Cynnwys

1. Main points

Aggregate net property wealth for all private households in Great Britain increased by £399 billion (11%) to £3,927 billion in current prices between July 2010 to June 2012 and July 2012 to June 2014

During the period of July 2012 to June 2014, half of all households who owned property had net property wealth of £152,500 or more

The highest median value of net property wealth was seen amongst households in London, where half of all households who owned property had net property wealth of £260,000 or more during July 2012 to June 2014

Half of all households with a mortgage on their main residence owed £83,000 or more during July 2012 to June 2014

2. Introduction

This chapter looks at estimates of household property wealth obtained from the Wealth and Assets Survey (WAS). Gross property wealth comprises the value of the main residence for a household and the value of any additional property or properties owned by any adults within the household. Estimates of a household’s property wealth do not include business assets owned by household members. The gross value of household property and the value of mortgages (liabilities) are presented at the beginning of this chapter and then combined to report on net property wealth (gross assets minus liabilities). This is followed by an analysis of net property wealth according to both household (for example, region of residence) and individual level (for example, age) characteristics.

All estimates are presented as current values (that is, the value at time of interview) and have not been adjusted for inflation.

Due to the complexity of the data, for example, the use of imputed values and complex weighting, only a very limited amount of high level significance testing has been undertaken, which is presented in the Technical chapter of this report (335.5 Kb Pdf). None of the estimates commented on in this chapter have been tested for significance.

Nôl i'r tabl cynnwys3. Property ownership

Home ownership

Table 3.1 presents estimates of ownership of main residence in each 2-year period covered by the separate period of the survey. Around two-thirds of households interviewed in each period owned their main residence (either outright or buying it with a mortgage); a percentage which has seen little change since 2006. However, the proportion of households who owned their home outright increased slightly across the survey periods (rising from 30% during July 2006 to June 2008 to 33% in the period July 2012 to June 2014). This increase is offset by the changes seen for households who own with a mortgage, as this has dropped from 38% to 34% over the survey periods. For the period July 2012 to June 2014, just over one-third (34%) of households did not own their main residence, a proportion that is fairly consistent across all periods of the survey.

Table 3.1: Ownership of main residence

| Great Britain, July 2006 to June 2014 | |||||

| % | |||||

| July 2012 to June 2014 | July 2010 to June 2012 | July 2008 to June 2010 | July 2006 to June 2008 | ||

| Owned | 66 | 68 | 67 | 68 | |

| of which owned outright | 33 | 32 | 31 | 30 | |

| of which owned with mortgage | 34 | 36 | 37 | 38 | |

| Not owned (rent or rent free)1 | 34 | 32 | 31 | 32 | |

| All Households2 | 100 | 100 | 100 | 100 | |

| Source: Wealth and Assets Survey, Office for National Statistics | |||||

| Notes: | |||||

| 1. Includes squatting. | |||||

| 2. Includes a small number of households (<1%) who part own part rent their residence. | |||||

Download this table Table 3.1: Ownership of main residence

.xls (26.6 kB)Ownership of other property

Some households own property other than their main residence1. Just over 1 in 10 households (11%) owned other property during the period July 2012 to June 2014. Most of these were buy-to-let properties (4%) and second homes (3%).

Table 3.2: Ownership of other property

| Great Britain, July 2006 to June 2014 | ||||

| % | ||||

| July 2012 to June 2014 | July 2010 to June 2012 | July 2008 to June 2010 | July 2006 to June 2008 | |

| Other houses/flats in UK1 | N/A | N/A | N/A | 6 |

| Second Homes | 3 | 3 | 3 | N/A |

| Buy-to-lets | 4 | 4 | 4 | N/A |

| Other buildings | 1 | 1 | 1 | 1 |

| Land in the UK | 1 | 1 | 1 | 1 |

| Land or property overseas | 2 | 3 | 3 | 3 |

| All Property2 | 11 | 11 | 10 | 10 |

| Source: Wealth and Assets Survey, Office for National Statistics | ||||

| Notes: | ||||

| 1. During the period July 2006 to June 2008, respondents were only offered the category ‘Other houses/flats in the UK’, second homes and buy-to-lets were not separately identified. | ||||

| 2. Households may own more than one type of other property, resulting in the columns not adding up. This estimate also includes households who owned other property but did not specify the type of other property owned. | ||||

| 3. N/A - Not available. | ||||

Download this table Table 3.2: Ownership of other property

.xls (28.2 kB)Notes for property ownership

Property other than the main residence can include:

- Second homes in the UK, including time-share and holiday homes

- Buy-to-let property in the UK (residential property which is let for profit)

- Other buildings, such as a shop, warehouse or garage in the UK

- Land in the UK

- Land or property overseas (including time-share)

- Other real estate

4. Household gross property wealth

For the period July 2012 to June 2014, half of all households who owned their main residence valued their home at £195,000 or more1(Table 3.3). Although this value is £15,000 higher when compared with the period July 2008 to June 2010, it is on a par with the median gross property wealth estimated during the other periods of the survey. (See the quality assurance annex at the end of this chapter)

Half of all households who owned other property2 valued this at £148,000 for the period July 2012 to June 2014. This value of other properties has increased each survey period since July 2006 to June 2008, when the valuation of other properties was £125,000. If the values of all property owned, including both main residence and any other property are considered, half of all households owning property had a gross property wealth of £200,000 for the period July 2008 to June 2010.

Figure 3.4 presents the distribution of gross values of main residences across 5 property value bands. In all of the periods of the survey, the most common valuation band was “£125,000 but less than £250,000”. For the period July 2012 to June 2014, 44% of households owning their main residence valued their property within this band. Around 2 in every 3 main residences in the period July 2012 to June 2014 fell into the bottom 2 bands, that is, less than £250,000 (65%).

Comparing the data over time provides evidence of a fall and subsequent rise in the value of main residences across the periods of the survey. The percentage of property owners, who valued their main residence in the lowest 2 bands, that is, less than £250,000, was 67% in the period July 2006 to June 2008. This percentage increased by 4 percentage points to 71% during the July 2008 to June 2010 period of the survey, which indicates that home owners perceived a fall in the value of their main residence over this period. However since this period, the proportion of main residences with a value of less that £250,000 has decreased by 6 percentage points which could indicate that home owners are now showing a perceived increase in their property value.

Figure 3.4: Gross value of main residence, by property value bands

Great Britain, July 2006 to June 2014

Source: Wealth and Assets Survey - Office for National Statistics

Download this chart Figure 3.4: Gross value of main residence, by property value bands

Image .csv .xlsFigure 3.5 presents the distribution of gross values of other properties by wave and across 5 property value bands. It is important to reiterate that ‘other property’ includes property types with a wide range of values. The propensity to buy and sell other property – notably lower valued property - may be higher and this should be borne in mind when interpreting valuation changes over time.

The most common valuation band for households with other property was less than £125,000. For the period July 2012 to June 2014, 43% of other properties were valued in the lowest band; lower than the corresponding percentage in previous period (47%).

The percentage of other properties valued in the lowest 2 bands, that is, less than £250,000, was 73% in the period July 2006 to June 2008. The percentage was the same in July 2008 to June 2010, but has decreased by 4 percentage points to stand at 69% during July 2012 to June 2014 . The changes in household's property valuation follows the same increasing pattern as shown with the value of the main residences.

Figure 3.5: Gross value of other property, by property value bands

Great Britain, July 2006 to June 2014

Source: Wealth and Assets Survey - Office for National Statistics

Download this chart Figure 3.5: Gross value of other property, by property value bands

Image .csv .xlsNotes for household gross property wealth

How is property wealth calculated?

Property wealth estimates are derived from respondents’ own valuations of their property. If a household’s main residence is either owned outright, with a mortgage or part owned/part rented, the person responding to the household questionnaire is asked to estimate the value of their property. For other property, each adult in the household is asked about any property owned other than the main residence and the value of their share in such property. If precise estimates of property value cannot be given, respondents are offered a choice of banded values. The precise values of these banded responses are later imputed, based on the distribution of the precise values obtained from other respondents. Respondents are also asked about any mortgages (including equity release) secured on their properties.

These data have been quality assured and compared against other sources. The quality assurance report is given in Annex 1 to this chapter.

Other property

It should be noted that ‘other property’ includes property types with a wide range of values compared to the values of main residence for example, timeshares, land plots, garages etc. The propensity to buy and sell this lower valued property may be higher than that for the higher valued property types, irrespective of the market at the time. Therefore values might be more subject to change between waves.

5. Mortgage debt

The survey asked households about mortgages (including all-in-one accounts1). The results show that:

the percentage of households who had a mortgage on their main residence was 38% in the period July 2006 to June 2008, falling to 34% during July 2012 to June 2014 – this fall is consistent with Table 3.1, which presented a drop in the percentage of households owning their main residence with help from a mortgage

the percentage of households who had a mortgage on another property or properties was 5% across for the latest period

In WAS, mortgage debt is recorded as the total outstanding on mortgages on a residence. The median value of mortgage debt on household’s main residence increased by 19% between July 2006 to June 2008 and July 2012 to June 2014. In the period July 2012 to June 2014, half of households owning their main residence with help from a mortgage owed at least £83,000 (Table 3.6).

The median value of mortgages on other property also continues to increase and for the period July 2012 to June 2014 was £90,000, which was £5,000 higher than the July 2010 to June 2012 value.

Table 3.6: Median value of mortgages

| Great Britain, July 2006 to June 2014 | ||||

| £ | ||||

| July 2012 to June 2014 | July 2010 to June 2012 | July 2008 to June 2010 | July 2006 to June 2008 | |

| Households with mortgage on main property | 83,000 | 80,000 | 75,000 | 70,000 |

| Households with mortgage on other property | 90,000 | 85,000 | 84,000 | 80,000 |

| Source: Wealth and Assets Survey, Office for National Statistics | ||||

| Notes: | ||||

| 1. Households may have one or more mortgages. | ||||

| 2. Results exclude households without a mortgage. | ||||

Download this table Table 3.6: Median value of mortgages

.xls (27.1 kB)Equity release schemes

The survey also asked about equity release schemes. Equity release is a way of getting cash from the value of a home without having to move out. It is usually restricted to people aged 55 and above. There are 2 main types of equity release scheme – lifetime mortgages and home reversion plans. A lifetime mortgage is a loan secured on the home (which is not repayable until the person dies or moves into long-term care). A home reversion plan involves a firm either buying the customer's home or a part of it at a discount to the market price, or arranges for someone else to do so. In return the customer gets a cash lump sum or an income. The home, or the part of it they sell, now belongs to someone else, but the customer is allowed to carry on living in it until they die or move out.

Although the values from the survey for equity release are taken into account for households who have reported it when calculating net property wealth, no separate figures are presented here as the number of households reporting equity release is very small (less than 1%), (some may be reporting these as re-mortgages etc.) with the resulting figures for equity release values thought unreliable.

Table 3.8: Aggregate estimates of property wealth

| Great Britain, July 2006 to June 2014 | ||||

| £ Billion | ||||

| July 2012 to June 2014 | July 2010 to June 2012 | July 2008 to June 2010 | July 2006 to June 2008 | |

| Aggregate household gross property wealth | 4,984 | 4,541 | 4,359 | 4,492 |

| Aggregate mortgage debt | 1,057 | 1,012 | 980 | 960 |

| Aggregate household net property wealth | 3,927 | 3,528 | 3,379 | 3,532 |

| Source: Wealth and Assets Survey, Office for National Statistics | ||||

Download this table Table 3.8: Aggregate estimates of property wealth

.xls (27.1 kB)Notes for mortgage debt

- There are 2 types of all-in-one accounts; the 'current account' mortgage and the 'offset' mortgage. Current account mortgages are where all finances are kept together in 1 pot so the mortgage, current account, any savings, credit card and loans are all combined, resulting in 1 overall account with 1 outstanding balance. Offset mortgages are where the different financial elements are held with a single provider, but as separate accounts with individual balances. The different elements are 'linked' so the mortgage amount is reduced ("offset") by the funds in the savings and/or current accounts. Interest is only paid on the net amount owing.

6. Household net property wealth

This section presents summary estimates for total household net property wealth in Great Britain. This is calculated as the sum of the values recorded for each household for the main residence plus any other property, minus the value of mortgage liabilities and equity release.

Table 3.7 shows the median values for total net property wealth for property owners. In the period July 2012 to June 2014, half of all property owning households had net property wealth of £ 152,500 or more.

Table 3.7: Median household net property wealth

| Great Britain, July 2006 to June 2014 | ||||

| £ | ||||

| July 2012 to June 2014 | July 2010 to June 2012 | July 2008 to June 2010 | July 2006 to June 2008 | |

| Median household net property wealth | 153,000 | 150,000 | 148,000 | 150,000 |

| Source: Wealth and Assets Survey, Office for National Statistics | ||||

| Notes: | ||||

| 1. Results are for property owners only. | ||||

Download this table Table 3.7: Median household net property wealth

.xls (27.1 kB)

Table 3.8: Aggregate estimates of property wealth

| Great Britain, July 2006 to June 2014 | ||||

| £ billion | ||||

| July 2012 to June 2014 | July 2010 to June 2012 | July 2008 to June 2010 | July 2006 to June 2008 | |

| Aggregate household gross property wealth | 4,984 | 4,541 | 4,359 | 4,492 |

| Aggregate mortgage debt | 1,057 | 1,012 | 980 | 960 |

| Aggregate household net property wealth | 3,927 | 3,528 | 3,379 | 3,532 |

| Source: Wealth and Assets Survey, Office for National Statistics | ||||

Download this table Table 3.8: Aggregate estimates of property wealth

.xls (26.1 kB)7. Household net property wealth by household characteristics

In this section, only the latest and sometimes 1 previous survey period of data are presented. Data for earlier years is presented in the reference tables available with this release.

This section considers household property wealth by region of residence and household type. In Tables 3.1 and 3.2, ownership rates were presented separately for a household’s main residence and any other property owned. Property ownership rates from now on combine these into a single property ownership rate. The rate is slightly higher than the ownership rate for a household’s main residence, highlighting the fact that persons living in a household might own other property, despite the household itself not owning the main residence.

Distribution of household net property wealth, by total household income

To have a true reflection of a household’s income a process of equivalisation has been performed. Household’s equivalised income is being used as this process adjusts income to compensate for both the size and composition of a given household. Performing this adjustment means that incomes of all households will be on a comparable basis.

Those households with the lowest equivalised income during July 2012 to June 2014 also have the lowest property ownership rates; conversely those households in the highest equivalised income band have the highest. Just under 4 out of 10 (38%) households own property in the lowest income band. This ownership rate rises to over 9 out of 10 (93%) for those households in the highest income bands.

Figure 3.9 shows that property ownerships rates rise as household equivalised income increases.

Figure 3.9: Household ownership rates, by total household net equivalised income decile

Great Britain, July 2010 to June 2014

Source: Wealth and Assets Survey - Office for National Statistics

Download this chart Figure 3.9: Household ownership rates, by total household net equivalised income decile

Image .csv .xlsProperty owning households with the highest levels of income have the largest median net property wealth; while those in the lowest income bands have the fifth highest median net property wealth. During July 2012 to June 2014, the median net property wealth in the highest income band was £280,000. Those in the lowest income band had a median net property wealth of £145,000.

Those property owning households in the lowest income bands were not the households with the lowest median net property wealth – likely to reflect the fact that older people may own property but are retired and have lower incomes. Figure 3.10a shows that the median net wealth decreases through the second and third lowest income bands, finally increasing once past the middle income groups, until reaching a peak in the highest income bands.

Figure 3.10a: Median household net property wealth for property owners, by total household net equivalised income decile

Great Britain, July 2010 to June 2014

Source: Wealth and Assets Survey - Office for National Statistics

Download this chart Figure 3.10a: Median household net property wealth for property owners, by total household net equivalised income decile

Image .csv .xlsSince the property ownership rates for the lowest 3 income deciles was 50% or less in July 2012 to June 2014, the median value of property wealth for all households (that is, including households not owning any property) in these 3 income deciles is zero. Figure 3.10b further shows that for all households, net property wealth increases as income decile increases, with households in the largest income band having a median net property wealth of £250,000 in July 2012 to June 2014, the largest of any income group.

Figure 3.10b: Median household net property wealth1, by total household net equivalised income

Great Britain, July 2010 to June 2014

Source: Wealth and Assets Survey - Office for National Statistics

Download this chart Figure 3.10b: Median household net property wealth1, by total household net equivalised income

Image .csv .xlsRegion of residence

Just under 7 in 10 households (68%) in Great Britain owned their main residence and/or other property in July 2012 to June 2014 (Figure 3.11). The lowest ownership rate in the latest period of the survey was amongst households in the North East and London, where 60% of households owned their main residence and/or other property of some kind. The regions with the highest ownership rate were the South East and the South West – where nearly three-quarters (74%) of households were property owners in the period July 2012 to June 2014.

Figure 3.11: Household ownership rates1, by region of residence

Great Britain, July 2010 to June 2014

Source: Wealth and Assets Survey - Office for National Statistics

Download this chart Figure 3.11: Household ownership rates1, by region of residence

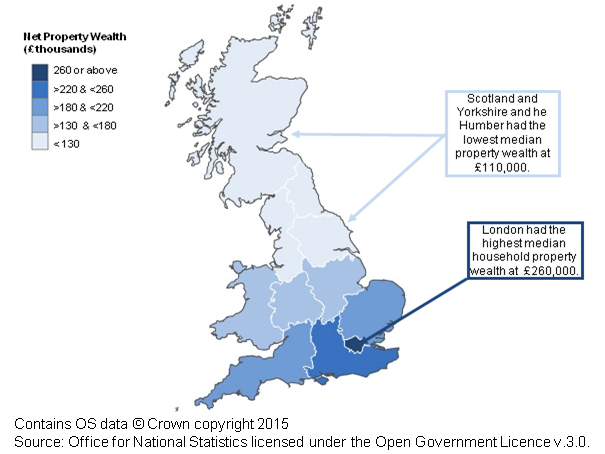

Image .csv .xlsFigure 3.12 shows median household property wealth according to the location of the main residence of the household. It shows Scotland, Wales and the 9 English regions (with London shown separately; the figures for the South East exclude London).

Median household net property wealth for property owners in Great Britain as a whole stood at £153,000 in the period July 2012 to June 2014. In each of the periods, the wealthiest parts of Great Britain in terms of median net household property wealth were London and the South East (Figure 3.12), with values of £260,000 and £220,000 respectively. The regions of Scotland and Yorkshire and The Humber had the lowest value of net property wealth at £110,000.

Figure 3.12: Median household net property wealth [1], by region of residence

![Figure 3.12: Median household net property wealth [1], by region of residence](/resource?uri=/peoplepopulationandcommunity/personalandhouseholdfinances/incomeandwealth/compendium/wealthingreatbritainwave4/2012to2014/chapter3propertywealthwealthingreatbritain2012to2014/0256997e.png)

Source: Wealth and Assets Survey - Office for National Statistics

Notes:

1.Results are for property owners only.

Download this image Figure 3.12: Median household net property wealth [1], by region of residence

.png (126.9 kB) .xls (29.7 kB){kind=link}

Apart from Scotland, each region of Great Britain saw a fall in median household net property wealth between July 2006 to June 2008 and July 2008 to June 2010. Between July 2010 and June 2014, 8 out of 12 regions had an increase, 2 had no change and 2 had a decrease in the median value of household net property wealth. Over the same time period, 6 of the regions saw a decrease, 4 increased and 1 stayed the same. London had the largest increase in median household net property wealth over this period, rising from £239,000 to £260,000. The South West had the largest percentage increase in median household net property wealth, rising by 19%. The biggest decrease was found in Yorkshire and The Humber, which had median value of household net property wealth fall by £9,000, equivalent to an 8% fall, the largest of all regions.

Figure 3.13: Percentage change in median household net property wealth [1], by region of residence

Great Britain, July 2010 to June 2012 and July 2012 to June 2014

Source: Wealth and Assets Survey - Office for National Statistics

Notes:

- Results are for property owners only.

Download this chart Figure 3.13: Percentage change in median household net property wealth [1], by region of residence

Image .csv .xlsHousehold type

The household type with the lowest property ownership rate in each of the waves was ‘lone parent, dependent children’ where less than a third of households (32%) owned their main residence and/or other property of some type in the period July 2012 to June 2014 (Figure 3.14). The household type with the highest property ownership rate in each of the waves was ‘Couple 1 over/1 under 60/651, no children’, where nearly 9 in 10 (89%) of such households were property owners (though this type of household accounted for only 5% of the WAS sample – see Introduction and demographics chapter).

Figure 3.14: Household ownership rates, by household type

Great Britain, July 2010 to June 2014

Source: Wealth and Assets Survey - Office for National Statistics

Download this chart Figure 3.14: Household ownership rates, by household type

Image .csv .xlsOlder couples with no children had the highest median household net property wealth in the period July 2012 to June 2014 (Figure 3.14). Half of all property-owning households in the household type ‘Couple both over 60/65, no children’ had a net property wealth of £230,000 or more, and half of all property-owning households in the household type ‘Couple Couple 1 over/ 1 under 60/65, no children’ had a net property wealth of £220,000 or more. Both of these household types are likely to be coming to the end of their mortgage and will therefore have less mortgage debt. (Only 5% of property-owning households in the household type ‘Couple both over 60/65, no children’ had a mortgage and 20% of property-owning households in the household type ‘Couple Couple 1 over/ 1 under 60/65, no children’ had a mortgage compared with the Great Britain figure of 34%).

The household type with the lowest median household net property wealth in all waves was ‘Lone parent, dependent children’, with a value of £95,000 in the period July 2012 to June 2014. ‘Single household, under 60/65’ was the household type with the second lowest median household net property wealth (£98,000).

The most common household type was ‘Couple with dependent children’ (please see demographic chapter). The median net household property wealth for this household type was £109,000 in the period July 2012 to June 2014.

Figure 3.15: Median household net property wealth for property owners, by household type

Great Britain, July 2010 to June 2014

Source: Wealth and Assets Survey - Office for National Statistics

Download this chart Figure 3.15: Median household net property wealth for property owners, by household type

Image .csv .xlsNotes for household net property wealth by household characteristics

- 60/65 refers to women up to the age of 60 and men up to the age of 65.

8. Household net property wealth by individual characteristics

In this section, only the latest survey period of data are presented. Data for earlier years is presented in the reference tables available with this release.

This section looks at some main characteristics of individuals living in households by net property wealth bands. It is important to remember that this analysis presents individual characteristics by the total property wealth of the household that the individual lives within. In certain instances it is possible that this wealth is more likely attributed to other individuals living within that household. Note that the lowest band of household property wealth includes negative property wealth.

Sex and marital status

Married individuals were the most likely to live in property-owning households. Just 17% of both married males and married females that lived in households did not own their main residence or another property (Table 3.16). Living in a household but not owning any property was most common for individuals whose marital status was either separated (49% for men and 56% for women) or divorced (49% for men and 46% for women).

The percentage of individuals living in households in the net property wealth band of £500,000 or more was highest for married individuals (9% of married males and 8% married females lived in households belonging to the highest net property wealth band). The percentage of cohabiting individuals living in households in the lowest net property wealth band was the highest of all the marital status groups (18% of both cohabiting males and cohabiting females lived in households with net property wealth of £50,000 or less).

Table 3.16: Individuals by sex and marital status, by household net property wealth

| Great Britain, July 2012 to June 2014 | ||||||||

| % | ||||||||

| Do not own property | Less than £50,000 | £50,000 but < £125,000 | £125,000 but < £250,000 | £250,000 but < £375,000 | £375,000 but < £500,000 | £500,000 or more | All Households | |

| Men | ||||||||

| Married2 | 17 | 11 | 19 | 26 | 13 | 6 | 9 | 100 |

| Cohabiting3 | 39 | 18 | 18 | 14 | 6 | 2 | 3 | 100 |

| Single4 | 38 | 12 | 18 | 17 | 7 | 3 | 5 | 100 |

| Widowed | 32 | .. | 18 | 25 | 14 | 6 | 4 | 100 |

| Divorced | 49 | 6 | 20 | 16 | 5 | .. | 2 | 100 |

| Separated | 49 | 17 | 15 | 11 | .. | .. | .. | 100 |

| All men | 30 | 12 | 18 | 21 | 10 | 4 | 6 | 100 |

| Women | ||||||||

| Married2 | 17 | 11 | 19 | 26 | 13 | 6 | 8 | 100 |

| Cohabiting3 | 40 | 18 | 18 | 14 | 6 | 2 | 3 | 100 |

| Single4 | 40 | 12 | 17 | 16 | 7 | 3 | 5 | 100 |

| Widowed | 32 | 2 | 15 | 29 | 14 | 4 | 4 | 100 |

| Divorced | 46 | 6 | 17 | 20 | 7 | 2 | 2 | 100 |

| Separated | 56 | 13 | 14 | 11 | .. | .. | .. | 100 |

| All women | 31 | 11 | 18 | 21 | 10 | 4 | 6 | 100 |

| All Persons | 30 | 11 | 18 | 21 | 10 | 4 | 6 | 100 |

| Source: Wealth and Assets Survey, Office for National Statistics | ||||||||

| Notes: | ||||||||

| 1. Includes all households - including those who rent their main accommodation. | ||||||||

| 2. Includes civil partnerships. | ||||||||

| 3. Includes same sex couples. | ||||||||

| 4. Includes persons of any age. | ||||||||

| 5. Figures in italics are based on 30 or more unweighted cases but less than 50 - such data should be treated with some caution. | ||||||||

| 6. ".." - estimates that have been suppressed due to fewer than 30 unweighted cases. | ||||||||

Download this table Table 3.16: Individuals by sex and marital status, by household net property wealth

.xls (28.7 kB)Age

Living in a non-property owning household was over twice as common amongst individuals aged 16 to 24 years as it was for those aged 55 to 64. Nearly 3 out of every 7 of 16 to 24 year olds (41%) lived in a household without property wealth; the highest percentage across each of the age bands (Table 3.16). Younger people are likely to be earning less than older people, and will have had less time to afford a deposit on a house and enter the property market. Nevertheless, three in five individuals aged 16 to 24 (60%) lived in a household with property wealth and 6% of this age group lived in households with property wealth valued at £500,000 or more. This finding is likely to be attributable to the high percentage of individuals aged between 16 and 24 who still live in their parental home.

The age group 55 to 64 years had the lowest percentage of individuals living in non-property owning households (19% lived in a household without net property wealth). Over 1 in 10 (11%) individuals aged 55 to 64 lived in households with net property wealth of £500,000 or more; the highest of any age group. In contrast, individuals aged 25 to 34 had the lowest percentage living in households with net property wealth in the highest wealth band, at 2%.

Considering the lowest net property wealth band, 1% of individuals aged 65 or older lived in households with net property wealth less than £50,000. Individuals aged between 25 and 34 years were the most likely to live in households with net property wealth of less than £50,000 (24%).

Table 3.17: Individuals by age, by household net property wealth

| Great Britain, July 2012 to June 2014 | ||||||||

| % | ||||||||

| Do not own property | Less than £50,000 | £50,000 but < £125,000 | £125,000 but < £250,000 | £250,000 but < £375,000 | £375,000 but < £500,000 | £500,000 or more | All Households | |

| Under 16 | 36 | 17 | 20 | 14 | 5 | 2 | 5 | 100 |

| 16-24 | 41 | 8 | 15 | 19 | 8 | 4 | 6 | 100 |

| 25-34 | 39 | 24 | 17 | 11 | 4 | 2 | 2 | 100 |

| 35-44 | 29 | 17 | 25 | 17 | 6 | 2 | 4 | 100 |

| 45-54 | 24 | 8 | 20 | 25 | 11 | 5 | 7 | 100 |

| 55-64 | 19 | 4 | 14 | 30 | 15 | 7 | 11 | 100 |

| 65+ | 22 | 1 | 13 | 31 | 18 | 6 | 9 | 100 |

| All Persons3 | 30 | 11 | 18 | 21 | 10 | 4 | 6 | 100 |

| Source: Wealth and Assets Survey, Office for National Statistics | ||||||||

| Notes: | ||||||||

| 1. Includes all households - including those who rent their main accommodation. | ||||||||

| 2. Includes persons of any age. | ||||||||

Download this table Table 3.17: Individuals by age, by household net property wealth

.xls (27.6 kB)Education level

Table 3.18 shows the percentage of individuals living in households with different values of net property wealth by education level.

The percentage of individuals educated at degree level or above living in households with a net property wealth of £500,000 or more was 12% – 9 percentage points higher than individuals reporting no educational qualifications. More than 2 in 5 individuals (45%) without qualifications lived in households that did not own property. This compared with 16% of individuals educated at degree level or above and 29% of individuals who reported other qualifications.

Table 3.18: Individuals by education level, by household net property wealth

| Great Britain, July 2012 to June 2014 | ||||||||

| % | ||||||||

| Do not own property | Less than £50,000 | £50,000 but < £125,000 | £125,000 but < £250,000 | £250,000 but < £375,000 | £375,000 but < £500,000 | £500,000 or more | All Households | |

| Degree level or above | 16 | 12 | 17 | 21 | 14 | 7 | 12 | 100 |

| Other qualifications | 29 | 11 | 18 | 24 | 10 | 4 | 5 | 100 |

| No qualifications | 45 | 5 | 16 | 21 | 8 | 2 | 3 | 100 |

| All Persons2 | 29 | 10 | 17 | 23 | 11 | 4 | 6 | 100 |

| Source: Wealth and Assets Survey, Office for National Statistics | ||||||||

| Notes: | ||||||||

| 1. Includes all households - including those who rent their main accommodation. | ||||||||

| 2. Includes only eligible adults who gave their education level. | ||||||||

Download this table Table 3.18: Individuals by education level, by household net property wealth

.xls (35.3 kB)Economic activity

Table 3.19 shows the percentage of individuals living in households with different values of net property wealth by economic activity.

One in 7 self-employed individuals (14%) lived in households with net property wealth of £500,000 or more. This is 9 percentage points higher than employees and 12 percentage points higher than unemployed individuals living in households within the highest band of net property wealth. One in 12 inactive students (8%) lived in households with net property wealth of £500,000 or more, which could be due to students living at home with their parents.

The percentage of individuals living in households without property wealth was highest for those who were economically inactive due to sickness or disability, or who were unemployed (68% and 59% respectively). The percentage of individuals living in non-property owning households was lowest for those who were self-employed (19%).

Table 3.19: Individuals by economic activity, by household net property wealth

| Great Britain, July 2012 to June 2014 | |||||||||

| % | |||||||||

| Do not own property | Less than £50,000 | £50,000 but < £125,000 | £125,000 but < £250,000 | £250,000 but < £375,000 | £375,000 but < £500,000 | £500,000 or more | All Households | ||

| Economically Active | |||||||||

| In Employment | 24 | 14 | 21 | 22 | 9 | 4 | 6 | 100 | |

| Employee | 24 | 15 | 22 | 22 | 9 | 4 | 5 | 100 | |

| Self Employed | 19 | 11 | 16 | 21 | 12 | 6 | 14 | 100 | |

| Unemployed | 59 | 8 | 12 | 12 | 4 | .. | 2 | 100 | |

| Economically Inactive | |||||||||

| Student | 46 | 5 | 10 | 16 | 8 | 7 | 8 | 100 | |

| Looking after family/home | 50 | 9 | 14 | 14 | 5 | 3 | 5 | 100 | |

| Sick / Disabled2 | 68 | 5 | 11 | 11 | 3 | .. | 1 | 100 | |

| Retired | 22 | 1 | 13 | 31 | 18 | 7 | 8 | 100 | |

| Other Inactive | 39 | 7 | 10 | 17 | 11 | 6 | 11 | 100 | |

| All Persons | 29 | 10 | 17 | 23 | 11 | 4 | 6 | 100 | |

| Source: Wealth and Assets Survey, Office for National Statistics | |||||||||

| Notes: | |||||||||

| 1. Includes all households - including those who rent their main accommodation. | |||||||||

| 2. Combined figure for temporarily sick / injured and long term sick and disabled. | |||||||||

| 3. ".." - estimates that have been suppressed due to fewer than 30 unweighted cases. | |||||||||

Download this table Table 3.19: Individuals by economic activity, by household net property wealth

.xls (27.1 kB)Socio-economic group

Over two-thirds of individuals who had routine occupations lived within a household without property wealth (62%), compared with just over 1 in 10 (11%) of individuals classified as working in large employer and higher managerial positions.

The percentage of individuals living within households in the net property wealth band of £500,000 or more was highest for those individuals classified as working within the large employer and higher managerial socio-economic grouping; 14% of such individuals lived within a household with net property wealth of £500,000 or more. The second highest percentage of individuals living in households belonging to the highest net property wealth band were those working within intermediate occupations (12%).

Table 3.20: Individuals by socio-economic classification, by household net property wealth

| Individuals by socio-economic classification, by household net property wealth1: Great Britain, July 2012 to June 2014 | ||||||||

| % | ||||||||

| Do not own property | Less than £50,000 | £50,000 but < £125,000 | £125,000 but < £250,000 | £250,000 but < £375,000 | £375,000 but < £500,000 | £500,000 or more | All Households | |

| Large employers and higher managerial | 11 | 11 | 18 | 24 | 15 | 8 | 14 | 100 |

| Higher professional | 15 | 13 | 20 | 25 | 13 | 6 | 8 | 100 |

| Lower managerial and professional | 21 | 12 | 18 | 27 | 12 | 4 | 5 | 100 |

| Intermediate occupations | 22 | 10 | 16 | 22 | 13 | 5 | 12 | 100 |

| Small employers and own account workers | 30 | 15 | 21 | 23 | 7 | 2 | 2 | 100 |

| Lower supervisory and technical | 40 | 10 | 19 | 20 | 7 | 2 | 2 | 100 |

| Semi-routine occupations | 48 | 9 | 18 | 19 | 5 | 1 | 1 | 100 |

| Routine occupations | 62 | 6 | 10 | 12 | 4 | 3 | 4 | 100 |

| Never worked/long term unemployed | 36 | 5 | 13 | 23 | 11 | 5 | 7 | 100 |

| All Persons2 | 29 | 10 | 17 | 23 | 11 | 4 | 6 | 100 |

| Source: Wealth and Assets Survey, Office for National Statistics | ||||||||

| Notes: | ||||||||

| 1. Includes all households - including those who rent their main accommodation. | ||||||||

| 2. Includes only adults who are 16 years old and above, not in full time education and gave sufficient information to determine socio-economic group. | ||||||||

Download this table Table 3.20: Individuals by socio-economic classification, by household net property wealth

.xls (28.2 kB)9. Quality assuring property wealth data

Ownership of main residence

The following section examines how the ownership rates for a household’s main residence compare across a number of different sources. Ownership here includes any household who owns their main residence outright, with help from a mortgage or through a shared ownership scheme.

Ownership rates for a households main residence were: 64% in the 2011 Census (covering England and Wales only); 63% from Family Resources Survey 2013/14 (covering Great Britain); 63% from the English Housing Survey 2013 to 2014 (covering England only); and 67% in the General Lifestyle Survey 2011 (covering Great Britain). WAS is reasonably consistent figure for 2010/12, indicating an ownership rate of 66%. These are presented in Figure A.

Figure 3A: Comparison of main residence ownership rates, by source of data

Great Britain, July 2006 to June 2014

Source: Wealth and Assets Survey - Office for National Statistics

Download this chart Figure 3A: Comparison of main residence ownership rates, by source of data

Image .csv .xlsA notable disparity in ownership rates is that those in London are lower. For London, Family Resources Survey 2013/14 data indicates an ownership rate of 50% and the 2011 Census indicated an ownership rate of 49%.

Property valuation comparisons

There are a number of sources of data for the valuation of properties. While it is important to compare the WAS data with these other sources, it has to be remembered that they are derived in very different ways. In particular the WAS estimates of gross value of main residence are based on self-valuation.

Table B shows the average house price values produced from WAS and 3 other data sources, for the time periods equivalent to wave 1, 2, 3 and 4 of WAS . These figures are broken down by type of property.

Table 3.B: Value of main residence by dwelling type

| Great Britain, July 2006 to June 2014 | ||||

| £ | ||||

| July 2012 to June 2014 | July 2010 to June 2012 | July 2008 to June 2010 | July 2006 to June 2008 | |

| Detached | ||||

| Land registry | 259,000 | 255,000 | 247,000 | 266,000 |

| Halifax | 302,000 | 277,000 | 282,000 | 324,000 |

| Nationwide | 238,000 | 231,000 | 224,000 | 244,000 |

| WAS | 411,000 | 390,000 | 319,000 | 327,000 |

| Semi-detached | ||||

| Land registry | 155,000 | 153,000 | 151,000 | 166,000 |

| Halifax | 183,000 | 163,000 | 166,000 | 198,000 |

| Nationwide | 160,000 | 160,000 | 156,000 | 174,000 |

| WAS | 238,000 | 222,000 | 196,000 | 202,000 |

| Terraced | ||||

| Land registry | 124,000 | 123,000 | 123,000 | 137,000 |

| Halifax | 170,000 | 147,000 | 148,000 | 184,000 |

| Nationwide | 143,000 | 135,000 | 131,000 | 148,000 |

| WAS | 225,000 | 208,000 | 179,000 | 178,000 |

| Flat | ||||

| Land registry | 155,000 | 151,000 | 149,000 | 166,000 |

| Halifax | 193,000 | 158,000 | 154,000 | 189,000 |

| Nationwide | 137,000 | 127,000 | 131,000 | 135,000 |

| WAS | 228,000 | 199,000 | 166,000 | 173,000 |

| Source: Land Registry, Halifax, Nationwide, Office for National Statistics | ||||

| Notes: | ||||

| 1. This section provides brief details on the methodology used by the Land Registry, Nationwide and Halifax in producing house prices indicators based on property sales data: | ||||

| The Land Registry has a record of all residential transactions in England and Wales since 1995. This dataset constitutes 16 million sales, of which 6 million are properties that have been resold during this period. The identification of these properties allow for a technique called repeated-sales regression to produce a housing price index which tracks changes in house prices over time. The ‘average prices’ reported by the Land Registry are standardised by taking a geometric mean price in April 2000 and adjusting it using the index, both backwards to 1995 and forwards to the present day. The average prices are also seasonally adjusted using classical seasonal decomposition methods. | ||||

| Nationwide is the second largest mortgage lender (by stock) in the UK, and using data for mortgages that are at approvals stage, it calculates a housing price index to gives current indications of the housing market. The house price data consist of mix-adjusted prices, which gives an indication of how the price of a typical property changes over time. The prices are also seasonally adjusted. See http://www.nationwide.co.uk/hpi/default.asp for further information. | ||||

| Halifax uses similar methods as those used by Nationwide in standardising house prices, and as such, both of these mortgage lenders produce similar housing price indices over time. Differences between the two indices are primarily due to the differences in their samples. Like Nationwide, Halifax takes into account various attributes associated with each property transacted. These attributes refer to both quantitative (e.g., age, number of rooms) or qualitative (e.g. location, type) characteristics of the property, and are translated into factors in a multivariate regression model to produce a standardised price. As a result, this technique allows the price of a ‘typical’ house to be tracked over time on a like-for-like basis. Both seasonally adjusted, and non-seasonally-adjusted house prices data for UK regions and different dwelling types are available on the Halifax website. For more details see http://www.lloydsbankinggroup.com/media1/research/halifax_hpi.asp | ||||

Download this table Table 3.B: Value of main residence by dwelling type

.xls (30.7 kB)The values derived from these external sources vary considerably, with the Halifax data being consistently higher than both the Land Registry and Nationwide. While, in 2006 to 2008 WAS results are very similar to or lower than the Halifax estimates, WAS is consistently higher than all 3 sources in the subsequent waves. This could indicate that households tend to overestimate the value of their property, and moreover, may not adjust their valuation in line with the market, particularly in times of falling house prices. While the perceived value of property may lead to an over-estimate of property wealth compared with market price indicators, it is nonetheless a useful indicator. It is the perceived value that may be influencing the behaviour of households with respect to their property assets as well as their other assets such as financial, pensions and, to a lesser extent, their physical wealth.

Trends in the Great Britain housing market

Figure C presents the long term-trend in the housing market in Great Britain using the ONS House Price Index. It then considers these trends in the context of the time period covered by the Wealth and Assets Survey.

Since the 1970s, the housing market has been characterised by 2 sustained periods of rapid increase (in the 1980s, and between the mid 1990s and the late 2000s) and 2 shorter periods of decrease (beginning in 1990 and in 2008). The data used for Figure C are based upon the mix-adjusted house price index (source: ONS).

The Great Britain housing market boom during the 2000s

This increase in house prices, which began around the mid 1990s, continued throughout much of the 2000s. There were several reasons for this prolonged period of price rises in the housing market. Up until 2008, Great Britain experienced strong economic growth and consumer confidence. Mortgages were also readily available as banks offered competitive interest rates and high loan-to-value (95% to 100%) mortgages to their customers. As a result, people from a wide range of income levels were able to obtain a mortgage to purchase their homes. The high demand for housing, coupled with a relatively low housing supply, pushed up house prices.

Figure 3C: The United Kingdom housing market over time – ONS’s House Price indices

Great Britain, Quarter 1 (Jan to Mar) to Quarter 2 (Apr to Jun) 2015

Source: Wealth and Assets Survey - Office for National Statistics

Download this chart Figure 3C: The United Kingdom housing market over time – ONS’s House Price indices

Image .csv .xlsThe Great Britain housing market since 2006

The WAS commenced its first wave in Quarter 3 (July to Sept) 2006. The majority of wave 1 was characterised by a continued rise in house prices, although this tailed off and began to decline towards the end of the wave. The Great Britain housing market experienced a decline throughout 2008 and including Quarter 1 (Jan to Mar) 2009 that is, the first year of the second wave of the survey, but began to recover in the second half of wave 2. As with the boom, there were several reasons for the housing market decline. One of the most significant factors was the credit crisis, during which banks were unable to lend due to a sudden shortage of funds (see Endnote 1). The reluctance of banks to lend higher-LTV and other higher-risk meant that mortgages were not as readily available. From Quarter 2 (Apr to June) 2009, house prices started rising again until Quarter 2 (Apr to June) 2010, since then the market has been a little more volatile.

Equity release

In WAS wave 4 data, the total value of equity release mortgages was just over £7.3 billion. This was made up of £3.5 billion (48%) lifetime mortgages, £2.0 billion (27%) home reversions and £1.8 billion (24%) private unknown schemes.

According to Mortgage Lending and Administration Return (MLAR) data that is reported by all regulated lenders, in 2012 to 2014, the total value of lifetime mortgages was around £8 billion, of which around £6 billion were regulated mortgages (so sold after 31 October 2004) and under £2bn were non-regulated mortgages (so sold before 31 October 2004 and those secured on buy to let properties). So WAS only slightly understates the size of this market, with around 10% of the market not captured.

Owner-occupier housing stock and wealth

Owner-occupier housing stock are considered using the following data:

- Department for Communities and Local Government (DCLG) produce live tables of dwellings

Table 3.D: Comparing DCLG figures for dwelling stock by tenure with WAS

| Great Britain, July 2010 to June 2014 | |||||||||

| Thousands of dwellings | |||||||||

| DCLG Results | WAS July 2010 to June 2014 Results1 | Differences | |||||||

| Owner Occupied | All Rented Dwellings2 | All Dwellings | Owner occupied | Rented privately or with a job or business | All Dwellings | Owner occupied | Rented privately or with a job or business | All Dwellings | |

| 20105 | |||||||||

| 20115 | 17,387 | 9,468 | 26,855 | 16,481 | 7,453 | 24,228 | -906 | -2,015 | -2,627 |

| 2012 | |||||||||

| 20135 | 17,204 | 9,948 | 27,151 | 17,005 | 8,324 | 25,615 | -199 | -1,624 | -1,536 |

| Source: Office for National Statistics | |||||||||

| Notes: | |||||||||

| 1. WAS data collected over a two year period; July 2010 to June 2014. | |||||||||

| 2. Includes 'Rented privately or with a job or business', 'Rented from housing associations', 'Rented from Local Authorities' and 'Other public sector dwellings'. | |||||||||

| 3. For detailed definitions of all tenures, see Definitions of housing terms in Housing Statistics home page. 'Other public sector dwellings' figures are currently only available for England. | |||||||||

| 4. Figures for census years are based on census output. | |||||||||

| 5. Series from 1992 to 2011 for England has been adjusted so that the 2001 and 2011 total dwelling estimate matches the 2001 and 2011 Census. | |||||||||

| 6. From 2003 the figures for owner-occupied and the private rental sector for England have been produced using a new improved methodology as detailed in the dwelling stock release. Previous to this vacancy was not accounted for. | |||||||||

Download this table Table 3.D: Comparing DCLG figures for dwelling stock by tenure with WAS

.xls (27.6 kB)As can be seen, the overall the number of dwellings is slightly less for the WAS. For the owner-occupied group of dwellings the WAS captures 99% of those present in the DCLG series. For all dwellings the WAS captures just over 94% of the DCLG counts. There are larger differences between the rented portion of dwellings but this could be down to definitional differences between the DCLG and WAS.

Owner-occupier housing wealth was compared by using the following data:

the WAS owner-occupier data for wave 4 is 17.4 million dwellings

the simple average house price for Great Britain in 2013, taken from the ONS’s HPI series, stood at £252,000

by multiplying these two elements together we get a level of household wealth that can be compared to the WAS gross wealth

Results indicate that the WAS wave 4 data might overstate the total value of owner-occupier housing wealth by 14%. However, house value is a subjective measure that cannot be assessed accurately unless the house is sold.

Table 3.E: Average house price comparisons

| Great Britain, July 2012 to June 2014 | ||||

| £ thousands | ||||

| Average GB house price from HPI (2013) | Number of owner occupied dwellings from WAS (Wave 4) | Estimate of owner occupied property wealth | Estimate of owner occupied property wealth from WAS wave 4 | Percentage Differences (%) |

| 252 | 17,400 | 4,384,800 | 4,984,000 | 14% |

| Source: Office for National Statistics | ||||

Download this table Table 3.E: Average house price comparisons

.xls (24.1 kB)Endnotes

The credit crisis in 2007 originated from a number of ‘subprime’ mortgages being sold to customers with low income and poor credit in the US during the early part of the 2000s. To finance further lendings, mortgage companies bundled debts into consolidation packages and sold to other financial companies. In most of these subprime mortgages, the interest rate is fixed for the first two years, but increases thereafter. Along with rising fuel and food costs, many people with subprime mortgages were unable to afford their mortgage repayments and, therefore, had to default on their mortgages. This signalled the end of the housing market boom in the US as house prices began to fall. Many mortgage companies also went bankrupt because of the number of mortgage defaults. Banks were also forced into writing off bad debts that they had bought from these mortgage companies. As a result, banks became reluctant to lend, and therefore it became more difficult to borrow money.

Council of Mortgage Lenders: Published data and reports on the buy-to-let market.

When comparing WAS data with other sources, gross property wealth has been used (that is, including both main residences and other property) as this better reflects the coverage of the other sources. However, it should be noted that the regional split for the WAS is based on the region of residence for a household’s main dwelling. Other properties may be in a different region.

Technical notes

This section provides brief details on the methodology used by the Land Registry, Nationwide and Halifax in producing house prices indicators based on property sales data.

The Land Registry has a record of all residential transactions in England and Wales since 1995. This dataset constitutes 16 million sales, of which 6 million are properties that have been resold during this period. The identification of these properties allow for a technique called repeated-sales regression to produce a housing price index which tracks changes in house prices over time. The ‘average prices’ reported by the Land Registry are standardised by taking a geometric mean price in April 2000 and adjusting it using the index, both backwards to 1995 and forwards to the present day. The average prices are also seasonally adjusted using classical seasonal decomposition methods.

The Land Registry collects information on all transactions regardless of method of purchase, and therefore is not only restricted to mortgage purchases. However, the dataset only includes transactions at full market value, and excludes sales from repossessions and auctions as they do not reflect full market price. Also, the data from the Land Registry are only available for England and Wales. For more details, visit the Land Registry website.

Nationwide is the second largest mortgage lender (by stock) in the UK, and using data for mortgages that are at approvals stage, it calculates a housing price index to gives current indications of the housing market. The house price data consist of mix-adjusted prices, which gives an indication of how the price of a typical property changes over time. The prices are also seasonally adjusted. Please visit the Nationwide website for further information.

Halifax uses similar methods as those used by Nationwide in standardising house prices, and as such, both of these mortgage lenders produce similar housing price indices over time. Differences between the 2 indices are primarily due to the differences in their samples. Like Nationwide, Halifax takes into account various attributes associated with each property transacted. These attributes refer to both quantitative (for example, age, number of rooms) or qualitative (for example, location, type) characteristics of the property, and are translated into factors in a multivariate regression model to produce a standardised price. As a result, this technique allows the price of a ‘typical’ house to be tracked over time on a like-for-like basis. Both seasonally adjusted, and non-seasonally-adjusted house prices data for UK regions and different dwelling types are available on the Halifax website. For more details visit the Lloyds Banking Group website.