1. Main points

Experimental analysis shows that 1.1% of businesses operating in the UK in 2018 were foreign owned but they accounted for 13.4% of total UK company assets.

Of the foreign-owned businesses, 19.1% of their assets were held by companies with an ultimate parent resident in the UK (that is, UK companies investing in the UK through a foreign affiliate).

Of the foreign-owned businesses in the UK, 93% were majority foreign owned (more than 50% foreign ownership) and 7% were minority foreign owned (between 10% and 50% foreign ownership).

Most foreign-owned local units are based in London, but the North East has the greatest proportion of its local units under foreign ownership (approximately 15%).

The construction industry constitutes 5.9% of total UK company assets but less than 1% of foreign-owned UK company assets.

Smaller companies tend to have fewer local units and those units are more likely to be based in London; large companies tend to have more local units, which are more widely distributed across the UK.

2. Introduction

The UK is both a leading source and a destination for foreign direct investment (FDI); a cross-border investment made with the objective of establishing a lasting interest in the host economy where the direct investor (parent company) controls at least 10% of the voting power (ordinary shares). FDI can play an important role in a country’s long-term economic growth as it can create new jobs, introduce new and more efficient management practices, and be a catalyst for technological progress.

This article contains experimental analysis using an extract from the Orbis dataset (compiled by Bureau van Dijk) consisting of information on UK businesses – the industries they operate in, their location and their global company structures. Detailed information on the global company structures of UK businesses provides an opportunity to investigate cross-border influences on UK businesses. As such, this article focuses on three main areas of interest:

- country of residence of foreign UK investors

- foreign-owned UK businesses by industry

- subnational distribution of foreign-owned UK businesses

Like the Inter-Departmental Business Register (IDBR), the Orbis dataset contains information on the location of each UK business and the main industry each business operates in. It contains variables such as turnover and employment but also alternative financial variables such as total asset values and shareholder’s funds.

This article makes use of these financial variables, total asset value and shareholder’s funds, to weigh business counts (see Figure 1 notes) and provide insights into foreign-owned UK businesses, including by industry and geography. The total assets variable provides an indication of the size of a company, while the shareholder’s funds variable represents the total assets of a company less its liabilities. Shareholder funds therefore provides an indication of how much liability the company has accrued relative to its assets. Though other variables were available, these two measures consistently provided the best coverage across all businesses in the dataset.

This analysis covers 2018 data only, as 2018 was the year with the best coverage of financial information. From the set of 4.1 million UK businesses considered, 46,063 (or 1.1%) were found to be foreign owned. Of these, 93% were majority foreign owned (that is, foreign shareholder holds more than 50% ownership) and 7% were minority foreign owned (that is, foreign shareholder owns between 10% and 50%).

Nôl i'r tabl cynnwys3. Countries of residence of foreign UK investors

While a relatively small number of UK businesses were foreign owned (1.1%), they accounted for 13.4% of total UK company assets in 2018.

Figure 1 shows that in 2018, the top 10 countries of residence of immediate parent companies of UK businesses owned 81.3% of the total value of foreign-owned UK company assets, of which the US (18.8%), Ireland (14.5%) and Luxembourg (13.1%) made up the top three.

On a shareholder’s funds basis (that is, once company liabilities are considered), the US (23.9%), Luxembourg (21.5%) and Netherlands (10.5%) made up the top three countries of residence of immediate parent companies, while Ireland has dropped out of the top 10.

The top 10 countries of residences of immediate parent companies of UK businesses owned 81.2% of the value of foreign-owned shareholder’s funds in the UK.

Minority foreign ownership make up a small percentage of total ownership for all countries, although the minority ownership of companies based in Jersey were most significant.

Figure 1: The United States is the top country of residence of immediate parent companies of UK businesses, by total assets and shareholder funds

The top 10 countries of residence of immediate parent companies of UK businesses by total assets (left) and shareholder’s funds (right), broken down by majority and minority ownership, 2018.

Embed code

Experimental analysis using Orbis’ detailed information on ownership structures allows us to also distinguish the country of residence of ultimate parent companies, which are companies or individuals at the top of a company structure with controlling influence. Estimates on an ultimate parent company basis allow us to better identify the true country of influence; more detail on this distinction can be found in Section 7: Methodology.

Figure 2 shows the top 10 countries in which ultimate parent companies of foreign-owned UK businesses are resident. The contribution of parent companies to country totals in Figure 2 are found by multiplying the shareholder’s funds and total assets of the UK company by the ultimate parent company’s total ownership percentage. On this ultimate basis, the UK features prominently, representing the large number of cases where a UK company is owned by a foreign company (that is, ultimately owned by a UK company). Of the total assets owned by foreign parent companies, 19.1% were held by ultimate parent companies resident in the UK.

Companies resident in the US and Ireland feature within the top 10 on UK company assets ownership on an ultimate basis – as they did on an immediate basis – with more than 22.9% of ultimate parent assets resident in the US and 18.5% in Ireland.

Figure 2: In 2018 more than 20% of UK company assets owned by ultimate parents were held by companies resident in the United States

The top 10 countries of residence of ultimate parent companies of UK businesses by total assets (left) and shareholder’s funds (right), broken down by majority and minority ownership, 2018.

Embed code

Figure 3 consolidates results from the previous two figures, highlighting the path ownership takes from the ultimate to the immediate parent company. Only cases where the ultimate parent company differs from the immediate parent are included, and only the ultimate and immediate parents are considered. Figure 3 shows that specifically in cases where a UK company is ultimately owned by a UK company through a foreign affiliate, the majority of ownership passes through the Cayman Islands, Luxembourg and Netherlands.

In the case of ultimate parent companies of UK businesses resident in Ireland and Japan, ownership tends to pass through other businesses based in their own country. Other countries on the list of top 10 ultimate owners tend to route ownership through companies based in a more diverse range of immediate owning countries.

Figure 3: UK companies that route ownership of a UK company through a foreign company, tend to do so through the Cayman Islands, Luxembourg or the Netherlands

The paths of ownership from the country of residence of the ultimate parent company (left) through the country of residence of the immediate parent company (right).

Embed code

Nôl i'r tabl cynnwys

4. Foreign-owned businesses in the UK by industry

Figure 4 shows the percentage of immediate foreign-owned company assets and total UK company assets in each industry. The largest industry by total assets is financial and insurance activities, with more than 45% of total foreign-owned assets. The top four industries are consistent both for all UK businesses and foreign-owned UK businesses.

The industry that has changed position most is construction. According to our experimental analysis, the construction industry is the fifth largest UK industry by total company assets, constituting 5.9% of total UK assets. However, it makes up less than 1% of foreign-owned assets.

Figure 4: The four largest UK industries by company asset value are also the largest by foreign ownership

Percentage of total company asset values in each industry as a percentage of total foreign-owned UK asset value (left) and percentage of total company asset values in each industry as a percentage of total UK company asset value (right).

Embed code

In this section, top level NACE rev. 2 industry classifications have been used to group businesses by industry. The contribution of each business to its industry total is weighted by total assets (and by shareholder’s funds in accompanying data tables). NACE rev. 2 industry classifications are similar to, but differ slightly from, the Standard Industrial Classification (SIC) industry codes used in other Office for National Statistics (ONS) publications; therefore, industrial breakdowns are not comparable.

5. Subnational distribution of foreign-owned UK businesses

In this section, two methods are used to estimate the subnational distribution of UK businesses with foreign ownership. The first method uses the Orbis postcode variable and results are aggregated to regions (to a NUTS 1 basis). A limitation of this approach is that registered company addresses often do not reflect the location in which the main business activity occurs. The postcode address can instead represent the location of the head office of a company or an administrative address such as that of an accountant or lawyer.

The second method utilises the shareholder information within Orbis to identify all local units owned by a foreign-owned UK business. The local units have addresses that better reflect the location of their main business activity and should give a more accurate estimate of the subnational distribution of foreign-owned businesses in the UK. However, not every foreign-owned business in the dataset has local units (about 15% of foreign-owned businesses have a local branch beneath them in their company structure), and local units have no financial information directly attributable to them.

Despite these limitations, Orbis still provides an opportunity to experiment with two methods in estimating the subnational distribution of UK businesses with foreign ownership.

Figure 5 shows the count of UK businesses with an immediate foreign shareholder, by region (left), the number of foreign-owned local branches by region (centre), and the proportion of all local branches in each region that are foreign owned (right).

Using method one, the addresses of businesses with direct foreign shareholders (left), the data are more heavily distributed towards London. In this approach, 48.9% of foreign-owned UK businesses are said to reside in London. As mentioned, this is likely because of businesses being more likely to have a head office or administrative address in London.

Using method two, the number of foreign-owned local branches by region (centre), the location of foreign-owned UK businesses are more evenly distributed across the UK. In this approach, almost a third of all foreign-owned local branches are based in either London or the South East. Despite the North East having the second fewest foreign-owned local branches by count, the rightmost figure shows that the highest proportion of its local branches were foreign owned in 2018 (at 15%).

Figure 5: Despite having the second-fewest foreign-owned local branches by count, the North East is the region with the highest proportion of local branches under foreign ownership

Count of businesses with direct foreign shareholders (left), count of foreign-owned branches (centre) and percentage of branches that are foreign-owned (right), NUTS1 regions.

Embed code

To maximise the usefulness of the subnational analysis in this article, a link can be made between the financial information available for foreign-owned UK companies and the local branches under their control. The list of foreign-owned UK companies used in this article has been sorted into deciles based on their company asset values. Local branches owned by the UK companies are then assigned to the deciles of their parent companies. Table 1 in Section 7: Methodology contains bounds for each decile and the numbers of businesses in each decile.

Figure 6 shows the percentage of local units in each region for each decile (each column sums to 100%). It indicates the regions that have the most local units belonging to large companies and, similarly, the regions that have the most branches belonging to smaller businesses (that is, businesses in the bottom five decile groups). For example, 13.6% of local branches belonging to the largest 10% of foreign-owned businesses by total assets are based in London. For most deciles, Northern Ireland has the smallest proportion of foreign-owned local branches.

The distribution of businesses across subnational regions is relatively consistent across the deciles. The obvious exception to this being that as asset values fall, the distribution of local branches becomes more London centric. The smallest 50% companies generally have fewer local branches and have chosen to have some representation in London.

Figure 6: Local units belonging to smallest 50% of companies are more likely to be based in London than local units belonging to largest 50% of companies

The percentage of branches in each sub-national region based on the size of the company, by decile group, 2018.

Embed code

6. Comparison with other publications

The Office for National Statistics (ONS) produces regular statistics on foreign-owned UK businesses using the Annual Business Survey (ABS). The Foreign-owned businesses in the UK non-financial business economy (Annual Business Survey): 2018 article provides information on the size and growth of the UK non-financial business economy. Within this set of UK businesses, the article investigates the number of foreign-owned businesses, their turnover, their industry, their employment size bands, their subnational UK region and the approximate gross value added (aGVA) of foreign-owned businesses.

Direct comparisons with the ABS should be treated with caution; the ABS excludes businesses from some lower-level industry groups and contains a narrower pool of UK businesses. Further, the ABS includes only majority foreign ownership in its foreign ownership statistics .

This article's experimental analysis uses Orbis data to add insight and demonstrate the information and value that is contained in the Orbis dataset. Despite differences in the datasets, the broad distributions of foreign ownership are similar in our results to those in the ABS publication. For example, using both datasets, the five largest industries in terms of foreign ownership are the wholesale retail and trade; professional, scientific and technical; manufacturing; information and communication; and administrative and support services industries. However, the exact order slightly changes between them. The differences could be because of the inclusion of minority ownership in the foreign ownership statistics in this article, which are not included in the ABS.

On 3 August 2020, the ONS will publish UK foreign direct investment, trends and analysis, which uses the foreign direct investment (FDI) survey combined with information from the Inter-Departmental Business Register (IDBR) to present FDI by country of the ultimate controlling parent company. While the concepts in both this article and the article on 3 August 2020 are similar, the release on 3 August 2020 presents analysis using the FDI stock (or position) rather than through financial variables such as total assets and shareholder’s funds. Further, these experimental statistics exclusively use Orbis as their source, while official estimates of FDI use ONS survey data.

It is also important to note when making comparisons with results in this report that the experimental analysis and methods used may be improved and developed over time, in conjunction with the needs of users.

Nôl i'r tabl cynnwys7. Methodology

Selecting businesses for analysis

The Orbis dataset contains information on 15.1 million businesses. Each company listed has a Status variable that describes whether it is active or not. To get the set of businesses used in this report, businesses dissolved before 2018 and any businesses registered overseas are excluded. Businesses are also removed if they have consolidated accounts or do not have 2018 listed as a year in which they reported financial information. The final set of UK businesses investigated in this article constitutes 4.1 million businesses.

From those UK businesses, foreign-owned businesses are defined using the following conditions:

the UK business has at least one direct foreign shareholder or immediate parent

the foreign shareholder holds a minimum of 10% ownership of the UK business

a foreign shareholder must not be listed as an individual or family (individuals and families are listed in the dataset as per their nationality as opposed to their residence)

After all conditions are met, the set of foreign-owned businesses contains 46,036 unique UK businesses or 1.1% of all UK businesses considered. While a relatively small number of businesses were foreign owned, they accounted for 13% of total UK company assets in 2018.

Of the 46,036 foreign-owned UK businesses, approximately 15% owned local branches. In Section 5: Subnational distribution of foreign-owned UK businesses, this 15% of businesses is used to produce Figure 6.

Variable selection

Throughout this article, total assets and shareholders’ funds are used to weight contributions to collections of businesses, grouped either by country of ownership or industry. Total assets and shareholders’ funds were the two variables with the highest and most reliable coverage across industry groups. Three other financial variables (employment numbers, turnover and profits) were also tested, but these had poor coverage and were not used in this analysis.

As an example of the coverage of the financial variables considered, Figure 7 shows the percentage of businesses with each financial variable available in our final set of foreign-owned businesses. The coverage has been broken down by industry (using NACE rev. 2 industry codes). Although there is some variation across industries, no less than 95% of businesses are represented by shareholders’ funds and total assets across all industry groupings (apart from where the industry code was unavailable where coverage was 92%). The other variables tested have inconsistent and generally poor coverage across the industry groupings.

Figure 7: Shareholder’s funds and asset values provided the most reliable coverage of financial variables in the Orbis dataset

Orbis' percentage coverage of financial information of UK companies across all industries, 2018

Source: Bureau van Dijk – Orbis

Notes:

- Industry breakdown using NACE industry codes.

- Figures have been rounded to zero decimal places.

- NA denotes missing industries.

Download this chart Figure 7: Shareholder’s funds and asset values provided the most reliable coverage of financial variables in the Orbis dataset

Image .csv .xlsUnderstanding company structures

Analysis in this report distinguishes cross-border ownership on both an immediate parent company and ultimate parent company basis.

An ultimate parent of a company is understood to be the company or individual at the top of a company structure, but the best way to define the company at the “top of a company structure” is not always clear.

The Orbis definition of an ultimate parent is adopted throughout the analysis (referred to as global ultimate owner (GUO) in Orbis). Within the Office for National Statistics (ONS) Orbis extract, a company’s ultimate parent must satisfy the following conditions for a company X:

the ultimate parent of company X is a shareholder with at least a 25% share (direct or total) in company X

the ultimate parent must itself have no shareholder with more than a 25% share in the company X

at each ownership link, the path of largest total ownership is taken so that the path to the ultimate parent always represents the path of maximal control over the original underlying business

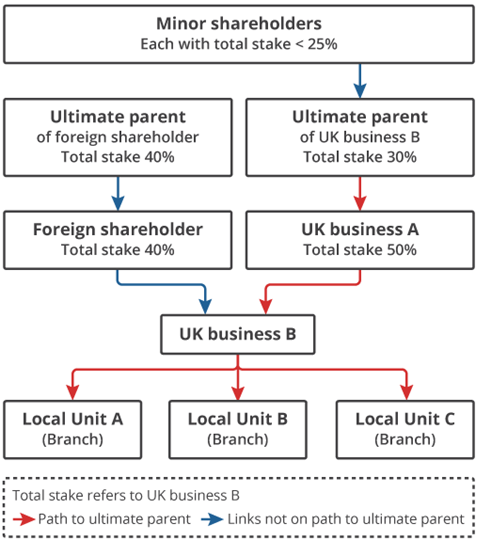

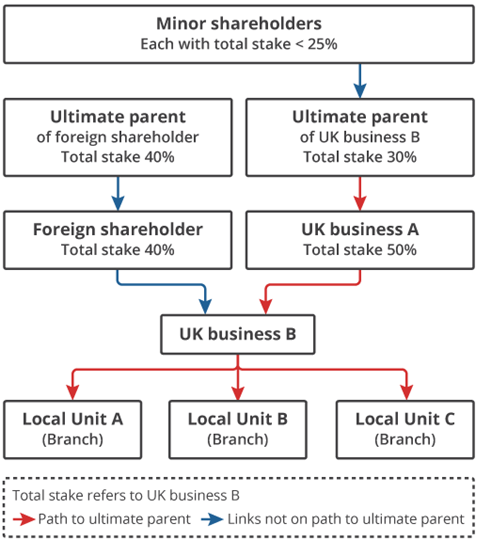

Figure 8 gives an example of a UK business and the path to its ultimate parent. The ultimate parent can have several shareholders, provided none of them have a total share in the UK business of more than 25%. It should also be noted that the ultimate parent does not always have the largest total stake in the company to which it is the ultimate parent. In Figure 8, the ultimate parent of the foreign shareholder has a larger total stake in the UK business than the ultimate parent of the UK business. However, because the route to the ultimate parent of the foreign shareholder was not the route of maximal control at every stage, it cannot be the ultimate parent of the UK business.

Figure 8: The path to the ultimate parent company from the UK company is via the route of largest shareholder at every stage

Example of path to the ultimate parent company from the UK company

Source: Bureau van Dijk – Orbis

Notes:

- Total stake refers to the total stake of the shareholder to UK business B.

Download this image Figure 8: The path to the ultimate parent company from the UK company is via the route of largest shareholder at every stage

.png (78.5 kB){kind=link}

In some instances, no ultimate parent information is provided within Orbis. This may be because two businesses each own 50% of a business and ultimate ownership could be apportioned to either business or the total ownership percentages were unknown. Where ultimate ownership information is missing from Orbis, we generate a value using the ownership information available. We do not use this process to define all ultimate parent companies because there is uncertainty about percentage ownership in some cases.

It should be noted that the definition of foreign ownership used in this article allows for a UK business to be ultimately owned by a UK business and still be classified as foreign owned, provided there is a foreign business between them in the company structure. These cases produce the UK total in ultimate parent charts in Section 3.

Subnational breakdowns

For subnational breakdowns of foreign-owned UK businesses, we use the postcode variable provided in Orbis. We then match this with the postcodes in the ONS 2019 postcode reference table to get the corresponding breakdowns on NUTS code basis.

The described process for assigning businesses to a region is reliant on the accuracy of the postcode variable. There are a number of business structures that have only one postcode listed despite containing many businesses. This is because the postcode variable generally reflects the correspondence address and therefore the head or administrative office rather than the location of the business. As a result, it inflates the reported number of foreign-owned UK businesses in regions more likely to contain company headquarters, for example, London.

Therefore, local units, referred to as “branches” in Orbis, are made use of in this research as their postcodes are more representative of local activity. Unfortunately, local branches do not have financial information available. Therefore, analysis is conducted based only on the unweighted counts of local units by region.

Approximately 15% of foreign-owned company structures contain at least one local branch. Although 15% is a small sample of the data, in this experimental investigation, it provides a useful supplement to existing approaches to understanding subnational foreign ownership.

To determine foreign-owned branches in Orbis, each ownership link of more than 10% is followed from the foreign-owned UK company, until no further subsidiaries can be found in the company structure. These company structures are then filtered leaving only the companies listed as “branches” in Orbis. This list can then be compared to the list of all “branches” in the dataset.

The local branch results in the subnational distribution of foreign-owned businesses section favour industries that have larger numbers of local branches and relatively underrepresent industries like financial and insurance activities that have fewer local branches relative to their size. Figure 9 shows the distribution of local branches over each industry grouping, which does not match the distribution of assets by industry in the foreign-owned businesses in the UK by industry section. While unsurprising given the nature of the different industries, it may affect the subnational distributions.

Figure 9: Wholesale and retail trade has the largest number of local branches despite not being the largest industry by assets

Count of local branches by industry, 2018, UK

Source: Bureau van Dijk – Orbis

Notes:

- Industry breakdown using NACE industry codes.

Download this chart Figure 9: Wholesale and retail trade has the largest number of local branches despite not being the largest industry by assets

Image .csv .xlsEarlier in the article, Figure 6 showed local branches assigned to the decile of their parent company based on parent's asset value. Table 1 shows the bounds of each decile used in Figure 6, along with the counts of local branches in each decile. Smaller businesses (that is, businesses in the bottom five decile groups) by total assets values intuitively have the fewest local branches.

| Decile | Number of branches in each decile. | Bounds of total assets for each decile. | Average number of branches per company structure. |

|---|---|---|---|

| 1 | 25,512 | £314M < X | 34 |

| 2 | 8,246 | £83.8M < X < £314M | 11 |

| 3 | 4,113 | £30.1M < X <£83.8M | 5 |

| 4 | 2,512 | £11.9M< X < £30.1M | 3 |

| 5 | 3,081 | £5.4M< X < £11.9M | 4 |

| 6 | 1,913 | £2.4M< X < £5.4M | 3 |

| 7 | 1,157 | £1.0M < X < £2.4M | 2 |

| 8 | 4,267 | £0.3M< X < £1.0M | 6 |

| 9 | 2,158 | £34,000 < X < £0.3M | 3 |

| 10 | 1,754 | £0< X < £34,000 | 2 |

Download this table Table 1: The decile boundaries and counts of businesses per decile for Figure 6

.xls .csv8. Glossary

Shareholder funds

Shareholder funds are total assets minus total liabilities. They are the total that can be divided among shareholders in the event of liquidation.

Foreign owned

A UK business is foreign owned if it has at least one foreign shareholder with a more than 10% direct share in the UK business.

Majority owned

A foreign-owned UK business with a foreign shareholder who has at least 50% direct share in the UK business.

Minority owned

A foreign-owned UK business where the largest direct foreign shareholder has a share of more than 10% and less than 50%.

Local branch

A unit based in the same country as its parent company, that is not legally separate from its parent company.

Nôl i'r tabl cynnwys