Cynnwys

- Other pages in this release

- Main points

- Current trading status of businesses

- Businesses’ financial performance

- Comparison with monthly GDP estimates across waves

- Business resilience

- Workforce

- Homeworking

- Government schemes

- Site closures

- EU and non-EU workers

- Business Impact of Coronavirus (COVID-19) Survey data

- Glossary

- Measuring the data

- Strengths and limitations

- Related links

1. Other pages in this release

More commentary on the impacts of the coronavirus (COVID-19) pandemic on the UK economy and society is available on the following pages:

Nôl i'r tabl cynnwys2. Main points

The accommodation and food service activities industry had the lowest percentage of businesses currently trading, at 75%, compared with 85% across all industries.

Between Wave 12 (10 to 23 August 2020) and Wave 16 (5 to 18 October 2020), the trend in the percentages of businesses experiencing a decrease in turnover has flattened.

In Wave 16 (5 to 18 October 2020), 8% of the workforce were on furlough leave, compared with 30% in Wave 7 (1 to 14 June 2020).

The accommodation and food service activities industry had the highest percentage of businesses with no cash reserves, at 6%, compared with 3% across all industries.

The accommodation and food service activities industry had the highest percentage of businesses with no or low confidence that their businesses would survive the next three months, at 32%.

Of businesses not permanently stopped trading, 17% intend to use increased homeworking as a permanent business model in the future.

3. Current trading status of businesses

Final results from Wave 16 of the Business Impact of Coronavirus (COVID-19) Survey (BICS) are for the period 5 to 18 October 2020, which closed on 1 November 2020.

These data were collected over the period 19 October to 1 November 2020 and refer to the period 5 to 18 October 2020. This should be kept in mind in relation to local and national lockdowns and, dependent on the location and date when the business responded, this could impact on the estimates.

For presentational purposes:

"has been trading for more than the last two weeks" and "started trading within the last two weeks after a pause in trading" have been combined to "currently trading"

"paused trading but intends to restart in the next two weeks" and "paused trading and does not intend to restart in the next two weeks" have been combined to "temporarily closed or paused trading"

The breakdowns of these categories are available in the accompanying dataset.

Figure 1: The accommodation and food services industry had the lowest percentage of businesses currently trading, at 75%, compared with 85% across all industries

Percentage of businesses, current trading status, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey (BICS).

- Bars may not sum to 100% because of rounding and percentages less than 1% being removed for disclosure purposes.

- Other services and Mining and quarrying have been removed for presentational purposes, but their totals are included in "All Industries".

- Businesses were asked for their current trading status and so responses will be from the point of completion of the questionnaire (19 October to 1 November 2020).

Download this chart Figure 1: The accommodation and food services industry had the lowest percentage of businesses currently trading, at 75%, compared with 85% across all industries

Image .csv .xlsAcross all industries:

82% of businesses had been trading for more than the last two weeks

2% of businesses had started trading within the last two weeks after a pause in trading

4% of businesses had paused trading but intended to restart in the next two weeks

8% of businesses had paused trading and did not intend to restart in the next two weeks

4% of businesses had permanently ceased trading

The arts, entertainment and recreation industry had the highest percentage of businesses that were temporarily closed or paused trading, at 22%. This was followed by the accommodation and food service activities industry and the administrative and support service activities industry, at 18% and 16% respectively.

Figure 2 shows the trend in weighted trading status estimates between Wave 7 (1 to 14 June 2020) and Wave 16 (5 to 18 October 2020).

Figure 2: After a steady increase, the percentage of businesses currently trading has flattened from Wave 14 (7 to 20 September 2020) to Wave 16 (5 to 18 October 2020)

Percentage of businesses, current trading status, broken down by wave, weighted, UK, 1 June to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 7 to Wave 16 of the Office for National Statistics (ONS) Businesses Impact of Coronavirus (COVID-19) Survey (BICS).

- Waves may not sum to 100% because of rounding, percentages less than 1% being removed for disclosure purposes, and those permanently ceased trading being removed.

- Businesses were asked for their current trading status and so responses will be from the point of completion of the questionnaire.

Download this chart Figure 2: After a steady increase, the percentage of businesses currently trading has flattened from Wave 14 (7 to 20 September 2020) to Wave 16 (5 to 18 October 2020)

Image .csv .xlsThe percentage of businesses currently trading steadily increased from 66% in Wave 7 (1 to 14 June 2020) to 86% in Wave 14 (7 to 20 September 2020), but has flattened over Waves 15 and 16. The percentage of businesses temporarily closed or paused trading has similarly flattened after a steady decline.

Table 1 shows how the trading status of larger businesses compare with micro businesses (businesses with fewer than 10 employees). In Wave 16, 84% of micro businesses were currently trading, compared with 98% of businesses with 250 or more employees.

| Size band | Currently trading | Temporarily closed or paused trading | Permanently ceased trading |

|---|---|---|---|

| 0 to 9 | 83.5% | 12.3% | 4.2% |

| 10 to 49 | 93.9% | 4.8% | 1.3% |

| 50 to 99 | 96.2% | 2.5% | 1.2% |

| 100 to 249 | 98.4% | 1.3% | * |

| 250 and over | 97.5% | 2.1% | * |

| All size bands excluding 0 to 9 | 94.4% | 4.3% | 1.2% |

| All size bands | 84.6% | 11.4% | 3.9% |

Download this table Table 1: Percentage of businesses, current trading status, broken down by size band, weighted, 5 to 18 October 2020

.xls .csv4. Businesses’ financial performance

For presentational purposes, in Figure 3 and Figure 4, decreased turnover categories and increased turnover categories have been combined. The breakdowns of these categories are available in the accompanying dataset.

Figure 3: There were three industries where more than 50% of businesses experienced a decrease in turnover

Impact on turnover, businesses that are currently trading, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey; businesses currently trading.

- Bars may not sum to 100% because of rounding and percentages less than 1% being removed for disclosure purposes.

- Other services and Mining and quarrying have been removed for presentational purposes, but their totals are included in "All Industries".

- Businesses were asked for their experiences for the reference period 5 to 18 October 2020. However, for questions regarding the last two weeks, businesses may respond from the point of completion of the questionnaire (19 October to 1 November 2020).

Download this chart Figure 3: There were three industries where more than 50% of businesses experienced a decrease in turnover

Image .csv .xlsAcross all industries, of businesses currently trading:

45% experienced a decrease in turnover compared with what is normally expected for this time of year

37% experienced no impact on turnover

10% experienced an increase in turnover compared with what is normally expected for this time of year

There were three industries where more than 50% of businesses experienced a decrease in turnover, compared with 45% across all industries. These were the accommodation and food service activities industry, at 72%; the arts, entertainment and recreation industry, at 69%; and the education industry (private sector and higher education businesses only), at 57%.

Only one other sector had a higher percentage of businesses experiencing a decrease in turnover compared with the average across all industries. This was the administrative and support service activities industry, at 46%.

Conversely, the wholesale and retail trade industry had the highest percentage of businesses experiencing an increase in turnover, at 16%. Additional information on the wholesale and retail trade industry is available in Retail sales, Great Britain: September 2020.

Figure 4 shows the trend in weighted turnover estimates between Wave 7 (1 to 14 June 2020) and Wave 16 (5 to 18 October 2020).

Figure 4: Between Wave 12 (10 to 23 August 2020) and Wave 16 (5 to 18 October 2020), the trend in the percentages of businesses experiencing a decrease in turnover has flattened

Impact on turnover, businesses that are currently trading, broken down by wave, weighted, UK, 1 June to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 7 to Wave 16 of the Office for National Statistics (ONS) Businesses Impact of Coronavirus (COVID-19) Survey (BICS); businesses currently trading.

- Waves may not sum to 100% because of rounding and percentages less than 1% being removed for disclosure purposes and "not sure" has been excluded.

- Businesses were asked for their experiences for the reference period. However, for questions regarding the last two weeks, businesses may respond from the point of completion of the questionnaire.

Download this chart Figure 4: Between Wave 12 (10 to 23 August 2020) and Wave 16 (5 to 18 October 2020), the trend in the percentages of businesses experiencing a decrease in turnover has flattened

Image .csv .xlsBetween Wave 12 (10 to 23 August 2020) and Wave 16 (5 to 18 October 2020), the downward trend in percentages of businesses experiencing a decrease in turnover has flattened. Overall, there has been a decrease, with 49% of businesses experiencing a decrease in turnover in Wave 12 compared with 45% in Wave 16. However, prior to Wave 12 there was a decreasing trend, with 65% of businesses experiencing a decrease in turnover in Wave 7 (1 to 14 June 2020) compared with 49% in Wave 12.

An unweighted regional breakdown of the impact of turnover for businesses' financial performance can be found in the accompanying dataset.

In Wave 16, businesses that were currently trading were also asked how the coronavirus (COVID-19) pandemic had affected their profits in the last two weeks, compared with normal expectations for this time of year.

For presentational purposes, in Figure 5, decreased profit categories and increased profit categories have been combined. The breakdowns of these categories are available in the accompanying dataset.

Figure 5: The accommodation and food service activities industry had the highest percentage of businesses who experienced a decrease in profits, at 71%, compared with 44% across all industries

Impact on profit, businesses that are currently trading, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the office for National Statistics (ONS) Businesses Impact of Coronavirus (COVID-19) Survey (BICS); businesses currently trading.

- Bars may not sum to 100% because of rounding and percentages less than 1% being removed for disclosure purposes.

- Other services and Mining and quarrying have been removed for presentational purposes, but their totals are included in “All Industries”.

- Businesses were asked for their experiences for the reference period 5 to 18 October 2020. However, for questions regarding the last two weeks, businesses may respond from the point of completion of the questionnaire (19 October to 1 November 2020).

Download this chart Figure 5: The accommodation and food service activities industry had the highest percentage of businesses who experienced a decrease in profits, at 71%, compared with 44% across all industries

Image .csv .xlsAcross all industries, of businesses currently trading:

44% experienced a decrease in profits compared with what is normally expected for this time of year

34% experienced no impact on profits

7% experienced an increase in profits compared with what is normally expected for this time of year

Similarly to the impact on turnover, the same four industries had the highest percentages of businesses experiencing a decrease in profits – the accommodation and food service activities industry, at 71%; the arts, entertainment and recreation industry, at 65%; the administrative and support service activities, at 50%; and the education industry (private sector and higher education businesses only), at 48%.

The wholesale and retail trade industry also had the highest percentage of businesses experiencing an increase in profits again, at 12%.

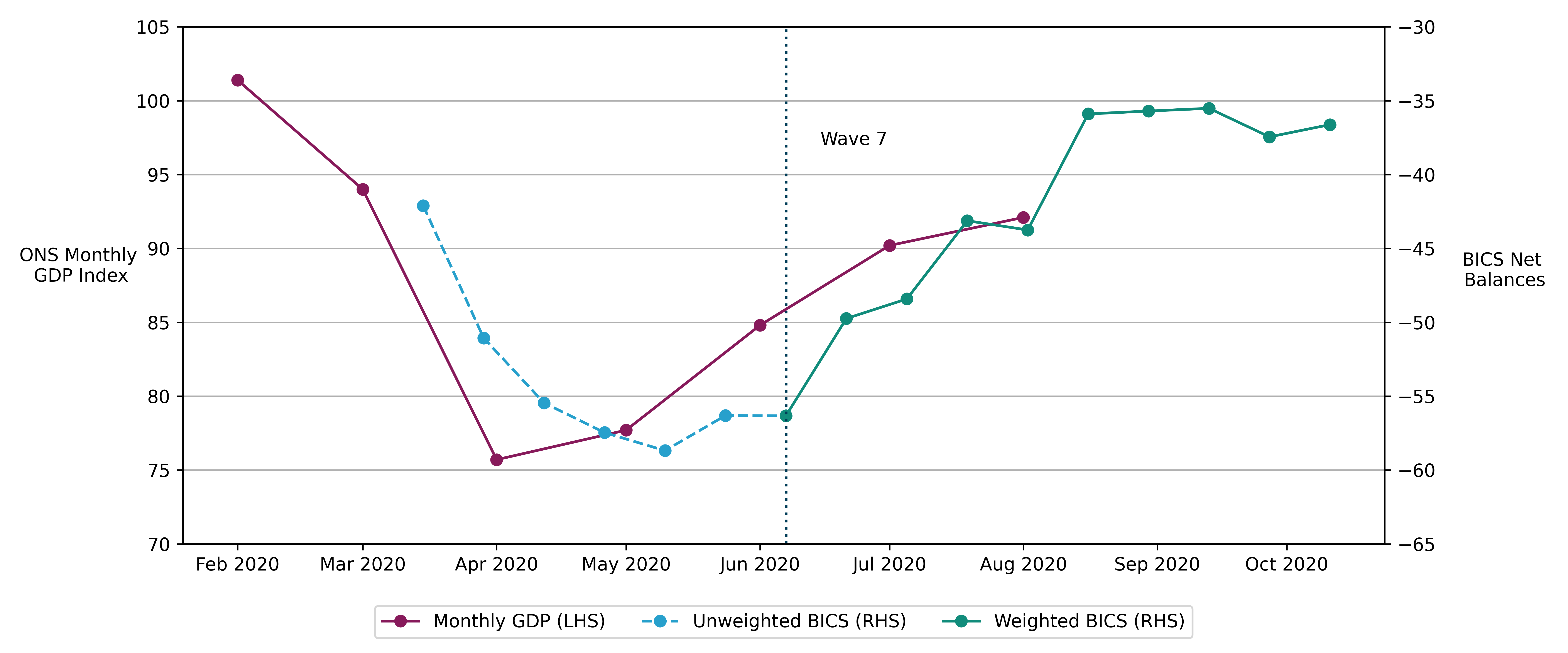

Nôl i'r tabl cynnwys5. Comparison with monthly GDP estimates across waves

Figure 6 shows how the fortnightly turnover estimates from the Businesses Impact of Coronavirus (COVID-19) Survey (BICS) broadly reflect the published UK monthly gross domestic product (GDP) estimates. This is despite the fact that BICS is published much earlier than the official monthly GDP estimates.

Figure 6: Fortnightly turnover estimates from Business Impact of Coronavirus Survey broadly reflect the published UK monthly gross domestic product estimates

Net turnover balances of businesses currently trading against GDP monthly estimates, UK, 1 February to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final unweighted results, Wave 1 to Wave 6, and final weighted results, Wave 7 to Wave 16, of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey (BICS).

- Weighted net balances have been calculated from Wave 7 onwards only. The sample redesign in Wave 7 improves our coverage for the small sized businesses, allowing for weighted results to be truly reflective of all businesses.

- Monthly gross domestic product (GDP) publications are available.

- Net balances have been calculated by subtracting the weighted by turnover number of businesses who have reported a decrease in turnover from the weighted by turnover number of businesses with an increase in turnover, all divided by the total weighted number of businesses currently trading for that wave.

Download this image Figure 6: Fortnightly turnover estimates from Business Impact of Coronavirus Survey broadly reflect the published UK monthly gross domestic product estimates

.png (494.4 kB) .xlsx (26.7 kB){kind=link}

6. Business resilience

For presentational purposes, in Figure 7, cash reserve categories between zero and three months have been combined. The breakdowns of these categories are available in the accompanying dataset.

Figure 7: The accommodation and food service activities industry had the highest percentage of businesses with no cash reserves, at 6%, compared with 3% across all industries

Cash reserves, businesses that have not permanently stopped trading, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey; businesses that have not permanently stopped trading.

- Bars may not sum to 100% because of rounding and percentages less than 1% being removed for disclosure purposes.

- Other services and Mining and quarrying have been removed for presentational purposes, but their totals are included in “All Industries”.

- Businesses were asked for their experiences for the reference period 5 to 18 October 2020. However, for questions regarding cash reserves, businesses may respond from the point of completion of the questionnaire (19 October to 1 November 2020).

Download this chart Figure 7: The accommodation and food service activities industry had the highest percentage of businesses with no cash reserves, at 6%, compared with 3% across all industries

Image .csv .xlsAcross all industries, of businesses not permanently stopped trading:

3% had no cash reserves

24% had less than three months' cash reserves

18% had between four and six months' cash reserves

34% had more than six months' cash reserves

The accommodation and food service activities industry had the highest percentage of businesses that had no cash reserves, at 6%. This was followed by the arts, entertainment and recreation industry and the transportation and storage industry, at 5% and 4% respectively.

Conversely, the education industry (private sector and higher education businesses only) and the information and communication industry had the highest percentages of businesses that had cash reserves to last more than six months, at 47% and 44% respectively.

In Wave 16, businesses that had not permanently stopped trading were also asked how much confidence they had that they would survive the next three months (Figure 8).

Figure 8: The accommodation and food service activities industry had the highest percentage of businesses with no or low confidence that their businesses would survive the next three months, at 32%

Confidence, businesses who have not permanently stopped trading, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey; businesses that have not permanently stopped trading.

- Bars may not sum to 100% because of rounding and percentages less than 1% being removed for disclosure purposes.

- Other services and Mining and quarrying have been removed for presentational purposes, but their totals are included in “All Industries”.

- Businesses were asked for their experiences for the references period 5 to 18 October 2020. However, for questions regarding confidence, businesses may respond from the point of completion of the questionnaire (19 October to 1 November 2020).

Download this chart Figure 8: The accommodation and food service activities industry had the highest percentage of businesses with no or low confidence that their businesses would survive the next three months, at 32%

Image .csv .xlsAcross all industries, of businesses not permanently stopped trading:

11% had no or low confidence that their business would survive the next three months

38% had moderate confidence that their business would survive the next three months

44% had high confidence that their business would survive the next three months

The accommodation and food service activities industry and the manufacturing industry had the highest percentages of businesses that had no or low confidence that their business would survive the next three months, at 32% and 16% respectively.

Conversely, the real estate activities industry and the professional, scientific and technical activities industry had the highest percentages of businesses that had high confidence that their business would survive the next three months, at 58% and 52% respectively.

Nôl i'r tabl cynnwys7. Workforce

Surveyed businesses that have not permanently stopped trading will have differing approaches to the management of employees, whether furloughing staff, working as normal or other scenarios. Because of the complex nature of this, the data in this section primarily focus on proportions of the workforce within responding businesses as opposed to proportion of businesses as is the case for other sections.

The workforce proportions are based on the responses provided by businesses. These are then apportioned to derive proportions of employees in those businesses using the employment recorded for each reporting unit on the Inter-Departmental Business Register (IDBR).

These data were collected over the period 19 October to 1 November 2020 and refer to the period 5 to 18 October 2020. This means these data are from before the announcement of the extension of the UK government's Coronavirus Job Retention Scheme (CJRS) on Saturday, which was due to come to an end on 31 October 2020.

Figure 9: The arts, entertainment and recreation industry had the highest proportion of its workforce on partial or full furlough leave, at 27%, compared with 8% across all industries

Working arrangements, businesses that have not permanently stopped trading, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey; businesses that have not permanently stopped trading.

- Bars may not sum to 100% because of rounding, percentages less than 1% being removed for disclosure purposes, and those off sick or in self-isolation because of coronavirus (COVID-19), permanently made redundant or "Other" have being removed.

- Other services and Mining and quarrying have been removed for presentational purposes, but their totals are included in “All Industries”.

- Businesses were asked for their experiences for the reference period 5 to 18 October 2020. However, for questions regarding the last two weeks, businesses may respond from the point of completion of the questionnaire (19 October to 1 November 2020).

Download this chart Figure 9: The arts, entertainment and recreation industry had the highest proportion of its workforce on partial or full furlough leave, at 27%, compared with 8% across all industries

Image .csv .xlsAcross all industries, of businesses not permanently stopped trading:

8% of the workforce were on partial or full furlough leave

27% of the workforce were working remotely instead of at their normal place of work

62% of the workforce were working at their normal place of work

The arts, entertainment and recreation industry and the accommodation and food service activities industry had the highest proportions of their workforce on partial or full furlough leave under the terms of the UK government's Coronavirus Job Retention Scheme (CJRS), at 27% and 18% respectively (Figure 9).

The information and communication industry and the professional, scientific and technical activities industry had the highest proportions of their workforce working remotely instead of at their normal place of work, at 72% and 65% respectively.

For a more detailed outline of "Other" working arrangements across waves, please see the Coronavirus and the experiences of UK businesses, textual analysis: March 2020 to July 2020 article, which outlines how these "Other" working arrangements have changed over Waves 2 to 9.

Figure 10 shows the trend in unweighted furlough estimates between Wave 2 (23 March to 5 April 2020) and Wave 6 (18 to 31 May 2020) and weighted furlough estimates between Wave 7 (1 to 14 June 2020) and Wave 16 (5 to 18 October 2020).

Figure 10: Furlough estimates from Wave 2 (23 March to 5 April 2020) to Wave 16 (5 to 18 October 2020)

Working arrangements, businesses that have not permanently stopped trading, broken down by wave, UK, 23 March to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final unweighted results, Wave 2 to Wave 6, and final weighted results, Wave 7 to Wave 16, of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey (BICS).

- Weighted data are available from Wave 7 onwards only. The sample redesign in Wave 7 improves our coverage for the small sized businesses, allowing for weighted results to be truly reflective of all businesses.

- Businesses were asked for their experiences for the reference period. However, for questions regarding the last two weeks, businesses may respond from the point of completion of the questionnaire.

Download this chart Figure 10: Furlough estimates from Wave 2 (23 March to 5 April 2020) to Wave 16 (5 to 18 October 2020)

Image .csv .xlsIn Wave 7 (1 to 14 June 2020), 30% of the workforce were on furlough leave. The proportion of the workforce on furlough has progressively dropped until Wave 14 (7 to 20 September 2020), when the trend began to flatten.

For an overview of the similarities and differences between the fortnightly Business Impact of Coronavirus (COVID-19) Survey (BICS) furlough estimates and HM Revenue and Customs' (HMRC's) CJRS data, over the period 1 May to 31 July, please see Comparison of furloughed jobs data: May to July 2020.

Figure 11: Across all industries, 17% of the workforce that were still on furlough leave returned to work in the last two weeks

Proportions of the workforce who have returned to work in the last two weeks, businesses currently trading, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey (BICS); businesses currently trading.

- Industries may not sum to 100% because of rounding, percentages less than 1% being removed for disclosure purposes, and businesses do not have to report workforce proportions that sum to 100%.

- Other services and Mining and quarrying have been removed for presentational purposes, but their totals are included in “All Industries”.

- Businesses were asked for their experiences for the reference period 5 to 18 October 2020. However, for questions regarding the last two weeks, businesses may respond from the point of completion of the questionnaire (19 October to 1 November 2020).

Download this chart Figure 11: Across all industries, 17% of the workforce that were still on furlough leave returned to work in the last two weeks

Image .csv .xlsWhen interpreting the proportion of the workforce estimates returning from furlough leave or from remote working in the last two weeks, consideration of the industries that had a higher proportion of their workforce furloughed is needed.

Across all industries, of businesses currently trading:

11% of the workforce returned from furlough leave to the normal place in the last two weeks

6% of the workforce returned from furlough leave to homeworking in the last two weeks

5% of the workforce moved from remote working to the normal workplace in the last two weeks

11% of the workforce moved from the normal workplace to homeworking in the last two weeks

8. Homeworking

In Wave 16, businesses who had not permanently stopped trading were asked a series of questions about their workforce and homeworking.

Figure 12: Of businesses not permanently stopped trading, 26% had more staff working from home as a result of the coronavirus (COVID-19) pandemic

Staff working from home, businesses who have not permanently stopped trading, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey; businesses not permanently stopped trading.

- Bars may not sum to 100% because of rounding and percentages less than 1% being removed for disclosure purposes.

- Other services, Mining and quarrying, and Water supply, sewerage, waste management and remediation activities have been removed for presentational purposes, but their totals are included in “All Industries”.

Download this chart Figure 12: Of businesses not permanently stopped trading, 26% had more staff working from home as a result of the coronavirus (COVID-19) pandemic

Image .csv .xlsAcross all industries, of businesses not permanently stopped trading:

26% had more staff working from home as a result of the coronavirus (COVID-19) pandemic

70% did not have more staff working from home as a result of the coronavirus pandemic

The professional, scientific and technical activities industry and the information and communication industry had the highest percentages of businesses who had more staff working from home as a result of the coronavirus pandemic, at 44% and 40% respectively.

Conversely, the transportation and storage industry, the accommodation and food service activities industry, and the human health and social work activities industry (private sector businesses only) had the highest percentages of businesses who did not have more staff working from home, all at 89%.

Figure 13: Of businesses not permanently stopped trading and had more staff working from home, 14% experienced an increase in productivity while 19% experienced a decrease

Levels of productivity, businesses who have not permanently stopped trading and who had more staff working from home, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey; businesses not permanently stopped trading and who reported more staff working from home.

- Bars may not sum to 100% because of rounding and percentages less than 1% being removed for disclosure purposes.

- Other services, Mining and quarrying, and Water supply, sewerage, waste management and remediation activities have been removed for presentational purposes, but their totals are included in “All Industries”.

Download this chart Figure 13: Of businesses not permanently stopped trading and had more staff working from home, 14% experienced an increase in productivity while 19% experienced a decrease

Image .csv .xlsAcross all industries, of businesses not permanently stopped trading and who reported more staff working from home:

14% experienced an increase in productivity

57% experienced no impact on productivity

19% experienced a decrease in productivity

The transportation and storage industry had the highest percentage of businesses experiencing a decrease in productivity because of having more staff working from home, at 63%. This was followed by the accommodation and food service activities industry and the real estate activities industry, at 56% and 44% respectively (Figure 13).

This self-reported measure of productivity differs from our leading measures of productivity – Labour and multi-factor productivity measures, UK: April to June 2020. These leading measures of productivity are calculated using gross value added and various measures of labour input. They provide the degree of change in productivity from quarter to quarter, as opposed to the previously described estimates, which measure the number of businesses that have self-reported changes in productivity since homeworking levels increased.

Figure 14: Of businesses not permanently stopped trading, 17% intend to use increased homeworking as a permanent business model in future

Intentions for staff working from home, businesses who have not permanently stopped trading, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey; businesses not permanently stopped trading.

- Bars may not sum to 100% because of rounding and percentages less than 1% being removed for disclosure purposes.

- Other services, Mining and quarrying, and Water supply, sewerage, waste management and remediation activities have been removed for presentational purposes, but their totals are included in “All industries”.

Download this chart Figure 14: Of businesses not permanently stopped trading, 17% intend to use increased homeworking as a permanent business model in future

Image .csv .xlsAcross all industries, of businesses not permanently stopped trading:

17% intend to use increased homeworking as a permanent business model in the future

65% do not intend to use increased homeworking as a permanent business model in the future (Figure 14)

Of businesses intending to use increased homeworking as a permanent business model in the future, 64% reported it was because of reduced overheads, 61% reported it was because of improved staff well-being, and 40% reported it was because of increased productivity.

Of businesses not intending to use increased homeworking as a permanent business model in the future, 91% reported it was because it was not suitable for their business, and 7% reported it was because it had reduced communication and reduced productivity.

Other effects on the workforce and industry breakdowns are available in the accompanying dataset.

Nôl i'r tabl cynnwys9. Government schemes

Data regarding the percentages of businesses applying for and receiving the different government schemes and initiatives (including the Coronavirus Job Retention Scheme (CJRS)) can be found in the accompanying dataset.

Nôl i'r tabl cynnwys10. Site closures

In Wave 16, businesses that had not permanently stopped trading were asked if they intended to permanently close any of their business sites in the next three months.

These data were collected over the period 19 October to 1 November 2020 and refer to the period 5 to 18 October 2020. This should be kept in mind in relation to local and national lockdowns and dependent on the location and date when the business responded this could impact on the estimates.

Of businesses not permanently stopped trading, 2% intend to permanently close a business site in the next three months.

The arts, entertainment and recreation industry had the highest percentage of businesses intending to permanently close a business site in the next three months, at 4%. This was followed by the professional, scientific and technical activities industry, the construction industry, and the information and communication industry, all at 3%. A full industry breakdown is available in the accompanying dataset.

Of businesses that intend to permanently close a business site in the next three months, 35% intend to close a business site in the South East of England, 26% in the North West of England, and 18% in Wales (Table 2).

| Region | % of businesses that intend to permanently close business sites in the next three months |

|---|---|

| Northern Ireland | * |

| Scotland | 3.1% |

| Wales | 18.4% |

| East of England | 9.8% |

| East Midlands | 13.7% |

| Greater London | 16.0% |

| North East of England | 6.9% |

| North West of England | 25.7% |

| South East of England | 35.2% |

| South West of England | 16.9% |

| West Midlands | 9.1% |

| Yorkshire and The Humber | 8.6% |

Download this table Table 2: Locations of intended site closures, businesses that have not permanently stopped trading and who intend to permanently close a business site in the next three months, weighted, UK, 5 to 18 October 2020

.xls .csv

Figure 15: Across all industries, of businesses who intend to permanently close a business site in the next three months, 61% expect this to affect their workforce through permanent redundancies

Expected impact on workforce, businesses that have not permanently stopped trading and who intend to permanently close a business site in the next three months, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey (BICS); businesses that have not permanently stopped trading and who intend to permanently close a business site in the next three months.

- Bars may not sum to 100% because of rounding, percentages less than 1% being removed for disclosure purposes, businesses could select more than one option, and 'Other', Not sure and No effect being removed.

- Other services, Mining and quarrying, and Water supply, sewerage, waste management and remediation activities have been removed for presentational purposes, but their totals are included in “All Industries”.

- Businesses were asked for their experiences for the reference period 5 to 18 October 2020. However, for questions regarding business site closures, businesses may respond from the point of completion of the questionnaire (19 October to 1 November 2020).

- Caution should be taken when interpreting these results based on the specific routing of this question meaning that only a small number of businesses responded.

Download this chart Figure 15: Across all industries, of businesses who intend to permanently close a business site in the next three months, 61% expect this to affect their workforce through permanent redundancies

Image .csv .xlsAcross all industries, of businesses not permanently stopped trading and who intend to permanently close a business site in the next three months:

61% expect it to affect the workforce through permanent redundancies

18% expect it to affect the workforce through relocations

10% expect it to affect the workforce by moving them to remote working

7% expect it to affect the workforce through decreased hours

11% expect it will not affect the workforce

The arts, entertainment and recreation industry and the wholesale and retail trade industry had the highest percentages of businesses expecting the workforce to be affected through permanent redundancies, both at 96%. This was closely followed by the accommodation and food service activities industry, at 95% (Figure 15).

Nôl i'r tabl cynnwys11. EU and non-EU workers

In Wave 16, businesses that had not permanently stopped trading were asked how the number of workers from within and outside the European Union (EU) at their business had changed.

Figure 16: Across all industries, 1% of businesses had an increased number of workers from within the EU and 7% had a decreased number

Workers from within the EU, businesses that have not permanently stopped trading, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey (BICS); businesses that have not permanently stopped trading.

- Other services and Mining and quarrying have been removed for presentational purposes, but their totals are included in “All Industries”.

- Please note the Business Impact of Coronavirus (COVID-19) Survey only collects data from private sector businesses.

- Percentages less than 1% have been removed for disclosure purposes.

Download this chart Figure 16: Across all industries, 1% of businesses had an increased number of workers from within the EU and 7% had a decreased number

Image .csv .xlsAcross all industries, of businesses not permanently stopped trading:

1% had an increased number of workers from within the EU

7% had a decreased number of workers from within the EU

The majority of businesses had the same number of workers from within the EU, at 61%, with an additional 28% not sure how the number of workers from within the EU at their business had changed and 3% preferring not to say.

The water supply, sewerage, waste management and remediation activities industry and the information and communication industry had the highest percentages of businesses with an increased number of workers from within the EU, both at 3%.

Conversely, the accommodation and food service activities industry and the administrative and support service activities industry had the highest percentages of businesses with a decreased number of workers from within the EU, at 13% and 12% respectively.

Figure 17: Across all industries, less than 1% of businesses had an increased number of workers from outside the EU and 3% had a decreased number

Workers from outside the EU, businesses that have not permanently stopped trading, broken down by industry, weighted, UK, 5 to 18 October 2020

Source: Office for National Statistics – Business Impact of Coronavirus (COVID-19) Survey

Notes:

- Final weighted results, Wave 16 of the Office for National Statistics (ONS) Business Impact of Coronavirus (COVID-19) Survey (BICS); businesses that have not permanently stopped trading.

- Other services and Mining and quarrying have been removed for presentational purposes, but their totals are included in “All industries”.

- Please note the Business Impact of Coronavirus (COVID-19) Survey only collects data from private sector businesses.

- Percentages less than 1% have been removed for disclosure purposes.

Download this chart Figure 17: Across all industries, less than 1% of businesses had an increased number of workers from outside the EU and 3% had a decreased number

Image .csv .xlsAcross all industries, of businesses not permanently stopped trading:

less than 1% had an increased number of workers from outside the EU

3% had a decreased number of workers from outside the EU

The majority of businesses had the same number of workers from outside the EU, at 61%, with an additional 32% not sure how the number of workers from within the EU at their business had changed and 4% preferring not to say.

The human health and social work activities industry (private sector businesses only), the information and communication industry and the education industry (private sector and higher education businesses only) had the highest percentages of businesses with an increased number of workers from outside the EU, all at 2%.

Conversely, the accommodation and food service activities industry and the administrative and support service activities industry had the highest percentages of businesses with a decreased number of workers from outside the EU, at 8% and 6% respectively.

Across all industries, businesses reported a greater decrease in number of workers from the EU (6% net decrease) compared with the number of workers from outside the EU (2% net decrease). The information and communication industry was the only industry that reported net positive increases in the number of workers from within and outside the EU, at 1% each. Conversely, the accommodation and food service activities industry and the administrative and support service activities industry reported the highest net losses of the number of workers from the EU (negative 12% and negative 10%, respectively) and from outside the EU (negative 7% and negative 5%, respectively).

Nôl i'r tabl cynnwys13. Glossary

Coronavirus

Coronaviruses are a family of viruses that cause disease in people and animals. They can cause the common cold or more severe diseases, such as COVID-19.

COVID-19

COVID-19 is the name used to refer to the disease caused by the SARS CoV-2 virus, which is a type of coronavirus. The Office for National Statistics (ONS) takes COVID-19 to mean presence of SARS-CoV-2 with or without symptoms.

Furlough

Furlough is a temporary absence from work allowing workers to keep their job while the coronavirus (COVID-19) pandemic continues.

Reporting unit

The business unit to which questionnaires are sent is called the reporting unit. The response from the reporting unit can cover the enterprise as a whole or parts of the enterprise identified by lists of local units.

Nôl i'r tabl cynnwys14. Measuring the data

The Business Impact of Coronavirus (COVID-19) Survey (BICS) is voluntary and may only reflect the characteristics of those that responded; the results are experimental.

| Wave | 8 October 2020 Publication Wave 14 | 22 October 2020 Publication Wave 15 | 5 November 2020 Publication Wave 16 |

|---|---|---|---|

| Sample | 23,912 | 24,353 | 24,315 |

| Response | 5,522 | 5,970 | 5,755 |

| Rate | 23.1% | 24.5% | 23.7% |

Download this table Table 3: Sample and response rates for Waves 14, 15 and 16 of Business Impact of Coronavirus (COVID-19) Survey

.xls .csvThe business indicators are based on responses from the voluntary, fortnightly BICS, which captures businesses' views on the impact on turnover, workforce, prices, trade and business resilience. Wave 16 data relate to the period 5 to 18 October 2020. The survey questions are available.

The different experiences of businesses during the coronavirus pandemic

In the final results of Wave 16, of 24,315 businesses surveyed, 5,755 businesses (23.7%) responded.

The Wave 16 survey was live for the period 19 October to 1 November 2020, and businesses were asked about their experience for the two-week survey reference period, 5 to 18 October 2020. Dependent on responses to certain questions, businesses are asked different questions.

For questions or response options referring to the "last two weeks" or expectations of the "next two weeks", businesses could respond from the point of completion of the questionnaire based on their current experiences. This means that businesses' responses may cover any two-week time period across the following reference periods respectively: 5 to 18 October 2020 and 19 October to 1 November 2020. More detail on the type of questions asked are available in the accompanying dataset.

Weighting

Weighted estimates for the BICS have now been developed for all variables that are collected at a UK level. A detailed description of the weighting methodology and its differences to unweighted estimates is available in Business Impact of Coronavirus (COVID-19) Survey (BICS): preliminary weighted results.

We currently do not produce country or regional breakdowns on a weighted basis. Work is ongoing to enable this and hope to include these for future waves of BICS outputs. Our aim is to produce subnational weighted estimates should the sample and response allow. We currently provide unweighted estimates with a country and regional split for selected variables in our detailed dataset. These should be treated with caution when used to evaluate the impact of the coronavirus pandemic across the UK. When unweighted, each business is assigned the same weight regardless of turnover, size or industry, and businesses that have not responded to the survey or that are not sampled are not taken into account.

Weighted estimates for Scotland for businesses with greater than nine employees are available from the Scottish Government.

Coverage

The approach for the sample design has been to use three standard Office for National Statistics (ONS) surveys -- the Monthly Business Survey (MBS), Retail Sales Inquiry (RSI) and Construction -- as a sampling frame. Each of these survey samples are drawn from the Inter-Departmental Business Register (IDBR), which covers businesses in all parts of the economy, except those that are not registered for Value Added Tax (VAT) or Pay As You Earn (PAYE); this includes very small businesses, the self-employed, those without employees and those with low turnover. Some non-profit-making organisations are also not registered on the IDBR.

The MBS covers the UK for production and only Great Britain for services. The RSI and Construction are Great Britain-focused. Therefore, BICS will be UK for production-based industries but Great Britain for the other elements of the economy covered.

The industries covered are:

non-financial services (includes professional, scientific, communication, administrative, transport, accommodation and food, private health and education, and entertainment services)

distribution (includes retail, wholesale and motor trades)

production (includes manufacturing, oil and gas extraction, energy generation and supply, and water and waste management)

construction (includes civil engineering, housebuilding, property development and specialised construction trades such as plumbers, electricians and plasterers)

The following industries are excluded from the survey:

agriculture

public administration and defence

public provision of education and health

finance and insurance

Reporting unit

The business unit to which questionnaires are sent is called the reporting unit. The response from the reporting unit can cover the enterprise as a whole or parts of the enterprise identified by lists of local units. Other than for a minority of larger business or businesses that have a more complex structure, the reporting unit is the same as the enterprise.

Where more than one type of economic activity is carried out by a local unit or enterprise, its principal activity is the activity in which most of the people are employed, and it does not necessarily account for 50% or more of the total employment of the unit. There are detailed rules for determining Standard Industrial Classification (SIC) for multiple-activity economic units.

Regional estimates

Regional BICS estimates are produced by taking the survey return from each reporting unit and then applying this to the reporting unit's local sites. If a business has a site or several sites (also known as local units) within a country, using information from the IDBR, then this business is defined to have presence there.

The business is then allocated once within each region (regardless of the number of sites) and the information provided by the reporting unit as a whole is copied and used within each country.

Aggregates of Nomenclature of Territorial Units for Statistics (NUTS1) regions such as the UK or England may have higher or lower response proportions than any of their constituent regions because of differences in the sample composition in terms of company workforce.

Since the larger, aggregate regions such as the UK or England generally have a larger proportion of smaller companies, if there is a substantial difference between the response proportions of larger and smaller companies, this will be reflected in the top-line figures.

Sample

For unweighted data only, the businesses that have responded to Wave 16 of BICS are represented, and as such these are not fully representative of the UK as a whole.

The sampling frame used in BICS was designed to achieve adequate coverage of the listed industries from the MBS. Coverage and response rate of the medium to largest businesses in terms of total employment are satisfactory to produce estimates on this basis.

To help interpret the data, we have presented results based on the number of employees in each business, grouping fewer than 250 employees and those with 250 employees or more.

All businesses with an employment of greater than 250 employees and that are included within the three monthly surveys (MBS, RSI and Construction) are included in the BICS sample with a random sample of 1% for those with an employment between 0 and 249.

As the sample is selected fortnightly, the same businesses will be selected for at least two waves depending on how many coronavirus survey selections there are between the selection of these feeder surveys. Because of the randomly selected element, there will be differences in this part of the sample once the feeder surveys have been redrawn. As this is a voluntary survey, businesses may or may not choose to respond to the different waves. Response coverage can be mixed between the different waves.

While we have the ability to align the reporting unit to lower-level detail, and also increased detail on the SIC, it is not advisable given the sparseness of response in certain industries and size bands.

Nôl i'r tabl cynnwys15. Strengths and limitations

Business Impact of Coronavirus (COVID-19) Survey

The Business Impact of Coronavirus (COVID-19) Survey (BICS) is voluntary. Unweighted estimates should be treated with caution, as results reflect the characteristics of those that responded and not necessarily the wider business population.

The survey was designed to give an indication of the impact of the coronavirus pandemic on businesses and a timelier estimate than other surveys.

Comparison of waves

A detailed description of the weighting methodology and its differences to unweighted estimates across waves can be found in BICS: preliminary weighted results.

The production of weighted BICS estimates will allow for comparisons between waves, as any imbalances caused by non-responding and non-sampled businesses are corrected. This means that weighted estimates in every wave represent the experiences of all businesses rather than just those that have responded.

Some BICS variables remain unweighted while development continues to weight all the BICS variables. Therefore, comparison of unweighted estimates between waves should still be treated with caution because of the voluntary nature of the survey, the difference in response rates and dependency on those businesses that only responded in particular waves.

For a time series analysis on how the unweighted estimates changed between Wave 2 (23 March to 5 April 2020) and Wave 7 (1 to 14 June 2020), please see Insights of BICS: 23 March to 5 April (Wave 2) to 1 to 14 June (Wave 7) 2020.

Nôl i'r tabl cynnwys