Cynnwys

- Main points

- Things you need to know about this release

- Private rental prices see steady growth in Great Britain

- England and Wales see growth in private rental prices, while Scotland remains zero

- Growth in private rental prices in London continues to slow

- Links to related statistics

- What’s changed in this release?

- Quality and methodology

1. Main points

Private rental prices paid by tenants in Great Britain rose by 1.8% in the 12 months to April 2017; this is down from 2.0% in March 2017.

In England, private rental prices grew by 2.0%, Wales saw growth of 0.7% while Scotland saw zero growth in the 12 months to April 2017.

London private rental prices grew by 1.4% in the 12 months to April 2017, 0.4 percentage points below the Great Britain 12-month growth rate.

2. Things you need to know about this release

The Index of Private Housing Rental Prices (IPHRP) measures the change in price of renting residential property from private landlords. The index is published as a series of price indices covering Great Britain, its constituent countries and the English regions. All data presented are non-seasonally adjusted.

IPHRP measures the change in price tenants face when renting residential property from private landlords, thereby allowing a comparison between the prices tenants are charged in the current month as opposed to the same month in the previous year. The index does not measure the change in newly advertised rental prices only, but reflects price changes for all private rental properties.

The IPHRP is constructed using administrative data. That is, the index makes use of data that are already collected for other purposes in order to estimate rental prices. The sources of private rental prices are Valuation Office Agency (VOA), Scottish government (SG) and Welsh government (WG). All three organisations deploy rental officers to collect the price paid for privately rented properties. The sources of expenditure weights are the Department for Communities and Local Government (DCLG), Scottish government, Welsh government and the VOA.

IPHRP is released as an Experimental Statistic. While the methodology for IPHRP is final, Northern Ireland is currently excluded from the price index. We are working with Northern Ireland Housing Executive to secure private rental data for Northern Ireland. Once the coverage of IPHRP has been improved to that of the UK, the IPHRP will be assessed against the Code of Practice for Official Statistics to achieve National Statistics status.

Nôl i'r tabl cynnwys3. Private rental prices see steady growth in Great Britain

Between January 2011 and April 2017, private rental prices in Great Britain increased by 14.6%, strongly driven by the growth in private rental prices within London. When London is excluded, private rental prices increased by 10.5% over the same period.

Figure 1: Index of Private Housing Rental Prices indices: Great Britain, January 2011 to April 2017

Source: Office for National Statistics

Download this chart Figure 1: Index of Private Housing Rental Prices indices: Great Britain, January 2011 to April 2017

Image .csv .xlsGrowth in private rental prices paid by tenants in Great Britain has seen signs of a slowdown since the end of 2015, increasing by 1.8% in the 12 months to April 2017. For example, a property that was rented for £500 a month in April 2016, which saw its rent increase by the average rate in Great Britain, would be rented for £509 in April 2017. This slowdown in the growth in private rental prices in Great Britain is mainly driven by a slowdown in London over the same period.

The 12-month growth rate of private rental prices paid by tenants in Great Britain fell slightly in April 2017 to 1.8%, from 2.0% in March 2017. Rental prices for Great Britain excluding London increased by 2.1% in the 12 months to April 2017, down from 2.2% in March 2017 (Figure 2). The growth rate for London (1.4%) in the 12 months to April is 0.4 percentage points below that of Great Britain.

The Royal Institute of Chartered Surveyors (RICS) March 2017 Residential Market Survey reported a continued rise in tenant demand, although demand growth remains more modest when compared to the same period a year ago. The indicator for new landlord instructions remained in negative territory for a sixth consecutive month.

The Association of Residential Letting Agents (ARLA) Private Rented Sector Report for March 2017 noted that while the supply of rental stock remained the same as February, demand for rental properties rose marginally in March.

Figure 2: Index of Private Housing Rental Prices percentage change over 12 months: Great Britain, January 2012 to April 2017

12-month percentage change

Source: Office for National Statistics

Download this chart Figure 2: Index of Private Housing Rental Prices percentage change over 12 months: Great Britain, January 2012 to April 2017

Image .csv .xls4. England and Wales see growth in private rental prices, while Scotland remains zero

All the countries that constitute Great Britain have experienced rises in their private rental prices since 2011 (Figure 3). Since January 2011, rental prices in England have increased more than those in Wales and Scotland.

Figure 3: Index of Private Housing Rental Prices indices for Great Britain and its constituent countries, January 2011 to April 2017

Source: Office for National Statistics

Download this chart Figure 3: Index of Private Housing Rental Prices indices for Great Britain and its constituent countries, January 2011 to April 2017

Image .csv .xlsThe annual rate of change for Wales (0.7%) in April 2017 continues to be below that of England (2.0%) and Great Britain (1.8%). The annual rate of change for Wales has not reached 1.0% since March 2012 (Figure 4).

Rental growth in Scotland was zero in the 12 months to April 2017 and has remained around zero since August 2016. This weaker growth may be due to stronger supply and weaker demand in Scotland as reported by the Association of Residential Letting Agents (ARLA).

Figure 4: Index of Private Housing Rental Prices percentage change over 12 months for Great Britain and its constituent countries, January 2012 to April 2017

12-month percentage change

Source: Office for National Statistics

Download this chart Figure 4: Index of Private Housing Rental Prices percentage change over 12 months for Great Britain and its constituent countries, January 2012 to April 2017

Image .csv .xls5. Growth in private rental prices in London continues to slow

Growth in private rental prices in London continues to slow, increasing by 1.4% in the 12 months to April, down from 1.6% in March 2017. New build constructions, buy to let investors and accidental landlords have led to high levels of stock available to rent in the capital according to Savills. This view is supported by Countrywide, who report that rental stock was growing at a faster rate than demand in London, pushing down rents. The Royal Institute of Chartered Surveyors (RICS) March 2017 Residential Market Survey notes that in London, respondents anticipate rents may continue to soften over the near term, and hold broadly flat when looking at the next 12 months as a whole.

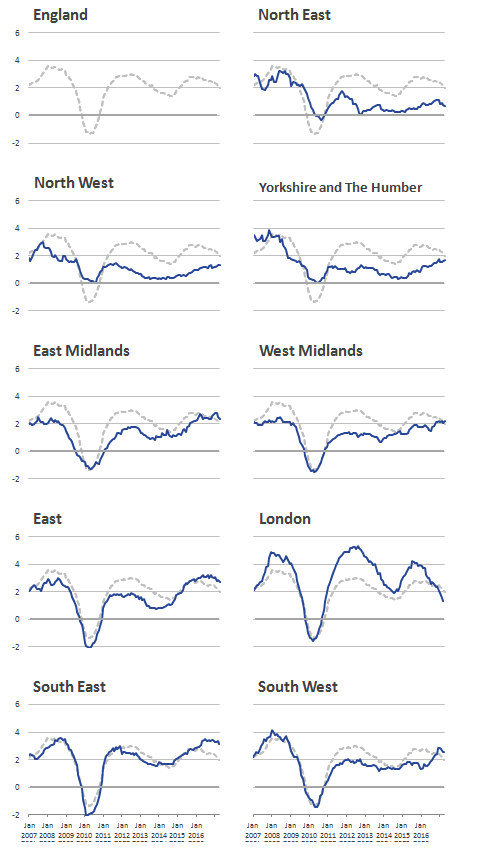

Private rental prices in the south and east of England continue to rise at a faster pace than those in the north (Figure 5). The largest annual rental price increases were in the South East (3.1%), down from 3.4% in March 2017.

This was followed by the East of England (2.7%), down from 2.8% in March 2017, the South West (2.5%), unchanged from March 2017, and the East Midlands (2.3%), down from 2.5% in March 2017.

The lowest annual rental price increases were in the North East (0.7%), unchanged from March 2017, the North West (1.3%), unchanged from March 2017, London (1.4%), down from 1.6% in March 2017, and Yorkshire and The Humber (1.7%), up from 1.6% in March 2017.

Figure 5: Index of Private Housing Rental Prices percentage change over the 12 months to April 2017, by English region

12-month percentage change

Source: Office for National Statistics

Download this chart Figure 5: Index of Private Housing Rental Prices percentage change over the 12 months to April 2017, by English region

Image .csv .xlsFigure 6 shows the historical 12-month percentage growth rate in the rental prices of each of the English regions.

Figure 6: Index of Private Housing Rental Prices percentage change over 12 months by English region, January 2007 to April 2017

12-month percentage change

Source: Office for National Statistics

Notes:

- The dotted grey line shows the average England 12 month percentage change.

Download this image Figure 6: Index of Private Housing Rental Prices percentage change over 12 months by English region, January 2007 to April 2017

.PNG (38.0 kB) .xls (59.9 kB){kind=link}

7. What’s changed in this release?

The Index of Private Housing Rental Prices (IPHRP) is now published on the second or third Tuesday of each month to bring it in line with other prices-related releases grouped under new “theme” days. This will increase the coherence of our data releases; for more information see Changes to publication schedule for economic statistics.

Tables 3 and 4 have now been removed from the IPHRP dataset as these data are now included in the quarterly article Comparing measures of private rental growth in the UK.

Nôl i'r tabl cynnwys8. Quality and methodology

Details of the methodology used to calculate the Index of Private Housing Rental Prices (IPHRP) can be found in the July 2013 IPHRP article but this article requires some updating. In March 2015, methodological improvements were implemented to improve the matching of properties over time; this ensures that we are comparing “like with like”. These methodological improvements were presented in the January 2015 article.

In September 2015, we published an evaluation of our rental price indices against the growth in average private rental prices published by Valuation Office Agency (VOA); please see the article Explaining private rental growth. Comparisons of IPHRP against other private rent measures can be found in the article published alongside this release.

The IPHRP Quality and Methodology Information document contains important information on:

the strengths and limitations of the data and how it compares with related data

uses and users of the data

how the output was created

the quality of the output including the accuracy of the data