Table of contents

- Main points

- Footfall

- Business impact of the coronavirus

- Social impacts of the coronavirus on Great Britain

- Online job adverts

- Online price change for high-demand products (HDPs)

- Energy Performance Certificates

- Shipping

- Universal Credit

- Data

- Glossary

- Measuring the data

- Strengths and limitations

- Related links

1. Main points

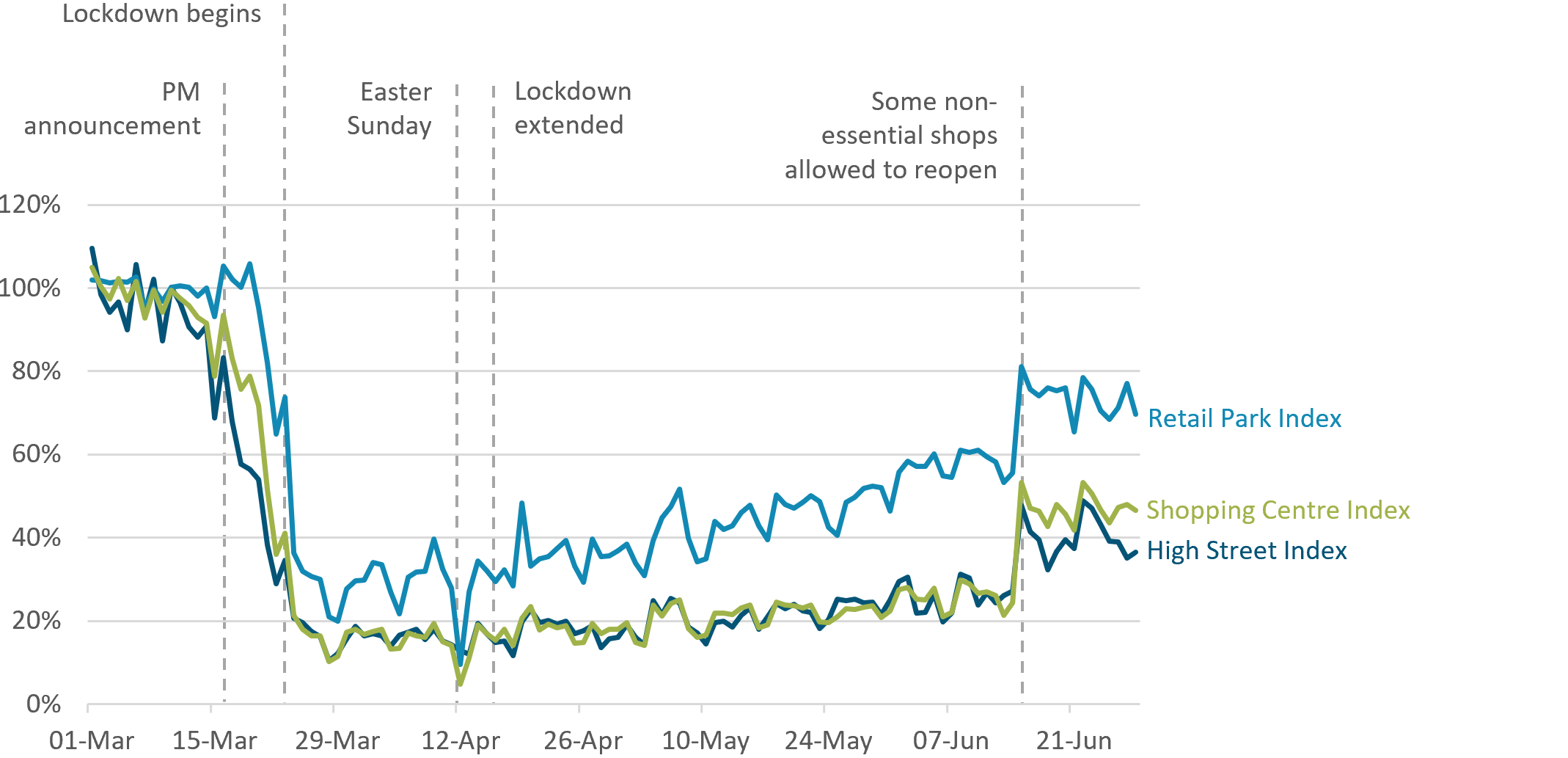

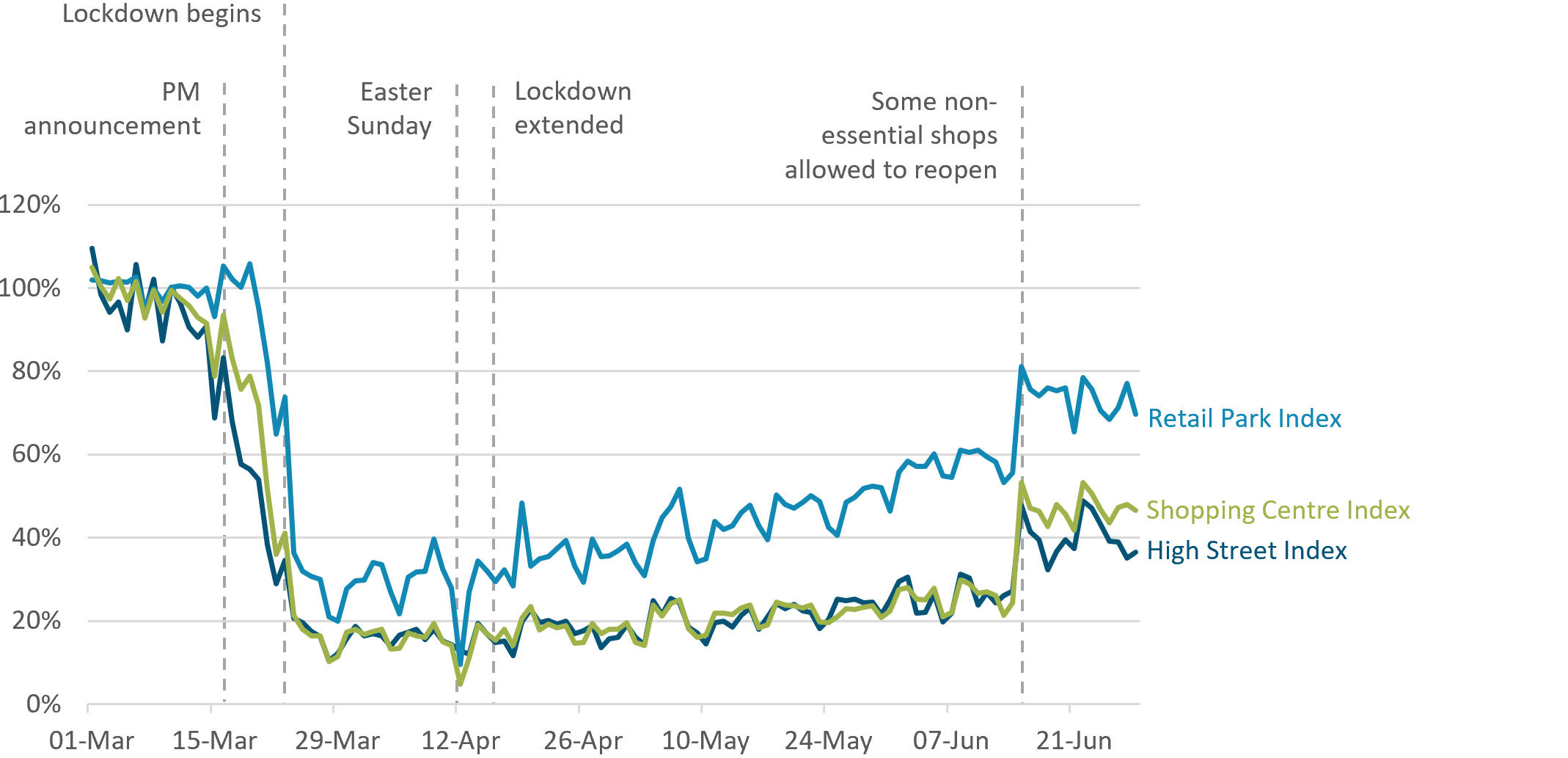

Daily footfall at shopping destinations saw a substantial increase on 15 June 2020, when some non-essential shops were first allowed to reopen in England.

Retail park footfall has shown a stronger overall recovery than shopping centres and high streets since March, though shopping centres saw the strongest growth on 15 June.

According to the latest Business Impact of Coronavirus Survey (BICS) collected 15 to 28 June, 23% of the workforce were on furlough, with 68% of those receiving wage top-ups from their employer in addition to the Coronavirus Job Retention Scheme.

According to the latest Opinions and Lifestyle Survey (collected 25 to 28 June), the proportion of working adults travelling to work increased to 49%, up from 44% the previous week.

Between 19 June and 26 June, job adverts across all industries remained around half of their 2019 average.

The number of Energy Performance Certificates for new homes fell by 76% from March to April 2020, but has partially recovered since then, with June levels 24% below their March level.

Total daily ship visits increased from 4,579 between 1 and 14 June to 5,316 visits between 15 June and 28 June, but daily visits have declined slightly in the second half of the most recent week.

In the week 17 to 23 June 2020, the volumes of individual and household universal credit declarations decreased to levels similar to early March, while the volume of new claim advances was below its level immediately before the announcement on 16 March.

The Business Impact of COVID-19 Survey (BICS) is voluntary and currently unweighted, so it may only reflect the characteristics of those who responded. Online price change analysis is experimental and should not be compared with our regular consumer price statistics. Results presented are experimental.

2. Footfall

These figures are provided by Springboard, a provider of data on customer activity. They measure the volume of footfall compared with the same day the previous year, across the categories of high streets, retail parks and shopping centres. For example, Tuesday 30 June 2020 was compared with Tuesday 2 July 2019.

Figure 1: Footfall saw a substantial increase on 15 June 2020, when some non-essential shops were first allowed to reopen in England

Volume of footfall, UK, 1 March to 28 June, year-on-year percentage change between footfall on the same day

Source: Springboard and the Department for Business, Energy and Industrial Strategy

Notes:

- Many essential shops were allowed to open on 12 June 2020 in Northern Ireland and 22 June in Wales. In Scotland, some non-essential shops were allowed to reopen from 29 June, and more from 13 and 15 July.

- Prime Minister's announcement refers to the advisory announcement on 16 March 2020 to avoid non-essential travel, bars, restaurants and other indoor leisure venues, and to work from home if possible.

Download this image Figure 1: Footfall saw a substantial increase on 15 June 2020, when some non-essential shops were first allowed to reopen in England

.png (157.8 kB){kind=link}

In the two weeks from 16 March 2020, footfall in high streets and shopping centres declined below 20% of its level the same time last year, while retail parks saw a slightly smaller decrease. This is reflected with a large upward movement in all three indices, with shopping centres seeing the greatest increase, for which footfall more than doubled from 14 June to 15 June 2020. On 28 June, footfall in retail parks had increased to around 70% of its level the same time last year, while footfall in shopping centres was just under 50% and that in high streets was below 40% of its level in the same period last year.

On 15 June, many types of non-essential shops and businesses were allowed to reopen in England. This is reflected with a large upward movement in all three indices, with shopping centres seeing the greatest increase, footfall more than doubling from 14 June to 15 June.

Note that while footfall in high streets and shopping centres has followed a very similar pattern, the trend of retail parks is somewhat different. Following the Prime Minister’s announcement on 16 March, retail parks saw their footfall drop roughly one week later than high streets and shopping centres. Their initial drop in footfall was somewhat less severe, and the recovery in footfall through April and May was greater, compared with the other two categories, reflecting that many essential stores are often at retail parks.

Back to table of contents3. Business impact of the coronavirus

This section includes final results from Wave 7 of the Business Impact of Coronavirus (COVID-19) Survey (BICS) for the period 1 June to 14 June 2020, which closed on 28 June 2020. Out of a sample of 24,473 businesses, 24% of businesses responded. Please see the section Measuring the data for information on recent sample changes.

Figure 2: 23% of the workforce1 were on furlough, with 68% of the workforce receiving wage top-ups to the Coronavirus Job Retention Scheme

Headline indicators from the Business Impact of Coronavirus Survey, 1 June to 14 June, UK

Embed code

Notes

All percentages are a proportion of the number of businesses who responded apart from the workforce percentages on furlough leave and receiving pay top-ups, which are apportioned by workforce size.

Businesses were asked for their experiences for the reference period 1 June to 14 June 2020, but for questions regarding to their experiences of the past two weeks or expectations in the next two weeks, businesses may respond from the point of completion of the questionnaire (15 June to 28 June).

Between 1 and 14 June 2020, 86% of businesses were trading (Figure 2), with 80% of businesses trading for more than the last two weeks prior to completing the questionnaire. The remaining 6% said they had restarted trading in the last two weeks after a pause in trading.

Of the businesses trading, 6% of their total workforce had returned from furlough in the two weeks prior to completing the questionnaire, while 2% returned from remote working to their normal workplace.

68% of the furloughed workforce of businesses not permanently stopped trading had their pay topped up. Those businesses within education, and human health and social work activities (private sector businesses only) reported the largest proportion of the furloughed workforce receiving top-ups, at 97% and 92% respectively.

Of all businesses who had not permanently stopped trading, 47% said they had less than six months or no cash reserves. Of accommodation and food service activities businesses, 67% reported less than six months or no cash reserves, followed by 58% of construction businesses.

The impact of the coronavirus on capital expenditure was asked about for the first time in Wave 7; see Figure 3.

Figure 3: 42% of businesses continuing to trade said that capital expenditure had stopped or was lower than normal because of the coronavirus (COVID-19)

Percentage of businesses continuing to trade, UK, 1 June to 14 June 2020

Source: Office for National Statistics – Business Impact of Coronavirus Survey

Notes:

- Bars may not sum to 100% because of rounding.

- Other services and mining and quarrying have been removed for disclosure purposes.

- For questions regarding capital expenditure businesses may respond from the point of completion of the questionnaire (15 June to 28 June 2020).

- BICS collects data from private sector businesses only so public sector capital expenditure is excluded from these data - more information on the sample coverage can be found in Measuring the data.

Download this chart Figure 3: 42% of businesses continuing to trade said that capital expenditure had stopped or was lower than normal because of the coronavirus (COVID-19)

Image .csv .xlsOf businesses continuing to trade, the arts, entertainment and recreation industry had the highest proportion of businesses reporting that capital expenditure had stopped or was lower than normal, at 57% (40% in this sector reported it had stopped completely, the highest of any industry). This was followed by accommodation and food service activities, with 56% of businesses continuing to trade in this industry stopping or reducing their capital expenditure.

Of businesses in private sector human health and social work activities, 18% reported that capital expenditure was higher than normal, the highest of any industry.

More about coronavirus

- Find the latest on coronavirus (COVID-19) in the UK.

- All ONS analysis, summarised in our coronavirus roundup.

- View all coronavirus data.

- Find out out how our studies and surveys are serving public need.

5. Online job adverts

These figures use job adverts provided by Adzuna, an online job search engine. These estimates are experimental and will be developed over the coming weeks. The number of job adverts over time is an indicator of the demand for labour.

Figure 5: Between 19 June and 26 June 2020, job adverts across all industries remained around half of their 2019 average

Total weekly job adverts on Adzuna, UK, 4 January 2019 to 26 June 2020: index 2019 average = 100

Embed code

Notes:

The observations were collected on a roughly weekly basis; however, they were not all observed at the same point in each week, leading to slightly irregular gaps between each observation.

These series have a small number of missing weeks, mostly in late 2019, and the latest is in January 2020. These values have been imputed using linear interpolation. The data points that have been imputed are clearly marked in the accompanying dataset.

Further category breakdowns are included in the Online job advert estimates dataset, and more details on the methodology can be found in Using Adzuna data to derive an indicator of weekly vacancies.

Between 19 and 26 June 2020, total online job adverts stood at around half of their 2019 average. They decreased slightly from 53% to 51% of their 2019 average, following five consecutive weeks of growth since 15 May 2020.

Out of the 29 Adzuna categories, 23 categories saw an increase in job adverts between 19 and 26 June 2020 whilst six Adzuna categories saw a decrease. Declining job adverts have been noticeable in the healthcare, wholesale and retail, and IT categories, which have fallen 4, 2 and 24 percentage points respectively between 19 and 26 June 2020. Note the large decline in the IT sector job adverts could be driven by volatility in the series, so it will be monitored in future weeks.

The volume of online job adverts in catering and hospitality continued to increase from 27% to 29% of its 2019 average, reflecting a growing expectation for pubs and bars to reopen. Job adverts in the education industry also continued to increase in the latest period.

The categories presented here were selected because of user interest, and because they more closely track trends in the Office for National Statistics (ONS) vacancies data. Note that the Adzuna categories used do not correspond to Standard Industrial Classification (SIC) categories, so these values are not directly comparable with the ONS Vacancy Survey.

The Institute for Employment Studies are also using Adzuna data to produce weekly vacancy indicators, and more granular breakdowns of these data can be found in their release.

Back to table of contents6. Online price change for high-demand products (HDPs)

A timely indication of weekly price change for high-demand products (HDPs) has been developed, covering the period 16 March to 28 June 2020.

As experimental indices, these data are subject to revisions as we develop our methodology and systems. This week we have made some changes to the way we classify products and calculate average weekly prices. A full timeline of developments for these indicators can be found in Online price changes of high-demand products methodology.

This analysis should not be compared with our regular consumer price statistics.

Figure 6: Overall, prices of items in the high-demand product basket remained stable between weeks 14 and 15

Online price change of high-demand products, UK, percentage change between week 14 (15 to 21 June) and week 15 (22 to 28 June)

Source: Office for National Statistics – Faster indicators

Notes:

- More information on the strengths and limitations of the online price changes data is available in the Online price changes of high-demand products methodology article.

Download this chart Figure 6: Overall, prices of items in the high-demand product basket remained stable between weeks 14 and 15

Image .csv .xlsFigure 6 shows that the all-HDP items index has remained stable between week 14 and week 15. Out of the 23 items, 20 changed by less than 0.5% in absolute terms.

The largest item-level price change between week 14 and week 15 was for vitamin C, where prices increased by 3.1%. Vitamin C prices had fallen in previous weeks as products were on sale, and these sales have now ended causing prices to bounce back. The overall series is now 0.4% higher compared with prices in week 1 (Figure 7).

Antibacterial hand wipes saw the largest price fall, decreasing by 0.7% between week 14 and week 15.

Figure 7 shows that the all-HDP items index remains below its level in week 1, decreasing by 0.2% between week 1 and week 15. The all food, and all household and hygiene indices have also seen decreases in prices this week, putting them slightly above their levels in week 1.

Figure 7: Overall, prices for food, and household and hygiene items have returned to similar levels as seen in March 2020

Online price change of selected high-demand products, UK, 16 March to 28 June 2020

Source: Office for National Statistics – Faster indicators

Notes:

- Index movements may not be exactly the same as percentage changes shown in Figure 6 as a result of rounding.

- Week 1 refers to the period 16 to 22 March 2020, and week 15 refers to the period 22 to 28 June 2020.

- The time series for all individual HDP items are published in a dataset alongside this release.

Download this chart Figure 7: Overall, prices for food, and household and hygiene items have returned to similar levels as seen in March 2020

Image .csv .xls7. Energy Performance Certificates

An Energy Performance Certificate (EPC) contains information on the energy efficiency of a property and is a requirement when a property is built, sold or rented in England and Wales. The data are published daily by the Ministry of Housing, Communities and Local Government (MHCLG) on the EPC register website (for England and Wales). As such, they can be used as a timely indicator for the number of completed constructions and number of transactions.

EPCs are also required for existing properties that are converted or have changed use. To note, an EPC is valid for 10 years, therefore if a house is sold more than once in that period it may not appear in the data.

Figure 8 shows a fall in the number of EPCs generated and lodged during April, which coincides with the first full month after government guidance was issued on 26 March 2020 requesting delays to property moves and restrictions on viewings. An EPC requires an energy assessor to physically visit a property to conduct the assessment. In addition, a reduction in construction would contribute to the delay in EPC assessments of new dwellings. EPC lodgements for both new and existing dwellings started to recover in May and June, though EPCs for new dwellings grew at a slower rate.

You can find out more about the impact of coronavirus on the housing market in Coronavirus and housing indicators in England and Wales published on 2 July 2020.

Figure 8: Existing Energy Performance Certificate lodgements fell by around 80% in April 2020, but rose again in May and June to around 125,000 lodgements in June

Energy Performance Certificates lodgements by month, non-seasonally adjusted, England and Wales, July 2019 to June 2020

Source: Ministry of Housing, Communities and Local Government (MHCLG)-Domestic Energy Performance Certificate Register

Notes:

- Data published 1 July 2020.

- Further notes are available on the EPC lodgement statistics webpage.

Download this chart Figure 8: Existing Energy Performance Certificate lodgements fell by around 80% in April 2020, but rose again in May and June to around 125,000 lodgements in June

Image .csv .xls8. Shipping

These shipping indicators are based on counts of all vessels, cargo and tanker vessels and passenger vessels. As discussed in Faster indicators of UK economic activity: shipping, we expect the shipping indicators to be related to the import and export of goods.

This week we have introduced daily and weekly passenger vessels from 1 April 2019 to 28 June 2020. The dataset contains both the seasonally adjusted and non-seasonally adjusted series as well as the trend shown in Figure 9.

Figure 9: Total daily ship visits increased between 1 to 14 June and 15 to 28 June 2020, but have declined slightly in the second half of the most recent week

Daily movements in shipping visits, UK, seasonally adjusted, 1 January 2020 to 28 June 2020

Source: exactEarth

Notes:

- The seasonally adjusted and trend estimates are estimated using a modified version of the seasonal adjustment method TRAMO-SEATS. More information is available in the Coronavirus and the latest indicators for the UK economy and society methodology.

- The seasonal adjustment method may be limited as this is a short time series, it will be fine-tuned in future releases.

- Daily and weekly shipping visits and unique visits are available by port in the dataset.

Download this chart Figure 9: Total daily ship visits increased between 1 to 14 June and 15 to 28 June 2020, but have declined slightly in the second half of the most recent week

Image .csv .xlsOn a seasonally adjusted basis, total daily ship visits increased to an average of 390 over the most recent week, 22 June to 28 June 2020 (Figure 9), which compares with an average of 369 in the previous week. Cargo and tanker visits rose slightly to an average of 106 visits from 103 visits in the previous period. Passenger visits have remained stable throughout June 2020, with a weekly average of 73 passenger visits in the latest weekly period.

Back to table of contents9. Universal Credit

Figure 10: In 17 to 23 June 2020, the volumes of individual and household Universal Credit declarations decreased to levels similar to early March

Embed code

Notes

- These declaration figures have not been derived to the same methodology as official statistics, and therefore the management Information and official statistics will not be directly comparable. Figures relate to Great Britain only, and Northern Ireland is not included.

The first chart in Figure 10 shows the number of new declarations, which is when an individual or household provides information on their personal circumstances to begin a Universal Credit (UC) claim. Note that not all declarations will go on to receive a payment.

Since the start of the coronavirus (COVID-19) pandemic, there have been unprecedented levels of demand for Universal Credit. Since 1 March 2020, the Department for Work and Pensions (DWP) has received 3.4 million individual declarations and 2.7 million household declarations. These volumes peaked on 27 March 2020, and since then they have gradually declined.

In the most recent week, declarations have decreased approximately to the levels seen immediately before the Prime Minister's advisory announcement on 16 March 2020. Across 17 to 23 June, there was an average of 11,056 individual declarations a day, slightly below the average of 11,151 a day across the first two weeks of March. Household declarations averaged 9,503 across the most recent week, compared with 9,349 across the first two weeks of March.

The second chart in Figure 10 shows the number of new claim advances, which provide support to new claimants in financial need until they receive their first regular payment of Universal Credit. In the latest week, new credit advances decreased below the level seen immediately before the lockdown announcement on 16 March. Across 17 to 23 June, there was an average of 3,774 new advance payments a day: substantially lower than the average of 4,309 across the first two weeks of March.

This is DWP’s last release of this weekly management information. After this release, Universal Credit information will continue to be released in the monthly and quarterly DWP official statistics publications.

Back to table of contents10. Data

Weekly and daily shipping indicators

Dataset | Released 2 July 2020

The weekly and daily shipping indicators dataset associated with the faster indicators of UK economic activity.

Online price changes for high-demand products

Dataset | Released 2 July 2020

Weekly online price changes of selected high-demand products (HDPs).

Online job advert estimates

Dataset | Released 2 July 2020

Experimental job advert indices covering the UK job market.

Business Impact of COVID-19 Survey (BICS) results

Dataset | Released 2 July 2020

Final results from the new BICS. This qualitative fortnightly survey covers business turnover, workforce, prices and trade. This dataset includes additional information collected as part of the survey including details on prices and imports and exports, which are not included within this bulletin or the Coronavirus and the economic impacts on the UK bulletin.

11. Glossary

Faster indicator

A faster indicator provides insights into economic activity using close-to-real-time big data, administrative data sources, rapid response surveys or experimental statistics, which represent useful economic and social concepts.

High-demand product (HDP) basket

The HDP basket contains everyday essential items that were identified at the beginning of the crisis to have high consumer demand, including items from food, health and hygiene categories. The selection of these items was based on anecdotal evidence on patterns of consumer spend. The basket does not cover all items within these categories.

Back to table of contents12. Measuring the data

The sample design for wave 7 of the Business Impact of Coronavirus (COVID-19) Survey (BICS) has been reviewed and refreshed to improve the coverage for smaller sized businesses.

Detailed information on the data sources, quality and methodology of the different indicators included in this bulletin is available in the Coronavirus and the latest indicators of the UK economy and society methodology.

We will summarise any crucial updates to the quality or methodology in this section in the future.

Back to table of contents13. Strengths and limitations

Detailed information on the strengths and limitations of the different indicators included in this bulletin is available in the Coronavirus and the latest indicators of the UK economy and society methodology.

We will summarise any crucial updates or caveats in this section in the future.

Back to table of contents

4. Social impacts of the coronavirus on Great Britain

This section includes some headline results from Wave 15 of the Opinions and Lifestyle Survey (OPN) covering the period 25 to 28 June 2020. The full results will be published in Coronavirus and the social impacts on Great Britain on 3 July 2020.

Figure 4 shows that the trend of people moving from working exclusively from home to travelling to work has continued in the latest wave. The proportion of adults travelling to work has increased to 49%, from 44% the previous week, while the proportion working from home has dropped to 29%, from 33% the week before.

This supplements findings from the latest Business Impacts of Coronavirus Survey (BICS) collected between 15 and 28 June, where businesses continuing to trade reported 2% of the total workforce had returned from remote working in the two weeks prior to completing their questionnaire.

Figure 4: The proportion of working adults travelling to work increased to 49%, from 44% in the previous week, while the proportion working exclusively from home dropped to 29%

Proportion of adults, Great Britain, 20 March to 28 June 2020

Source: Office for National Statistics – Opinions and Lifestyle Survey

Notes:

Download this chart Figure 4: The proportion of working adults travelling to work increased to 49%, from 44% in the previous week, while the proportion working exclusively from home dropped to 29%

Image .csv .xls