Cynnwys

- Main points

- Things you need to know about this release

- Interactive map

- Public sector net fiscal balance

- Public sector revenue

- Public sector expenditure

- What’s changed in this release?

- Public value of statistics on public finances in a devolved UK

- Links to related statistics

- Future developments

- Quality and methodology

1. Main points

London, the South East and the East of England all had net fiscal surpluses in the financial year ending (FYE) 2018, with all other countries and regions of the UK having net fiscal deficits.

London had the highest net fiscal surplus per head at £3,905 and Northern Ireland had the highest net fiscal deficit per head at £4,939, in FYE 2018.

London raised the most revenue per head in FYE 2018, at £17,090, with Wales and the North East raising the least revenue per head at £8,691 and £8,938 respectively.

Northern Ireland and Scotland incurred the highest expenditure per head, in FYE 2018, at £14,195 and £13,682 respectively, with the lowest expenditure per head attributed to the East of England and the East Midlands at £10,970 and £11,146 per head respectively.

2. Things you need to know about this release

What do these statistics tell me?

The aim of the country and regional public sector finances statistics is to provide users with information on what public sector expenditure has occurred, for the benefit of residents or enterprises, in each country or region of the UK and what public sector revenues have been raised in each country or region, as well as the balance between them.

“Public sector” is used in this publication to refer to central government departments and bodies (such as the Department for Work and Pensions), local authorities and other local government bodies (such as police authorities), and public sector-controlled corporations (such as Scottish Water).

Public sector revenue is the total current receipts (mainly taxes, but also social contributions, interest, dividends, gross operating surplus and transfers) received by central government and local government bodies as well as public corporations. It is recorded on an accrued basis, following the national accounts rules.

Public sector expenditure is the total capital and current expenditure (mainly wages and salaries, goods and services, and expenditure on fixed capital, but also subsidies, social benefits and other transfers) of central government and local government bodies as well as public corporations. It is recorded on an accrued basis, following the national accounts rules.

Net fiscal balance is the gap between total spending (current expenditure plus net capital expenditure) and revenue raised (current receipts), which at the UK level is equivalent to public sector net borrowing. A negative net fiscal balance figure represents a surplus, meaning that a country or region is receiving in revenue more than is being spent for the benefit of residents or enterprises in that country or region. A positive net fiscal balance represents a deficit, meaning a country or region is attracting more expenditure for the benefit of its residents or enterprises than it is receiving in revenue.

The country and regional public sector finances statistics are neither reflective of the annual devolved budget settlements nor are these data used when calculating devolved budget settlements. They may not be an accurate representation of public finances should fiscal powers be fully devolved among UK countries and regions. Furthermore, they do not provide information on the spending and revenue of individual country or regional bodies such as the Greater London Authority.

The geographic boundaries used for countries and regions in the UK follows the Nomenclature of Units for Territorial Statistics: NUTS1 definitions. Country and regional public sector finances are Experimental Statistics, but at the UK level they are consistent with the February 2019 public sector finances (PSF) bulletin, which is badged as National Statistics.

What does it mean that these are Experimental Statistics?

Experimental Statistics are statistics that are within their development phase and are published to involve potential users at an early stage in building a high-quality set of statistics that meet user needs.

This is the third time that we have published country and regional statistics on public sector revenue and expenditure. Since the first publication in May 2017, we have developed the statistics further. It should be emphasised that an Experimental Statistics label does not mean that the statistics are of low quality, it only signifies that the statistics are novel and still being developed.

Alongside this publication there is a detailed methodology guide, which sets out exactly how each revenue and expenditure item has been apportioned to countries and regions. Users should refer to this methodological information when judging whether their particular use of the statistics is appropriate.

Why are there two measures of net fiscal balance shown?

This bulletin allocates North Sea oil and gas revenues (mainly received from the Petroleum Revenue Tax and Corporation Tax) using two distinct methodologies. The first approach is to allocate the revenue on a geographic basis according to where the oilfields that give rise to the revenue are situated. The second approach to apportioning North Sea oil and gas revenue is to allocate it to all countries and regions based on their populations.

More information on the methodology used to apportion North Sea oil and gas revenue, and all other revenues and expenditures, can be found in the methodology guide.

When will the next statistical release be published?

This is the third country and regional public sector finances publication, following the first release that we published in May 2017. We aim to publish the fourth release, relating to statistics for the financial year ending (FYE) 2019, in winter 2019 to 2020 to reduce the lag for when data are available and to publish at similar times to other related statistics, such as HM Revenue and Customs Disaggregated Tax Receipts.

To accommodate the move of publication dates it has been necessary to minimise updates to this publication and accompanying dataset. We have not updated the indicator datasets used to apportion revenue and certain expenditure aspects to regions and have rationalised some content in this bulletin. This means proportions for FYE 2018 have not changed from FYE 2017; indicator data will be updated in the next release.

If you would like to be kept up-to-date with next year’s release dates, please send your contact details to psa@ons.gov.uk and we will inform you of any changes.

Nôl i'r tabl cynnwys3. Interactive map

Figure 1: Interactive map of country and regional public sector finances main aggregates

Embed code

4. Public sector net fiscal balance

Most of the 12 Nomenclature of Units for Territorial Statistics: NUTS1 regions saw an improvement in their net fiscal balances between financial year ending (FYE) 2017 and FYE 2018, meaning a decreased deficit or an increased surplus. However, this change was smaller than that which occurred between FYE 2016 and FYE 2017. The largest change occurred in the South East, which saw an increase in its net fiscal surplus of £1.3 billion.

The change in net fiscal balances between FYE 2017 and FYE 2018 was largely driven by an increase in total revenue in NUTS1 regions. Figure 2 and Figure 3 show the net fiscal balances calculated on a geographic and population basis for the NUTS1 regions and the UK. The largest net fiscal surplus was in London at £34.3 billion on a geographic basis; this was similar on a population basis. The largest net fiscal deficit was in the North West – £20.8 billion on a geographic basis and similar on a population basis.

Figure 2: The largest net fiscal surplus was in London with £34.3 billion in financial year ending 2018

Net fiscal balance in financial year ending 2018, by NUTS1 countries and regions

Source: Office for National Statistics

Notes:

- North sea oil and gas revenues included on a geographic share and a population share.

Download this chart Figure 2: The largest net fiscal surplus was in London with £34.3 billion in financial year ending 2018

Image .csv .xlsTable 1 shows the net fiscal balance of each country and region in £ millions and as a percentage of gross domestic product (GDP). The largest surplus increase was in the South East, which saw a rise from £19.2 billion in FYE 2017 to £20.4 billion in 2018. The largest deficit increase was in the North West, which saw a rise from £19.6 billion in FYE 2017 to £20.8 billion in FYE 2018.

| Net Fiscal Balance¹ (£ million) | |||||||

|---|---|---|---|---|---|---|---|

| North Sea revenue geographic share | % of GDP² | ||||||

| Country/Region | 2015/16 | 2016/17 | 2017/18 | 2015/16 | 2016/17 | 2017/18 | |

| North East | 10,517 | 9,778 | 9,675 | 0.55% | 0.49% | 0.47% | |

| North West | 21,894 | 19,604 | 20,860 | 1.14% | 0.99% | 1.01% | |

| Yorkshire and the Humber | 14,150 | 12,170 | 11,752 | 0.74% | 0.61% | 0.57% | |

| East Midlands | 7,718 | 6,270 | 5,983 | 0.40% | 0.32% | 0.29% | |

| West Midlands | 14,521 | 13,565 | 13,243 | 0.76% | 0.68% | 0.64% | |

| East of England | -2,446 | -5,620 | -5,930 | -0.13% | -0.28% | -0.29% | |

| London | -25,625 | -33,599 | -34,302 | -1.34% | -1.69% | -1.66% | |

| South East | -14,796 | -19,165 | -20,421 | -0.77% | -0.96% | -0.99% | |

| South West | 6,916 | 5,087 | 4,796 | 0.36% | 0.26% | 0.23% | |

| England | 32,849 | 8,090 | 5,656 | 1.72% | 0.41% | 0.27% | |

| Wales | 13,969 | 13,365 | 13,695 | 0.73% | 0.67% | 0.66% | |

| Scotland | 15,507 | 14,128 | 13,265 | 0.81% | 0.71% | 0.64% | |

| Northern Ireland | 9,514 | 9,304 | 9,208 | 0.50% | 0.47% | 0.45% | |

| United Kingdom³ | 71,840 | 44,887 | 41,823 | 3.76% | 2.26% | 2.02% | |

| North Sea revenue population share | % of GDP | ||||||

| Country/Region | 2015/16 | 2016/17 | 2017/18 | 2015/16 | 2016/17 | 2017/18 | |

| North East | 10,508 | 9,750 | 9,608 | 0.55% | 0.49% | 0.46% | |

| North West | 21,892 | 19,579 | 20,705 | 1.14% | 0.98% | 1.00% | |

| Yorkshire and the Humber | 14,094 | 12,067 | 11,586 | 0.74% | 0.61% | 0.56% | |

| East Midlands | 7,706 | 6,238 | 5,873 | 0.40% | 0.31% | 0.28% | |

| West Midlands | 14,529 | 13,562 | 13,128 | 0.76% | 0.68% | 0.64% | |

| East of England | -2,455 | -5,649 | -6,066 | -0.13% | -0.28% | -0.29% | |

| London | -25,614 | -33,604 | -34,475 | -1.34% | -1.69% | -1.67% | |

| South East | -14,786 | -19,175 | -20,602 | -0.77% | -0.96% | -1.00% | |

| South West | 6,909 | 5,068 | 4,678 | 0.36% | 0.25% | 0.23% | |

| England | 32,783 | 7,836 | 4,435 | 1.71% | 0.39% | 0.21% | |

| Wales | 13,974 | 13,364 | 13,634 | 0.73% | 0.67% | 0.66% | |

| Scotland | 15,566 | 14,384 | 14,584 | 0.81% | 0.72% | 0.71% | |

| Northern Ireland | 9,516 | 9,303 | 9,171 | 0.50% | 0.47% | 0.44% | |

| United Kingdom | 71,840 | 44,887 | 41,823 | 3.76% | 2.26% | 2.02% | |

Download this table Table 1: Net fiscal balance from financial year ending (FYE) 2016 to FYE 2018, by NUTS1 countries and regions

.xls .csvAs the number of people in a particular country or region can affect the amount of revenue raised in that area or the amount of expenditure needed to benefit the residents and enterprises, the main aggregates in this publication are also presented on a per head basis.

Table 2 shows the net fiscal balance per head of the NUTS1 countries and regions from FYE 2016 to FYE 2018.

| Net Fiscal Balance per head (£)¹ | |||||||

|---|---|---|---|---|---|---|---|

| North Sea revenue geographic share² | North Sea revenue population share² | ||||||

| Country/Region | 2015/16 | 2016/17 | 2017/18 | 2015/16 | 2016/17 | 2017/18 | |

| North East | 4,003 | 3,706 | 3,667 | 3,999 | 3,695 | 3,641 | |

| North West | 3,046 | 2,710 | 2,884 | 3,046 | 2,707 | 2,863 | |

| Yorkshire and the Humber | 2,621 | 2,241 | 2,164 | 2,610 | 2,222 | 2,133 | |

| East Midlands | 1,646 | 1,324 | 1,263 | 1,643 | 1,317 | 1,240 | |

| West Midlands | 2,517 | 2,329 | 2,274 | 2,518 | 2,329 | 2,254 | |

| East of England | -402 | -915 | -966 | -403 | -920 | -988 | |

| London | -2,948 | -3,825 | -3,905 | -2,947 | -3,826 | -3,925 | |

| South East | -1,650 | -2,119 | -2,258 | -1,648 | -2,120 | -2,278 | |

| South West | 1,261 | 920 | 868 | 1,260 | 917 | 846 | |

| England | 598 | 146 | 102 | 597 | 142 | 80 | |

| Wales | 4,502 | 4,289 | 4,395 | 4,504 | 4,289 | 4,375 | |

| Scotland | 2,882 | 2,612 | 2,452 | 2,893 | 2,659 | 2,696 | |

| Northern Ireland | 5,131 | 4,991 | 4,939 | 5,132 | 4,990 | 4,919 | |

| United Kingdom³ | 1,101 | 683 | 636 | 1,101 | 683 | 636 | |

Download this table Table 2: Net fiscal balance per head from financial year ending (FYE) 2016 to FYE 2018, by NUTS1 countries and regions

.xls .csvNorthern Ireland had the highest net fiscal deficit, while London had the highest net fiscal surplus per head, in FYE 2018. The UK as a whole has had a net fiscal deficit since FYE 2002. However, this varies between countries and regions. Most countries and regions have had a net fiscal deficit for the full duration of the period presented in these statistics, which is since FYE 2000. Some regions, such as the East of England, the East Midlands and the South West had net fiscal surpluses in the early period, while London and the South East have generally maintained net fiscal surpluses for the full period.

Nôl i'r tabl cynnwys5. Public sector revenue

During the financial year ending (FYE) 2018, total public sector revenue raised in the UK was £753.1 billion (£11,434 per head), representing an increase of £26.0 billion (£395 per head), from FYE 2017. All of the 12 Nomenclature of Units for Territorial Statistics: NUTS1 regions have also seen an increase in revenue in this financial year.

Most revenue was raised in London (£150.1 billion) and the South East (£121.4 billion), which has remained fairly consistent over time when North Sea revenue was included either on a geographic or population basis. This is equivalent to £17,090 and £13,427 per head, respectively.

Figure 3: Between the financial years ending 2000 and 2018, London, the South East and the East of England raised more revenue per head than the UK average

Average NUTS1 revenue per head differences against UK per head, financial year ending 2000 to financial year ending 2018

Source: Office for National Statistics

Notes:

- North sea oil and gas revenues included on a geographic share and a population share.

Download this chart Figure 3: Between the financial years ending 2000 and 2018, London, the South East and the East of England raised more revenue per head than the UK average

Image .csv .xlsThe increase in revenue in all NUTS1 regions, and therefore the UK, was mainly driven by growth in National Insurance contributions (NICs), Onshore Corporation Tax, Income Tax and Value Added Tax (VAT). We have also seen a large increase in Offshore Corporation Tax between FYE 2017 and FYE 2018, caused by an increase in the value of oil sales despite a reduction in production.

Over time, the revenue of most countries and regions as a percentage of gross domestic product (GDP) has been fairly stable. At the UK level, it has remained between 33% and 37% of GDP for the full duration presented in these statistics. Table 3 shows revenue raised in each country and region over the last three years, as a percentage of GDP, presented alongside revenue raised per head.

| Total public sector revenue, incl. North Sea revenue geographic basis | |||||||

|---|---|---|---|---|---|---|---|

| Revenue as % of GDP | Revenue per head¹ (£) | ||||||

| Country/Region | 2015/16 | 2016/17 | 2017/18 | 2015/16 | 2016/17 | 2017/18 | |

| North East | 1.13% | 1.15% | 1.14% | 8,234 | 8,634 | 8,938 | |

| North West | 3.26% | 3.32% | 3.31% | 8,681 | 9,132 | 9,452 | |

| Yorkshire and the Humber | 2.44% | 2.49% | 2.47% | 8,651 | 9,102 | 9,416 | |

| East Midlands | 2.24% | 2.27% | 2.26% | 9,133 | 9,547 | 9,883 | |

| West Midlands | 2.59% | 2.63% | 2.62% | 8,577 | 8,984 | 9,308 | |

| East of England | 3.51% | 3.56% | 3.54% | 11,028 | 11,552 | 11,936 | |

| London | 7.11% | 7.31% | 7.26% | 15,652 | 16,561 | 17,090 | |

| South East | 5.74% | 5.91% | 5.87% | 12,247 | 13,002 | 13,427 | |

| South West | 2.82% | 2.87% | 2.86% | 9,842 | 10,339 | 10,685 | |

| England | 30.85% | 31.51% | 31.34% | 10,747 | 11,325 | 11,705 | |

| Wales | 1.29% | 1.31% | 1.31% | 7,974 | 8,375 | 8,691 | |

| Scotland | 2.83% | 2.88% | 2.94% | 10,063 | 10,609 | 11,230 | |

| Northern Ireland | 0.84% | 0.84% | 0.83% | 8,614 | 8,945 | 9,255 | |

| United Kingdom² | 35.81% | 36.55% | 36.43% | 10,498 | 11,059 | 11,454 | |

| Total public sector revenue, incl. North Sea revenue population basis | |||||||

| Revenue as % of GDP | Revenue per head¹ (£) | ||||||

| Country/Region | 2015/16 | 2016/17 | 2017/18 | 2015/16 | 2016/17 | 2017/18 | |

| North East | 1.13% | 1.15% | 1.14% | 8,237 | 8,644 | 8,963 | |

| North West | 3.26% | 3.32% | 3.31% | 8,681 | 9,135 | 9,473 | |

| Yorkshire and the Humber | 2.45% | 2.49% | 2.48% | 8,661 | 9,121 | 9,446 | |

| East Midlands | 2.24% | 2.27% | 2.27% | 9,136 | 9,554 | 9,906 | |

| West Midlands | 2.59% | 2.63% | 2.63% | 8,576 | 8,985 | 9,328 | |

| East of England | 3.51% | 3.57% | 3.55% | 11,029 | 11,556 | 11,958 | |

| London | 7.11% | 7.31% | 7.27% | 15,651 | 16,562 | 17,110 | |

| South East | 5.74% | 5.91% | 5.88% | 12,246 | 13,003 | 13,447 | |

| South West | 2.82% | 2.87% | 2.86% | 9,843 | 10,342 | 10,706 | |

| England | 30.86% | 31.53% | 31.40% | 10,748 | 11,330 | 11,728 | |

| Wales | 1.29% | 1.31% | 1.31% | 7,973 | 8,376 | 8,710 | |

| Scotland | 2.83% | 2.87% | 2.87% | 10,052 | 10,562 | 10,986 | |

| Northern Ireland | 0.84% | 0.84% | 0.84% | 8,613 | 8,945 | 9,275 | |

| United Kingdom² | 35.81% | 36.55% | 36.43% | 10,498 | 11,059 | 11,454 | |

Download this table Table 3: Total public sector revenue as percentage of UK gross domestic product and per head from financial year ending (FYE) 2016 to FYE 2018, by NUTS1 countries and regions

.xls .csv6. Public sector expenditure

In the financial year ending (FYE) 2018, total public sector expenditure at the UK level was £795.0 billion, or £12,091 per head. The Nomenclature of Units for Territorial Statistics: NUTS1 region incurring the most expenditure for the benefit of residents and enterprises was London, at approximately £115.8 billion, which equates to £13,185 per head, or approximately 15% of the UK total.

On average, for the full duration of the statistics presented in this publication, spending per head each year in Northern Ireland, Scotland, Wales, London, the North West and the North East has been above the UK average. Figure 4 shows how much each NUTS1 region has spent per head, compared with the UK on average, between FYE 2000 and FYE 2018.

Figure 4: Between the financial years ending 2000 and 2018, Northern Ireland, Scotland, Wales, London, the North West and the North East have spent more per head than the UK average

Average NUTS1 per head spending differences against UK per head, financial year ending 2000 to financial year ending 2018

Source: Office for National Statistics

Download this chart Figure 4: Between the financial years ending 2000 and 2018, Northern Ireland, Scotland, Wales, London, the North West and the North East have spent more per head than the UK average

Image .csv .xlsTable 4 shows how much of this expenditure occurred for the benefit of residents and enterprises in each country and region in the UK from FYE 2016 to FYE 2018.

| Total public sector expenditure | |||||||

|---|---|---|---|---|---|---|---|

| Total public sector expenditure (£ million) | Per head (£)¹ | ||||||

| Country or region | 2015/16 | 2016/17 | 2017/18 | 2015/16 | 2016/17 | 2017/18 | |

| North East | 32,152 | 32,559 | 33,258 | 12,236 | 12,339 | 12,604 | |

| North West | 84,284 | 85,650 | 89,221 | 11,727 | 11,842 | 12,336 | |

| Yorkshire and The Humber | 60,855 | 61,608 | 62,895 | 11,272 | 11,343 | 11,580 | |

| East Midlands | 50,548 | 51,495 | 52,797 | 10,779 | 10,871 | 11,146 | |

| West Midlands | 64,002 | 65,884 | 67,446 | 11,094 | 11,314 | 11,582 | |

| East of England | 64,705 | 65,294 | 67,343 | 10,626 | 10,636 | 10,970 | |

| London | 110,432 | 111,864 | 115,808 | 12,704 | 12,736 | 13,185 | |

| South East | 95,058 | 98,411 | 100,997 | 10,598 | 10,883 | 11,169 | |

| South West | 60,878 | 62,234 | 63,858 | 11,103 | 11,259 | 11,553 | |

| England | 622,914 | 634,999 | 653,623 | 11,345 | 11,471 | 11,808 | |

| Wales | 38,710 | 39,464 | 40,776 | 12,477 | 12,664 | 13,085 | |

| Scotland | 69,656 | 71,519 | 74,015 | 12,945 | 13,220 | 13,682 | |

| Northern Ireland | 25,486 | 25,980 | 26,463 | 13,745 | 13,935 | 14,195 | |

| UK² | 756,767 | 771,962 | 794,876 | 11,599 | 11,742 | 12,090 | |

Download this table Table 4: Total public sector expenditure from financial year ending (FYE) 2016 to FYE 2018, by NUTS1 countries and regions

.xls .csvBetween FYE 2017 and FYE 2018, total expenditure increased from £772.0 billion to £795.9 billion, however, this equated to a fall of 0.36 percentage points of gross domestic product (GDP). Between FYE 2010 and FYE 2018, total UK public sector expenditure has fallen by 6.49 percentage points of GDP. London has seen the largest drop in expenditure, while all other NUTS1 regions have seen smaller falls in expenditure as percentages of GDP.

| Total public sector expenditure as % of GDP¹ | |||||

|---|---|---|---|---|---|

| Country or region | 2013/14 | 2014/15 | 2015/16 | 2016/17 | 2017/18 |

| North East | 1.77% | 1.72% | 1.68% | 1.64% | 1.61% |

| North West | 4.60% | 4.50% | 4.41% | 4.31% | 4.32% |

| Yorkshire and The Humber | 3.32% | 3.25% | 3.18% | 3.10% | 3.04% |

| East Midlands | 2.75% | 2.72% | 2.64% | 2.59% | 2.55% |

| West Midlands | 3.50% | 3.48% | 3.35% | 3.31% | 3.26% |

| East of England | 3.47% | 3.45% | 3.38% | 3.28% | 3.26% |

| London | 5.96% | 5.83% | 5.77% | 5.62% | 5.60% |

| South East | 5.17% | 5.08% | 4.97% | 4.95% | 4.89% |

| South West | 3.32% | 3.26% | 3.18% | 3.13% | 3.09% |

| England | 33.85% | 33.28% | 32.57% | 31.92% | 31.62% |

| Wales | 2.11% | 2.07% | 2.02% | 1.98% | 1.97% |

| Scotland | 3.82% | 3.71% | 3.64% | 3.60% | 3.58% |

| Northern Ireland | 1.41% | 1.39% | 1.33% | 1.31% | 1.28% |

| UK | 41.19% | 40.45% | 39.57% | 38.80% | 38.45% |

Download this table Table 5: Total public sector expenditure as a percentage of UK gross domestic product from financial year ending (FYE) 2014 to FYE 2018, by NUTS1 countries and regions

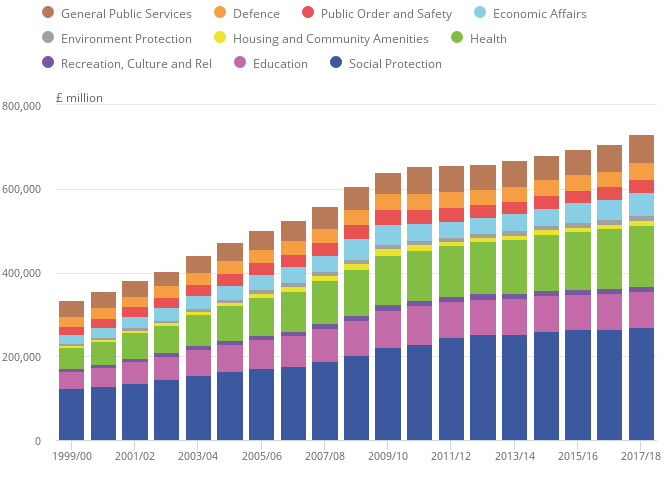

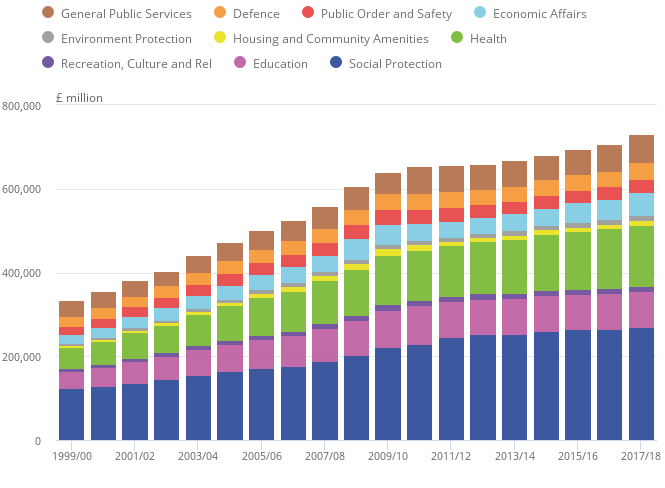

.xls .csvFor all regions and for the full duration of the statistics presented in this publication, social protection (mainly expenditure on pensions, but also on social benefits) has been the largest category of spending, followed by health and education.

Figure 5: For all regions and between the financial years ending 2000 and 2018, social protection has been the largest category of spending

UK total expenditure on services by function, financial year ending 2018

Source: Office for National Statistics

Download this image Figure 5: For all regions and between the financial years ending 2000 and 2018, social protection has been the largest category of spending

.png (19.3 kB) .xlsx (19.6 kB){kind=link}

7. What’s changed in this release?

A number of data and methodological changes have been made since the last publication, which gives rise to revisions in the data when compared with last year’s estimates. This section presents the revisions to net fiscal balance for each country and region and provides a brief explanation for these revisions.

Changes to the monthly public sector finances

Since June 2018, routine data source updates, quality improvements and methodological changes have revised the underlying UK public sector finances (PSF) data that this bulletin is based on. Not all of these changes affect the country and regional public sector finances. Only those that affect UK public sector net borrowing also have an impact on the country and regional public sector finances. These changes include:

fines and penalties for the late payments of taxes: additional revenue from fines and penalties for the late payment of taxes was included from the December 2018 PSF release

Value Added Tax (VAT) refunds data: updated source data following a review of the recording of VAT refunds data were introduced in the September 2018 PSF release only affecting FYE 2018 data

routine data source updates: revisions occur to the monthly PSF as a result of provisional estimates being replaced by final data

In this publication, we have also introduced some changes that had been implemented in the UK public sector finances previously but had not been introduced in the country and regional public sector finances because they only affected the data from the FYE 2017 onwards. These changes are:

Apprenticeship Levy: the revenue from this levy was recorded in the June 2017 PSF release after the classification decision in June 2017

Immigration Skills Charge: the revenue from this tax was included in the November 2017 PSF release

Revisions prior to FYE 2011 are a result of improving our business processes for producing these statistics.

| Year (£ million) | UK² ³ | North East | North West | Yorkshire and The Humber | East Midlands | West Midlands | East of England |

|---|---|---|---|---|---|---|---|

| 1999/00 | 0 | -5 | -9 | -6 | -8 | -6 | -4 |

| 2000/01 | 0 | -6 | -11 | -9 | -8 | -7 | -5 |

| 2001/02 | 0 | -6 | -10 | -9 | -8 | -7 | -4 |

| 2002/03 | 0 | -5 | -7 | -5 | -6 | -6 | -3 |

| 2003/04 | 0 | -4 | -8 | -5 | -6 | -5 | -3 |

| 2004/05 | 0 | -4 | -7 | -5 | -6 | -6 | -3 |

| 2005/06 | 0 | -4 | -7 | -4 | -6 | -6 | -4 |

| 2006/07 | 0 | -4 | -7 | -5 | -7 | -6 | -4 |

| 2007/08 | 0 | -4 | -10 | -5 | -7 | -7 | -5 |

| 2008/09 | 0 | -5 | -9 | -7 | -8 | -8 | -7 |

| 2009/10 | 0 | -6 | -8 | -6 | -9 | -7 | -7 |

| 2010/11 | -343 | -14 | -38 | -26 | -26 | -28 | -36 |

| 2011/12 | -305 | -12 | -33 | -23 | -21 | -23 | -35 |

| 2012/13 | -459 | -17 | -47 | -33 | -31 | -36 | -49 |

| 2013/14 | -550 | -71 | 231 | -120 | 137 | -126 | 217 |

| 2014/15 | -620 | 23 | 21 | 9 | 84 | 147 | 221 |

| 2015/16 | -618 | 88 | -149 | 47 | -20 | -23 | 91 |

| 2016/17 | -790 | -32 | 195 | 226 | 38 | 195 | -125 |

| Year (£ million) | London | South East | South West | England | Wales | Scotland | Northern Ireland |

| 1999/00 | 54 | -1 | -3 | 12 | -5 | -3 | -4 |

| 2000/01 | 62 | -1 | -4 | 11 | -6 | -2 | -3 |

| 2001/02 | 60 | 0 | -4 | 12 | -7 | -2 | -3 |

| 2002/03 | 43 | 0 | -3 | 8 | -5 | -1 | -2 |

| 2003/04 | 42 | -1 | -2 | 8 | -4 | -3 | -1 |

| 2004/05 | 41 | -2 | -3 | 5 | -4 | 0 | -1 |

| 2005/06 | 44 | -4 | -3 | 6 | -4 | 0 | -2 |

| 2006/07 | 47 | -2 | -3 | 9 | -4 | -3 | -2 |

| 2007/08 | 54 | -5 | -3 | 8 | -5 | -1 | -2 |

| 2008/09 | 64 | -5 | -3 | 12 | -6 | -3 | -3 |

| 2009/10 | 65 | -1 | -3 | 18 | -8 | -4 | -6 |

| 2010/11 | -34 | -57 | -29 | -288 | -16 | -30 | -9 |

| 2011/12 | -29 | -56 | -25 | -257 | -14 | -25 | -9 |

| 2012/13 | -60 | -80 | -37 | -390 | -19 | -37 | -13 |

| 2013/14 | -502 | 102 | -28 | -157 | -81 | -217 | -97 |

| 2014/15 | -785 | 139 | -138 | -277 | -57 | -262 | -21 |

| 2015/16 | -58 | 19 | -237 | -241 | -66 | -263 | -50 |

| 2016/17 | -1,124 | 279 | -301 | -649 | 117 | -214 | -44 |

Download this table Table 6a: Revisions to public sector net fiscal balance¹ (geographic basis), financial year ending (FYE) 2000 to FYE 2017, by NUTS1 countries and regions

.xls .csv

| Year (£ million) | UK² ³ | North East | North West | Yorkshire and The Humber | East Midlands | West Midlands | East of England |

|---|---|---|---|---|---|---|---|

| 1999/00 | 0 | -5 | -9 | -6 | -8 | -6 | -4 |

| 2000/01 | 0 | -6 | -11 | -9 | -8 | -7 | -5 |

| 2001/02 | 0 | -6 | -10 | -9 | -8 | -7 | -4 |

| 2002/03 | 0 | -5 | -7 | -5 | -6 | -6 | -3 |

| 2003/04 | 0 | -4 | -8 | -5 | -6 | -5 | -3 |

| 2004/05 | 0 | -4 | -7 | -5 | -6 | -6 | -3 |

| 2005/06 | 0 | -4 | -7 | -4 | -6 | -6 | -4 |

| 2006/07 | 0 | -4 | -7 | -5 | -7 | -6 | -4 |

| 2007/08 | 0 | -4 | -10 | -5 | -7 | -7 | -5 |

| 2008/09 | 0 | -5 | -9 | -7 | -8 | -8 | -7 |

| 2009/10 | 0 | -6 | -8 | -6 | -9 | -7 | -7 |

| 2010/11 | -343 | -14 | -38 | -26 | -26 | -28 | -36 |

| 2011/12 | -305 | -12 | -33 | -23 | -21 | -23 | -35 |

| 2012/13 | -459 | -17 | -47 | -33 | -31 | -36 | -49 |

| 2013/14 | -550 | -71 | 231 | -120 | 137 | -126 | 217 |

| 2014/15 | -620 | 23 | 21 | 9 | 84 | 147 | 221 |

| 2015/16 | -618 | 88 | -149 | 47 | -20 | -23 | 91 |

| 2016/17 | -790 | -32 | 195 | 226 | 38 | 195 | -125 |

| Year (£ million) | London | South East | South West | England | Wales | Scotland | Northern Ireland |

| 1999/00 | 54 | -1 | -3 | 12 | -5 | -3 | -4 |

| 2000/01 | 62 | -1 | -4 | 11 | -6 | -2 | -3 |

| 2001/02 | 60 | 0 | -4 | 12 | -7 | -2 | -3 |

| 2002/03 | 43 | 0 | -3 | 8 | -5 | -1 | -2 |

| 2003/04 | 42 | -1 | -2 | 8 | -4 | -3 | -1 |

| 2004/05 | 41 | -2 | -3 | 5 | -4 | 0 | -1 |

| 2005/06 | 44 | -4 | -3 | 6 | -4 | 0 | -2 |

| 2006/07 | 47 | -2 | -3 | 9 | -4 | -3 | -2 |

| 2007/08 | 54 | -5 | -3 | 8 | -5 | -1 | -2 |

| 2008/09 | 64 | -5 | -3 | 12 | -6 | -3 | -3 |

| 2009/10 | 65 | -1 | -3 | 18 | -8 | -4 | -6 |

| 2010/11 | -34 | -57 | -29 | -288 | -16 | -30 | -9 |

| 2011/12 | -29 | -56 | -25 | -257 | -14 | -25 | -9 |

| 2012/13 | -60 | -80 | -37 | -390 | -19 | -37 | -13 |

| 2013/14 | -502 | 102 | -28 | -157 | -81 | -217 | -97 |

| 2014/15 | -785 | 139 | -138 | -277 | -57 | -262 | -21 |

| 2015/16 | -58 | 19 | -237 | -241 | -66 | -263 | -50 |

| 2016/17 | -1,124 | 279 | -301 | -649 | 117 | -214 | -44 |

Download this table Table 6b: Revisions to public sector net fiscal balance¹ (population basis), financial year ending (FYE) 2000 to FYE 2017, by NUTS1 countries and regions

.xls .csv8. Public value of statistics on public finances in a devolved UK

In July 2018, the Office for Statistics Regulation (OSR) announced a review into the public value of statistics on public finances in a devolved UK. The review researched existing published devolved public finance statistics, including the country and regional public sector finances, and engaged with statisticians and users of these statistics to assess relevance, transparency and coherence of the statistics. OSR published their findings and recommendations on 24 May 2019. The review suggested that we produce useful and plentiful data on devolved public finances, though suggested there was an opportunity to work with those within countries and regions who can provide additional local context to the statistics and so develop more compelling narratives. We will incorporate findings of the report into our future work plans and continue to collaborate with devolved nations and other producers of similar statistics to find ways to further improve the communication of our statistics.

Nôl i'r tabl cynnwys10. Future developments

As described at the start of this publication, Experimental Statistics are statistics still under development. As such, we welcome and encourage your feedback about how you use these statistics, what you have found useful and what you would potentially like to see in the future.

Areas of development and improvement we plan to focus on over the next year include, but are not limited to:

moving the annual publication timing to late November or early December, from 2019; this means that the lag will be reduced from 13 months to 7 months after the end of the reporting period and our statistics will be available at a similar time to HM Revenue and Customs’ (HMRC) Disaggregation of tax receipts and HM Treasury’s Country and regional analysis, which are published in October and November respectively

improving methods and data sources to refine allocation of UK revenue or expenditure to the NUTS1 regions, while also working to further align methods with those used by HMRC and Scottish Government in their publications

working with colleagues in devolved administrations, HMRC, Office for Budget Responsibility and the Scottish Funding Council to align and improve methodologies of those taxes due to be devolved

investigating extending the current presentation to include expenditure by type (for example, pay, goods and services) and not just function, as well as producing sectoral breakdowns (for example, central government, local government, public corporations)

investigating the feasibility of introducing work-placed estimates for some revenues to complement the residential-based estimates currently produced

working towards achieving National Statistics accreditation

11. Quality and methodology

How are the country and regional estimates calculated?

The total UK public sector revenue and expenditure reported in this publication are the same as those in the February 2019 public sector finances (PSF) bulletin. However, the country and regional allocation of revenue and expenditure data in this publication are largely based on various assumptions. This is because taxes are generally not levied or collected on a regional basis and most spending is planned to benefit a category of individuals and enterprises irrespective of location.

Estimates of public sector revenue are based on the concept of “who pays”. Revenue is attributed to the countries and regions of the UK using apportionment methods, such as the use of surveys, population shares and gross value added (GVA) shares.

Estimates of public sector expenditure are based on the concept of “who benefits”. Expenditure in each of the countries and regions of the UK is calculated using methods that attempt to apportion expenditure based on the location of the residents or enterprises who have benefited from expenditure of a particular department or body. This can be challenging as most public spending is planned to benefit categories of individuals and enterprises irrespective of location and only a minority of public spending is planned on a regional basis.

The UK data used in this publication are sourced from the PSF bulletin and are apportioned to Nomenclature of Units for Territorial Statistics: NUTS1 regions using various methodologies. Expenditure data are sourced from HM Treasury’s Country and regional analysis (CRA), with few adjustments made to bring the data in line with PSF aggregates.

The CRA data are based on HM Treasury’s measure of “total expenditure on services” and accounting adjustments are used to move to “total managed expenditure”, which is equivalent to that recorded in the UK PSF. As such, the expenditure statistics in this publication are presented on the functional classification used by HM Treasury in their expenditure publications.

For further information on the statistical methods used to allocate revenue and expenditure items, please refer to the country and regional public sector finances methodology guide. This guide describes the data and methods used to attribute revenue and expenditure to countries and regions. It also compares the method used with that followed in other publications (see Section 9,Links to related statistics) and highlights any potential weaknesses in the data and/or methodology.

What is the relationship between these statistics and those of the UK public sector finances?

The UK public sector finances (PSF) bulletin is a monthly publication jointly produced by Office for National Statistics (ONS) and HM Treasury. By contrast this is an annual publication produced solely by ONS. However, the two publications are closely linked as the UK totals published in the monthly PSF bulletin form the UK expenditure and revenue totals that must be apportioned to the NUTS1 country and regions of the UK. The total UK expenditure and revenue in this publication match those in the February 2019 PSF bulletin.

At the UK level the equivalent of the net fiscal balance is termed public sector net borrowing excluding public sector banks (PSNB ex). A positive PSNB ex (and positive net fiscal balance) indicates a deficit, whereas negative values indicate a surplus. The net fiscal balance is not to be interpreted as the actual borrowing of a country or region; it is instead a statistical construct indicative of the difference between the revenue raised from residents and enterprises in a region and the public sector expenditure from which those residents and corporations benefit.

Are our figures adjusted for inflation?

All monetary values in the PSF bulletin are expressed in “current prices‟, that is, they represent the price in the period to which the expenditure or revenue relates and are not adjusted for inflation.

To compare data over long time periods, commentators often discuss changes over time to fiscal aggregates in terms of gross domestic product (GDP) ratios. GDP represents the value of all the goods and services currently produced by an economy in a period of time.

Quality

We have developed Guidelines for measuring statistical quality; these are based upon the five European Statistical System (ESS) quality dimensions, which are:

relevance – the degree to which statistics meet current and potential needs of the users

accuracy and reliability – the closeness between an estimated result and the (unknown) true value

timeliness and punctuality – the lapse of time between the period to which the data refer and publication of the estimate; and the time lag between the actual and planned dates of publication

accessibility and clarity – the ease with which users can access the data, the format(s) in which the data are available, the availability of supporting information and the extent to which easily comprehensible metadata are available, where these metadata are necessary to give a full understanding of the statistical data

coherence and comparability – the degree to which the statistical processes, by which two or more outputs are generated, use the same concepts and harmonised methods; and the degree to which data can be compared over time, region or other domain

The quality of our statistics is partially dependent on the quality of our data sources. While these guidelines are concerned with the quality of those data sources to the extent that it impacts the quality of our statistics, comprehensive information on a particular data source should be obtained through the links provided throughout the methodology guide.

Relevance

The aim of these statistics is to provide users with information on what public sector expenditure has occurred, for the benefit of residents or enterprises, in each country or region of the UK and what public sector revenues have been raised in each country or region. This is with the aim of supporting the devolution debate. The statistics refer to financial years running from April to March and are based on NUTS1 boundaries, which separate Wales, Scotland, Northern Ireland and nine English regions.

Consultations have been held in 2016 and 2017 to gather information about the requirements of users and feedback on the 2017 publication. Consultation responses and actions that have been taken as a result appear throughout the bulletin and methodology guide. There is wide support for the completeness, consistency and comparability between countries and regions that the publication provides.

Where it has not been possible to take a consistent approach to all countries and regions, this is stated in the methodology guide. This has been kept to a minimum and is most notable in the case of Corporation Tax (offshore) and Petroleum Revenue Tax. Apportionment methods are described in detail in the methodology guide, which also lists data sources.

Accuracy and reliability

Accuracy depends upon the absence of errors. Statistics that rely upon a broad range of data sources are inevitably affected by various types of error. The main sources of error are described and assessed in this section.

Sampling error

Sampling errors occur when statistics are based upon random samples from the population of interest. For example, the Living Costs and Food Survey, data from which is used to apportion tobacco duties (and, indirectly, alcohol duties), uses expenditure data from a random sample of individuals to estimate the average expenditure of the UK population. While certain statistical controls will increase the likelihood that the sample is representative of the population, the estimates are unlikely to be the same as the population averages. Moreover, different samples will produce different estimates. The variability amongst the individuals in the sample can be used to estimate the variability between all the samples that might have been taken and therefore the accuracy of the estimate.

Much of the data used come from administrative sources and are therefore not subject to sampling error. However, a non-trivial amount of apportionment data are from sample surveys. Measures of the sampling error present in these surveys can be used to construct estimates of the resulting sampling error in our statistics. Unfortunately, these measures are not always produced and when they are produced it is not always at a granularity that suits our purposes.

Due to the range of data sources involved and the work needed to gather the necessary information, it has not been possible to include measures of sampling error in this year’s publication. These measures are currently being developed and we expect to publish them in the next release.

Imputation

In statistics, imputation is the substitution of missing values with estimated quantities. Imputation is performed in the production of some of our source data and in the processing of certain parts of that data.

In some cases, apportionment data for the most recent year are not available at the time of publication. In these cases, the previous year’s apportionment is usually used. There are also circumstances where data on a calendar-year basis must be converted to a financial-year basis. Occasionally, other imputations are required, most notably for Air Passenger Duty, where the passenger numbers for some categories in select periods are unavailable. Measures of the robustness and likely impact of these approximations are also being developed.

Coverage error, measurement bias and processing error

Coverage error occurs when the population being measured does not precisely align to the population of interest. Known sources of coverage error are described throughout the methodology guide.

Measurement bias refers to consistent differences between a measured quantity and the quantity of interest. This may be attributable to imperfect methods of observation or indirect measurement. One example is self-reported alcohol consumption, which is used to apportion alcohol duties. This is known to be lower than actual consumption. Assuming that under-reporting is consistent across regions, this should not affect apportionment.

Processing errors include incorrect data entry and categorisation. These errors are minimised by quality assurance procedures.

Other sources of error include the use of tax receipts data as a proxy for accrued tax and apportionment by population or GVA where no preferable regional data are available.

Timeliness and punctuality

The Country and regional public sector finances publication is published on an annual basis. It was initially expected that the statistics would be published in May each year, 13 months after the end of the reporting period, but this was delayed to August 2018. We intend to publish country and regional PSF twice in 2019; in May and again in November or December, shortly after the publication of HM Treasury’s Country and regional analysis. Thereafter, publication will occur in November each year, seven months after the end of the reporting period, to improve timeliness and coincide with HM Treasury’s publication.

Accessibility and clarity

Our recommended format for accessible content is a combination of HTML web pages for narrative, charts and graphs, with data being provided in Excel format. Our website also offers users the option to download the narrative in PDF format. In some instances, other software may be used, or may be available on request. Available formats for content published on our website but not produced by us, or referenced on our website but stored elsewhere, may vary. For further information, please refer to the contact details at the beginning of this article.

For information regarding conditions of access to data, please refer to the following links:

terms and conditions (for data on the website)

Coherence and comparability

Our statistics are fully coherent with UK public sector finances as this is the source of our total UK values. With regards to apportionment methods, the level of consistency with similar publications is discussed throughout the methodology guide.

As far as possible, the data are comparable across countries and regions but certain items necessarily have different data sources for country-level data and English regional data. This is explained in the relevant sections of the methodology guide.

Nôl i'r tabl cynnwys