1. Abstract

The 2008 economic slowdown highlighted the need for high quality statistics measuring the current state of the UK economy and the build-up of risk across different sectors.

Office for National Statistics (ONS), in partnership with the Bank of England, is undertaking the Enhanced Financial Accounts (EFA) Initiative, which seeks to improve the quality, coverage and granularity of the UK’s Financial Accounts. Part of this development involves the acquisition, interrogation and ultimately implementation of new data sources to meet the aims set out by users across government, industry and further afield.

This article sets out the progress and next steps for research into the application of European Market Infrastructure Regulation (EMIR) trade repository microdata as a potential data source for financial derivatives within the UK National Accounts.

In response to the 2008 global financial crisis, a number of reforms have been implemented to improve the functioning of derivative markets. Most significantly, in September 2009 G20 leaders agreed to make it mandatory for over-the-counter (OTC) derivatives transactions to be reported to trade repositories (TRs). In the EU, this was implemented by EMIR. Under EMIR, all OTC and exchange-traded derivatives transactions undertaken by EU counterparties since August 2012 (or open at that point) have had to be reported by the following business day to a TR. The responsibility for reporting lies with counterparties to these transactions that are EU legal entities – this covers entities that are clearing houses, financial counterparties and non-financial.

Nôl i'r tabl cynnwys2. Introduction

We have ambitious plans to transform our economic statistics over the coming years, informed by our Economic Statistics and Analysis Strategy and with the aim of increasing the robustness and quality of UK economic statistics. Working in partnership with the Bank of England, one important element of our transformation work is the development of enhanced financial accounts (EFA) – in particular more detailed “flow of funds” statistics – to meet evolving user needs.

Some of the main aims of the EFA initiative are to improve the quality, coverage and granularity of financial statistics and a possible avenue for these improvements is through the use of non-survey data. Non-survey data can potentially be obtained in a timelier manner and has the possibility for more granularity. Obtaining data from a single source, rather than multiple respondents to surveys also further ensures that the same definitions are being applied across a common subject, leading to higher quality.

This article provides an update on recent progress made in this area and the short-term plans for this data.

Nôl i'r tabl cynnwys3. What are financial derivatives?

The European System of Accounts 2010: ESA 2010 defines derivatives as financial assets based on, or derived from a different underlying instrument. The underlying instrument is usually another financial asset but may also be a commodity or an index. Financial derivatives are also referred to as secondary instruments and, since the hedging or offsetting of risk are frequently a motivation for their creation, they can be referred to as hedging instruments. Only those secondary instruments that have a market value, because they are tradable or can be offset on the market, are financial assets in the system of accounts and are classified as derivatives.

Derivatives are widely used in the financial and commercial sectors, both for hedging against risk and also, in the case of financial institutions that specialise in the derivatives markets, market-making and trading in derivatives for profit. Derivatives have also been introduced indirectly to the fields of retail finance and savings – examples of where derivatives are linked to financial products might include fixed-rate or capped mortgages, or equity-linked investment bonds offering investors a return linked to rises in a stock index, while offering an element of protection against future falls in the value of the index.

Usage of derivatives have expanded beyond purchasing commodity contracts to ensure future supplies of a raw material at a pre-determined price. The growth in derivatives usage has been driven in part by the greater commercial (and regulatory) emphasis on risk management in the conduct of an enterprise’s business.

The main risk determinants are foreign exchange, interest-rate, and commodity-related (including more recently power and gas). Derivatives markets are constantly innovating and new risk variants or products continually evolve.

Financial derivatives are subcategorised using the following broad-based definitions within the ESA 2010 framework:

- options

- forwards

- swaps

- forward rate agreements

- credit derivatives

- credit default swaps

Financial instruments not included in financial derivatives are:

- underlying instrument, structured debt securities (combination of debt securities and financial derivatives) where these are inseparable and the financial derivative prospective return is small

- repayable margin payments – these are classified as other deposits or loans

- secondary instruments, which are not negotiable and cannot be offset on the market

- gold swaps and securities repos are classified as other deposits or loans

- commissions to brokers or intermediaries are classed as payments for services

4. EMIR trade repository data

In response to the 2008 global financial crisis, a number of reforms have been implemented to improve the functioning of derivative markets. Most significantly, in September 2009 G20 leaders agreed to make it mandatory for counterparties to derivatives transactions to report details of such contracts to trade repositories (TR) under the European Market Infrastructure Regulation (EMIR) reporting obligation. Under EMIR, all over-the-counter and exchange-traded derivatives transactions undertaken by EU counterparties since August 2012 (or open at that point) have had to be reported by the following business day to a TR. The definition of counterparties covers primarily clearing houses, financial counterparties and non-financial counterparties that are EU legal entities (loosely speaking natural and legal persons that are based in the EU and therefore subject to EU legal obligations).

Unlike previous legislation covering financial regulation, which applied only to prudentially regulated entities such as banks or investment firms, EMIR imposes obligations on all types and sizes of entities that enter into any form of derivative contract, including those not involved in financial services. It applies indirectly to non-EU firms trading with EU firms.

Nôl i'r tabl cynnwys5. EMIR structure

The European Market Infrastructure Regulation (EMIR) trade repository (TR) data can be broadly divided into two types of reports:

- activity reports, which contain trade information on flows, for example, new trades, modifications, and valuation and cancellation updates

- state reports, which contain trade information on stock, that is, all end-of-day outstanding transactions between individual counterparties

These reports are generated each day and are available for the Bank of England to access with a one-day lag. They contain both information about the counterparty making the report and information about the trade. The reports contain more than 100 fields for each trade (not all of them are relevant to all trades), including the following:

- unique identifier for reporting trade counterparty, including the name and Legal Entity Identifier

- domicile, corporate sector and the financial or non-financial nature of counterparty

- details of the transaction, including:

- Unique Trade Identifier

- asset class (foreign exchange, interest rates, and so on) and product type (forward or future, swap, option)

- execution date, effective date, maturity date

- relevant price, for example, forward exchange rate for forwards

- for options, information also includes the type of option (call or put) and style (for example, European)

- risk mitigation, including confirmation details and collateral posted

- information about clearing

- purpose of the report (new trade, amendment, cancellation, and so on)

6. Potential application in the UK National Accounts

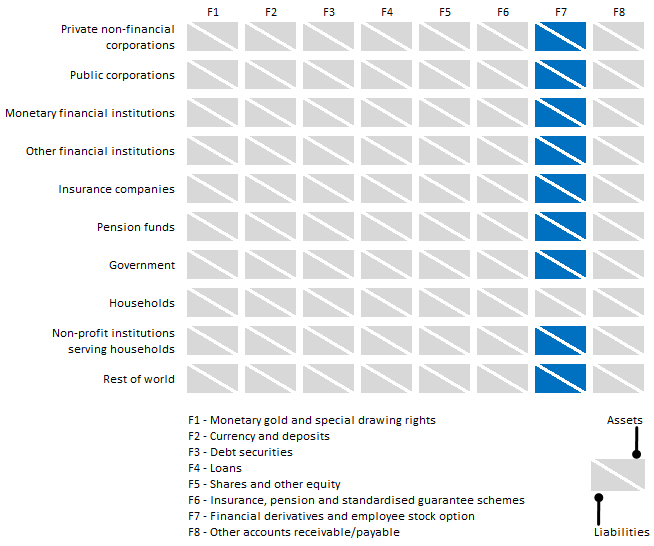

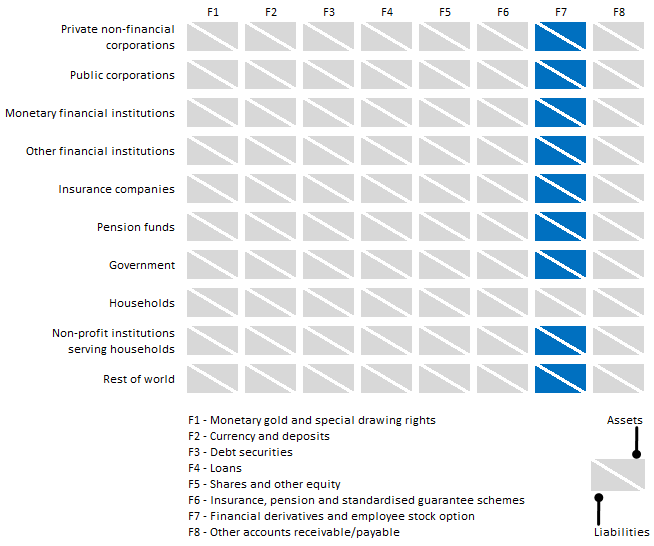

The System of National Accounts requires the valuation of derivatives as either an asset or liability based on the mark-to-market valuation or mark-to-model market valuation – one of the main variables reported under European Market Infrastructure Regulation (EMIR). Conceptually, the wide-ranging reporting of derivatives under EMIR should provide coverage of most of the European System of Accounts 2010: ESA 2010 sectors and transactional requirements. Some entities, however, fall entirely outside the scope of EMIR; these are the European Central Bank, the national central banks of the member states (including the Bank of England), other government or EU bodies “charged with intervening in the management of the public debt” and the Bank for International Settlements. Overseas organisations such as the US Federal Reserve, the Bank of Japan and the debt management offices of those two countries are also exempted. Households are also not required to report.

Figure 1: Potential European Market Infrastructure Regulation trade repository coverage by European System of Accounts 2010 sector

Source: Office for National Statistics

Download this image Figure 1: Potential European Market Infrastructure Regulation trade repository coverage by European System of Accounts 2010 sector

.PNG (15.9 kB){kind=link}

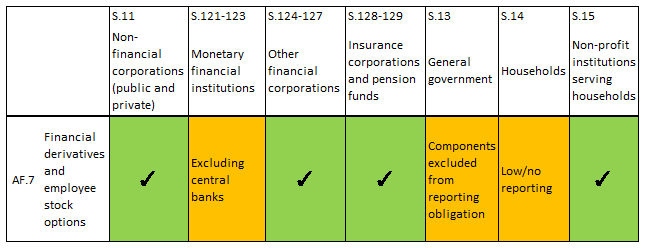

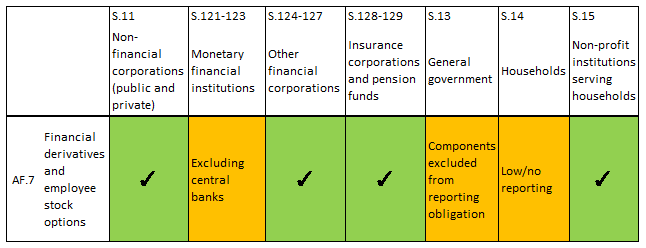

Figure 2: Summarised view of what this would cover in the UK National Accounts

Source: Office for National Statistics

Download this image Figure 2: Summarised view of what this would cover in the UK National Accounts

.PNG (32.1 kB) .ppt (252.4 kB){kind=link}

Given the comprehensive coverage, EMIR trade repository data could provide a new range of potential applications in policy analysis, supervision, research and statistical production.

Nôl i'r tabl cynnwys7. International progress and technical challenges

Although European Market Infrastructure Regulation (EMIR) legislation has the potential to provide a rich data source for the national accounts, since EMIR reporting started there have been significant data quality issues, which made analysis of the reports particularly challenging. The European Securities and Markets Authority has instigated two major improvements to the data quality, which have ensured that the data are now more complete and conform more precisely to the legal requirements. The result is that data reported since late 2015 are generally of significantly higher quality than previously.

The Financial Stability Board has made annual progress reports on the implementation and challenges of the over-the-counter (OTC) derivative market reforms; the most recent report highlighted several recurring issues have also been identified, posing challenges in supporting the underlying G20 reform objectives. These include:

- concerns over data quality

- the capacity to effectively aggregate information across trade repositories (TRs)

- the existence of barriers to reporting complete data to TRs

- barriers to authorities’ access to TR-held data

Of these challenges, data quality has been a primary concern, some of the main issues relating to data quality were:

- inadequacies in data standards both nationally and internationally

- lack of consistent and harmonised trade and product identifiers

- uneven use of Legal Entity Identifiers (used to identify the counterparties to trades)

The lack of harmonisation and data quality is being partly addressed by the Committee on Payments and Markets Infrastructures-International Organisation of Securities Commissions (CPMI-IOSCO) group, which has published technical guidance on Unique Transaction Identifiers and is due to publish technical guidance on unique product identifiers and a range of other data items that are felt to be necessary to improve the reports.

Thus by the end of 2017, it is intended that a specification and roadmap to achieve a degree of harmonisation of OTC derivatives reports will exist. Implementation will, however, have to follow this, and may take some time to achieve.

Nôl i'r tabl cynnwys8. Current status

The opportunities identified previously around data quality and consistency pose the most significant challenge for any application within the national accounts. Initial research has also found it challenging to use existing Legal Entity Identifiers to form statistical reporting units. This is particularly true within the state report files; with large variation in the quality and content of data reported to individual trade repositories. Due to the timescale to deliver necessary improvements, initial evaluation of this data source suggests that it does not provide an “off-the-shelf” data source for the national accounts.

Nôl i'r tabl cynnwys9. Next steps

After this initial “data exploration” stage, research will now focus on how the data could be used to improve existing financial derivatives statistics. The main components of this research will include:

- developing further understanding of how legal entity identifiers can be used to form statistical reporting units

- cross-validating with alternative data sources including the ONS Financial Services Survey and triennial turnover surveys

- identifying the largest contributors within the derivatives market to analyse gaps in existing data coverage

- evaluating the costs and benefits of using trade repository data compared with improvement of existing sources

- where appropriate, developing sampling and imputation methodologies

We will update you with our progress at an appropriate future date.

It is also important to us that we consider user needs when evaluating the data. We therefore seek your input on our research plans via flowoffundsdevelopment@ons.gov.uk.

Nôl i'r tabl cynnwys10. Further information

CPMI-IOSCO: Harmonisation of critical OTC derivatives data elements – second batch

Flow of Funds archived background information

31 May 2017 article – Economic Statistics Transformation Programme: Enhanced financial accounts (UK flow of funds) commercial data use

31 May 2017 article – Economic Statistics Transformation Programme: Enhanced financial accounts (UK flow of funds) improving the economic sector breakdown

27 April 2017 article – Economic Statistics Transformation Programme: Enhanced financial accounts (UK flow of funds) employee stock options

29 March 2017 article – Economic Statistics Transformation Programme: Enhanced financial accounts (UK flow of funds) Government tables for the special data dissemination standards plus (SDDS plus)

30 January 2017 article – The UK Enhanced Financial Accounts: changes to defined contribution pension fund estimates in the national accounts; part 2 – the data

16 January 2017 article – The UK Enhanced Financial Accounts: changes to defined contribution pension fund estimates in the national accounts; part 1 – the methodology

8 August 2016 article – Economic Statistics Transformation Programme: UK flow of funds experimental balance sheet statistics, 1997 to 2015

14 July 2016 article – Economic Statistics Transformation Programme: Flow of funds - the international context

14 July 2016 article – Economic Statistics Transformation Programme: Developing the enhanced financial accounts (UK Flow of Funds)

10 March 2016 article – Identifying Sectoral Interconnectedness in the UK Economy

24 February 2016 article – Improvements to the Sector and Financial Accounts

12 January 2016 article – Historical Estimates of Financial Accounts and Balance Sheets

6 November 2015 article – Comprehensive Review of the UK Financial Accounts including explanatory notes for each financial instrument covered in the article

13 July 2015 article – Introduction Progress and Future Work

Financial Statistics Expert Group Minutes can be requested from FlowOfFundsDevelopment@ons.gov.uk

Nôl i'r tabl cynnwys