Cynnwys

- Main points

- Business impact of the coronavirus

- Social impacts of the coronavirus on Great Britain

- Company incorporations and voluntary dissolution applications

- Online job adverts

- Online price change for high-demand products (HDPs)

- Energy Performance Certificates

- Footfall

- Road traffic

- Shipping

- Data

- Glossary

- Measuring the data

- Strengths and limitations

- Related links

1. Main points

Of businesses paused or currently trading, 10% said that their risk of insolvency was "moderate" and 1% said it was "severe", according to the latest Business Impact of Coronavirus (COVID-19) Survey (BICS). See Section 2.

The proportion of adults wearing a face covering at some point when leaving the home was at least 95% for the third consecutive week, according to the latest Opinions and Lifestyle Survey (OPN). See Section 3.

In the week starting Saturday 8 August, there were 3,002 incorporations per working day on average, a decrease from the previous week but still above the Quarter 3 (July to Sept) 2019 average (2,612 per working day). See Section 4.

Between 7 and 14 August 2020, the total volume of online job adverts decreased from 62% to 58% of its 2019 average, partially offsetting the large increase of the previous week. See Section 5.

The index for all food items within the high-demand product (HDP) basket increased by 0.3%, although the all items index remained static. See Section 6.

In the week commencing 10 August 2020, existing Energy Performance Certificate (EPC) lodgements in England remained around the level observed at the end of February 2020, while EPC lodgements for new dwellings remain below February 2020 levels across all regions. See Section 7.

Footfall across all retail locations continued to rise slightly in the latest week, with overall footfall at 68% of its level the same day a year ago, the highest since the week beginning 16 March 2020. See Section 8.

Road traffic across all motor vehicles has been gradually returning to pre-lockdown levels following a low point around the end of March 2020, using road traffic data from the Department for Transport (DfT). See Section 9.

Between 10 and 16 August 2020, the average volume of daily total ship visits and cargo ship visits both remained unchanged from the previous week. See Section 10.

The Business Impact of Coronavirus (COVID-19) Survey (BICS) is voluntary and currently unweighted, so it may only reflect the characteristics of those businesses that responded. Online price change analysis is experimental and should not be compared with our regular consumer price statistics. Results presented are experimental.

2. Business impact of the coronavirus

This section includes initial results from Wave 11 of the Business Impact of Coronavirus (COVID-19) Survey (BICS) for the period 27 July to 9 August 2020, which closes on 23 August 2020. Out of 23,905 businesses sampled, 21% had responded as of 18 August.

As a user of the BICS data, the Office for National Statistics (ONS) would like to hear your thoughts on the future of the survey. If you would like to provide your views, please complete our short questionnaire to help shape the future of BICS. The questionnaire will remain open until 21 August 2020.

Figure 1: 12% of the workforce remain on furlough leave, with 67% of furloughed employees receiving top ups to their pay

Headline indicators from the Business Impact of Coronavirus (COVID-19) Survey, UK, 27 July to 9 August 2020

Embed code

Source: Office for National Statistics - Business Impact of Coronavirus (COVID-19) Survey

Notes:

- All percentages are a proportion of the number of businesses that responded apart from the workforce percentages on furlough leave and receiving pay top-ups, which are proportions of employees for each responding business.

Download this chart

Of all responding businesses:

93% had been trading for more than the last two weeks

2% had started trading again within the last two weeks after a pause in trading

less than 1% had paused trading but intended to restart trading in the next two weeks

3% had paused trading and did not intend to restart in the next two weeks

less than 1% had permanently ceased trading

Table 1 shows the financial performance of businesses currently trading.

| Turnover has increased by more than 50% | <1% |

| Turnover has increased between 20% and 50% | 3% |

| Turnover has increased by up to 20% | 7% |

| Turnover has not been affected | 32% |

| Turnover has decreased by up to 20% | 23% |

| Turnover has decreased between 20% and 50% | 17% |

| Turnover has decreased by more than 50% | 11% |

| Not sure | 6% |

Download this table Table 1: Over half of currently trading businesses reported that their turnover had decreased below what is normally expected for this time of year

.xls .csvBusinesses were also asked about their risk of insolvency, shown in Figure 2.

Figure 2: 10% of businesses said that their risk of insolvency was “moderate”, and 1% said it was “severe”

Percentage of businesses not permanently stopped trading, UK, 27 July to 9 August 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- The percentages in this chart might not sum to 100% because of rounding and the removal of the category “the business is insolvent” as the result is less than 1%.

Download this chart Figure 2: 10% of businesses said that their risk of insolvency was “moderate”, and 1% said it was “severe”

Image .csv .xlsMore about coronavirus

4. Company incorporations and voluntary dissolution applications

Incorporations

Figure 4: In the week starting Saturday 8 August, there were 3,002 incorporations per working day on average, a decrease from the previous week, but above the Quarter 3 2019 average (2,612)

Company incorporations per working day, UK, quarterly and weekly, Quarter 1 (Jan to Mar) 2019 to Quarter 2 (Apr to June) 2020 and week commencing Saturday 28 February 2020 to week commencing Saturday 8 August 2020

Source: Companies House and Office for National Statistics

Notes:

Data presented per working day to allow comparison between quarterly data and weekly data and account for processing differences associated with Bank Holidays.

Quarterly data from Companies House official statistics release, divided by number of working days, presented at the mid-point of the calendar quarter.

Weekly data are for week commencing Saturday to Friday, as incorporation requests received on Saturdays and Sundays are typically processed on subsequent weekdays. For more information, see the accompanying Companies House methodology page.

Please note that Companies House quarterly Official Statistics include figures for Community Interest Company (CIC) incorporations, which are not included in the weekly series. Typically, these account for less than 1% of incorporations.

Download this chart Figure 4: In the week starting Saturday 8 August, there were 3,002 incorporations per working day on average, a decrease from the previous week, but above the Quarter 3 2019 average (2,612)

Image .csv .xlsIn the week starting Saturday 8 August, there was an average of 3,002 incorporations per working day, a substantial decrease from 3,332 in the previous week. While this decrease is a departure from the high levels observed in the previous two months, it is still higher than the Quarter 3 (July to Sept) 2019 average of 2,612 per working day.

The observed fluctuations in weekly incorporations per working day between April and early May 2020 and June and the end of July 2020 coincide with government-instigated lockdown measures and the subsequent easing of them in response to the coronavirus (COVID-19) pandemic. This is in line with official statistics published by Companies House on 30 July 2020.

Voluntary dissolution applications

Figure 5: For the week starting Saturday 8 August, there were 865 voluntary dissolution applications per working day on average, which remains lower than the Quarter 3 2019 average (1,008)

Company voluntary dissolutions applications per working day, UK, quarterly and weekly, Quarter 1 (Jan to Mar) 2019 to Quarter 2 (Apr to June) 2020 and week commencing Saturday 28 February 2020 to week commencing Saturday 8 August 2020

Source: Companies House and Office for National Statistics

Notes:

Data presented per working day to allow comparison between quarterly data and weekly data and account for processing differences associated with Bank Holidays. Quarterly data are presented at the mid-point of the quarter.

Weekly data are weeks from Saturday to Friday, as voluntary dissolution requests received on Saturdays and Sundays are typically processed on subsequent weekdays. For more information, see the accompanying Companies House methodology page.

Download this chart Figure 5: For the week starting Saturday 8 August, there were 865 voluntary dissolution applications per working day on average, which remains lower than the Quarter 3 2019 average (1,008)

Image .csv .xlsFor more information on other measures of company closures not presented here, see Weekly indicators of company creations and closures from Companies House methodology: August 2020.

Nôl i'r tabl cynnwys5. Online job adverts

These figures use job adverts provided by Adzuna, an online job search engine. We are able to include experimental estimates of online job adverts by Adzuna category and by UK country and NUTS1 regions, which will be developed over the coming weeks. The Adzuna categories used do not correspond to Standard Industrial Classification (SIC) categories, so these values are not directly comparable with the Office for National Statistics (ONS) Vacancy Survey. The number of job adverts over time is an indicator of the demand for labour.

Figure 6: Between 7 and 14 August 2020, the total volume of online job adverts decreased from 62% to 58% of its 2019 average, partially offsetting the large increase of the previous week

Total weekly job adverts on Adzuna, UK, 4 January 2019 to 14 August 2020, index 2019 average = 100

Embed code

Notes:

The observations were collected on a roughly weekly basis; however, they were not all observed at the same point in each week, leading to slightly irregular gaps between each observation.

These series have a small number of missing weeks, mostly in late 2019, and the latest is in January 2020. These values have been imputed using linear interpolation. The data points that have been imputed are clearly marked in the accompanying dataset.

Further category breakdowns are included in the Online job advert estimates dataset, and more details on the methodology can be found in Using Adzuna data to derive an indicator of weekly vacancies.

Download this chart

Although the total volume of online job adverts decreased from the previous week, online job adverts are still higher than they have been for the previous two months, when they remained close to half their 2019 average.

Of the 29 Adzuna categories, 16 increased compared with the previous week and 13 decreased. However, please note that some decreases at the category level have been affected by changes in Adzuna's coverage. See the Online job advert estimates dataset for more information.

Figure 7 shows the latest volume of online job adverts in each region compared with the 2019 average (blue bars), the percentage point change from the 2019 average to the lockdown minimum, which may be a different date for each region (yellow bars), and the percentage point change from the lockdown minimum to the latest value (blue dots).

Figure 7: In the latest week, the volume of online job adverts decreased in all four countries of the UK and in six of England’s nine NUTS1 regions

Total weekly job adverts on Adzuna, UK, 4 January 2019 to 14 August 2020: index 2019 average = 100, percentage points

Source: Adzuna

Notes:

Full series for each country and the NUTS1 regions are available in the accompanying dataset.

Note that from 7 August 2020, a new source for Northern Ireland has been included, leading to a discontinuity in the series.

Download this chart Figure 7: In the latest week, the volume of online job adverts decreased in all four countries of the UK and in six of England’s nine NUTS1 regions

Image .csv .xlsOn 14 August, out of the UK's countries and NUTS1 regions, online job adverts were closest to their 2019 average in Northern Ireland, where they were 74% of their 2019 average. The next closest region was the East Midlands at 73% of its 2019 average. While Northern Ireland had a comparatively small decline from its 2019 average to the lockdown minimum, the East Midlands saw the largest increase from its low point to its latest value.

Compared with the previous week, the largest percentage point decreases in online job adverts were in Northern Ireland (23 percentage points), followed by London (12 percentage points) and the West Midlands (10 percentage points). Online job adverts increased in the East Midlands by three percentage points, the only increase larger than one percentage point.

Nôl i'r tabl cynnwys6. Online price change for high-demand products (HDPs)

Online price indices for several high-demand products (HDPs) have been created using daily web-scraped data from several large online UK retailers (typically supermarkets and other prominent high-street chains) and provide an indication of weekly price change for items in the HDP basket. This analysis is experimental and should not be compared with our regular consumer price statistics.

Figure 8: Prices in the overall HDP basket remained static, though the all food index increased by 0.3%, driven by an increase in dried pasta and kitchen rolls

Online price change of high-demand products, UK, percentage change between week 21 (3 to 9 August 2020) and week 22 (10 to 16 August 2020)

Source: Office for National Statistics – Faster indicators

Notes:

- As well as food and household and hygiene products, the all items index contains items such as pet food and medicines, which means that the all items index sometimes moves differently to the two subseries.

Download this chart Figure 8: Prices in the overall HDP basket remained static, though the all food index increased by 0.3%, driven by an increase in dried pasta and kitchen rolls

Image .csv .xlsThe increases in prices of dried pasta and kitchen roll were driven by a number of retailers, while the decreases in pasta sauce, hand sanitiser and tinned soup were caused by some retailers putting these products on offer.

Figure 9: All three aggregate indices continued to remain below their week 1 level (16 March to 22 March)

Online price change of selected high-demand products 16 March to 16 August 2020: index week 1 (16 to 22 March 2020) = 100, UK

Source: Office for National Statistics – Faster indicators

Notes:

Index movements may not be exactly the same as percentage changes shown in Figure 8 as a result of rounding.

Week 1 refers to the period 16 to 22 March 2020, and week 22 refers to the period 10 to 16 August 2020.

The time series for all individual high-demand product (HDP) items are published in a dataset alongside this release.

Download this chart Figure 9: All three aggregate indices continued to remain below their week 1 level (16 March to 22 March)

Image .csv .xlsThis week, the time series has been revised because of improvements in the identification of unique products. A timeline of developments for these indicators can be found in Online price changes for HDPs methodology.

Nôl i'r tabl cynnwys7. Energy Performance Certificates

This release includes weekly Energy Performance Certificates (EPCs) for new and existing domestic properties in England and Wales up to the beginning 10 August 2020, split by NUTS1 English regions.

EPCs are used as a timely indicator for the number of completed constructions (new EPCs) and number of transactions (existing EPCs). The statistics are published weekly by the Ministry of Housing, Communities and Local Government (MHCLG).

Figure 10: In the week commencing 10 August 2020, existing EPC lodgements in England remained around the level observed at the end of February 2020, while EPC lodgements for new dwellings remained below February 2020 levels across all regions

Existing and new Energy Performance Certificates lodgements by region, non-seasonally adjusted, UK, February to August 2020, percentage change since week commencing 24 February 2020

Embed code

Source: Ministry of Housing, Communities and Local Government (MHCLG) Domestic Energy Performance Certificate Register

Notes:

Further notes are available in the weekly Energy Performance Certificates (EPCs) for domestic properties dataset.

More information on the EPC methods, strengths and limitations is available in the accompanying methodology article.

Week commencing 24 February 2020 is when the time series begins; we will look to expand this in the future.

Wales shown on a different scale. The spikes in the number of EPCs for existing dwellings seen in Wales during the weeks commencing 8 and 15 June 2020 were caused by some local authorities in Wales reviewing their social housing stock.

Download this chart

The percentage of new EPC lodgements was lowest in Yorkshire and The Humber, with new EPC lodgements 56% lower than that observed at the end of February (the next lowest was the North West, at 37% lower). A reduction in construction would contribute to the slower recovery of EPC assessments of new dwellings.

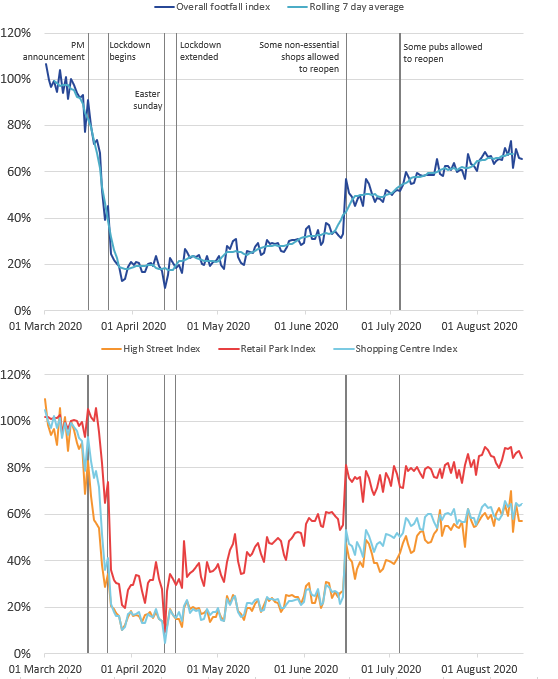

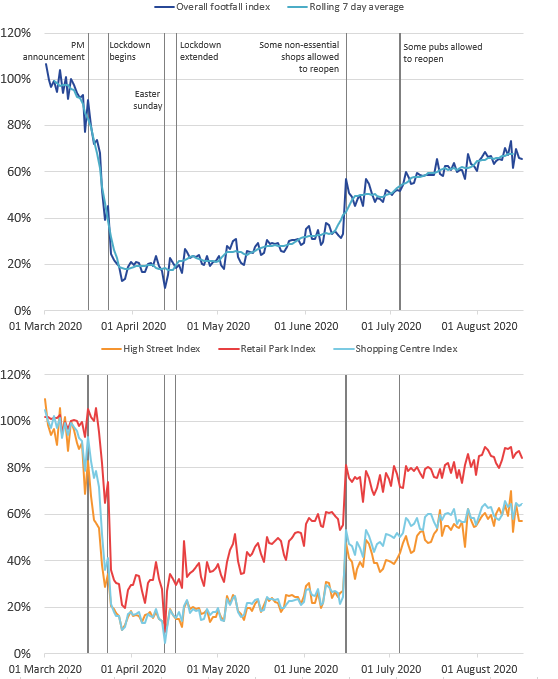

Nôl i'r tabl cynnwys8. Footfall

These figures are provided by Springboard, a provider of data on customer activity. They measure the volume of footfall compared with the same day the previous year at the overall level and across the categories of high streets, retail parks and shopping centres. For example, Tuesday 14 July 2020 was compared with Tuesday 16 July 2019.

Figure 11 shows the overall footfall seven-day average continued to increase in the latest week (10 to 16 August 2020), to just over two-thirds of the level on the same day a year ago. This continues the gradual increase in footfall seen since the reopening of non-essential shops and businesses in England on 15 June.

Footfall at all locations showed a small increase in the week commencing 10 August, with retail parks to over 85% compared with the same day a year ago and shopping centres and high streets at both over 60%.

This complements findings from our latest Business Impact of Coronavirus (COVID-19) Survey (BICS), which show 54% of applicable trading businesses have seen decreased footfall compared to what is normally expected for this time of year.

Figure 11: Footfall across all locations continued to rise slightly in the latest week, with overall footfall at 68% of its level the same day a year ago, the highest since the week beginning 16 March 2020

Volume of footfall, year-on-year percentage change between footfall on the same day, UK, 1 March to 16 August

Source: Springboard and the Department for Business, Energy and Industrial Strategy

Notes:

Many essential shops were allowed to open on 15 June 2020 in England, 12 June 2020 in Northern Ireland and 22 June 2020 in Wales. In Scotland, some non-essential shops were allowed to reopen from 29 June 2020 and more from 13 to 15 July 2020.

“Prime Minister’s announcement” refers to the advisory announcement on 16 March 2020 to avoid non-essential travel, bars, restaurants and other indoor leisure venues, and to work from home if possible.

Pubs were allowed to reopen on 4 July in both England and Northern Ireland, with beer gardens allowed to reopen on 6 July in Scotland and 13 July in Wales. Pubs were also allowed to reopen indoors in Scotland on 15 July.

Download this image Figure 11: Footfall across all locations continued to rise slightly in the latest week, with overall footfall at 68% of its level the same day a year ago, the highest since the week beginning 16 March 2020

.PNG (66.3 kB){kind=link}

9. Road traffic

This section introduces:

daily change in road traffic by selected vehicle types in Great Britain up to 17 August 2020, produced by the Department for Transport (DfT); this uses data from around 275 automatic traffic count sites across Great Britain covering all road types, which are published weekly

monthly road traffic counts on English motorways and major 'A' roads providing access to selected regional ports up to June 2020 using data from the Highways England's TRIS dataset; average 15-minute road traffic counts and average speed data for around 10,000 sensors across England are published in the experimental dataset

Road traffic in Great Britain

The DfT daily road traffic estimates are useful as an indication of traffic change rather than actual traffic volumes. The data provided are indexed to the first week of February and the comparison is to the same day of the week. More information on the methods, quality and economic analysis for these indicators can be found in the article.

Figure 12: Road traffic across all motor vehicles has been gradually returning to pre-lockdown levels following a low point around the end of March 2020

Daily road traffic index: 100 = same traffic as the equivalent day of the week in the first week of February, 1 March 2020 to 17 August 2020, non-seasonally adjusted

Source: Department for Transport road traffic statistics: management information

Notes:

- Dips in data relate to bank holidays on Easter weekend, May Day and the late-May bank holiday.

Download this chart Figure 12: Road traffic across all motor vehicles has been gradually returning to pre-lockdown levels following a low point around the end of March 2020

Image .csv .xlsRoad traffic across all motor vehicles has been gradually returning to levels seen in the first week of February 2020 following a lockdown low point around the end of March. The latest road traffic data up to Monday 17 August show overall road traffic was around 9 percentage points lower than traffic seen on the equivalent Monday in the first week of February.

Heavy goods vehicles were first to return to early February levels of traffic in early July, followed by light commercial vehicles. However, car road traffic remains around 10 percentage points lower compared with the first week of February.

Highways England road traffic

Highways England (HE) data are available monthly up to June 2020. The data are less timely than the DfT road traffic data but include detailed road traffic for key roads serving 13 selected ports, within a 10-kilometre radius of each port location. These 13 ports were selected because of their identification as "major" ports.

Figures 13 and 14 show HE road traffic within 10 kilometers of all selected English ports. HE road traffic near Bristol, London and Southampton ports represents approximately 55% of this HE total.

We expect large vehicles (over 11.66 metres in length) such as lorries to be more closely related to the movement of goods than small vehicles (less than 5.2 metres in length). More information on the methods, quality and economic analysis for these indicators can be found in the article.

Figure 13: In June 2020, road traffic across all 13 ports returned to 90% of its level in February 2020 for large vehicles (over 11.66 metres in length)

Average large vehicle port road traffic count per sensor per 15-minute observation in England, index February 2020 = 100, seasonally adjusted, January 2019 to June 2020

Source: Highways England – Road traffic sensor data

Download this chart Figure 13: In June 2020, road traffic across all 13 ports returned to 90% of its level in February 2020 for large vehicles (over 11.66 metres in length)

Image .csv .xls

Figure 14: In June 2020, road traffic across all 13 ports remained 35% lower than February 2020 levels for small vehicles (under 5.2 metres in length)

Average small vehicle port road traffic count per sensor per 15-minute observation in England, index February 2020 = 100, seasonally adjusted, January 2019 to June 2020

Source: Highways England – Road traffic sensor data

Notes:

- Monthly average road traffic counts and speed data are available by port in the dataset, along with non-seasonally adjusted aggregate series.

Download this chart Figure 14: In June 2020, road traffic across all 13 ports remained 35% lower than February 2020 levels for small vehicles (under 5.2 metres in length)

Image .csv .xlsFigures 13 and 14 show that in April 2020, total HE road traffic on key roads serving all 13 English ports identified in the HE dataset fell by 25% for large vehicles and 71% for small vehicles when compared with February 2020 road traffic levels. This is broadly consistent with the drop in heavy vehicles and cars observed in the April 2020 DfT data shown in Figure 12.

Data for June 2020 show road traffic counts for large vehicles near major ports picked up to 90% of February 2020 levels, whereas average traffic counts across small vehicle types were 65% of the February 2020 level. Of the three ports shown here, road traffic near London port was the least affected in April 2020, recovering the strongest during May and June 2020. Whereas road traffic near Bristol port was the most affected and has also seen a relatively slow recovery.

Nôl i'r tabl cynnwys10. Shipping

These shipping indicators are based on counts of all vessels and cargo and tanker vessels. As discussed in Faster indicators of UK economic activity: shipping, we expect the shipping indicators to be related to the import and export of goods.

The time series of daily and weekly passenger visits have been temporarily suspended because of quality concerns. We are investigating and hope to reinstate these series in future releases.

Figure 15: Between 10 and 16 August, the average volume of daily ship visits remained broadly flat at 345, compared with 348 in the previous week

Daily movements in shipping visits, seasonally adjusted, UK, 1 January to 16 August 2020

Source: exactEarth

Download this chart Figure 15: Between 10 and 16 August, the average volume of daily ship visits remained broadly flat at 345, compared with 348 in the previous week

Image .csv .xls

Figure 16: Between 10 and 16 August, the volume of daily visits for cargo ships remained constant at just under 100 ships a day

Daily movements in shipping visits, seasonally adjusted, UK, 1 January to 16 August 2020

Source: exactEarth

Notes:

The number of visits for Hull are included in these data from 1 June 2020 onwards.

The seasonally adjusted and trend estimates are estimated using a modified version of the seasonal adjustment method TRAMO-SEATS. More information is available in the Coronavirus and the latest indicators for the UK economy and society methodology.

The seasonal adjustment method may be limited as this is a short time series.

Download this chart Figure 16: Between 10 and 16 August, the volume of daily visits for cargo ships remained constant at just under 100 ships a day

Image .csv .xls11. Data

Weekly shipping indicators

Dataset | Released 20 August 2020

The weekly and daily shipping indicators dataset associated with the faster indicators of UK economic activity.

Online price changes for high-demand products

Dataset | Released 20 August 2020

Weekly online price changes of selected high-demand products (HDPs).

Online job advert estimates

Dataset | Released 20 August 2020

Experimental job advert indices covering the UK job market.

Economic activity, faster indicators, UK

Dataset | Released 20 August 2020

The datasets associated with the Faster indicators of UK economic activity research output.

12. Glossary

Faster indicator

A faster indicator provides insights into economic activity using close-to-real-time big data, administrative data sources, rapid response surveys or Experimental Statistics, which represent useful economic and social concepts.

High-demand product (HDP) basket

The high-demand product (HDP) basket contains everyday essential items that were identified at the beginning of the crisis to have high consumer demand, including items from food, health and hygiene categories. The selection of these items was based on anecdotal evidence on patterns of consumer spend. The basket does not cover all items within these categories.

Company incorporations

Incorporations are when a company is added to the Companies House register of limited companies. This can also include where an existing business applies to become a limited company, where it was not one before.

Voluntary dissolutions

A voluntary dissolution is when a company applies to begin dissolution proceedings. As such, they effectively chose to be removed from the Companies House register. For a company to be eligible to voluntarily dissolve, it should not have completed any trading activity for a period of three months.

Nôl i'r tabl cynnwys13. Measuring the data

Detailed information on the data sources, quality and methodology of the different indicators included in this bulletin is available in the Coronavirus and the latest indicators of the UK economy and society methodology.

We will summarise any crucial updates to the quality or methodology in this section in the future.

Nôl i'r tabl cynnwys14. Strengths and limitations

Detailed information on the strengths and limitations of the different indicators included in this bulletin is available in the Coronavirus and the latest indicators of the UK economy and society methodology.

We will summarise any crucial updates or warnings in this section in the future.

Nôl i'r tabl cynnwys

3. Social impacts of the coronavirus on Great Britain

This section includes some headline results from Wave 22 of the Opinions and Lifestyle Survey (OPN) covering the period 12 to 16 August 2020. The full results will be published in Coronavirus and the social impacts on Great Britain on 21 August 2020.

Figure 3 shows that the proportion of adults wearing a face covering in the previous week when leaving the home was 95%. This follows an increasing trend after face coverings became mandatory on public transport in England on 15 June, in Scotland on 22 June and in Wales on 27 July. Face coverings became mandatory in shops and other enclosed spaces in Scotland on 10 July and in England on 24 July. Further breakdowns such as the situations when a face covering was worn (for example, while shopping) and by the constituent countries of Great Britain will be available in Coronavirus and the social impacts on Great Britain published on 21 August 2020.

Figure 3: The proportion of adults wearing a face covering at some point when leaving the home was at least 95% for the third consecutive week

Proportion of adults, Great Britain, 12 to 16 August 2020

Source: Office for National Statistics – Opinions and Lifestyle Survey

Notes:

See Measuring the data for full detail of the questions asked and response categories.

Base population for Work from home exclusively and Travelled to work series: adults who had a paid job, either as an employee or self-employed; or did any casual work for payment; or did any unpaid or voluntary work in the previous week.

Travelled to work series includes either travelling to work exclusively or a mixture of travelling and working from home.

Download this chart Figure 3: The proportion of adults wearing a face covering at some point when leaving the home was at least 95% for the third consecutive week

Image .csv .xls