- Excludes Financial and insurance; Public administration and defence; Public provision of Education; Public provision of Health and all medical and dental practice activities

Figure 5b: Non-Financial Services, details of aGVA by section, 2008-2013

Source: Office for National Statistics

Notes:

- Excludes Financial and insurance; Public administration and defence; Public provision of Education; Public provision of Health and all medical and dental practice activities

Professional, scientific & technical activities (Section M)

Turnover in Professional, scientific & technical activities increased by 9.9% (£20.6 billion) between 2012 and 2013, with purchases showing an increase of 13.9% (£12.5 billion). This resulted in growth of 8.6% (£10.3 billion) in aGVA, resulting in aGVA remaining above that reported for 2008 for the third consecutive year.

This broad section, which covers a range of industries from Legal & accounting activities to Advertising & market research and Veterinary activities, saw increases in aGVA in almost all its divisions between 2012 and 2013. Those having the largest impact on aGVA growth were Legal & accounting activities (Division 69) and Architectural & engineering activities; technical testing & analysis (Division 71) which between them contributed £8.3 billion to the increase in aGVA. However, Scientific Research & Development (Division 72) showed a decrease of £1.5 billion in aGVA over this period which may be due to lack of investment in research since the economic downturn.

Administrative & support services (Section N)

Between 2012 and 2013 Administrative & support services saw turnover rise by 8.9% (£15.4 billion), while purchases increased by 9.0% (£7.7 billion) leading to an aGVA increase of 9.5% (£8.3 billion).

The main industries contributing to growth within Administrative & support services were Office administrative, office support & other business support activities (Division 82) where aGVA increased by 14.1% (£2.8 billion). Employment activities (Division 78) also made a substantial contribution with an 8.9% (£2.3 billion) increase in aGVA.

Information & communication (Section J)

Turnover in Information & communication increased by 4.6% (£8.8 billion) between 2012 and 2013 which, coupled with a smaller 3.5% (£3.4 billion) increase in purchases, resulted in an increase in aGVA of 6.7% (£6.3 billion) between 2012 and 2013.

The main division causing the growth in aGVA within this section was Computer programming, consultancy & related activities (Division 62), with an increase of 14.8% (£5.9 billion) between 2012 and 2013. This increase could be attributed to growth in the UK games industry.

Arts, entertainment & recreation (Section R)

Turnover in Arts, entertainment & recreation increased by 8.4% (£9.3 billion) between 2012 and 2013, while purchases increased by 5.4% (£4.9 billion) leading to a 35.6% (£5.9 billion) rise in aGVA. This growth was driven by Gambling & betting (Division 92) where aGVA increased by a significant 64.9% (£3.4 billion). The growth in this industry is likely to be due to the types and geographical spread of the interactive entertainment industry.

Transport & storage (Section H)

Turnover in Transport & storage increased by 4.2% (£6.3 billion) between 2012 and 2013, with purchases rising by 0.5% (£0.5 billion) resulting in a 9.0% (£5.8 billion) increase in aGVA.

The main divisions contributing to aGVA growth within Transport & storage were Land transport & transport via pipelines (Division 49), and Warehousing & support activities for transportation (Division 52). Increases in this sector may be related to the effect of the internet economy. Data on the retail sector indicates that turnover from mail order and via the internet continued to increase at a higher rate than turnover from shops. An increase seen in Warehousing & support activities for transportation is likely to partly result from the storage of items ordered from the internet.

Figure 6: Non-Financial Services, details of aGVA growth by section 2008-2013

Source: Office for National Statistics

Notes:

- M - Professional, scientific and technical activities N - Administrative and support service activities J - Information and communication R - Arts, entertainment and recreation H - Transport and storage L - Real estate activities Q (part) - Human health and social work activities P (part) – Education S - Other service activities I - Accommodation and food service activities

- A list of industries which are included in the ABS measure of the UK Non-Financial Business Economy, can be found in background note 8

Download this chart Figure 6: Non-Financial Services, details of aGVA growth by section 2008-2013

Image .csv .xls7. Production industries, Sections B-E

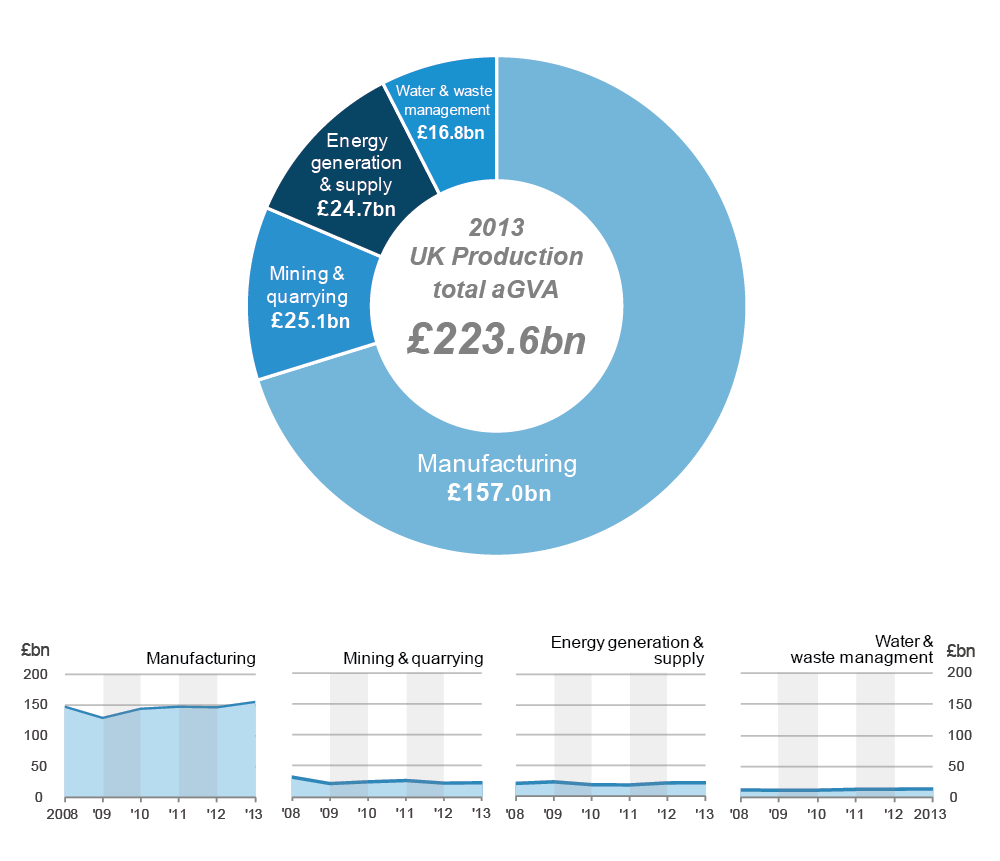

The Production sector in 2013 provided just over a fifth (22.1%) of the estimated aGVA total of £1,012.6 billion for the UK Non-Financial Business Economy.

Between 2012 and 2013 Production sector turnover and purchases increased by 2.7% (£18.9 billion) and 3.1% (£14.3 billion) respectively. Together with rises in stock levels and changes in taxes, this led to an increase in aGVA of 4.7% (£10.0 billion), which followed a slight fall between 2011 and 2012. The increase sees Production sector aGVA above the level in 2008, at the start of the recession, for the first time (see Figure 7).

Figure 7: Production, details of turnover and purchases and resulting aGVA, 2008-2013

Source: Office for National Statistics

Download this chart Figure 7: Production, details of turnover and purchases and resulting aGVA, 2008-2013

Image .csv .xlsManufacturing (Section C), which contributes 70% of Production sector aGVA, saw a rise in aGVA of 5.8% (£8.6 billion) between 2012 and 2013, and was the main reason for overall growth.

Over the same period the other sections in the Production sector: B (Mining & quarrying), E (Water & waste management) and D (Energy generation & supply), also saw increases in aGVA of 2.9% (£0.7 billion), 2.2% (£0.4 billion) and 1.1% (£0.3 billion) respectively (see Figures 8 and 9).

Figure 8: Production, details of aGVA by section, 2008-2013

Source: Office for National Statistics

Figure 9: Production, details of aGVA growth by section, 2008-2013

Source: Office for National Statistics

Download this chart Figure 9: Production, details of aGVA growth by section, 2008-2013

Image .csv .xlsManufacturing (Section C)

The divisions contributing nearly half (46.3%) of Manufacturing aGVA are (see Figure 10):

Manufacture of food products (Division 10)

Manufacture of Fabricated metal products, except machinery & equipment (Division 25)

Manufacture of motor vehicles, trailers & semi-trailers (Division 29)

Manufacture of Machinery & equipment n.e.c. (Division 28)

Manufacture of other transport equipment (Division 30)

Figure 10: Manufacturing, details of aGVA by division, 2013

Standard Industrial Classification (Revised 2007) Division

Source: Office for National Statistics

Notes:

- 10 - Food products

25 - Fabricated metal products, except machinery & equipment

29 - Motor vehicles, trailers & semi-trailers>br> 28 - Machinery & equipment n.e.c.

30 - Other transport equipment

26 - Computer, electronic & optical products

20 - Chemicals & chemical products

22 - Rubber & plastic products

33 - Repair & installation of machinery & equipment

21 - Basic pharmaceutical products & pharmaceutical preparations

18 - Printing & reproduction of recorded media

27 - Electrical equipment

24 - Basic metals

23 - Other non-metallic mineral products

32 - Other manufacturing

17 - Paper & paper products

31 - Furniture

16 - Wood & of products of wood & cork, except furniture; manufacture of articles of straw & plaiting materials

13 - Textiles

19 - Coke & refined petroleum products

14 - Wearing apparel

15 - Leather & related products

11 - Beverages

12 - Tobacco products

Download this chart Figure 10: Manufacturing, details of aGVA by division, 2013

Image .csv .xlsBetween 2012 and 2013 Manufacturing saw increases of 1.8% (£9.1 billion) in turnover and 1.2% (£4.1 billion) in purchases which, together with rises in stock levels and changes in taxes, contributed to an increase in aGVA of 5.8% (£8.6 billion).

The increase in Manufacturing aGVA was mainly in:

manufacture of motor vehicles, trailers & semi-trailers (Division 29)

manufacture of other transport equipment (Division 30)

manufacture of food products (Division 10)

repair and installation of machinery and equipment (division 33)

manufacture of basic metals (Division 24)

Together these five divisions contributed £8.3 billion to the overall £8.6 billion increase in Manufacturing aGVA (see Figures 11 and 12).

Accounting for a third of the overall manufacturing growth was Manufacture of motor vehicles, trailers & semi-trailers (Division 29), where the aGVA increase of £2.9 billion can be largely attributed to the increase in sales and, in particular, export of high-end vehicles and also hybrid cars.

New overseas contracts awarded to businesses in Manufacture of other transport equipment (Division 30) contributed to the aGVA increase of £2.2 billion.

Across Manufacturing almost two thirds (17 out of 24) of the divisions contributing to this sector experienced increases in aGVA between 2012 and 2013.

Other reasons cited by businesses as contributing to the rise in Manufacturing aGVA were businesses restructuring, the take-over of a similar business, the gaining of new contracts and reduction in purchases.

The 48.6% (£1.0 billion) decrease in aGVA for Manufacture of coke & refined petroleum products (Division 19) is caused by the level of duty paid on oil refining. Due to the small size of this division in terms of Manufacturing aGVA, annual changes should be viewed with care.

Figure 11: Manufacturing, details of aGVA growth by division, 2012-2013

Division

Source: Office for National Statistics

Notes:

- 10 - Food products

11 – Beverages

12 – Tobacco products

13 – Textiles

14 - Wearing apparel

15 - Leather & related products

16 - Wood & of products of wood & cork, except furniture; manufacture of articles of straw & plaiting materials

17 - Paper & paper products

18 - Printing & reproduction of recorded media

19 - Coke & refined petroleum products

20 - Chemicals & chemical products

21 - Basic pharmaceutical products & pharmaceutical preparations

22 - Rubber & plastic products

23 - Other non-metallic mineral products

24 - Basic metals

25 - Fabricated metal products, except machinery & equipment

26 - Computer, electronic & optical products

27 - Electrical equipment

28 - Machinery & equipment n.e.c

29 - Motor vehicles, trailers & semi-trailers

30 - Other transport equipment

31 – Furniture

32 - Other manufacturing

33 - Repair & installation of machinery & equipment

Download this chart Figure 11: Manufacturing, details of aGVA growth by division, 2012-2013

Image .csv .xls

Figure 12: Manufacturing, details of aGVA percentage growth by division, 2012-2013

Section/Division

Source: Office for National Statistics

Notes:

- 10 - Food products

11 - Beverages

12 - Tobacco products

13 - Textiles

14 - Wearing apparel

15 - Leather & related products

16 - Wood & of products of wood & cork, except furniture; manufacture of articles of straw & plaiting materials

17 - Paper & paper products

18 - Printing & reproduction of recorded media

19 - Coke & refined petroleum products

20 - Chemicals & chemical products

21 - Basic pharmaceutical products & pharmaceutical preparations

22 - Rubber & plastic products

23 - Other non-metallic mineral products

24 - Basic metals

25 - Fabricated metal products, except machinery & equipment

26 - Computer, electronic & optical products

27 - Electrical equipment

28 - Machinery & equipment n.e.c

29 - Motor vehicles, trailers & semi-trailers

30 - Other transport equipment

31 - Furniture

32 - Other manufacturing

33 - Repair & installation of machinery & equipment

Download this chart Figure 12: Manufacturing, details of aGVA percentage growth by division, 2012-2013

Image .csv .xlsOther production (Sections B, D-E)

This sector consists of Mining & quarrying (Section B, which includes oil and gas extraction), Energy generation & supply (Section D) and Water supply, sewerage, waste management and remediation activities (Section E). The sector saw increases in turnover and purchases of 5.3% (£9.9 billion) and 8.3% (£10.3 billion) respectively, which resulted in an increase in aGVA of 2.0% (£1.3 billion).

The industry contributing the most to this growth was Mining & quarrying.

Mining & quarrying (Section B, Which includes oil and gas extraction)

Turnover in Mining & quarrying increased by 3.4% (£1.7 billion) while purchases increased by 9.2% (£2.5 billion). Together with increases in work of a capital nature, this resulted in a 2.9% (£0.7 billion) rise in aGVA.

The main contributor was Other Mining and Quarrying (Division 08) where the increase in aGVA was generally attributed to increased margins and procurement savings and also an increase in demand for business.

Energy Generation & Supply (Section D)

Electricity generation & supply also saw an increase between 2012 and 2013. Turnover increased by 5.5% (£5.8 billion) and purchases by 7.1% (£5.8 billion), which together with rising stock levels resulted in an aGVA increase of 1.1% (£0.3 billion).

Reasons given for this increase were a growth in business in onshore/offshore wind and offshore gas and price increases for gas and electricity.

The continuing population rise of micro-businesses (with less than 10 people in employment) in this sector is thought to be due to the growth of small producers of renewable energy encouraged by various green grants, subsidies and "feed in tariffs". Between 2012 and 2013 the number of micro-businesses in this area increased by 42.5% (to over 2,300).

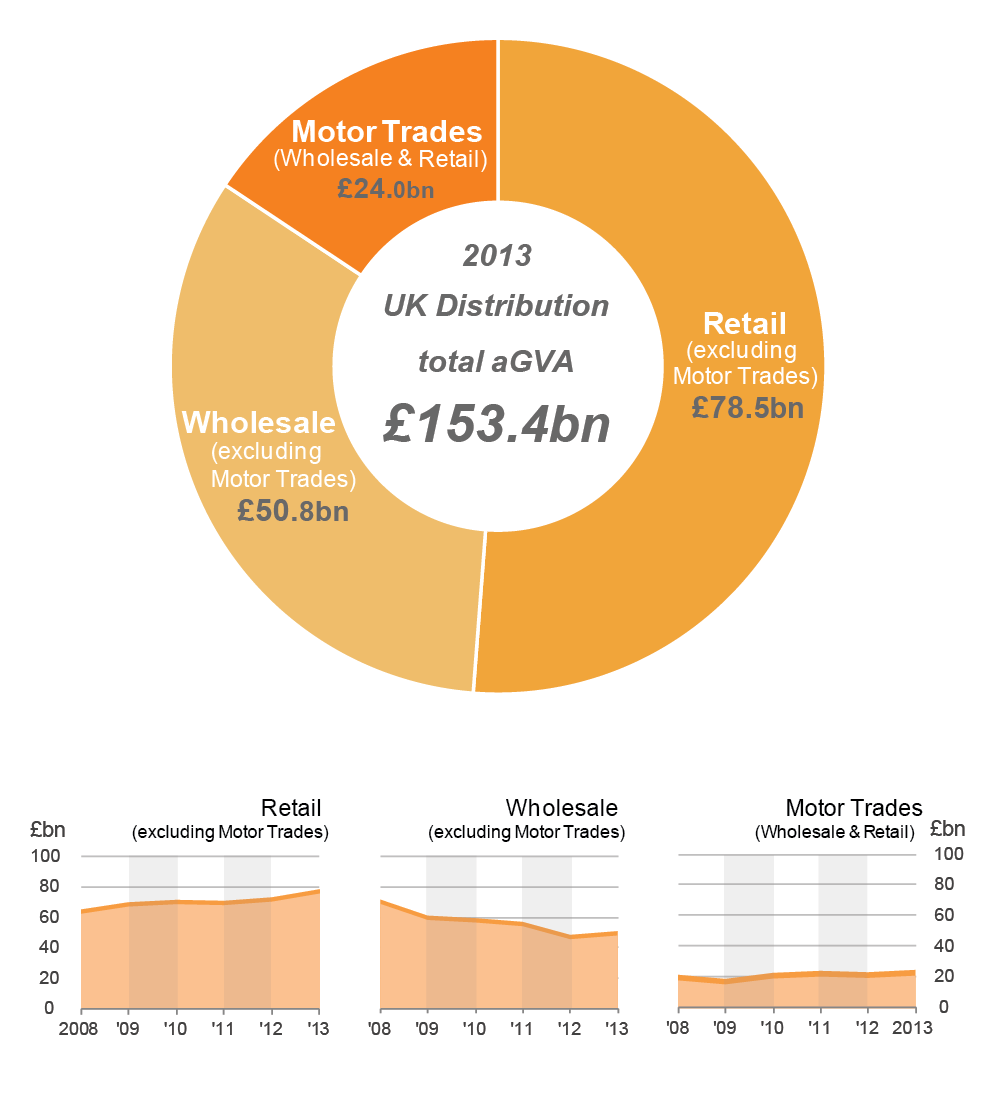

Nôl i'r tabl cynnwys8. Distribution industries, Section G

The Distribution industries in 2013 contributed 15.1% to the estimated aGVA total of £1,012.6 billion for the UK Non-Financial Business Economy.

This sector saw an 8.4% (£115.8 billion) rise in turnover and an 8.8% (£105.8 billion) increase in purchases between 2012 and 2013. This contributed to the increase in aGVA of 6.5% (£9.3 billion). This is the first annual increase since 2010, with aGVA for the Distribution sector at its highest level since the start of the recession in 2008 (see Figure 13).

Figure 13: Distribution, details of turnover and purchases and resulting aGVA, 2008-2013

Source: Office for National Statistics

Download this chart Figure 13: Distribution, details of turnover and purchases and resulting aGVA, 2008-2013

Image .csv .xlsIncreases in aGVA were seen in all three divisions within Distribution (see Figures 14 and 15), with the largest increase between 2012 and 2013 seen in Retail (excluding Motor Trades - Division 47).

Figure 14: Distribution, details of aGVA by division, 2008-2013

Source: Office for National Statistics

Retail (excluding motor trades) (Division 47)

Retail aGVA saw an increase of 7.3% (£5.4 billion) between 2012 and 2013. This growth in aGVA was a result of a 2.9% (£10.2 billion) increase in turnover and a smaller 2.1% (£5.9 billion) increase in purchases.

The increases in aGVA were driven by an 8.9% (£1.7 billion) rise in Retail sale in non-specialised stores (Group 47.1) which includes retail sales in super-stores and department stores.

Reports from businesses continued to indicate that turnover from mail orders and via the internet increased at a higher rate than turnover from shops. Although increasing, retail sales from mail order and the internet remains a small share of total turnover.

Wholesale (excluding motor trades) (Division 46)

Wholesale experienced an increase in turnover of 11.0% (£96.7 billion) and purchases of 11.3% (£91.2 billion) between 2012 and 2013 which resulted in an increase in aGVA of 5.1% (£2.5 billion).

The rise in aGVA between 2012 and 2013 was driven by Wholesale on a fee or contract basis (Group 46.1), which showed an increase of £1.4 billion.

Motor trades (wholesale and retail) (Division 45)

Between 2012 and 2013 both purchases and turnover increased again, by 7.2% (£8.7 billion) and 6.2% (£8.9 billion) respectively. This resulted in aGVA increasing by 6.6% (£1.5 billion), following a decrease last year.

Within Motor Trades, Sale of motor vehicles (Group 45.1) contributed most to the growth with a 9.6% (£1.1 billion) increase in aGVA between 2012 and 2013. This increase comes after a slight fall of 0.4% (£0.1 billion) in aGVA between 2011 and 2012.

Figure 15: Distribution, details of aGVA growth by division, 2008-2013

Source: Office for National Satistics

Download this chart Figure 15: Distribution, details of aGVA growth by division, 2008-2013

Image .csv .xlsNotes for Distribution Industries, Section G

Retail (Excluding Motor Trades) (Division 47)

Please note that the ABS figures for the Retail industry should not be compared directly with the annual value non seasonally adjusted’ figures in the monthly 'Retail Sales Inquiry' release because:

- the ABS figures cover the United Kingdom, while the 'Retail Sales Inquiry' covers Great Britain only

- the ABS ‘total’ turnover figures in the main results tables represent sales to both business and the public and are published excluding VAT, while those in the 'Retail Sales Inquiry' represent sales to the public only and are published including VAT

The ABS does publish ‘retail’ turnover figures (for sales to the public only) in its Retail Commodities tables in the June release which are inclusive of VAT and will be closer to 'Retail Sales Inquiry' figures, however;

- the ABS ‘retail’ turnover figures includes data for National Health Service receipts and commissions whereas the 'Retail Sales Inquiry' do not

- Retail Sales Inquiry does not cover household spending on services bought from the retail sector as it is designed to only cover goods

- although both quote figures for a calendar year, the 'Retail Sales Inquiry' produce monthly output measures which include average weekly value and volume estimates. The value estimates reflect the average total turnover that businesses have collected over a standard reporting period, while the volume estimates are calculated by taking the value estimates and adjusting to remove the impact of price changes. ABS figures are based on annual responses from businesses covering a range of financial years

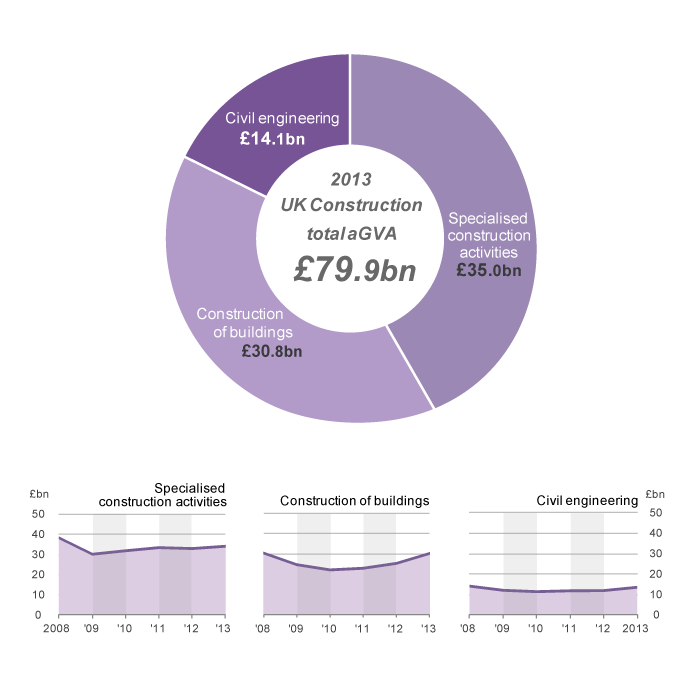

9. Construction industries, Section F

The Construction Industries `contributed 7.9% to the estimated aGVA total of £1,012.6 for the UK Non-Financial Business Economy in 2013.

Construction turnover increased by 8.0% (£15.1 billion) between 2012 and 2013 with purchases increasing by 7.9% (£9.2 billion) to give overall growth in aGVA of 10.7% (£7.7 billion). This is the third consecutive year of growth, which leaves Construction aGVA £4.9 billion lower than the level in 2008, before the recession (see Figure 16).

Figure 16: Construction, details of turnover and purchases and resulting aGVA, 2008-2013

Source: Office for National Statistics

Download this chart Figure 16: Construction, details of turnover and purchases and resulting aGVA, 2008-2013

Image .csv .xlsAs in the previous year, the growth in Construction was mainly in Construction of buildings (Division 41), see Figures 17 and 18. However, the other two divisions within Construction also contributed to the rise for 2013; aGVA in Civil engineering (Division 42) rose by 12.7% (£1.6 billion) and Specialised construction activities (Division 43) increased by 3.4% (£1.2 billion).

Figure 17: Construction, details of aGVA by division, 2008-2013

Source: Office for National Statistics

Construction of buildings (Division 41)

Construction of buildings, which was the main cause for the growth in the Construction sector, experienced an increase in aGVA of 19.1% (£4.9 billion) between 2012 and 2013. This was a result of a 13.3% (£9.9 billion) increase in turnover and a 14.1% (£6.7 billion) increase in purchases, coupled with a 417% (£1.8 billion) rise in stock levels.

As was the case in 2012, this year’s main reason for the increase in aGVA was in the Development of building projects (Group 41.1).

Figure 18: Construction, details of aGVA growth by division, 2008-2013

Source: Office for National Satistics

Download this chart Figure 18: Construction, details of aGVA growth by division, 2008-2013

Image .csv .xlsNotes for construction industries, Section F

Please note that the ABS figures for the Construction industries should not be compared directly with annual figures in the monthly ‘Output in the Construction Industry’ release because:

- the ABS figures cover the United Kingdom, while the 'Output in the Construction Industry' covers Great Britain only

- the two surveys measure different concepts of this industry

- while both quote figures for a calendar year, the ‘Output in the Construction Industry’ are based on the aggregate of the responses to 12 monthly surveys, whereas ABS figures are based on annual responses covering a range of business years

- the ABS figures will always be larger than those in the ‘Output in the Construction Industry’ because the latter excludes: Property developers (SIC 41.1); Payment on purchased services (architects, technical engineering, etc.); Payment to subcontractors, unless the subcontractors are not classified to construction and therefore are not part of the survey; Value of land; Value of materials sold (which are not part of a structure); and Fixtures, equipment and tools that are sold

- the ABS figures include secondary activities related to businesses classified within the construction sector, while the ‘Output in the Construction Industry’ covers only the construction activity of the businesses

10. Agriculture (part), forestry and fishing, Section A

The ABS covers only hunting, forestry, fishing and the support activities to agriculture. Commentary is therefore limited because the sector’s size in terms of economic output, as measured by the ABS, is small in comparison to the other sectors of the UK Non-Financial Business Economy. However, data for these parts of Section A can be found in the reference tables linked to this bulletin.

Note that the values quoted below for Section A are in £ millions.

The part of Section A covered by ABS showed rises in turnover of 23.7% (£852 million) between 2012 and 2013 and in purchases of 18.6% (£441 million) which led to an increase of 28.4% (£399 million) in aGVA between 2012 and 2013. The main contributor to this increase was Support activities to agriculture & post-harvest crop activities (Group 01.6).

This rise means that, at £1,804 million, aGVA is now higher than the level in 2008, at the start of the recession.

Comparable GVA figures for the rest of Agriculture (which includes crop and animal production) are available in Chapter 3 (Table 3.2) of the Agriculture in the United Kingdom release published annually by the Department for Environment, Food and Rural Affairs (DEFRA), and shows a value of £9,222 million for 2013.

Nôl i'r tabl cynnwys