1. Main points

- Falling implied rates of return contributed to lower net foreign direct investment (FDI) income, which had a negative impact on the current account balance between 2011 and 2016.

- Had the implied rate of return on FDI remained constant at its 2011 rate, the UK current account deficit would have stood at 3.0% of nominal gross domestic product (GDP) in 2018, compared with a reported 3.9%.

- FDI credits in mining and quarrying, and manufacturing industries affected the overall trend in UK FDI credits.

- Had the implied rates of return on financial and insurance liabilities remained at its 2011 rate, the value of FDI debits could have been more than double the £24.6 billion estimated in 2018, with alternative debits £26.7 billion higher.

2. FDI and implied rates of return

Foreign direct investment (FDI) refers to cross-border investments made by residents and businesses from one country into another, with the aim of establishing a lasting interest in the country receiving investment. Statistics used in this analysis are presented using the asset and liability principle, published in our Foreign direct investment involving UK companies (asset and liability): 2018 statistical bulletin. This is in line with internationally-agreed best practice and our asset and liability statistics are consistent with the UK Balance of Payments, The Pink Book.

The stock of FDI that UK residents hold abroad is UK FDI assets, and the income generated on those assets is FDI credits. UK FDI liabilities are the stock of FDI investment held in the UK by non-resident companies, and FDI debits is the income generated on those liabilities.

Implied rates of return indicate how much income is generated per pound of investment. We calculate rates of return on UK FDI assets as the ratio of FDI credits to FDI assets in the same year. Likewise, we calculate rates of return on UK FDI liabilities as the ratio of FDI debits to FDI liabilities in the same year. Further information on the recent trends in implied rates of return for UK FDI can be found in our UK foreign direct investment, trends and analysis: (implied rates of return) February 2020 article.

This article explores the impact of FDI on the UK current account, which feeds into the UK’s Balance of Payments. The UK current account measures the economy’s international transactions with the rest of the world, comprising net trade (exports less imports), primary income and secondary income. Net income (or earnings) from FDI, which is the value of credits less debits, is a sub-component of primary income. Any changes in FDI credits or debits can reflect changes in assets or liabilities respectively, changes to the profitability of that investment (implied rate of return), or a combination of both. Further information on the contribution of net FDI earnings on the UK current account balance can be found in our Foreign direct investment involving UK companies (asset and liability): 2018 statistical bulletin.

Our previous analysis from January 2017, July 2017 and January 2018 identified a downward trend in FDI credits and debits since 2011, while the values of FDI assets and liabilities continued to increase. This indicates falling implied rates of return on those direct investments over that period. Our our article published in February 2020 found that the implied rates of return on FDI assets increased considerably in 2017 from 2016, with a further increase between 2017 and 2018. The value of FDI debits increased in 2018 from 2017 at a slightly faster rate than that of FDI credits. This made net FDI income lower in 2018 than 2017, yet still added positively to the current account balance.

This article joins all of our previous analysis together to look at how changes in implied rates of return on FDI may have affected the current account balance. We calculate alternative scenarios in this analysis (previously referred to as “counterfactuals”) to separate the impact of changes in rates of return and changes to FDI stocks on FDI income. These show what the value of FDI income would have been if the implied rates of return had remained at the same rate since 2011, when rates of return were at their most recent peak. This means that any changes in alternative FDI earnings are only the result of movements in the stock of FDI, that is assets and liabilities.

Nôl i'r tabl cynnwys3. FDI and the UK current account

Net foreign direct investment (FDI) earnings, that is the value of FDI credits less FDI debits, has been one of the main contributors to the fall in the UK current account balance since 2011. Falling implied rates of return for UK FDI notably contributed to most of the change in net FDI income between 2011 and 2018. Figure 1 combines this information with the other components for the current account. It reproduces the chart using published current account components and adds the difference to net FDI income had implied rates of return remained at 2011 rates to 2018. The alternative current account balance assumes that all other components of the current account do not change as a result of alternative net FDI income.

Figure 1: Falling net FDI income was the main contributor to widening the UK current account deficit between 2011 and 2016

UK current account balance and its components, 2010 to 2018

Source: Office for National Statistics - Foreign direct investment involving UK companies (asset and liability) and UK Balance of Payments

Notes:

- The "difference from alternative net FDI income" shows the additional value of net FDI earnings, had implied rates of return remained at 2011 rates.

- The sum of "FDI income (published)" and the "difference from alternative net FDI income" gives the value of alternative FDI income.

- In line with the UK National Accounts Revisions Policy, revised estimates presented for 2017 will be incorporated into UK Balance of Payments in September 2020.

- The sum of components will not necessarily sum to the current account balance because of rounding.

Download this chart Figure 1: Falling net FDI income was the main contributor to widening the UK current account deficit between 2011 and 2016

Image .csv .xlsThe alternative scenarios – assuming the implied rate of return had remained at the same rate since 2011 – estimate that net FDI income would have been higher in every year from 2012 to 2018. The biggest difference would have been in 2016, when published net FDI income was £1.0 billion whereas alternative net FDI income would have been £45.8 billion. This is also the year where there was the greatest difference between the published and alternative current account balances, negative £104.0 billion compared with the alternative balance of negative £59.2 billion.

There would be a much smaller increase in the value of net FDI income under the alternative scenario in 2017. Published net earnings were £30.4 billion with the alternative scenario adding £12.8 billion. This reflects the extent to which the value of published credits increased considerably in 2017 from 2016, which brought the implied rate of return on assets closer to its 2011 rate. There was then a fall in the value of published net FDI income in 2018 from 2017 as FDI debits increased by more than credits. The alternative scenario could have added £18.4 billion to the value of FDI income had implied rates of return remained at 2011 rates.

The UK current account balance remains negative under the alternative scenario. However, the lowest current account balance under the alternative scenario would have been in 2014, at negative £70.0 billion, rather than in 2016 (negative £104.0 billion). Under the alternative scenario, the current account balance followed a flatter trend between 2013 and 2018 compared with the more marked downward trend using published statistics. By 2018, the current account balance accounted for negative 3.9% of nominal gross domestic product (GDP) in 2018, whereas this could have been 0.9 percentage points higher at negative 3.0% using the alternative scenario.

Nôl i'r tabl cynnwys4. Implied rates of return on FDI assets

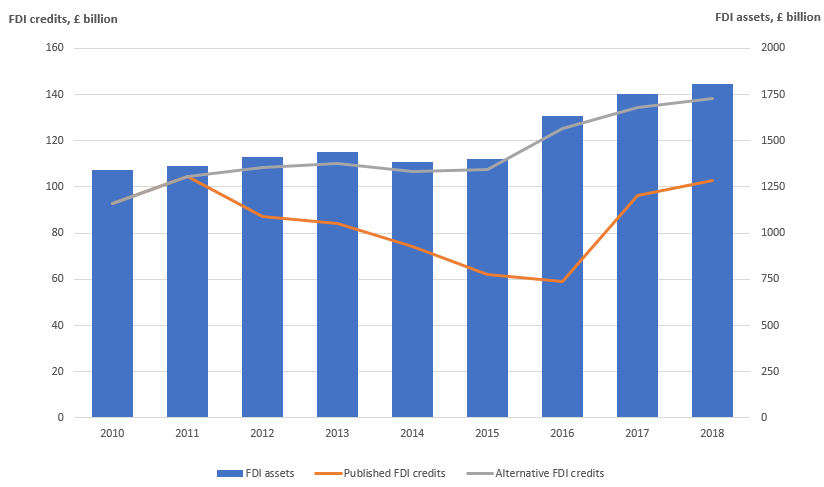

The value of foreign direct investment (FDI) assets followed a gradual upward trend between 2010 and 2018. At the same time, the value of FDI credits fell in consecutive years between 2011 and 2016. As a result, the implied rate of return on FDI assets of 7.7% in 2011 fell to 3.6% by 2016. The bigger increases in the value of FDI credits relative to assets in 2017 and 2018 saw the implied rates of return increase in both years, to 5.5% and 5.7% respectively. Figure 2 shows the value of reported and alternative FDI credits with the published value of FDI assets.

Figure 2: Rates of return on FDI assets caused most of the rise in the value of FDI credits between 2016 and 2017

Foreign direct investment assets, and published and alternative foreign direct investment credits, 2010 to 2018

Source: Office for National Statistics - Foreign direct investment involving UK companies (asset and liability)

Download this image Figure 2: Rates of return on FDI assets caused most of the rise in the value of FDI credits between 2016 and 2017

.PNG (27.7 kB) .xlsx (22.8 kB){kind=link}

Since the implied rate of return on assets is fixed at 7.7% – the 2011 rate – under the alternative scenario, the value of alternative credits matches changes in the value of FDI assets. The biggest increase in the value of alternative FDI credits would have been between 2015 and 2016, where FDI assets increased by £229.4 billion, leading to alternative credits increasing by £17.6 billion; both 16.3% higher in 2016 than 2015. In 2016, the value of alternative FDI credits were £66.3 billion higher than published FDI credits, therefore reflecting changes in the implied rate of return since 2011.

Published and alternative FDI credits increased between 2017 and 2018, by £6.6 billion and £4.0 billion respectively, because of a £51.6 billion rise in FDI assets in 2018. A rise in the implied rate of return on FDI assets led to an additional increase of £2.6 billion in FDI credits in 2018. Implied rates of return on assets accounted for £27.9 billion of the £37.1 billion (or 75.2%) increase in reported FDI credits between 2016 and 2017, whereas increasing FDI assets would have only led to a £9.2 billion rise in FDI credits in 2017. Rising rates of return, coupled with higher asset values, increased the published returns from FDI assets for the first time in 2017 since 2011.

Implied rates of return from mining and quarrying, and manufacturing industries have been important for rates in 2017 and 2018

While the overall implied rate of return on UK FDI assets fell between 2011 and 2016, there were differences in those trends in returns by industry. Industries are defined using the UK Standard Industrial Classification of Economic Activities 2007: SIC 2007 and further details of how we group industries can be found in Section 6.

Our previous analysis found that falling implied rates of return in mining and quarrying industries, contributed greatly to the fall in FDI credits since 2011. This can be seen in Figure 3, which presents the published and alternative FDI credit values across seven industry groupings. It shows that the impact of falling implied rates of return since 2011 on FDI credits was largest for mining and quarrying, information and communication, and professional and support industries.

The value of alternative credits in mining and quarrying is constant between 2011 and 2018, indicating that the value of mining and quarrying assets has also remained constant. This is in contrast with published mining and quarrying credits, which decreased year-on-year between 2011 and 2016, becoming negative in that last year. Since then, there has been a notable increase in the value of FDI credits among mining and quarrying companies, which has contributed to the increase in the UK implied rate of return on all FDI assets.

Figure 3: Implied rates of return have changed the most for mining and quarrying between 2011 and 2018 relative to FDI asset values in those industries

Published and alternative foreign direct investment credits by industry, 2011 to 2018

Source: Office for National Statistics - Foreign direct investment involving UK companies (asset and liability)

Notes:

- Data on banks, bank holding companies, property and public corporations are removed from the analysis in order to focus upon the main industrial groupings.

- M&Q is mining and quarrying; M is manufacturing; WT&A is wholesale, transport and accommodation; I&C is information and communication; F&I is financial and insurance; P&S is professional and support; and O is other industries.

Download this chart Figure 3: Implied rates of return have changed the most for mining and quarrying between 2011 and 2018 relative to FDI asset values in those industries

Image .csv .xlsInformation and communication is another industry grouping where the value of FDI assets has been relatively stable, yet the published value of credits is below the alternative scenario. While there has been an increase in the value of published FDI credits among these companies, it has been less pronounced than for mining and quarrying companies. Published FDI credits in both industries were lower in 2018 than they were in 2011. Despite large differences between the published and alternative FDI credits in professional and support industries throughout the period, increasing values of FDI assets in those industries meant that both published and alternative credits in 2018, at £15.7 billion and £25.2 billion respectively, were above their 2011 value (£12.4 billion).

Manufacturing industries had the biggest increase in the value of published FDI credits in 2017 compared with 2016. These went from £19.1 billion in 2016 to £36.0 billion in 2017, an increase of £16.9 billion (or 88.5%). This increase was supported by increasing values of FDI assets in those industries, with the alternative credits going from £28.8 billion in 2016 to £32.7 billion in 2017, an increase of £3.9 billion (or 13.5%). The value of FDI credits in these industries resembles the alternative credits to some extent and we also found that the value of published FDI credits for these industries in 2018 (£33.4 billion) was close to the alternative value (£34.3 billion), indicating that the implied rate of return among FDI manufacturers in 2018 (7.7%) was similar to that in 2011 (7.9%).

There were also two industrial groupings where the value of published credits closely follows the alternative credits – wholesale, transport and accommodation, and financial and insurance industries. This indicates that implied rates of return for both groupings remained largely constant between 2011 and 2018 so that any changes in the value of credits were more a reflection of changes in the underlying value of FDI assets.

Therefore, the overall trend in the value of UK FDI credits – and by extension, implied rates of return on FDI assets – was mostly affected by mining and quarrying industries, yet the subsequent increase in credit values in 2017 and 2018 was from increasing rates of return among mining and quarrying companies as well as higher FDI asset values in manufacturing industries.

Nôl i'r tabl cynnwys5. Implied rates of return on FDI liabilities

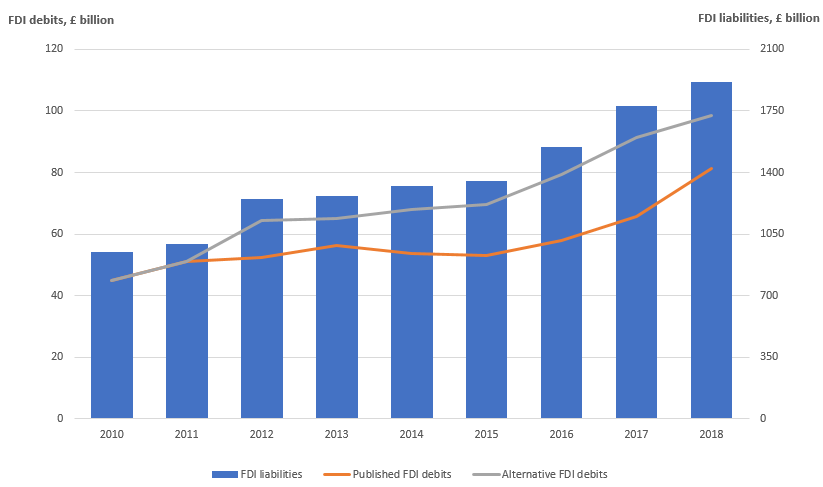

The value of foreign direct investment (FDI) liabilities has followed an upward trend between 2010 and 2018. These values have increased at a faster rate than that of FDI assets, giving the UK a negative net international FDI position in 2017 and 2018. The trend in FDI debits has also followed the trend in FDI liabilities much closer than credits followed asset values between 2011 and 2018. This is indicated by the similar upward trend in the value of alternative FDI debits over that period (Figure 4). While implied rates of return on FDI liabilities have fallen, this has been to a lesser extent than on FDI assets. Nevertheless, our analysis still suggests that FDI debits were £17.4 billion (21.4%) lower in 2018 than they could have been had the implied rate of return remained at its 2011 rate. This was a slightly smaller difference than the £25.7 billion (39.1%) difference in 2017.

Figure 4: Reported FDI debits in 2018 grew at a faster rate than alternative values because of a rise in the rate of return on liabilities

Foreign direct investment liabilities, and published and alternative foreign direct investment debits, 2010 to 2018

Source: Office for National Statistics - Foreign direct investment involving UK companies (asset and liability)

Download this image Figure 4: Reported FDI debits in 2018 grew at a faster rate than alternative values because of a rise in the rate of return on liabilities

.PNG (24.9 kB) .xlsx (21.0 kB){kind=link}

Financial and insurance debits could have been much higher in 2018 had implied rates of return been at their 2011 rate

The increase in the value of FDI debits has been evenly spread across most industrial groupings. However, the alternative scenario still highlights differences in implied rates of return (Figure 5). This is most apparent among financial and insurance companies, where the value of FDI liabilities continued to increase steadily between 2011 and 2018, yet the debits on those direct investments have only followed a similar upward trend since 2014. This indicates that, had the implied rates of return on financial and insurance liabilities remained at 2011 rates, the value of FDI debits could have been more than double the £24.6 billion estimated in 2018, with alternative credits at £51.3 billion, or £26.7 billion higher. These higher alternative debits from financial and insurance industries offset the increase in the value of alternative FDI credits in net FDI income and the current account.

Figure 5: Implied rates of return on liabilities with financial and insurance, and mining and quarrying industries have changed the most compared with 2011 rates

Published and alternative foreign direct investment debits by industry, 2011 to 2018

Source: Office for National Statistics - Foreign direct investment involving UK companies (asset and liability)

Notes:

- Data on banks, bank holding companies, property and public corporations are removed from the analysis in order to focus upon the main industrial groupings.

- M&Q is mining and quarrying; M is manufacturing; WT&A is wholesale, transport and accommodation; I&C is information and communication; F&I is financial and insurance; P&S is professional and support; and O is other industries.

Download this chart Figure 5: Implied rates of return on liabilities with financial and insurance, and mining and quarrying industries have changed the most compared with 2011 rates

Image .csv .xlsMining and quarrying industries is another industrial grouping where the value of FDI debits could have been higher had the implied rate of return on liabilities remained at the 2011 rate. Unlike for the financial and insurance industries, the value of FDI liabilities among mining and quarrying companies steadily increased between 2011 and 2014, yet debits declined at the same time. The values of FDI liabilities have remained stable among mining and quarrying companies since 2015, indicating a smaller difference between published and alternative debits than for financial and insurance industries. While increasing rates of return on mining and quarrying liabilities narrowed the gap between published and alternative debits, the value of FDI debits could have been £5.6 billion higher at £8.7 billion in 2018 had the implied rate of return remained at the 2011 rate.

The published and alternative debit values were similar for four of the seven industry groupings. The greatest similarities between 2011 and 2018 were for wholesale, transport and accommodation, and information and communication industries. For both of these, the value of published debits was higher than alternative debits in 2018, showing that implied rates of return were higher than their respective 2011 rates.

Therefore, the overall trend in the value of UK FDI debits – and by extension, implied rates of return on FDI liabilities – was mostly affected by financial and insurance industries. The faster growth in debits than credits in 2018 contributed to a fall in net FDI income and the UK current account balance.

Nôl i'r tabl cynnwys6. Details of SIC 2007 industries for each FDI industrial grouping used

| Industry grouping | Section(s) within SIC07 |

|---|---|

| Mining and Quarrying | B – Mining and quarrying |

| Manufacturing | C – Manufacturing |

| Wholesale, Transportation and Accommodation | G – Wholesale and retail trade; repair of motor vehicles and motorcycles |

| H – Transportation and storage | |

| I – Accommodation and food service activities | |

| Information and Communication | J – Information and communication |

| Financial and Insurance | K – Financial and insurance activities |

| Professional and Support | M – Professional, scientific and technical activities |

| N – Administrative and support service activities | |

| Other | A – Agriculture, forestry and fishing |

| D – Electricity, gas, steam and air conditioning supply | |

| E – Water supply, sewerage, waste management and remediation activities | |

| F – Construction | |

| L – Real estate activities | |

| O – Public administration and defence; compulsory social security | |

| P – Education | |

| Q – Human health and social work activities | |

| R – Arts, entertainment and recreation | |

| S – Other service activities | |

| T – Activities of households as employers; undifferentiated goods- and services-producing activities of households for own use | |

| U – Activities of extra-territorial organisations and bodies |

Download this table Table 1: Details of Standard Industrial Classification (SIC 2007) industries for each FDI industrial grouping used

.xls .csv7. Acknowledgements

Authors: Laura Garcia Blasco and Andrew Jowett, Office for National Statistics

The authors would like to acknowledge the contributions of Freddy Farias Arias, Lee Mallett, and Aphra Smith.

Nôl i'r tabl cynnwys